- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Universal Life Insurance Plan Vs Term Life Insurance Plan

By Pushpinder Puri

CEO & Founder

- 11 min read

- April 16th, 2025

SUMMARY

The blog compares the Universal Life Insurance Plan vs Term Life Insurance Plan in Canada. It explains their differences in cost, coverage, duration, investment value, and flexibility. It shares real client stories from Canadian LIC to highlight when each plan fits best. It also covers how to access Term Life Insurance Policy Quotes Online and Universal Life Insurance Policy quotes while breaking down the cost of a Universal Life Insurance Plan and the cost of a Term Life Insurance Plan clearly.

Introduction

Choosing Between Two Life Insurance Plans Isn’t Always Easy

Families, professionals, and business owners walk into our office every day with the same conundrum: “Universal Life Insurance Plan or Term Life Insurance Plan? The confusion is very real. Some have seen ads online for term life insurance policy quotes and figure it’s the easiest and cheapest route. Some learn about Universal Life Insurance and its lifelong investment value and want to lock in that future value for their children.

We did have one couple out of Mississauga who were looking to cover their mortgage period. But when they learned that Universal Life Insurance offers tax-deferred savings potential, they began rethinking their strategy. A second client, a small business owner from Surrey, said, “I want coverage now but also don’t want to waste my premiums.” Both are essentially asking the same underlying question: What is a better plan — a Universal Life Insurance Plan or a term life insurance plan?

If you also have such confusion, this blog will take you step by step through each of those real-life events and advice we play to our clients at Canadian LIC on a daily basis.

What is a Term Life Insurance Plan?

A Term Life Insurance Plan provides coverage for a set period — usually 10, 20, or 30 years. If the insured person passes away during that term, their beneficiaries receive the payout.

Why Many Clients Ask for Term Life Insurance Policy Quotes Online

Most people search for quotes for a Term Life Insurance Policy online because these are simple, easy-to-understand plans, and they usually come with low premiums. It’s a sensible decision if you’re:

- Paying off a mortgage

- Raising young children

- Desiring coverage within working years

We insured a young couple from Brampton, Ontario, teachers, with a 20-year term life policy. They planned to protect their kids until the kids were financially independent. They loved that it was affordable and covered their specific needs.

The Cost of Term Life Insurance Plans in Canada

One of the biggest selling points of term life coverage is its affordability. A $500,000 20-year policy for a healthy 30-year-old nonsmoker could cost as little as $25/month. That makes it appealing to young families, new immigrants, or anyone seeking low-cost coverage.

But what most folks don’t realize is that once the term is over, the premiums can go through the roof if you try to extend. That is something we often have to explain to clients who call in to request renewal quotes — especially when their health has changed over the years.

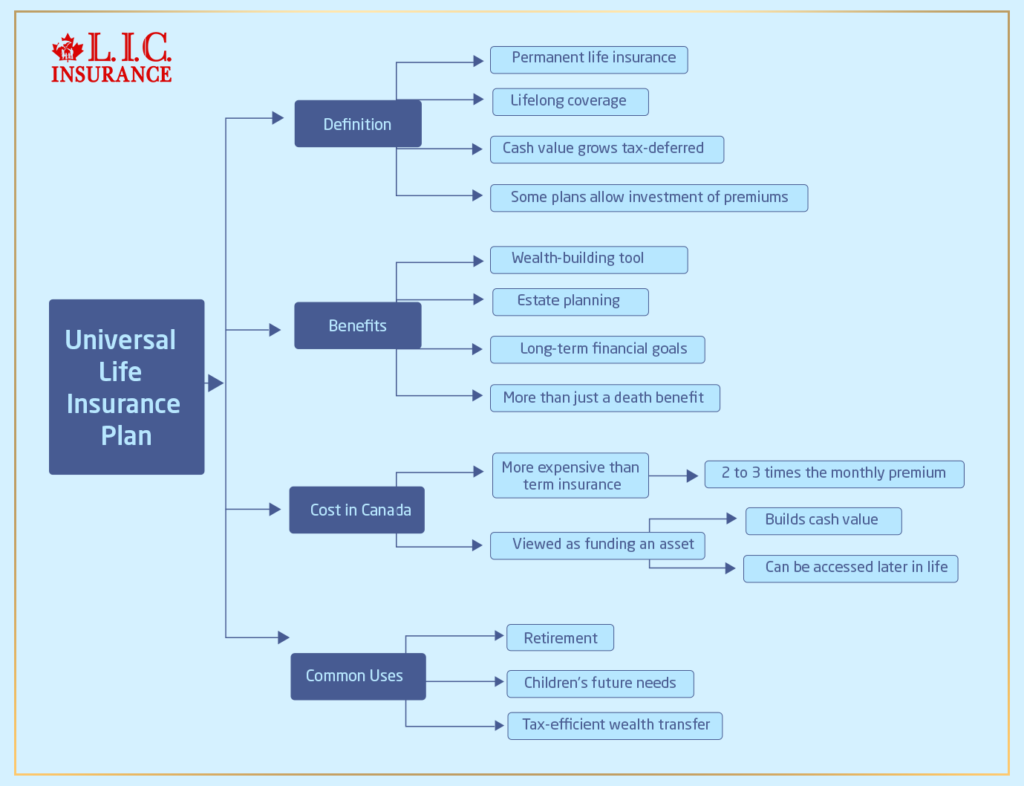

What is a Universal Life Insurance Plan?

Universal Life Insurance is a form of permanent life insurance. It provides lifelong coverage and accrues cash value that grows tax-deferred. You might even have the option to invest some of your premium, depending on how the plan works.

This is best for long-term goals, estate planning, or anyone who wants their insurance policy to serve more than merely as a death benefit.

We once guided a dentist based in Toronto who didn’t just want protection — he wanted a way to grow his wealth, shielded from tax while he did so. He selected a Universal Life Insurance Policy and said, “This feels like I’m building my child’s legacy with every premium I pay.”

The Cost of Universal Life Insurance Plan in Canada

Yes, the price of a Universal Life Insurance Plan exceeds the similar term plans — often up to 2 to 3 times the monthly premium. But this is what clients soon learn: You’re not just buying coverage. You’re funding an asset. A portion of your premium builds cash value that you can tap into later in life.

This plan is often the one our clients use to help pay for:

- Retirement

- Children’s future needs

- Tax-efficient wealth transfer

Universal Life Insurance Plan Vs Term Life Insurance Plan: Head-to-Head Comparison

Let’s break it down further so you can understand the key differences through the lens of what families are really dealing with when they come to us.

1. Coverage Duration

- Term Life Insurance Plan:

- Provides protection for a set number of years. Once the term expires, coverage ends unless it is renewed at a higher rate.

- Universal Life Insurance Plan:

- Provides lifelong coverage, no expiry — as long as you continue funding the policy appropriately.

A self-employed father from Ottawa came in frustrated when his 10-year term expired just when he got diagnosed with a health condition. He now faced high premiums and limited options. Had he opted for a universal plan early on, he wouldn’t have been in that position.

2. Premium Structure

- Term Life Insurance Plan:

- It has a low initial cost, but premiums increase significantly upon renewal.

- Universal Life Insurance Plan:

- It has a higher cost from the start, but premiums can stay level for life, and you build value over time.

When comparing the cost of a Universal Life Insurance Plan to the cost of a Term Life Insurance Plan, it’s really a trade-off between paying less now vs. gaining more later.

3. Cash Value Accumulation

- Term Plan:

- No cash value. Once your policy ends, you walk away with nothing.

- Universal Life Plan:

- Accumulates tax-sheltered savings that you can borrow against or withdraw.

One of our long-time clients in Alberta used the cash value from his universal policy to pay for his daughter’s university tuition without touching his RRSP. “It was a huge relief,” he said. “I never expected my insurance policy would help us with education too.”

4. Flexibility in Premiums and Investments

- Term Plan:

- Fixed premiums, no investment options, and no policy adjustments.

- Universal Plan:

- Flexible premiums and investment options depending on your risk appetite.

We’ve seen entrepreneurs use this flexibility to reduce premiums during lean business periods temporarily, something you can’t do with term plans.

5. Purpose and Goals

- Term Life Insurance Plan:

- Best for short-term financial obligations — mortgage, children’s education, income replacement.

- Universal Life Insurance Plan:

- Ideal for lifelong protection, estate planning, wealth transfer, and investment growth.

A retired couple from Vancouver wanted to leave something for their grandchildren. They chose a universal life policy for its growth potential and because it made estate planning easier. “We liked knowing the value will keep growing, even after we’re gone,” they said.

6. Renewal and Conversion Options

This is a big one that most people overlook when comparing a Universal Life Insurance Plan vs a Term Life Insurance Plan.

- Term Plan:

- You can usually renew or convert your policy at the end of its term, but the cost can go up significantly. And if your health has changed, you may not qualify for a new policy at all.

- Universal Plan:

- No need for renewal. The coverage is permanent, so you don’t face rising premiums or requalification down the road.

We once had a teacher from Montreal who had a 10-year term policy. After her term ended, she was shocked at the new price for a similar policy. She told us, “I wish someone had told me this would be the case. I would’ve thought differently.” That’s why we guide our clients to think long-term when choosing their coverage.

7. Investment Growth Potential

- Term Life Insurance Plan:

- No investment feature, strictly coverage.

- Universal Life Insurance Plan:

- Has an investment component that allows you to grow your savings within the policy. Depending on how the plan is structured, you can select from a range of investment options, from conservative to aggressive.

One small business owner we worked with in Mississauga used his universal policy to grow funds that later helped cover business expansion costs. “I wasn’t just protected — I was planning for growth,” he said.

8. Tax Benefits

- Term Plan:

- No savings or investments, so there are no tax benefits during the life of the policy.

- Universal Plan:

- Cash value grows tax-deferred. That means you don’t pay taxes on growth inside the policy unless you withdraw it.

This is especially important for high-income earners or incorporated professionals who are already maxing out their RRSPs and TFSAs. Many use universal life plans as an extra tax shelter, which makes sense, given Canada’s increasing tax landscape.

9. Affordability vs. Value Over Time

When clients compare Term Life Insurance Policy Quotes Online and Universal Life Insurance Policy quotes, the price difference often surprises them.

- Term Life Insurance seems more affordable in the short term. A young, healthy Canadian can get $500,000 in coverage for under $30/month.

- Universal life, while more expensive upfront, offers lifetime benefits. The cost of a Universal Life Insurance Plan may start at $100 or more per month, but you’re building equity, and your premiums stay steady.

That’s a huge plus for anyone thinking beyond just the next 10 or 20 years.

Which Plan Do Canadian LIC Clients Choose More Often?

It really depends on the person’s stage of life and financial goals. Here’s what we commonly see:

Young Families

Most young families with kids choose Term Life Insurance first. They need coverage fast, and the budget is tight. They often start by looking for Term Life Insurance Policy Quotes Online to find an affordable entry point.

Homeowners and Mortgage Holders

Term Life Insurance is still popular here because the plan aligns with the mortgage term. But more and more homeowners are adding a universal plan later to prepare for retirement and estate planning.

Business Owners and Professionals

These clients often prefer universal life plans because of their tax benefits, flexibility, and long-term value. The cost of a Universal Life Insurance Plan is seen as a business investment, not just a monthly expense.

Clients Often Ask Us: Can I Start With Term and Switch to Universal Later?

Yes. Many insurance providers offer the option to convert your term plan to a universal life policy later — often without another medical exam. This allows you to get affordable coverage now and move into a lifelong plan as your financial situation improves.

We encourage many of our younger clients to start small and grow into their coverage as their income grows.

Helping You Decide: What Questions Should You Ask Yourself?

When helping clients compare Universal Life Insurance Plan vs Term Life Insurance Plan, we often ask them:

- Do you need short-term or lifelong protection?

- Are you comfortable paying more now for future benefits?

- Is your priority affordability or long-term growth?

- Do you want your insurance plan to double as a savings tool?

- What’s your vision for your family 10, 20, or 30 years from now?

Your answers will help guide the right path.

Summary: Choosing the Right Plan for You

To help you choose more confidently, here’s a quick side-by-side:

Final Thoughts on Universal Life Insurance Plan Vs Term Life Insurance Plan

As with any financial decision, choosing between a Universal Life Insurance Plan and a Term Life Insurance Plan in Canada all boils down to what is most valuable to you: saving money today or lifelong financial protection with additional value.

Term Life Insurance is ideal for people who would like affordable coverage now, particularly for finite needs such as protecting a mortgage or raising children. But after the term, there is nothing to be left.

Universal life is for people who want a policy that can grow with them — through family changes, business goals, retirement and beyond. This is not only protection; this is a strategy.

Every day at Canadian LIC, we assist clients in navigating through these choices. The reality is that either plan can serve as a strong financial plan. Some begin as a term, but if they are lucky, they graduate into universal. Others will buy Universal stock immediately because they perceive long-term value.

Whatever path you choose, be sure that you’re asking the right questions — and working with advisers who are attuned to your individual goals.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

A Universal Life Insurance plan provides lifetime coverage and accumulates tax-deferred savings over time, while a Term Life Insurance Plan covers you for a specified term, such as 10, 20, or 30 years. The term plan is cheaper initially, but a universal plan builds cash value over time and offers greater investment options.

Your Universal Life Insurance Policy quotes are usually higher than term life quotes because they provide both insurance coverage and a savings component. However, the additional expense also provides lifelong protection, tax-deferred growth, and access to cash value if you need to use it for retirement or other emergencies down the line.

The lowest rates tend to go to non-smokers in good health. Higher coverage and longer terms raise the cost of coverage, but most people find it the right fit for short-term financial responsibilities.

You can see the cost of becoming a Universal Life Insurance Plan that allows you to do more than just basic protection. It features permanent coverage, flexible premiums, investment growth, and a tax-deferred savings account. For Canadians who are establishing long-term wealth transfer or estate planning, it’s more than just insurance — it’s a financial instrument.

Key Takeaways

- A Term Life Insurance Plan is cost-effective and ideal for short-term needs like mortgage protection, childcare, and income replacement during working years.

- A Universal Life Insurance Plan offers lifelong coverage with the added benefit of tax-deferred cash value growth and flexible investment options.

- When comparing the cost of a Universal Life Insurance Plan vs the cost of a Term Life Insurance Plan, the term is more affordable upfront, while universal adds long-term financial value.

- Term Life Insurance Policy Quotes Online are easy to access and help Canadians find affordable protection tailored to a specific time frame.

- Universal Life Insurance Policy quotes may show higher premiums, but they reflect benefits like lifetime coverage, cash value access, and wealth-building potential.

- Term plans expire, often with no return unless a claim is made, while universal plans grow in value, and the funds can be used for retirement, business, or estate planning.

- Many Canadians start with term life and later convert to Universal Life Insurance as their financial situation matures.

Sources and Further Reading

- Government of Canada – Life Insurance Overview

Basic explanations of different life insurance types, including term and permanent coverage.

🔗 https://www.canada.ca/en/treasury-board-secretariat/services/benefit-plans/management-insurance-plan/public-service-management-insurance-plan-life-insurance-glance.html - Canadian Life and Health Insurance Association (CLHIA)

Industry-level insights and consumer guides on life insurance in Canada.

🔗 https://www.clhia.ca - Canada Revenue Agency – Taxation of Life Insurance

Explain how the cash value of permanent insurance (like universal life) is taxed in Canada.

🔗 https://www.canada.ca/en/revenue-agency.html - Insurance Bureau of Canada – Understanding Your Insurance

Provides general insurance guidance and how to work with licensed brokers.

🔗 https://www.ibc.ca

- Government of Canada – Life Insurance Overview

Your Feedback Is Very Important To Us

We’d love to learn more about your experience so we can better support families like yours. Please take a moment to answer the following questions. Your responses will remain confidential and will only be used to help us offer more personalized solutions.

Thank you for your feedback! It helps us create more helpful content tailored to your needs.

IN THIS ARTICLE

- Universal Life Insurance Plan Vs Term Life Insurance Plan

- What is a Term Life Insurance Plan?

- What is a Universal Life Insurance Plan?

- Universal Life Insurance Plan Vs Term Life Insurance Plan: Head-to-Head Comparison

- Which Plan Do Canadian LIC Clients Choose More Often?

- Clients Often Ask Us: Can I Start With Term and Switch to Universal Later?

- Helping You Decide: What Questions Should You Ask Yourself?

- Summary: Choosing the Right Plan for You

- Final Thoughts on Universal Life Insurance Plan Vs Term Life Insurance Plan

Sign-in to CanadianLIC

Verify OTP