- Connect with our licensed Canadian insurance advisors

- Schedule a Call

Basics

- What Is the Maturity Period of Term Insurance?

- Understanding the Uses of a Term Insurance Calculator

- What Is Underwriting in Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- How Do You Choose Term Insurance?

- Can You Cash Out a Term Life Insurance Policy?

Reviews

Common Inquiries

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- How Do You Choose The Right Claim Payout Option For Your Term Insurance?

- What Are the Claim Payout Options?

- Factors to Consider When Choosing a Claim Payout Option

- Benefits of Each Payout Option

- Insurance Struggles from Canadian LIC's Perspective

- Role of Term Life Insurance Brokers in Decision-Making

- Steps to Choose the Right Claim Payout Option

- Why Canadian LIC is the Best Choice

- Act Today for a Secure Tomorrow

How Do You Choose The Right Claim Payout Option For Your Term Insurance?

By Harpreet Puri

CEO & Founder

- 11 min read

- January 9th, 2025

SUMMARY

Choosing the right claim payout option for your Term Life Insurance Plan ensures your family’s financial security. This blog explains payout types—lump sum, staggered payments, or a mix—and how to select the best option based on immediate and long-term needs. It highlights real-life struggles and the role of Term Life Insurance Brokers in guiding families. Learn how factors like financial habits, inflation, and flexibility impact your decision, ensuring your Term Life Insurance Investments serve their purpose.

Introduction

Deciding how the claim would be paid is one of the most crucial decisions concerning a Term Life Insurance Plan with regard to safety for your family’s future. The average person would be left feeling puzzled over whether the payout should come in a single lump sum or staggered in installments, sometimes both. Often, it’s simply because they have no idea about how such an option might coexist with a set of already established financial goals. It is not just about securing life insurance but ensuring the payout will provide the support intended for your loved ones at the right time.

We have had so many families struggle with the same decision-making processes at Canadian LIC. Take the father of two, for example, who opted for a lump sum payout. Although his family did receive a very significant amount, they reported how hard it was to manage the sum. However, another family that opted for staggered payouts received an amount better suited for their budgeting patterns. These stories reflect why it is crucial to select the right payout claim.

In this blog, we will take you through the primary considerations in choosing a claim payout option, the options available, and how to make an informed decision with help from Term Life Insurance Brokers such as Canadian LIC.

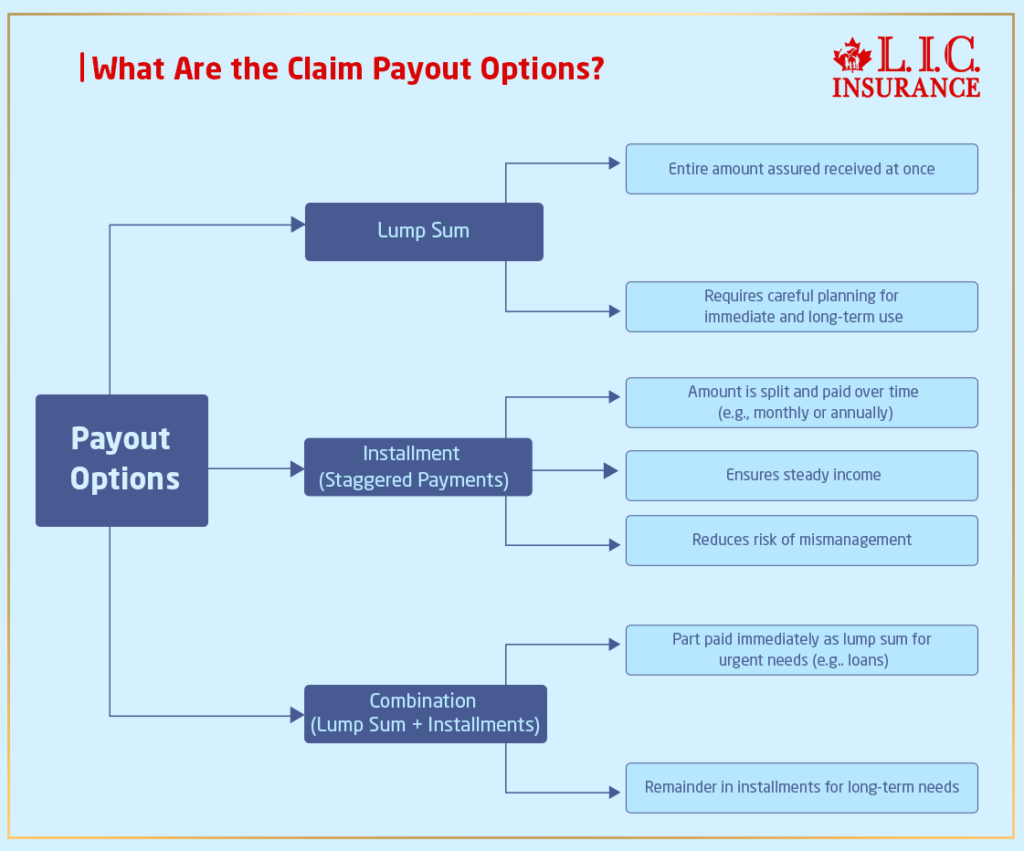

What Are the Claim Payout Options?

Selecting the correct payout for your Term Life Insurance investment begins with choosing a payout. Many Term Life Insurance companies have three basic payout forms:

Lump Sum

The most conventional form of payout and the most often selected one. The entire amount assured is received by the beneficiary in a lump sum. Such a large sum of money has to be carefully planned and immediately put into use to serve as an emergency fund or for some other urgent need.

Installment or Staggered Payments

Under this format, the sum assured is proportionately split up and allowed to be paid out over a period, like monthly or annually. This can help beneficiaries maintain a steady income and avoid the risk of mismanaging a large lump sum.

A mixture of Lumps and Instalments

A few persons prefer a mixture of both—a part of it is given immediately as a lump sum to solve immediate needs, such as settling loans or mortgages, while the rest is in installments, which would address long-term needs.

Factors to Consider When Choosing a Claim Payout Option

When deciding on a claim payout option, several factors come into play. Here’s a breakdown of what you should evaluate:

Your Family’s Financial Literacy

Think about how comfortable your beneficiaries are in managing money. A lump sum may work well for a person who has a good grasp of financial planning, but staggered payments will work better for someone who needs steady support or guidance.

In Canadian LIC, it happened with a client who admitted to underestimating this factor. A client narrated his wife’s struggle after receiving a lump sum due to her unpreparedness to handle such huge sums. After discussions, he opted for a staggered payout in his updated Term Life Insurance Plan.

Immediate Financial Needs

For instance, consider what immediate expenses your family might have to pay in your absence: mortgage payments, credit card debt, or tuition fees. A lump sum will take care of such costs right away, while installments may not solve urgent needs so well.

Long-Term Financial Goals

A lot of families benefit from staggered repayments if children are still younger and have further financial obligations with respect to higher education or Term Life Insurance Cost of living for sustenance.

Inflation and Economic Changes

Inflation eats up the purchasing power. Payment in installment form, with some clause for an adjustment in inflations, secures the full buying power at home. Salespersons of these term life covers remind one often enough during discussion time.

Benefits of Each Payout Option

In order to choose wisely, it’s essential to weigh the advantages of each option:

Lump-Sum Payment

- With instantaneous access to the full sum assured.

- Best suited for repayment of large debts like mortgages.

- It provides flexibility in managing funds.

Lump sums, however, require planning. Beneficiaries should avoid spending the money too quickly or making poor financial decisions.

Installment Payments

- Ensures a steady income stream over time.

- Helps prevent overspending or mismanagement.

- Suitable for families with ongoing financial needs.

Combination Payout

- Balances immediate needs with long-term financial security.

- Provides flexibility for both urgent expenses and sustained income.

Insurance Struggles from Canadian LIC's Perspective

We usually hear clients voice their concerns about whether their families will make the right choices in their respective absence. An example would be a single mother who hung between a lump sum and installments. The reason was that she wanted her teenage son to have money available for his education, but she was afraid he could not make a big payment properly. Based on the detailed discussions, she opted for a combination payout wherein funds for tuition were available immediately, and the rest was paid over for other costs of living.

Another client was a young couple who had just conceived their first child and preferred the installments. The major reason they opted for this mode was to provide steady child-rearing financial support for the next 20 years.

These stories reveal how personal circumstances and family dynamics greatly affect the choice of claim payout options.

Role of Term Life Insurance Brokers in Decision-Making

You must not make this choice in isolation. A competent Term Life Insurance agent will advise you based on your financial goals, your family needs, and policy features. At Canadian LIC, we have guided hundreds of clients to tailor-made Term Life Insurance Plans that assist them with payout options that suit their distinct circumstances.

Steps to Choose the Right Claim Payout Option

Evaluate Your Family’s Needs

Take into account your family’s short-term and long-term financial needs. Create a list of possible expenses, including debt repayment and education costs.

Talk to Beneficiaries

Communication with your family will make them understand the benefits of the payout option chosen. This will also help them prepare for the management of funds.

Consult Term Life Insurance Brokers

A broker can guide you on the advantages and disadvantages of each payout option and suggest the best for your case. They are professionals in Term Life Insurance Investments and will guide you through the decision-making process.

Review Inflation-Protection Features

If you are opting for installments, look for inflation protection in your policy to protect you from inflationary increases.

Customize Your Policy

Many insurance companies provide an option for personalizing payout. Take full advantage of the choices to tailor a plan to fit your family.

Why Canadian LIC is the Best Choice

We at Canadian LIC specialize in aiding our clients with Term Life Insurance to make proper decisions regarding such policies. Our team is dedicated to guiding our clients, who may need advice about how to buy Term Life Insurance online or the actual buying of such a plan.

Act Today for a Secure Tomorrow

Choosing the best claim payout option is a rather daunting task; however, under proper guidance, you can rest assured that your family’s future will be safe and sound. Contact Canadian LIC, the top-Term Life Insurance broker in Canada, and get started on the road to protecting your loved ones.

When you select a payout option that works well for your family, you’re not only investing in insurance-you’re investing in their peace and security. Get your Term Life Insurance quote today and make a choice your family will thank you for.

More on Term Life Insurance

- Limited Pay vs Regular Pay Term Insurance

- When To Cancel Term Life Insurance?

- Best Term Life Insurance Plans For Couples

- Joint Term Insurance VS. Two Separate Term Plans

- Which Is Better – Term Insurance Or Health Insurance?

- Importance Of Accidental Total And Permanent Disability Rider With Term Insurance

- Why Are Term Life Insurance Claims Rejected

- What Type Of Risk Is Covered By Short Term Insurance?

- What Happens If You Can’t Pay Your Term Life Insurance?

- What Will Disqualify You From Term Life Insurance?

- Can Riders Be Added To Term Life Insurance?

- Why Buy Term Life Insurance From An Insurance Broker?

- Why Not Buy Term Life Insurance From Banks?

- What Is The Difference Between Term Insurance And Group Term Insurance?

- Is There 10-Year Term Life Insurance?

- Does the Term Life Cover Accidental Death?

- Is Buying a Term Plan Online Safe?

- When Does Term Life Insurance Payout?

- Who Should Not Get Term Life Insurance?

- What Is the Maximum Limit in Term Insurance?

- What Are the 4 Types of Term Life Insurance?

- Can a Child Be the Owner of a Term Life Insurance Policy?

- Which Is Better, Term Insurance or SIP?

- What types of death are not covered in Term Insurance?

- Can I Pay Term Insurance Monthly?

- Pros and Cons of Buying Term Life Insurance Plans

- Can Term Life Insurance Be a Business Expense?

- What Happens When Term Life Insurance Expires?

- What Happens After 20 Years of Term Life Insurance?

- Can Term Life Insurance Be an Investment?

- Term Life Insurance Plan for All Age Groups

- What Does It Mean to Buy Term & Invest the Difference?

- How Do You Calculate Term Insurance Value?

- Why Is Term Life Insurance with a Return of Premium Option Not the Best Risk Coverage for You?

- Group Term Life Insurance & Individual Term Insurance: Know the Details

- What Is the Claim Period for Term Life Insurance?

- Can I Convert My Term Policy to Whole Life?

- Can You Use Term Life Insurance to Pay Off a Mortgage?

- Do Term Life Insurance Plans Offer Cash Value?

- What Happens to Term Insurance If the Nominee Dies?

- What Is the Shortest-Term Life Insurance Policy?

- What Is the Cheapest Term Life Insurance for Seniors Over 70?

- Who Benefits from Term Life Insurance?

- Can Term Insurance Be Rejected After Five Years?

- What Is the Longest Term Life Insurance?

- Does Term Insurance Automatically Renew?

- Can you extend a 20-Year Term Life Policy?

- Do I Get Money Back from Term Life Insurance?

- Can You Cash Out a Term Insurance Policy?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 844-542-4678 to speak to our advisors.

Get Quote Now

FAQs About Choosing the Right Claim Payout Option for Your Term Life Insurance Plan

A claim payout option determines which form the life insurance company uses to pay a death benefit. It can be paid out as an all-at-one time, divided payments, or a combination. Term Life Insurance Brokers should explain these payouts in detail to their clients so as to make the decision-making process correct.

The best option is based on what your family requires. A lump sum is suitable for paying large debts, but staggered payments ensure steady income over time. At Canadian LIC, we usually help families decide between these two options based on their financial aims and comfort level with managing money.

In general, you are allowed to change the payout option, provided that the policy allows it. Most people find out that their families’ needs may change over time, and informed brokers can guide you through this process.

This product allows staggering the amount assured in smaller payments disbursed monthly, quarterly, or annually for a certain period. Thus, families can manage their expenses more productively. Many of our clients at Canadian LIC prefer this to ensure regular income for day-to-day requirements.

Lump sums allow the whole amount to be available at one time, which makes it challenging to manage. Unless financial planning is in place, beneficiaries tend to spend the money too fast. The Term Life Insurance Brokers recommend this type for families that do not have any problems managing finances.

Yes, most policies can be combined. For instance, you can pay some of the benefit towards debts and use the remaining part for day-to-day expenses. This flexibility has helped many Canadian LIC clients to meet short and long-term financial needs.

Brokers at Canadian LIC can analyze your family’s needs and recommend the pros and cons of every option while offering you the best one suitable for your needs. Their years of experience with Term Life Insurance Investments ensure you are making a very informed choice.

Yes, you can purchase Term Life Insurance online and also have the payout structure customized to meet your family’s needs. Canadian LIC offers smooth online services with the help of expert brokers who can guide you through tailoring your policy.

Request a Term Life Insurance quote from any broker or obtain one online; specify your preference for the mode of payout in the quote and make sure this reflects the respective terms and benefits.

If the returns are not sufficient to support your family, they end up struggling to survive financially. Avoid such a situation by consulting experienced brokers in Term Life Insurance Plans to get the right policy according to your intentions.

No, life insurance payouts are generally tax-free in Canada. This means your family receives the full benefit regardless of the payout option you select.

Consider the financial literacy of your family, their present and future requirements, and whether they are capable of managing money. A broker typically pushes his client to engage his family for better assimilation.

Discuss the policy details and payout structure with your beneficiaries. Canadian LIC frequently facilitates such conversations, ensuring families are well-informed and prepared to handle the payout.

If you don’t decide how the insurance company is to pay for a Life Insurance claim, they will commonly make a lump-sum payout. It is better to decide upfront so that the payout matches your family’s requirements. At Canadian LIC, we also encourage our clients to consider their family’s financial habits before finalizing a Term Life Insurance Plan.

Yes, staggered payments can sustain steady income with a daily current requirement and potential long-term usage in education funds for children; that is a significant reason, given the size of many children at this period.

Yes, it is possible to split the policy among various beneficiaries and provide a different payout option for each one. For instance, one might get a lump sum and another staggered payment. A Canadian LIC broker often advises such families with differing financial needs to do so.

The payout option does not normally affect the premium, but most insurers charge small differences in rate for installment payouts since it involves administrative costs. Always ask for Term Life Insurance Quotes specific to your chosen payout structure.

Yes, but depends on the policy terms. Most insurers allow adjustment during the policy term. You may get assistance updating your Term Life Insurance Plan from brokers, such as those at Canadian LIC if your family’s needs change.

Payout options don’t impact the investment or coverage value, but they determine how the benefits are distributed. Choosing the right option ensures the investment serves your family as planned.

Ask how each option works, how flexible it is to change, and how it aligns with your family’s financial situation. This is often what Canadian LIC brokers will answer in consultations to make decisions easier.

The key risk is that your family will require a more significant amount up front in the event of emergencies. Some clients opt for a combination of a lump sum with staggered payments for added flexibility.

Brokers analyze your financial goals and recommend policies that maximize your investment. They also guide you in selecting claim payout options that best serve your family’s needs.

Many insurance companies provide competitive offers to those who make an online purchase. Nevertheless, considering experienced brokers helps ensure you get the right coverage and payout options along with the best quote for Term Life Insurance.

Inflation can reduce the buying power of future payouts. Canadian LIC brokers often advise clients to include an inflation adjustment clause in their policies to address this issue.

Some insurers may charge administrative fees for managing installment payouts. Discuss these details with your broker before finalizing your Term Life Insurance Plan.

Mismanagement can lead to financial instability. To avoid this, many families choose staggered payments or involve trusted brokers to guide beneficiaries in managing their payout.

In Canada, Term Life Insurance payouts are typically tax-free, regardless of the option you choose. Brokers clarify these details to ensure your family understands the benefits.

The time frame depends on the conditions of your policy. Some policies allow payment over 10, 20, or even 30 years. Canadian LIC has provided families with options to customize their policies for long-term financial security.

These FAQs address typical concerns of a claim payout option available in Term Life Insurance Plans. Feel free to make a decision and get in touch with Term Life Insurance Brokers like Canadian LIC, or start searching for quotes online to secure your family’s future.

Sources and Further Reading

Government of Canada – Life Insurance Basics

https://www.canada.ca

Comprehensive information on life insurance options, tax benefits, and regulations in Canada.

Insurance Bureau of Canada (IBC)

https://www.ibc.ca

Resources on choosing the right life insurance policy and understanding coverage.

Canadian Life and Health Insurance Association (CLHIA)

https://www.clhia.ca

Insights into life insurance types, payout structures, and consumer protection.

Globe and Mail – Financial Planning Articles

https://www.theglobeandmail.com

Expert articles on financial planning, including Term Life Insurance Investments and family security.

Investopedia – Term Life Insurance Explained

https://www.investopedia.com

Detailed guides on Term Life Insurance policies, payout options, and financial considerations.

Sun Life Canada – Life Insurance Resources

https://www.sunlife.ca

Helpful guides and tools to understand Term Life Insurance Plans and their benefits.

Key Takeaways

- Government of Canada – Life Insurance Basics

https://www.canada.ca

Comprehensive information on life insurance options, tax benefits, and regulations in Canada. - Insurance Bureau of Canada (IBC)

https://www.ibc.ca

Resources on choosing the right life insurance policy and understanding coverage. - Canadian Life and Health Insurance Association (CLHIA)

https://www.clhia.ca

Insights into life insurance types, payout structures, and consumer protection. - Globe and Mail – Financial Planning Articles

https://www.theglobeandmail.com

Expert articles on financial planning, including Term Life Insurance Investments and family security. - Investopedia – Term Life Insurance Explained

https://www.investopedia.com

Detailed guides on Term Life Insurance policies, payout options, and financial considerations. - Sun Life Canada – Life Insurance Resources

https://www.sunlife.ca

Helpful guides and tools to understand Term Life Insurance Plans and their benefits.

Your Feedback Is Very Important To Us

Thank you for taking the time to provide your feedback. Your input helps us understand the challenges individuals face when choosing a claim payout option for their Term Life Insurance Plan. Please fill out the questionnaire below.

(We value your privacy. Your information will not be shared or used for any purposes outside of providing assistance.)

IN THIS ARTICLE

- How Do You Choose The Right Claim Payout Option For Your Term Insurance?

- What Are the Claim Payout Options?

- Factors to Consider When Choosing a Claim Payout Option

- Benefits of Each Payout Option

- Insurance Struggles from Canadian LIC's Perspective

- Role of Term Life Insurance Brokers in Decision-Making

- Steps to Choose the Right Claim Payout Option

- Why Canadian LIC is the Best Choice

- Act Today for a Secure Tomorrow

Sign-in to CanadianLIC

Verify OTP