- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Whole Life Insurance For Seniors In Canada: Is It Worth It In 2026?

By Harpreet Puri

CEO & Founder

- 12 min read

- May 1st, 2026

SUMMARY

Whole Life Insurance for seniors in Canada is examined through premiums, tax-free death benefits, cash value growth, and Guaranteed Life Insurance Canada options. The discussion compares whole life, term Life Insurance, and universal Life Insurance, explains how Life Insurance Policies help cover funeral expenses, estate taxes, and final costs, and outlines when Permanent Life Insurance supports financial security and long-term planning in retirement.

Introduction

Aging does not imply that one puts all financial liabilities behind. Financial clarity is a pressing concern for most Canadians in retirement. Statistics Canada statistics suggest that close to 70% of those aged 65 and above still have some sort of debt, and the funeral costs in Canada have currently been classified as between 9,000 and 15,000 dollars, depending on the province and services specified. Meanwhile, medical bills, estate tax, and dying expenses are ever-increasing.

Another very real question that appears to seniors within our day-to-day experience at the Canadian LIC in 2026 is: Is Whole Life Insurance even worth it at this age? The question of how Life Insurance, Whole Life Insurance, and Permanent Insurance actually operate, rather than the manner in which they are being sold.

This manual simplifies it, based on actual Canadian statistics, actual planning rationality, and actual real-life results.

Permanent Life Insurance For Seniors: What Changes After Age 60

At age 60 and above, Permanent Life Insurance assumes a much different role in the lives of Canadians. Permanent Life Insurance among the elderly does not concentrate on replacement of income, as it was done in the past, but is about financial security, final expenses, and estate planning.

Upon retirement, the majority of Canadians do not require huge amounts of coverage. Children are free, work is no longer, and it is now life-long coverage, stability, and predictability. This is precisely what Permanent Life Insurance Policies are created to do; they do not expire like term policies, and may also be used to provide a lifetime cover, provided that premiums are paid.

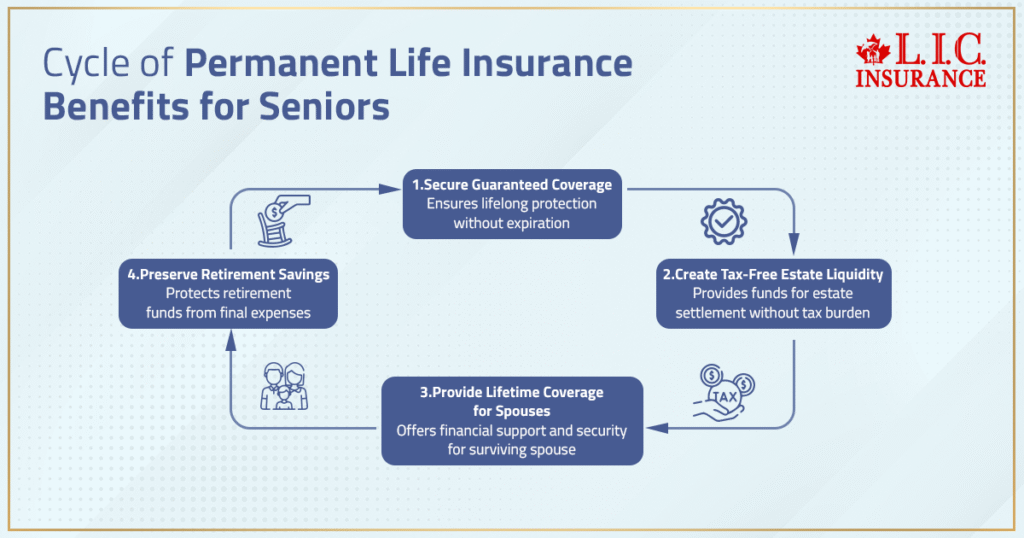

We consistently see seniors using Permanent Insurance to:

- Lock in guaranteed coverage

- Create tax-free estate liquidity

- Provide lifetime coverage for spouses

- Preserve retirement savings from being drained by the final cost.

Can You Get A Life Insurance Policy As A Senior In Canada?

Yes — and more options exist than most people realize.

A Life Insurance Policy can be issued well into your 70s and even early 80s, depending on the product. While coverage limits are smaller than those of younger-age policies, seniors still have access to meaningful insurance coverage.

Most senior policies range from $10,000 to $50,000, which aligns closely with real needs like:

- Funeral expenses

- Outstanding mortgage payments

- Final medical bills

- Estate taxes

When purchasing Life Insurance, the key question becomes how much Life Insurance is appropriate. We help clients assess how much coverage they actually need, based on debts, estate goals, and family circumstances — not guesswork.

Whole Life Insurance Explained: How It Works For Seniors

Whole Life Insurance is one of the most traditional forms of Permanent Life Insurance, sometimes referred to as entire life coverage. It offers three defining features that appeal strongly to seniors:

- Guaranteed death benefit

- Fixed monthly premiums

- A built-in cash value component

Whole life, as opposed to Term Life, has no expiry as it is lifelong. The premiums do not go up, and the death benefit is given irrespective of the date of death, provided the policy is still in place.

The entire Life Insurance is more expensive than the term cover, yet it provides certainty, which most seniors will find to be more important than flexibility.

Death Benefits Of Whole Life Insurance And Why They Matter

The death benefits of Whole Life Insurance are one of its strongest features. In Canada, the Life Insurance payout is generally tax-free, making it one of the most efficient ways to transfer wealth.

From our experience, seniors commonly use the death benefit to:

- Cover funeral expenses

- Pay off remaining mortgage payments

- Settle estate taxes

- Support a surviving spouse

Because the death benefit tax-free structure applies, families receive the full value without erosion from income tax, preserving dignity and financial stability during a difficult time.

Cash Value In Whole Life Policies: Understood Properly

The cash value component of Whole Life Insurance is often misunderstood. It grows slowly, conservatively, and tax-advantaged inside the policy.

We caution seniors not to treat cash value as an investment replacement. Instead, it acts as:

- A reserve

- A liquidity option

- A conservative financial buffer

For corporately held policies, cash values may also interact with the Capital Dividend Account, creating planning opportunities. While insurance companies’ profits do influence dividends in participating policies, guarantees remain contractually defined.

Guaranteed Life Insurance For Seniors Without A Medical Exam

Many seniors worry about health issues or health concerns preventing approval. This is where Guaranteed Life Insurance Canada becomes relevant.

These policies typically:

- Require no medical exam

- Offer smaller coverage amounts

- Include graded death benefits in early years

The best Whole Life Insurance without a medical exam is suitable for seniors with serious health challenges who still want coverage. However, we always evaluate whether a medically underwritten policy — even with a simplified medical exam — might offer better value.

Whole Life Vs. Term Life Insurance For Seniors

Term Life Insurance becomes increasingly expensive with age, and many Life Insurance companies restrict term availability past certain ages. For seniors, term life often:

- Expires before death

- Requires renewal at higher rates

- Offers no cash value

In contrast, Whole Life Insurance offers certainty. When comparing Life Insurance rates, seniors often find that smaller whole life policies provide better long-term value than short-term solutions that may lapse.

Whole Life Vs Universal Life Insurance In Retirement

Universal Life Insurance is flexible and creates risk. Although universal life policies offer flexibility when it comes to premiums and investment elements, they can be easily compromised by underperformance or inadequate funding.

Retirees who want certainty might not find a Universal Life Insurance Policy as appropriate as whole life. The term universal life is frequently prescribed at the Canadian LIC, but only in the case when the client is familiar with the mechanics and is ready to take care of the performance control.

What Does Whole Life Insurance Actually Cover For Seniors?

Whole Life Insurance is commonly used to:

- Cover funeral costs

- Handle final expenses

- Pay outstanding medical bills

- Protect estate assets

With funeral costs continuing to rise and healthcare expenses increasing in later years, having an insurance policy in place prevents families from selling assets under pressure.

What Affects Whole Life Insurance Premiums In Canada

Several factors determine insurance premiums, including:

- Age at issue

- Coverage amount

- Smoking status

- Overall health

While monthly premiums are higher than term insurance, they remain fixed for life, offering budgeting certainty — a major advantage for retirees.

Is Whole Life Insurance Affordable For Seniors In 2026?

Affordability depends on expectations. Seniors often prioritize affordable coverage over large payouts. Smaller policies with manageable premiums deliver peace of mind without financial strain.

We structure policies so coverage fits naturally into a broader financial plan, not as a burden.

When Whole Life Insurance Makes Sense — And When It Doesn’t

Whole Life Insurance makes sense when:

- Final expenses need funding

- Estate liquidity is required

- A surviving spouse needs protection

- Financial security matters more than growth

It may not be ideal for seniors who are already financially secure and have sufficient liquid assets earmarked for end-of-life costs.

The Role Of Canadian Life Insurance Companies In Senior Coverage

The Canadian Life Insurance market is very stable and regulated. The major insurers are still trading with senior products since there is still demand.

When an insurance advisor is a licensed individual, the choice of a policy is not based on general sales stories, but rather on what the individual really needs.

Key Takeaways: Life Insurance For Seniors In Canada

Whole Life Insurance is not concerned with income replacement in retirement. It is an issue of money, security, assurance, and pride. Whole Life Insurance for seniors in Canada can be seen as a viable, tax-efficient answer for many seniors in 2026, made strategically.

We just have to do this: to cover the reality and make sure that everything is understood and all clients are ready to enter into the next stage of financial activity.

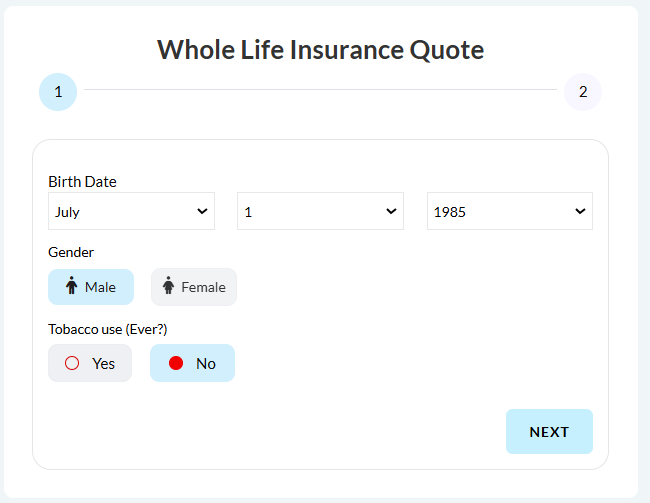

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Whole Life Insurance among the seniors in Canada can be used to ensure liquidity despite high savings, even in cases where the assets are market-linked or illiquid. Life Insurance guarantees an economic cushion that avoids forced sales of assets. A lot of seniors rely on a Life Insurance Policy in order to save in investment accounts. It does not substitute savings, it complements them.

A majority of the Guaranteed Life Insurance Canada policies have a graded period in which the entire death benefit is not paid. In the initial years of the plan, Life Insurance premiums can be returned with interest and paid out. Following the waiting period, there is a death benefit tax-free structure. The design of the policies differs depending on the insurance companies.

Whole life policy has flexibility with the option of surrendering cash, and there is also access to cash value. Lifetime coverage is cancelled by cancelling the coverage; therefore, the decision made must be in line with the long-term requirements of Life Insurance. There are reduced paid-up option policies. A qualified insurance consultant would be able to consider leaving options without risk.

Health issues will affect the eligibility, costs, and need for a medical examination. Older people with illnesses can get medical Life Insurance options or simplified underwriting. Guaranteed Life Insurance applies where underwriting will be restrictive. The amounts of coverage are modified to ensure that risk is addressed in a responsible manner.

In the case of retirees, the Whole Life Insurance focuses on the aspect of certainty, and the universal Life Insurance brings about the performance risk. The elderly who value the predictability of their insurance payment usually shun variable financing. There needs to be active management of a universal life policy. The appropriateness is not restricted to age but to risk tolerance.

Estate taxes will be funded using Life Insurance without depleting registered and taxable accounts. Life Insurance payout is liquidity at the right time. This safeguards the heirs against the sale of property and investments. The tax-free is much more efficient in terms of the estate.

Smaller policies are usually designed to take only the funeral expenses and final expenses. This makes the monthly premium affordable and fulfills actual commitments. A large percentage of the elderly demand specific, low-priced Life Insurance with excess coverage. Accuracy is greater than the size of the policy.

Yes, maximum issue ages and face amounts are established by Canadian Life Insurance companies. The limits are depictions of longevity risk and sustainability in the Canadian Life Insurance sector. Despite this, the meaningful Life Insurance cover is still available. The trick is to align the purpose with policy design.

Comparison of Term Life Insurance prevents doubts about temporary coverage. At later ages, term insurance becomes impractical due to the increasing costs of Life Insurance. Whole life offers lifetime coverage, but it is not renewable. Comparison is a guarantee of an informed buying of Life Insurance decisions.

Upon approval, a Whole Life Insurance Policy is guaranteed by a contract. There is no age or market-based increment in insurance premiums. Such stability is attractive to the elderly who want a stable financial investment. Guarantees are based on the policy payment maintenance.

Sources and Further Reading

Whole Life Insurance & Permanent Insurance (Canada)

- Canadian Life and Health Insurance Association (CLHIA)

https://www.clhia.ca/consumers/life-and-health-insurance/life-insurance - Financial Consumer Agency of Canada – Life Insurance Basics

https://www.canada.ca/en/financial-consumer-agency/services/insurance/life.html - Canada Revenue Agency – Life Insurance & Death Benefits

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/deductions-credits-expenses/other-deductions/line-23200-other-deductions/life-insurance.html

Whole Life vs Term vs Universal Life (Senior-Focused Education)

- Sun Life Canada – Whole Life Insurance Explained

https://www.sunlife.ca/en/insurance/life/whole-life-insurance/ - Manulife Canada – Permanent Life Insurance Overview

https://www.manulife.ca/personal/insurance/life-insurance/permanent-life-insurance.html - Canada Life – Universal Life Insurance Guide

https://www.canadalife.com/insurance/life-insurance/universal-life-insurance.html

Guaranteed Life Insurance & No Medical Exam Policies

- Desjardins Insurance – Guaranteed Life Insurance

https://www.desjardins.com/ca/personal/insurance/life/guaranteed-life-insurance/index.jsp - Empire Life – Life Insurance Without Medical Exam

https://www.empire.ca/individual-insurance/life-insurance/no-medical

Estate Planning, Taxes & Final Expenses

- Government of Canada – Estate Planning Basics

https://www.canada.ca/en/services/finance/pensions/retirement-planning.html - CRA – Capital Dividend Account (CDA)

https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/capital-dividend-account.html - Statistics Canada – Seniors, Debt & Household Finances

https://www.statcan.gc.ca/en/subjects-start/older_adults_and_population_aging

Insurance Regulation & Industry Oversight

- Office of the Superintendent of Financial Institutions (OSFI)

https://www.osfi-bsif.gc.ca - Canadian Institute of Actuaries (CIA)

https://www.cia-ica.ca

Key Takeaways

- Whole Life Insurance for seniors in Canada focuses on certainty, not growth, providing lifetime coverage that supports estate planning, funeral expenses, and financial security.

- Fixed Whole Life Insurance premiums eliminate renewal risk, making Permanent Life Insurance easier to manage as a retirement income.

- The death benefits of Whole Life Insurance are generally tax-free, helping families handle final expenses, estate taxes, and mortgage payments without asset liquidation.

- Guaranteed Life Insurance Canada expands access for seniors with health issues, even when a medical exam is not possible.

- Cash value within a Whole Life Insurance Policy should be viewed as a conservative reserve rather than an investment strategy.

- Compared with term Life Insurance and universal Life Insurance, whole life offers predictable coverage that does not depend on market performance or future insurability.

- Smaller, well-structured policies often deliver more affordable coverage and better alignment with real-life Insurance needs in retirement.

- Working with a licensed insurance advisor helps ensure the Life Insurance Policy fits long-term financial plans and protects surviving spouses effectively.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- Whole Life Insurance For Seniors In Canada: Is It Worth It In 2026?

- Permanent Life Insurance For Seniors: What Changes After Age 60

- Can You Get A Life Insurance Policy As A Senior In Canada?

- Whole Life Insurance Explained: How It Works For Seniors

- Death Benefits Of Whole Life Insurance And Why They Matter

- Cash Value In Whole Life Policies: Understood Properly

- Guaranteed Life Insurance For Seniors Without A Medical Exam

- Whole Life Vs. Term Life Insurance For Seniors

- Whole Life Vs Universal Life Insurance In Retirement

- What Does Whole Life Insurance Actually Cover For Seniors?

- What Affects Whole Life Insurance Premiums In Canada

- Is Whole Life Insurance Affordable For Seniors In 2026?

- When Whole Life Insurance Makes Sense — And When It Doesn’t

- The Role Of Canadian Life Insurance Companies In Senior Coverage

- Key Takeaways: Life Insurance For Seniors In Canada

Sign-in to CanadianLIC

Verify OTP