- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Why Many Older Parents In Canada Are Underinsured?

By Pushpinder Puri

CEO & Founder

- 13 min read

- April 15th, 2026

SUMMARY

Older parents in Canada face rising financial obligations and heavier protection needs, creating a growing Life Insurance Coverage gap. The content explains why Life Insurance for older parents in Canada is essential, how Term Life Insurance rates by age chart impact affordability, and how permanent options, cash value benefits, and tailored insurance solutions strengthen financial protection for Canadian families.

Introduction

There’s a quiet drift going on across Canada, and it is manifesting itself in some ways that people did not anticipate. Families are being made later in life, careers last longer than they once did, and the burdens of home rarely double up the way they used to. According to Statistics Canada, the average age of first-time parents has been steadily increasing over the last 20 years, and that means Life Insurance for older parents in Canada is one of the most important financial topics going on behind closed doors in this country. More troubling still, new data that the research firms Angus Reid and PolicyMe have shared with me show that almost a third of Canadians say they’re not sure whether their own families would remain financially secure if they were to die prematurely — a figure that only climbs further among households with parents in the late stages of life.

This uncertainty is compounded by pressures from inflation, rising housing costs, and the fact that many Canadians are cutting back on necessities such as insurance. That same Angus Reid–PolicyMe report indicates that uninsured Canadians who are not holding out for a vaccine will mostly not be purchasing coverage in the foreseeable future, despite older households being the most at risk of financial hardship. These holes are real, and they’re felt most acutely by families when something unexpected occurs: lost income, a medical emergency, or a sudden change in financial priorities.

We’re having these conversations every day — parents who delayed family life to rebuild careers, or supported multiple generations under one roof. Somewhere in our hearts, they come to us for answers, not jargon. They want the kind of protection that reflects their world today, not the one they imagined living in twenty years ago. And in a financial environment marked by mounting burdens, delayed life events, and squeezed household income, the imperative for solving the Life Insurance coverage gap for Canadian parents has never been more acute.

The Growing Life Insurance Coverage Gap Among Canadian Parents

Why More Canadian Families Are Having Children Later In Life

All over the country, older households are caring for toddlers, tweens, and teens — sometimes all at the same time. And these older parents are juggling the dynamics of young kids, younger children, university-bound teens, and even adult children returning home. With the cost of child care, school fees, and long-term education costs, those post-gap families often have higher than expected financial responsibilities. Many are still worried about paying for day-to-day living expenses, as they juggle the reality of caregiving for aging parents.

For families like these, the math grows complicated quickly. Even just one parent gone can throw everything out of whack — the schedule, the home routines, and that carefully-constructed financial apparatus. There are high stakes, and the protection demands are far greater than what is often assumed.

The Rising Cost Of Insurance Amid Late-Life Parenthood

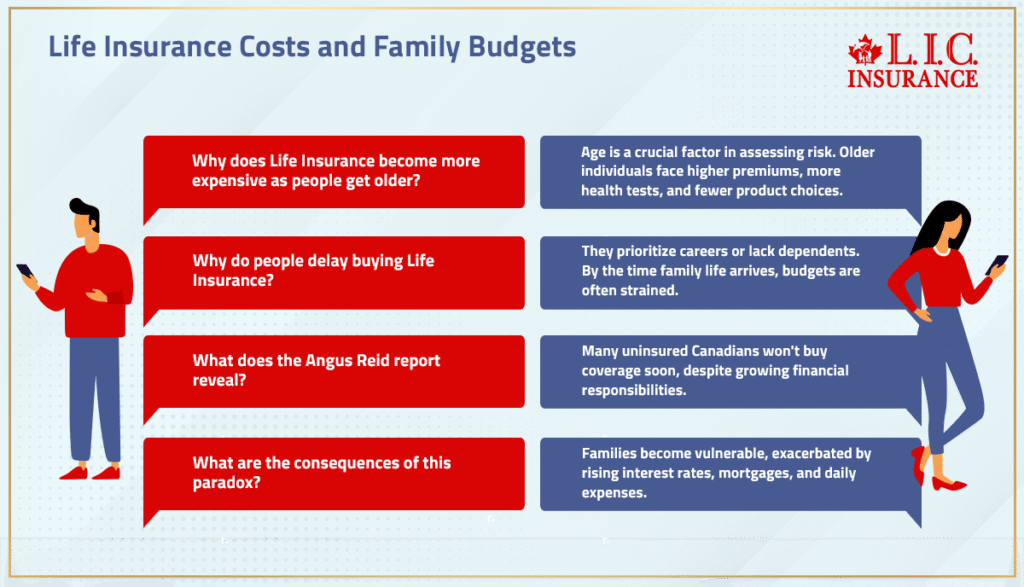

Life Insurance becomes more expensive as people get older. This is an industry of risk curves, and age is one of the most important. That is why older heads of households are charged higher premiums, may be subject to more mandatory health testing, and in some cases, have fewer products from which to choose. A lot of people say they put off buying Life Insurance before because they were concentrating on their careers or didn’t have any dependents. When family life did come along, many family budgets were already strained.

The Angus Reid report confirms this trend: A hefty portion of uninsured Canadians reported that they won’t be purchasing coverage soon, even though financial responsibilities are increasingly high. It’s a paradox that leaves families open to real vulnerability. Toss in rising interest rates and taller mortgages, as well as day-to-day expenses, and the gap widens even further.

Why Many Older Parents Lack Proper Life Insurance Protection

Balancing Mortgages, Retirement Savings, And Children’s Needs

Parents in their 40s, 50s, and even 60s are driving in more than one financial lane at once. They are saving for retirement, paying down mortgages, giving a boost to children’s education, and supporting young kids who need years more of help. Those obligations require a solid financial plan, but many people fail to fully consider the implications of an untimely death. Without insurance, families may find themselves fighting to remain financially secure, particularly if one-income homes are common.

Why Older Parents Acknowledge The Need But Still Avoid Purchasing Coverage

We see many families where older parents must admit to the need but are reluctant to take the step. Some worry about the cost. Others fear medical requirements. A lot of people just kind of assume that the insurance they bought 20 years ago is going to stretch somehow to meet their new reality and bigger mortgages, longer-term dependents, and heavier, whatever the case may be.

Responses from experts such as those at Truth Insurance Services Corp and RBC Insurance raise a separate worry: Families tend to underestimate “how much insurance coverage” they truly require. Their protection requirements are often twice, sometimes three times as great as in their younger years. But older households buy less — or do without.

How Life Insurance Works For Older Parents With Higher Financial Obligations

Term Life Insurance Options For Older Parents

For a lot of families, term life insurance is still the easiest way to restore that protection fast. It provides simple coverage and an easy-to-predict cost. Looking at a term life insurance rates by age chart can be shocking for families, who might not realize how steep a premium increase they could face over the years. This is why even preventing some of those future deaths, not just in this pandemic but also in the next one and the one after that, is so meaningful when we act early instead of waiting.

In the event that something unfortunate happens, then a term plan ensures a detectable lump-sum amount that can help to support your dependents, pay off debts, and maintain their lifestyle. There are also many more older households who would wish to insure their own policy for both parents and ensure there are no gaps that could occur in later years.

Permanent Life Insurance And Cash Value Benefits

Those who seek lifelong coverage often gravitate toward permanent Life Insurance, particularly if they want to build a solid estate plan. These policies accumulate a cash value over time, and that component of the cash value can provide financial flexibility in the future. Some parents go so far as to consider borrowing against a Whole Life Insurance Policy to address short-term needs without interfering with long-term goals.

For older, longer-established households with developing assets, we here at such places as RBC Insurance and Sun Life Canada (and the professionals in individual insurance development) often note that a properly planned one of these strategies could increase the guaranteed death benefit paid out to the following generation.

Insurance Solutions Older Parents Should Consider Right Now

Joint First-To-Die Term Insurance For Immediate Protection

Families feeling the financial pinch who are trying to make their dollar go further, while still providing protection for loved ones, often turn to insurance products such as joint first-to-die coverage. It’s low-cost protection for two people at the same time, when they most need it—the death benefit that is. The surviving spouse gets the payout immediately when the first parent dies, so that the children’s routine and support of their home life does not fall off a cliff.

Joint Last-To-Die Policies For Estate Planning

Families that want their legacy to live on beyond them tend to prefer joint last-to-die options. These strategies make it possible to transfer wealth to those who are dear and intend that your wishes for the estate be honoured over the long term. They’re for parents who are looking to financially protect their family throughout their life, rather than simply replacing income in the immediate term. For many families with high net worth, this is the time-play that would keep their nuclear family’s financial future intact.

How Much Coverage Older Parents Really Need

Calculating Coverage Based On Financial Responsibilities

When we coach families on how much insurance they actually need, we look at four pillars: outstanding debts, living expenses, child care costs, and final expenses. These are non-negotiable financial realities. Without proper protection, they can quickly become financial hardships for the surviving family.

Balancing Premium Affordability With Proper Coverage

We assist families too in shielding their money spectrum without sacrificing the tempo. Whether they take a Life Insurance policy (or not), double down on the fund pools, or simply purchase further Life Insurance under an original setup, it is all about securing financial protection that reflects time and situation. With tuition costs going up and expectations in flux, parents can’t afford to guess.

How Canadian LIC Helps Older Parents Secure Proper Life Insurance Protection

Tailored Insurance Plans For Older Parents With Complex Needs

We listen and learn about how people really live as families — not as insurance textbooks assume we do. Our advisers customize insurance packages built on the appropriate blend of life policies for your household. Whether families need more robust Life Insurance, more intelligent estate planning, or just meaningful coverage, we design solutions that fit their makeup.

Reviewing Existing Policies And Filling The Life Insurance Coverage Gap

In our consultations, we uncover situations where too many Canadians rely on outdated coverage purchased years ago. We help parents close the Life Insurance Coverage gap for Canadian parents, especially among older parents who now carry heavier responsibilities than before.

Securing Your Family’s Financial Future Before It’s Too Late

Why Acting Now Matters For Aging Parents

And as costs of living soar and timelines shift, postponing coverage only means more risk. The longer families wait, the more their options are shaped by the rising cost of protection. For households juggling dependents, mortgages, and substantial investments, the smartest moves are invariably the ones made early — well before a crisis dictates that they act. Older parents, who are working around the clock to raise young children who rely on them for everything, deserve stability during these years. And the best way to truly serve that role is by securing their family’s financial future with the proper infrastructure.

More To Learn

- Cash Value Life Insurance In Canada: Pros, Cons, And How It Really Works

- Simplified Vs. Guaranteed Issue Life Insurance: Choosing What Truly Fits You

- Is There A Life Insurance Policy Where You Get Your Money Back?

- How Geopolitical Tensions In The Middle East Are Affecting Life Insurance Premiums In Canada?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

For many in midlife who have older children, the financial responsibilities continue to accumulate, but not their protection. Life can get so busy at times that Life Insurance decisions take a back seat to everything else. That such a delay builds an uneven foundation is something you do not realize until the pressure comes. A back-of-the-envelope type of analysis frequently shows how easily a Life Insurance gap can arise in the later years.

Families typically begin by considering their long-term plans, not only today’s expenses and debt obligations, since life shifts more rapidly than people imagine. Considering future objectives, changing responsibilities, and potential financial protection needs is a good start. This helps determine how much coverage “feels” right for their world, rather than an arbitrary guideline. The objective is to inspire tranquillity, not anxiety.

Yes, combining the two can enhance the rhythmic parts of contemporary family living. One provides concentrated protection; the other accrues long-term value that might help undergird all kinds of goals over time. This balance is favoured by some parents because it can adjust as responsibilities change. Together, they can enhance a family’s overall Life Insurance program without being limited to a single structure.

Canadian families most often start by drawing lines around the places where one member of the family is doing a disproportionate amount of work. Transferring some of that burden with the proper insurance policy provides stability when life jolts off course. Even modest steps can alleviate hidden pressure on the household. The goal is long-term financial security, not short-term relief.

Delays frequently shift the pricing landscape, risk increasing naturally with each passing year. But families sometimes manage to juggle the cost by opting for things that meet them where they are in life. But even with a more moderate Life Insurance choice, long-term security can still be steadied. The question is whether you move forward, not whether you do so at the perfect time.

An online Life Insurance quote provides a rapid baseline, but that is all it should be. What families ought to be examining is what is likely to work best, beginning in late summer or early fall, and not just as of today. “Parents are able to understand what works best for them by comparing structures.” A pause can bring in a more confident buy Life Insurance decision.

It starts with reclaiming clarity in a crowded financial world. Understanding which responsibilities matter most helps parents reset their priorities and breathe easier. From there, choosing the right insurance solutions becomes a tool instead of a task. Small corrections today can ease tomorrow’s financial stress.

Protection acts as a quiet guardrail for the years ahead. It steps in when routine, plans, or income face sudden change. For households carrying a lot on their shoulders, the right Life Insurance Policy makes life’s unpredictability less overwhelming. It preserves space for families to grow, rather than recover.

Most people go through life preoccupied by the next urgent task, not the slow-motion danger lurking just below the surface. Over time, that habit leads to a growing number of Life Insurance Policies sitting unloved while responsibilities keep expanding. A fast skim can uncover gaps that they never even knew were there. Closing those gaps early in their lives bolsters their financial security for decades to come.

Absolutely — families evolve, and their protection needs shift with them. Whether welcoming new family members or supporting older ones, coverage helps maintain balance during transitions. The right plan adjusts as life pivots. This flexibility keeps Canadian families grounded during unpredictable seasons.

If one parent has to pick up the slack for another, a household becomes especially dependent on their stability. This sudden transformation can bring pressure that is more immediate than families realize. The proper Life Insurance softens those things which affect and maintains day-to-day routines. That stability affords the family the space to go through hardship without losing traction.

In many cases, yes. Older parents often manage broader commitments and heavier financial obligations than families starting out earlier. Their timeline for recovering from unexpected loss is also shorter. A focused Life Insurance Plan helps preserve stability during these years of increased responsibility.

Insurance provides space for families to breathe when life doesn’t go as planned. It reduces the weight of big life changes and protects loved ones from many unexpected economic blows. By targeting the right risks at the right time, parents reinforce the foundation they’re working on. This is why Life Insurance is a long-term stabilizer, not just a policy.

It helps to start with clarity rather than price alone. Families should consider how each insurance policy supports long-term goals, structure, and flexibility. From there, choosing protection that aligns with lifestyle and obligations becomes easier. The focus is on support that lasts, not a quick fix.

Yes — that’s what it was made for. Households wrestling with tuition, care needs, mortgages, and multi-generational roles are helped by durability. With the right Life Insurance Policy, those commitments remain in place even if you are not. It’s one of the most straightforward ways to get a family’s momentum going in the right direction.

Advisors see the patterns families often overlook. They review timelines, priorities, and existing structures to build a more complete layer of protection. Their insight helps families understand how much insurance fits their world today. This guidance reduces uncertainty and builds confidence for the road ahead.

Online tools offer a clear starting point, especially when comparing ranges and costs. But families with layered responsibilities usually benefit from deeper conversations about structure. The right Life Insurance quote online should help spark direction, not replace personalized planning. A blended approach gives the strongest results.

Yes — it is one of the few forces that brings stability to a stage of life in which everything moves so quickly. In the case of raising young children, responsibilities span education, care, and long-term support. If something unexpected interrupts the plan, coverage helps keep those priorities afloat. It enables both parents to build confidence that their work will not disappear regardless of what happens.

Strong protection doesn’t always require large adjustments. Instead, it often starts with choosing the right structure and reviewing it regularly. Even in a period of rising costs, families can build plans that fit their pace. The goal is maintaining financial protection, not adding more stress.

Yes, extended support is increasingly available now, and adds an extra layer to longer-term planning. Whether providing support for the daily necessities or time until income is restored, strong Life Insurance prevents financial burden. It prevents adult kids from becoming a drain on the household, giving them time to get back on their feet. That allows the family’s path to remain open and smooth.

Sources and Further Reading

- Statistics Canada – Families & Households Portal

(Stable portal covering late-life parenting trends, household income, and Canadian families)

- Globe and Mail – Personal Finance Section

(Covers older parents, rising financial obligations, Life Insurance trends in Canada)

https://www.theglobeandmail.com/personal-finance

- Government of Canada – Benefits, Families, and Financial Support Portal

(Authoritative resource for Canadians with dependents, financial responsibilities, and family needs)

Key Takeaways

- Older parents in Canada face a widening Life Insurance Coverage gap as financial obligations pile up later in life.

Rising responsibilities, shifting priorities, and stretched household income leave many families without enough protection when support matters most. - Delayed family planning increases the need for stronger financial protection, not less.

With younger children at home and ongoing commitments, older parents carry risks that benefit from well-structured Life Insurance solutions rather than guesswork. - Term and permanent options each play a different role in securing a family’s financial future.

Some households need clear short-term protection through Term Life Insurance, while others rely on permanent choices and cash value benefits to support long-term goals. - Affordability concerns often stop families from reviewing their insurance policy, even when needs have grown.

A simple conversation about how much coverage fits today’s reality can close gaps before they become costly problems. - Joint first-to-die and joint last-to-die structures give older parents flexibility in protecting family members and managing estate goals.

These insurance solutions help balance rising expenses while keeping protection strong and reliable. - Online tools help families compare options, but personalized guidance brings clarity to complex needs.

A Life Insurance quote online is a starting point; expert planning ensures the coverage aligns with the family’s full financial plan. - Financial protection becomes more important as responsibilities expand with age.

Older parents shoulder more than many Canadians realize, and proper Life Insurance keeps their family steady through sudden change.

Feedback Questionnaire:

We’d love to understand what you’re facing so we can guide you better. Your answers help us create solutions that actually fit your life, not someone else’s.

IN THIS ARTICLE

- Why Many Older Parents In Canada Are Underinsured?

- The Growing Life Insurance Coverage Gap Among Canadian Parents

- Why Many Older Parents Lack Proper Life Insurance Protection

- How Life Insurance Works For Older Parents With Higher Financial Obligations

- Insurance Solutions Older Parents Should Consider Right Now

- How Much Coverage Older Parents Really Need

- How Canadian LIC Helps Older Parents Secure Proper Life Insurance Protection

- Securing Your Family’s Financial Future Before It’s Too Late

Sign-in to CanadianLIC

Verify OTP