BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

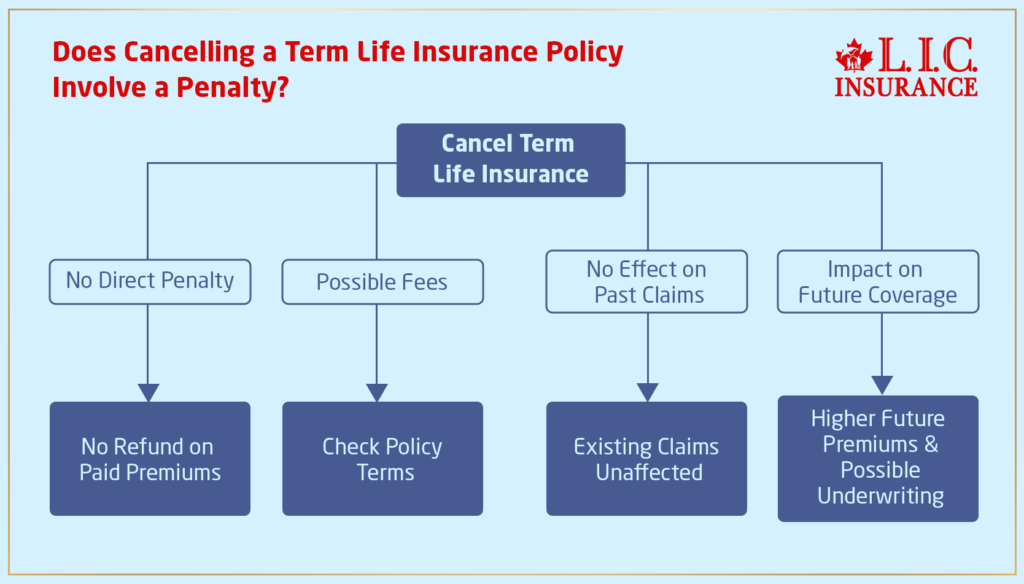

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

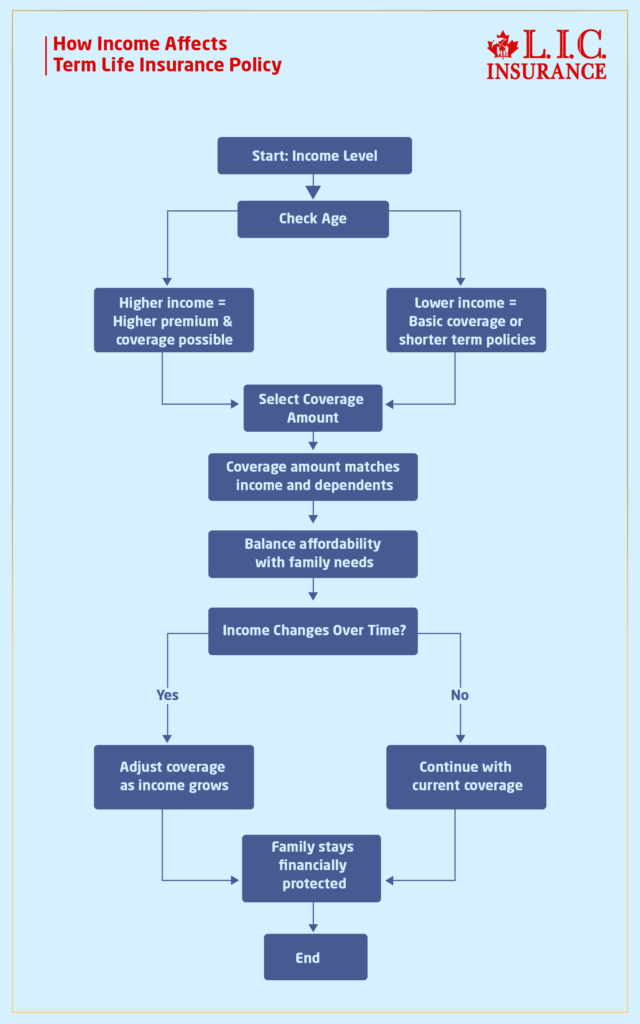

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Life Insurance Death Benefits in Canada: How They Work, Who Gets Paid, and Tax Rules Explained

By Harpreet Puri

CEO & Founder

- 12 min read

- May 13th, 2026

SUMMARY

Life Insurance death benefits in Canada can protect families from financial disruption when structured properly. The content explains how death benefits work, who receives the payout, tax treatment in Canada, estate and creditor implications, beneficiary rules, claim timelines, and common filing mistakes. It also covers business-owned policies, government regulations, funeral expense access, and how proper Life Insurance planning helps families preserve wealth and avoid unnecessary legal or tax complications.

Introduction

Life Insurance is one of the most depended financial safety measures in Canada, and still, it has been found that very little family knows how Life Insurance death benefits in Canada actually work when a death happens. The Canadian Life and Health Insurance Association reports that it insures more than 23 million Canadians in one way or another, though confusion over claim times has slowed a payout, caused tax anxiety, and put estates at risk of unwarranted creditors. Meanwhile, according to the statistics provided by Statistics Canada, the household debts per household have reached over 1.8 trillion, which is why the role of the well-organized benefits is more important than ever.

We do not regard death benefits as paperwork, but as the last financial advice a person leaves behind. Properly put together, they guard the family, save assets, and channel money within seconds. Being misunderstood, they bring legal tensions, tax anxieties, and conflicts that no bereaved family should have.

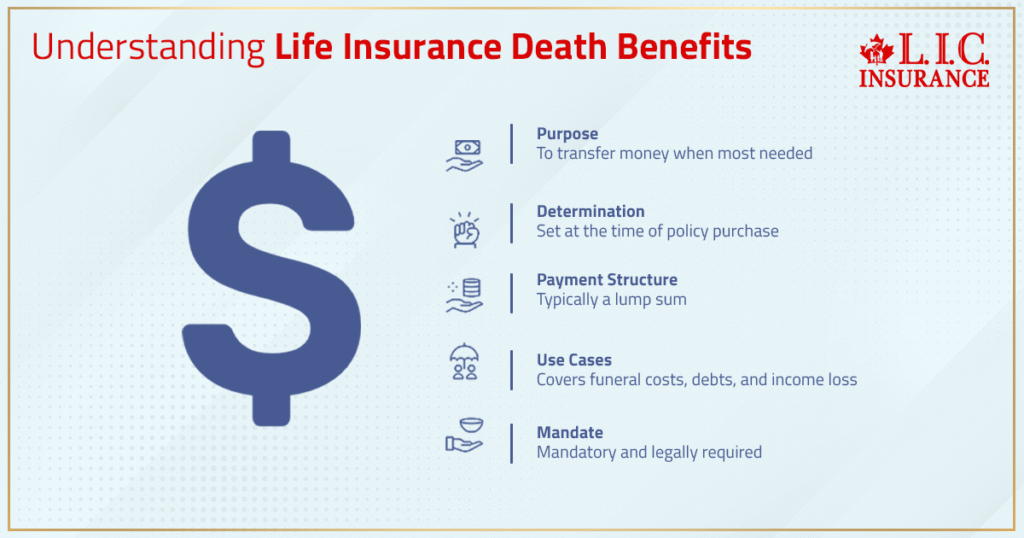

What Is A Life Insurance Death Benefit, And Why Does It Exist

Death Benefit

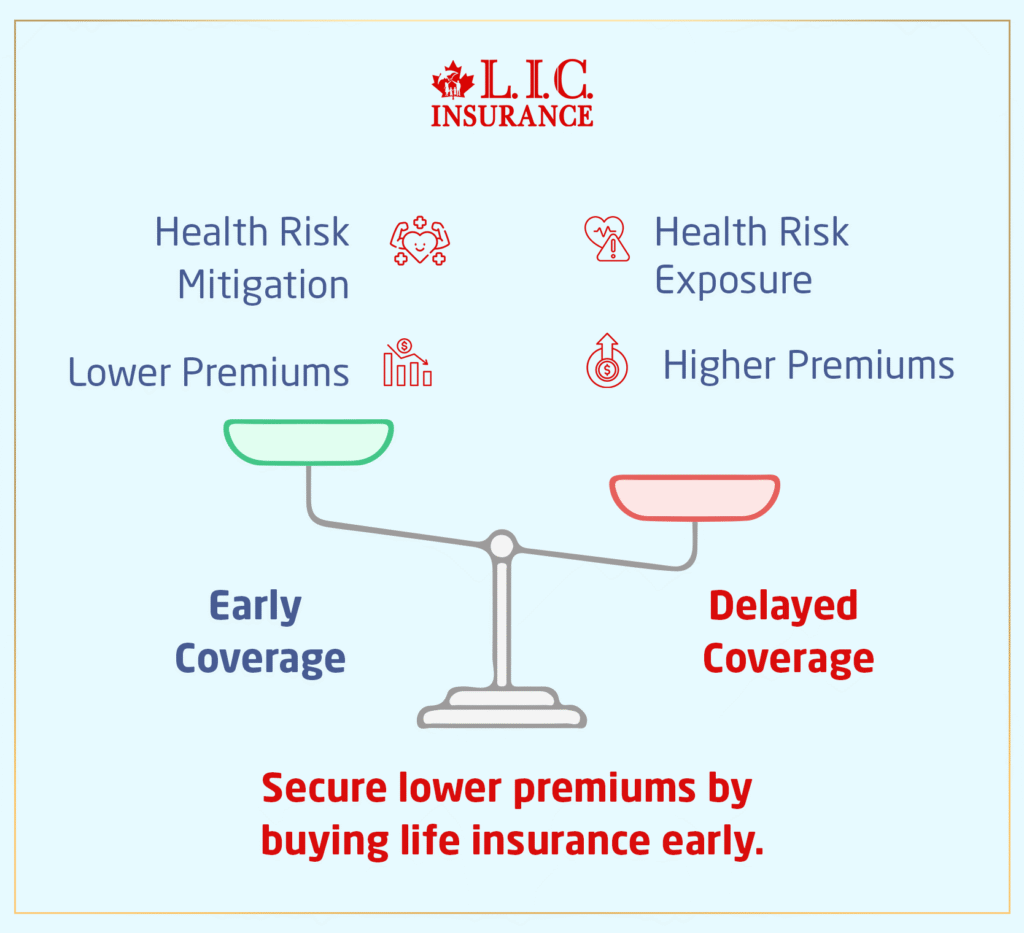

The payment made by the insurance company upon the death of the insured person is referred to as the death benefit. It is there with one purpose only, and that is to transfer money at the time when it is most required. This benefit of Life Insurance is determined at the time the Life Insurance is taken up and is payable so long as the Life Insurance Premiums in Canada are paid up.

With very few exceptions, the payment that benefits is a lump sum rather than a continuing income. The motive is urgent cash flow- to pay off funeral bills, compensation, lost income, debts, or secure property without selling off assets in order to do so. The cover is mandatory and not optional, and the insurer has a legal mandate to pay in case eligibility is established.

How Death Benefits Work In Real Canadian Claims

The procedural answer is yes when the clients enquire how death helps work; however, timing is the key. After a death has been experienced, the stipulated beneficiaries should then make a claim with the insurer. This is done by presenting a death certificate, policy details, and identification. The insurance company shall then evaluate the claim, determine that it is accurate, and verify the eligibility.

In our experience, most of the Canadian claims are settled in weeks, not months, in the case of clean documentation. The failure to obtain forms, vague designation of beneficiaries, or resolution of certain cases, such as disputed estates, are the major causes of delays. Upon approval, the payment is discharged by the insurer to the beneficiary, and the file is closed.

Who Gets Paid: Beneficiaries, Estate, And Priority Rules

Priority is the most misunderstood issue that we observe. In case a Life Insurance Policy has one or more beneficiaries, that payment will not pass through the estate. This implies that the money is not subject to probate, will not be consolidated with other holdings, but will be insulable to the majority of creditors.

A registered charity, a business partner, children, or a surviving spouse are some of the common beneficiaries. In isolated incidences, a relative can be appointed. In cases of no beneficiary, the death benefit shall be paid to the estate, where an actuary or an administrator shall administer distribution in accordance with provincial law, and failure to do so shall be regarded as unlawful: Government of Canada, 2015.

This difference is the only factor that will ensure that funds can come in a few weeks or will still be on ice months later.

When Death Benefits Become Part Of The Estate

A death benefit is exposed once it is sent into the estate. Liabilities such as outstanding loans, debts, and obligations to credit card companies, among others, should be entirely settled by the trustee or executor before proceeding with any other activities. The debt clearing is necessary, after which the rest of the money can be distributed.

This is where families are forced to lose unnecessarily. The liquid assets can be sold off, property might need to be refinanced, and the surviving spouse can be deprived of financial momentum at a bad time. Planning-wise, the estate routing avoidance is one of the best forms of protection of insurance design in Canada.

Are Life Insurance Death Benefits Taxable In Canada?

Income tax is one of the most widespread issues that we hear. The death benefit in Life Insurance is normally paid out in Canada as a tax-free lump sum to the named beneficiaries. They are neither counted as income, nor do they prompt taxes, nor do they create any personal tax liability on the beneficiary.

It is one of the reasons why Life Insurance is still a different category of investment vehicles as opposed to registered vehicles. The insurance payout is not subject to normal taxation frameworks and is not affected by the marginal tax rates when well organized.

How Death Benefits Affect A Tax Return

Even though the benefit is not taxable, some of the expenses incurred on the deceased have to be handled on the final tax return. These can be unpaid income, allowable deductions, or funeral expenses recorded. Death benefit is not to be included in the taxable income; however, the expenses related to the estate are to be filed.

This distinction matters. Combining insurance proceeds with estate income may lead to an error in reporting. We constantly recommend that families keep these streams distinct so as to eliminate redundant CRA scrutiny.

Role Of The Government Of Canada In Life Insurance Tax Rules

The Canada Revenue Agency and the overall federal government structure determine the tax treatment of Life Insurance proceeds. Other countries can charge death benefits in many ways, but Canada boasts one of the best in the world.

In normal cases, the government does not receive insurance proceeds, nor does it levy direct taxes on the recipient beneficiaries. Supervision is there only to make sure that there is compliance, not to collect.

What Happens If False Information Was Provided On The Policy

Misleading information in underwriting may invalidate a claim. Under the contestability period, the insurer is entitled by law to consider disclosures and ascertain material misrepresentation. In case the inaccuracies have a material impact on risk, the claim can be revised or rejected.

This is why accuracy matters. As an advisor, we would recommend transparency to guard families. We promote disclosure in the initial stages compared to correction in the later stages when it comes to clients being involved.

Life Insurance and Creditors: Who Can and Cannot Access the Money

Well-organized policies are safe against creditors. The death benefit is neither available as collateral when beneficiaries have been named, nor can a credit holder or any third-party entity claim the benefit. Lenders can be given preference, however, when they are collateralized on a mortgage or loan.

This difference underscores the importance of policy ownership, and beneficiary structure should be consistent with overall financial exposure.

Business-Owned Policies And Death Benefits

Death benefits promote continuity in a business. Policies can finance buy-sell deals, secure a surviving spouse, or stabilize income to dependents. Proceeds are not part of personal estates, and those that are structured properly are safe from corporate liabilities.

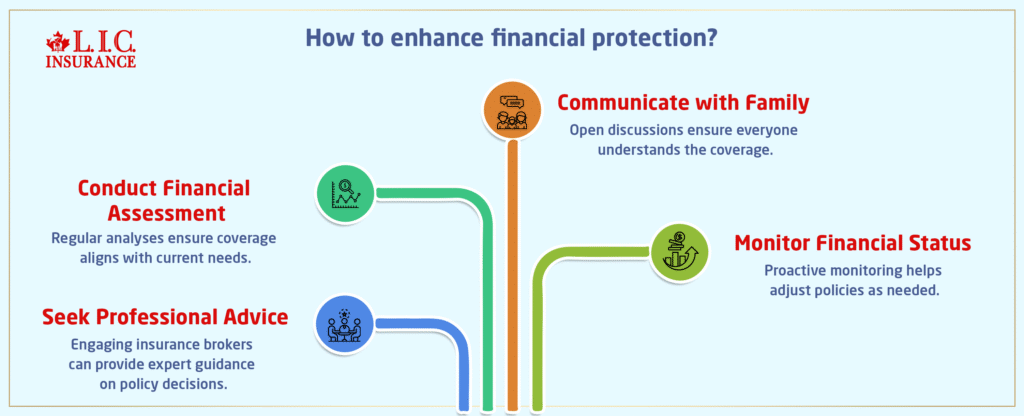

How Much Death Benefit Amount Is Enough?

It does not involve a simple calculation and thus has to be done comprehensively by taking into account income, fixed costs, future requirements, and current assets. Families will have to take into consideration residual debts, lifestyle needs, and long-term demands. We normally consider replacement income, settling debts, and legacy objectives as a unit.

Choosing The Best Life Insurance Policies In Canada

Optimal Life Insurance Policies are not universal but relative. The type of coverage, the type of premium, and the duration are important. The trick is matching the protection objectives with the affordability of the Life Insurance Premiums in Canada.

Getting A Life Insurance Quote Online Without Mistakes

A Life Insurance quote online is very easy to get through the internet, although it is very important to note that accuracy should be observed. Mistaken disclosures in the present may destroy assertions in the future. We request clients to question, call the advisors, and pose all the questions that drive the answers, and then commit.

Final Perspective From Canadian LIC

Death benefits have nothing to do with death; they have to do with control. The power to control the payment targets, the delivery of money, the exclusion of creditors, and the recovery by families. Life Insurance provides certainty when needed most, the time of the year when a person is at the unpredictable stage in life. It is that clarity we are assisting the Canadian families in acquiring, even before it is required.

FAQs

The answer to this is yes, a Life Insurance Policy has the ability to apportion that death benefit between a series of beneficiaries in terms of percentages. Such an arrangement assists in the management of priority, eliminates conflicts in the estate, and each individual is provided with the desired payment. The insurance company acts on the instructions on file. Accuracy matters.

The beneficiaries cannot be delayed in making a Life Insurance claim when the names have been designed correctly. The death benefit is paid out of the pocket by the insurer, and creditors are held off. Delays are normally due to documentation problems and not debts. Paperwork is clean, and this makes the process smooth.

Unpaid debts do not lessen Life Insurance death benefits when the estate is bypassed by the payouts. The money is sent straight to the beneficiaries, and it cannot be used on debts such as credit cards and loans. These problems only come about when the estate is the recipient.

Yes, the death benefit is frequently used by the beneficiaries to settle the funeral expenses without settling their estate. Being a single payment, it allows access quicker than other assets. This flow of money is instant and relieves tension when it comes to initial preparations. Timing matters here.

In most cases, a Life Insurance payment made tax-free is not considered income when calculating the benefits of the federal government. The insurance proceeds and earned income are treated differently by the Government of Canada. Nevertheless, possession of large assets in the future can influence future ratings. Context always matters.

Yes, it is allowed to name a charity as a beneficiary, and it is quite a common practice in estate planning. The death benefit goes to an organization of choice, eliminates estates, and no additional taxes are paid. It is also an efficient method of making the administration less complicated for the executor. Intent stays clear.

Obsolete beneficiary transactions may cause the death benefit to be included in the estate, altering priority and putting funds under the control of creditors. The insurer should act according to the law, which is on record, even though the situations may have transformed. Periodic reviews avoid unplanned results. Minor changes have a huge significance.

Yes, other nations tend to tax death benefits or include them in the estate. Canada is still a special place, having good tax regulations and protection of creditors. This difference is significant to cross-border families and policies. There should be the jurisdiction to plan.

In circumstances where false information is only discovered after the death, the claimant can be reviewed by the insurer during the review period. This may influence the time or eligibility for payment. The accuracy of the initial application will be passed on to the beneficiaries. Openness will safeguard all parties.

Yes, it is better to consult as soon as possible to prevent the beneficiaries from waiting, losing forms, or making mistakes in filing. The process of a Life Insurance claim does not seem difficult, and it includes legal and formal procedures. Guidance makes the payment flow in the right direction and in a fast manner. Support reduces friction.

Sources and Further Reading

Official Canadian Government & Tax Sources

🔗 Life Insurance Overview — Financial Consumer Agency of Canada (FCAC)

Explains what Life Insurance is, how the death benefit works, and typical uses like income replacement, funeral expenses, and debt payoff. Life Insurance – Government of Canada (FCAC)

🔗 Death Benefits & Tax Reporting Guidance — Canada Revenue Agency (CRA)

Official CRA guidance on how certain death benefit amounts (e.g., CPP/QPP death benefits) are reported and taxed. Death Benefits — CRA Tax Reporting Guidance

🔗 CRA Premiums & Taxable Benefits Chart

Details when Life Insurance or other benefit payments may or may not be taxable under CRA rules. Premiums & Contributions To Insurance Plans — CRA

🔗 Canadian Income Tax Rules (Wikipedia summary)

Overview of income categories not taxed in Canada, including Life Insurance death benefits. Income Tax In Canada — Wikipedia

Industry & Insurance Company Sources

🔗 What Is A Life Insurance Death Benefit — Canada Life

Defines death benefit, beneficiary roles, and how payouts work within Canadian insurance policies. What Is A Life Insurance Death Benefit? — Canada Life

🔗 Life Insurance Claim Process — OneDay Insurance

Explains in straightforward terms how the Life Insurance claim process works in Canada, including typical timelines and reasons for delay. How Life Insurance Claims Work In Canada

🔗 Life Insurance Payout Tax Rules — RBC Insurance

Shows when Life Insurance payouts are not taxable and how interest or dividends may affect tax reporting. Is A Life Insurance Payout Taxable? — RBC Insurance

🔗 Life Insurance Premium Deductibility & Tax — Blue Cross

Explains Canadian tax treatment of Life Insurance premiums and non-taxable payout status, helpful when discussing Life Insurance Premiums in Canada. Are Life Insurance Premiums Tax Deductible? — Blue Cross

Consumer Guides & Brochures

🔗 Complete Canadian Life Insurance Consumer Guide — CLHIA

Comprehensive guide Canadian consumers can use to understand types of coverage, beneficiaries, and planning. Guide To Life Insurance — CLHIA Brochure

Additional Contextual Reading

🔗 Taxes On Death Benefits — IBC Financial

Breaks down how death benefits are taxed (or not) and includes employer benefit context with exemption details. Taxes On Death Benefits — IBC Financial

🔗 Assuris Protection For Life Insurance Holders

Explains how policies, including death benefits, are protected if a Canadian insurer becomes insolvent. Assuris Life Insurance Protection Organization

Key Takeaways

- Life Insurance death benefits in Canada are designed for speed and certainty. When beneficiaries are named correctly, the payment moves outside the estate, reaches the right people faster, and avoids unnecessary legal friction.

- Beneficiary designations matter more than most people realize. A small oversight can reroute the death benefit into the estate, exposing money to creditors, delays, and administrative priority rules.

- Most Life Insurance death benefits are paid as a tax-free payment. They do not count as income for beneficiaries, which makes insurance a uniquely efficient financial tool compared to many other assets.

- The Life Insurance claim process is straightforward—but accuracy controls timing. Clean documentation and truthful disclosures allow the insurer to pay quickly, while gaps or false information slow everything down.

- Estate involvement changes everything. Once a death benefit becomes part of the estate, it may be used to settle debts, outstanding loans, and obligations to financial institutions before family receives anything.

- Creditors generally cannot access death benefits paid to named beneficiaries. Protection holds unless the policy was assigned as collateral or structured incorrectly.

- Funeral expenses are often the first practical use of the payout. The one-time payment provides immediate liquidity when other assets remain frozen.

- The Government of Canada tax rules strongly favour Life Insurance. Compared with other countries, Canada offers one of the most beneficiary-friendly environments for death benefit payments.

- Business and partnership planning rely heavily on an insurance structure. Proper ownership and beneficiary setup keep proceeds separate from personal estates and business liabilities.

- The right death benefit amount is about stability, not guesswork. It should reflect income replacement needs, existing debts, assets, and the financial reality of the people left behind.

- Online quotes are only as good as the information provided. Inaccurate inputs today can affect claim outcomes later—consulting before applying reduces long-term risk.

- Life Insurance is less about death and more about control. Control over who gets paid, when money arrives, what stays protected, and how a family moves forward.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- Life Insurance Death Benefits in Canada: How They Work, Who Gets Paid, and Tax Rules Explained

- What Is A Life Insurance Death Benefit, And Why Does It Exist

- How Death Benefits Work In Real Canadian Claims

- Who Gets Paid: Beneficiaries, Estate, And Priority Rules

- When Death Benefits Become Part Of The Estate

- Are Life Insurance Death Benefits Taxable In Canada?

- How Death Benefits Affect A Tax Return

- Role Of The Government Of Canada In Life Insurance Tax Rules

- What Happens If False Information Was Provided On The Policy

- Life Insurance and Creditors: Who Can and Cannot Access the Money

- Business-Owned Policies And Death Benefits

- How Much Death Benefit Amount Is Enough?

- Choosing The Best Life Insurance Policies In Canada

- Getting A Life Insurance Quote Online Without Mistakes

- Final Perspective From Canadian LIC