Get ready to enter the world of life insurance, where safety and protection are woven together like a beautiful fabric. When it comes to making financial decisions, there are two main types of insurance: Term Life Insurance and Whole Life Insurance. But many don’t know how they are different from one another.

Term Life Policy is just like a temporary shield for a period of time. It provides the same kind of protection that Whole Life Insurance Policy offers, but only for a particular time.

We are here today not to let you get lost in all these complications of the differences between Term Life Insurance and Whole Life Insurance and to make you understand Term Life Insurance and Whole Life Policies better.

Let’s walk through this knowledge together and find a way to achieve financial peace of mind.

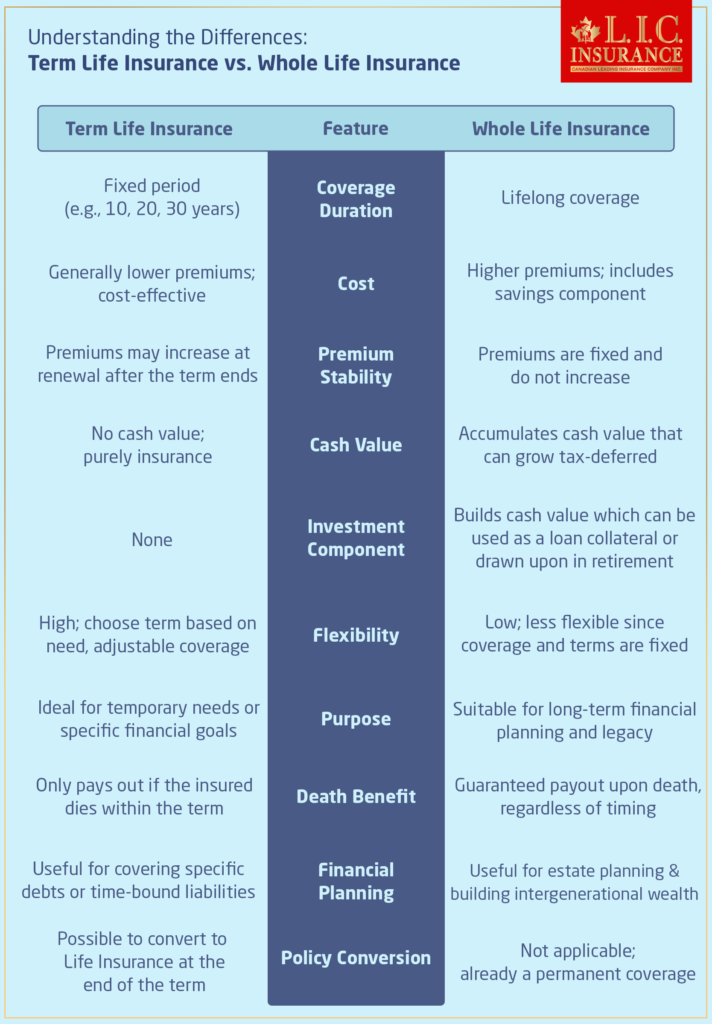

Understanding the Differences: Term Life Insurance vs. Whole Life Insurance

Before making a decision on which policy to go for, it’s helpful to have a good grasp of the subject. Term Life Insurance is like getting an apartment in the world of real estate: no equity is involved in the purchase, but it is cheaper and simpler. On the flip side, Whole Life Insurance Policy is like buying a house with higher costs but with the promise of long-term benefits and asset accumulation.

Take Anita, a young professional and 30-year-old graphic designer who has just recently started her freelance journey. He has the classic Young Professional dilemma: “How in the world do I get affordable insurance coverage without sacrificing future financial stability?” Anita’s story will enable us to get into the features of a Term Life Insurance Plan or Term Life Insurance benefits, pointing at reasons that may make it the right decision for people in such situations.

Term Life Insurance—Affordable and Flexible

Term Life Insurance provides protection over a certain period, say from 10 to 50 years, making it an attractive option for people like Anita. It merely means that on the occurrence of death within the term, the company pays the beneficiaries. The rates are what make this policy attractive. The Term Life Insurance rate in 2025 is reasonably low, making it possible for young professionals, first-time parents, and homeowners to get financial security without having to spend a lot of money.

Customizing Your Plan

The Term Life Insurance could be based on your life timeline. It may just be the period when you will need this coverage to a point when the mortgage is paid off or when children have completed college. This personalization guarantees not only that your insurance should bear direct relation to the times in life when one is most financially vulnerable but also that insurance is kept at reasonably manageable costs.

Eliana, a single mother of two, opted to take the 20-year Term Life Insurance Plan. The goal? To secure the educational future of her children in case something happens to her way before the children reach adulthood. Emily’s story tells about the practicality and direct benefits of Term Life Insurance to a parent.

Whole Life Insurance—Comprehensive and Continuous

On the other hand, Whole Life Insurance is an insurance policy underwritten to cover an individual for the entire life since the commencement of the policyholder’s term. This kind of life insurance policy has no expiry, as compared to Term Insurance. It does provide coverage so long as there are premiums paid. It also includes an investment component that is termed ‘cash value’ and the cash value component grows on a tax-deferred basis.

Building Cash Value

This part of the policy works somewhat like a savings account, accumulating funds from which to borrow when needed. It is usually designed to grow at a guaranteed rate, so it may look attractive if you are seeking a single product for insurance and investment benefits.

John, a retired police officer, decided to settle for Whole Life Insurance at the age of 48. His idea was to provide both a safety net for his wife at the time of his death and something to pass down to the grandkids. The Whole Life Insurance really gave him peace of mind because he knew that his premiums would never go up and the cash value of the policy could serve the generations.

Making a choice—Which is Better for You?

Deciding whether to go with Whole Life Insurance Policies or Term Life Insurance can be overwhelming, but viewed through the prism of your current financial situation, your long-term goals, and certainly the needs of your loved ones, it becomes manageable. Let’s unpack these options, highlighting their differences.

Assessing Your Financial Goals

It is very crucial to make the right decision on the kind of life insurance that meets your set objectives. The following question will help to guide you: Do you need protection that is only for the short run, or are you building a legacy that extends past your lifetime? Here is what you should consider:

Coverage Duration

- Term Life Insurance: It is insurance for a certain term, e.g., 10, 20, 30, or 50 years. This type of life insurance would be ideal for you if you are to fill up with a certain financial vulnerability period, e.g., time your children graduate from college or till your mortgage gets paid off.

- Meet Tom, a new father in his mid-30s, who recently purchased a Term Life Insurance Plan. Tom opted for a 20-year term that aligns with his goal of providing for his children’s education and securing their young adulthood, reflecting the current Term Life Insurance rates for 2025. His decision was driven by the desire for affordability and the certainty that his family’s primary financial needs would be temporarily covered.

- Whole Life Insurance: It lasts for the entire life of the insured, ensuring that the insured is under coverage, whichever number of years he lives. This alternative is eligible for those who would like to leave a financial legacy or use the policy as a tool in their estate planning.

- Real-Life Scenario: Sambhavana is an established businesswoman who went for Whole Life Insurance to ensure that her estate bears benefits from her lifelong efforts. With the cash value that will have been accumulated through her policy, the heir will be using it for whatever reasons, together with the death benefit, as it secures her legacy.

Investment Component

- Term Life Insurance: This does not involve investment. It is purely an assurance cover, meaning it is cheap and straightforward but does not accumulate any value over the term.

- Real-Life Scenario: Think of Rajesh, who wanted very basic life insurance without any frills to it. Raj found that Term Life Insurance was much cheaper, and the Term Life Insurance rates in 2025 allowed him to take the savings and put it in other investments. This was quite an economically wise decision.

- Whole Life Insurance: Whole Life is a kind of life insurance policy under which the money acquires cash value against the policy, and from that, money can be loaned out. It provides a forced saving plan and provides financial options in the later years of one’s life.

- Real-Life Scenario: Laila, on the other hand, preferred the cash value aspect of Whole Life Policies. Her premiums are higher, but part of those payments goes toward the cash value growing at a guaranteed rate, providing part and parcel to further financial security while also offering an opportunity to borrow against this cash reserve if need be.

Premium Stability

- Term Life Insurance: Term Life Insurance – Generally, this has lower premiums but can increase if you choose to renew after the term has lapsed. This is best for those who require lower life insurance costs in coverage and do not mind the uncertainty that may follow in the rates.

- Real-Life Scenario: Among the good examples of the Term Life Insurance Plan is its low initial cost, which enticed Alex to take it because it would offer flexibility within his tight budget owing to the low premiums he would pay. However, he knows that choosing to renew the policy after the term period will come with higher Term Life Insurance rates.

- Whole Life Insurance: While it has higher premiums than Term Life Insurance, the premiums remain level and consistent for as long as the policyholder lives, providing both predictability and stability.

- Real-Life Scenario: Melissa appreciated the stability of the Whole Life Insurance premiums. While the cost of Whole Life Insurance was significantly higher in comparison with Term Insurance, knowing that her premiums would not grow higher over time helped her plan long-term finances and gave her a sigh of relief for future cost hikes.

Conclusion: Why Act Now?

As we close in on our journey, remember that the choice of the right insurance is not an option to cover probable risks but a prudent investment towards your and your family’s future. With Term Life Insurance Plans specific to your requirements and competitive Term Life Insurance rates for 2025, Canadian LIC allows you to cover your needs affordably, effectively, and instantaneously. Don’t wait for something bad to happen to tell you that you need to be safe. Contact Canadian LIC today to help protect a financially stable future for you and your loved ones.

By understanding every road, as Anita and John did, one can surely make a solid decision that will not only meet one’s current needs but also lay out the ground for a secure future. That just makes the decision easier when one is further down the path with Whole Life Insurance or flexible, affordable Term Life Insurance. Decide now, and ensure today’s insurance decision lives on as an integral part of your tomorrow.

Find Out: How to buy Term Life Insurance?

Find Out: The main disadvantage of Term Life Insurance

Find Out: What is the longest Term Life Insurance you can get?

Find Out: Why to get Term Life Insurance?

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Frequently Asked Questions on Term Life Insurance Policy

The main difference between term vs Whole Life insurance is the duration and benefits. Term Life Insurance covers you for a specific period, like 10, 20, or 30 years, and is generally more affordable. Whole Life insurance provides lifetime coverage and includes a cash value component that grows over time. Term Insurance is often best for temporary needs, while Whole Life offers permanent protection and long-term value.

When comparing term vs Whole Life insurance cost, Term Insurance is significantly more affordable upfront. For instance, a healthy 35-year-old might pay $25/month for Term Insurance but over $200/month for Whole Life Coverage with the same death benefit. Whole Life is costlier because it includes lifelong coverage and a savings feature, while term is designed for budget-conscious, time-limited protection.

Here are the term vs Whole Life insurance pros and cons:

- Term Life Pros: Lower premiums, simple to understand, great for short-term needs like mortgage protection.

- Term Life Cons: No cash value, expires after a set term.

- Whole Life Pros: Provides lifetime coverage, builds cash value, and is good for estate planning.

Whole Life Cons: Higher cost, less flexible in early years, and can be complex.

Choosing term or Whole Life insurance for seniors depends on your goals. Term Life Insurance may suit seniors with short-term needs, like covering final expenses or outstanding debts. Whole Life may be better for those wanting to leave a guaranteed inheritance or cover lifelong needs. Seniors should also consider health status and budget when deciding between the two.

Yes—if you value lifelong protection, fixed premiums, and a cash value you can access. It’s especially worth it for those planning for estate taxes, long-term wealth transfer, or guaranteed coverage regardless of health changes. However, if the budget is tight and needs are temporary, term life might be a better fit.

So, the right choice from among Term Life Insurance Plans is a matter of thinking over your personal and financial position. What do you need the coverage for, and for what time? For example, there is Michael, a father to two very young children who just opted to take up a 30-year Term Life Insurance so that his children would be well provided for the duration of the years that they would go schooling. That is, compare the plans available and consider how the coverage supports your goals, just like Michael did; you should be able to find a Term Life Insurance Plan that best fits your life stage and financial objective.

The major difference lies in the period and financial gains. Term Life Insurance is a specific type of period insurance, and it pays out its benefits only if a person dies during the term of his insurance. On the other hand, Whole Life Insurance covers your Whole Lifetime and also includes some form of savings that will increase with time. For instance, Lisa had the only chance of Term Life Insurance since she needed cheap cover only up to a point in time when her mortgage would have been fully repaid, while Mark had the opportunity of lifetime cover through Whole Life Insurance and the opportunity to build cash value.

Yes, most Term Life Insurance Policies do come with an option for the policyholder to convert it to Whole Life Insurance. Sam had first bought a term plan for the much lower premiums at that point in time. As his financial needs improved and changes occurred, the need arose to change the policy to a Permanent Life Insurance, that of a Whole Life Insurance Policy, so that over some time, he could enjoy the growth of cash value. Please check with your insurance provider for specific terms and conversion options in your policy.

Term Life Insurance is one of those sorts of life insurance that has changeable life insurance rates by age, health condition, and economic situation. When Karen first shopped for Term Life Insurance Policy at the very tender age of 25, the rates looked incredibly low. But when at 35 she went for another policy, the rates had increased as she had grown older and had slight health changes.

If you outlive your Term Life Insurance Plan, the coverage ends and you do not receive a payout. That’s what happened to Tony; he did outlive his 20-year term policy. Though now he is relieved to be healthy and active, at the end of the term, he could derive no benefits from the policy. To avoid that situation, keep a lookout for options in renewal or take up Whole Life Insurance, which provides cover for the whole of the lifetime.

Finding the most affordable Term Life Insurance rates in 2025 means soliciting and obtaining quotes from several providers. Anna paid much less as she had checked several life insurance companies. She used to use several agents who did not have information and used to negotiate the best prices using online comparison tools. So scrutinize the offer from any company like Anna did, making sure the plan is equal to your needs without being overpriced and overstretching your budget.

When choosing a Term Life Insurance Plan, you should consider factors such as the length of coverage, the amount of the death benefit, your current health, and your financial obligations. A 40-year-old parent, for example, with two children who are at a young age and schooling, had chosen 20-year Term Life Insurance until the time these children finished school and were already standing on their own feet. He considered his debts, the costs of educating his children, and his savings to determine how much coverage could ensure the future support of his family.

Your health significantly affects Term Life Insurance rates; healthy individuals usually acquire lower rates. Take the case of Priya, who, at 30, has a favourable rate based on being very healthy and a non-smoker. Her friend Laura, who had a couple of health problems and smoked, was quoted a higher rate for the same coverage. It should, therefore, be best advised that you apply for life insurance at an early and healthy stage in order to lock in those low rates.

Yes, that is true. Most of the time, when you buy a Term Life Insurance Policy at a young age, it comes with several benefits attached, such as lower premiums and a long coverage time. Take the example of Kevin, who bought a Term Life Insurance Plan at the age of 25. He is actually securing his policy at such a young age, wherein low rates have been locked, and is unaffected by his aging or any potential health issues that could have led to higher premiums if he had waited until later in life.

Family health history would be something that will affect your Term Life Insurance Plan since it’s a very important factor when it comes to accessing risk. This is what Elena learned when she took insurance. She was asked if any of her family members were diagnosed with any disease, and her answer was the heart disease of her grandfather. Full medical records for the history of her family will be required, which shall be determinative to influence premium rates. There is a need to be upfront with the family history of health in determining the right coverage.

Remember, prepare to make adjustments in some cases by revisiting your policy and other options if and when Term Life Insurance needs change. For example, Neil learned that the first policy was not enough when he got married and had a baby. He had contacted his insurance company to increase his death benefit and policy term so that he might be better secured in the future.

Armed with the knowledge from these FAQs, you will be able to easily navigate the alternatives between term and Whole Life Insurance to ensure the decision you are making best fits your long-run financial and personal well-being. Being proactive, will help you secure not just coverage but the RIGHT coverage for your family and you.

Sources and Further Reading

To enhance your understanding of Term Life Insurance rates for 2024 and various life insurance plans, consider exploring these reputable sources and materials:

Life Insurance Management Research Association (LIMRA) – For up-to-date research and statistics on life insurance trends and ownership. Visit their website at LIMRA.

Insurance Bureau of Canada – Provides comprehensive resources on different types of insurance available in Canada, including detailed guides on life insurance policies. Access their resources at Insurance Bureau of Canada.

Financial Consumer Agency of Canada – Offers consumer information on choosing life insurance, understanding different types of policies, and managing insurance effectively. Their website is a reliable source for Canadian financial products at the Financial Consumer Agency of Canada.

Canadian Life and Health Insurance Association (CLHIA) – A detailed guide to life and health insurance in Canada can be found on their website, which includes tips on selecting the right policy at CLHIA.

Investopedia: Term Life Insurance – For a clear, concise explanation of what Term Life Insurance is, including its benefits and drawbacks. Investopedia’s Term Life Insurance Guide is an excellent starting point.

NerdWallet: How to Choose Between Term and Whole Life Insurance – Offers a practical approach to deciding between term and Whole Life Insurance, suitable for those new to the topic. Check out NerdWallet’s Insurance Comparison.

These sources will provide you with a solid foundation of knowledge to help you navigate the complexities of life insurance, ensuring that you make informed decisions based on current trends and reliable information.

Key Takeaways

- Term Life Insurance offers temporary, cost-effective coverage, ideal for specific life stages or financial obligations.

- Whole Life Insurance provides permanent coverage and includes a cash value component for long-term financial planning.

- Term Life Insurance is affordable and flexible, with options to convert to Whole Life for extended protection.

- Choosing between term and Whole Life Insurance should align with personal financial goals and dependent needs.

- Monitoring Term Life Insurance rates for 2024 is essential for timely and cost-effective policy decisions.

- Consulting with insurance experts or financial advisors is recommended to ensure well-informed insurance choices.

Your Feedback Is Very Important To Us

Your feedback is invaluable to us, and we appreciate the time you took to help us understand your needs better. Thank you for participating!

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com