- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

7 Common Life Insurance Mistakes To Avoid

By Pushpinder Puri

CEO & Founder

- 20 min read

- May 12th, 2025

SUMMARY

Know seven common mistakes Canadians make when they buy Life Insurance online. It offers expert guidance from Canadian LIC on how to avoid costly errors, such as delaying purchase, underestimating inflation, or ignoring policy details. The blog helps readers choose the right Life Insurance Plans by sharing real client experiences, data-backed insights, and practical steps to ensure financial security for their families.

Introduction

If you’re thinking about purchasing Life Insurance online, your objective is probably straightforward: You want your loved ones to be financially secure. However, many Canadians unintentionally make errors that undermine this security. At Canadian LIC, clients frequently tell us of their regrets for decisions that they made without a full understanding of the implications. It could be because you’ve felt lost in all the jargon or bewildered by the types of policies and the different levels of coverage, but these feelings are common and can be avoided.

Here are seven common but easily avoidable Life Insurance mistakes you should avoid to protect your family’s long-term financial security.

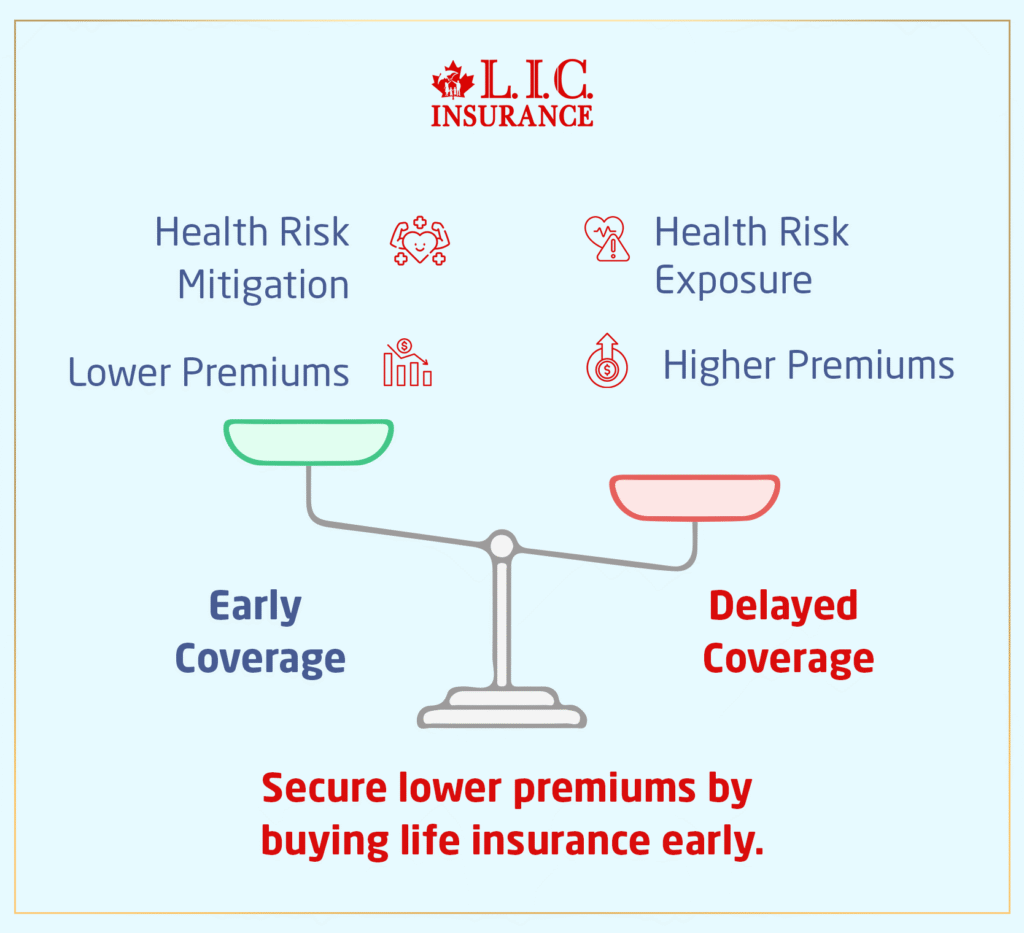

Mistake #1: Putting Off Buying Life Insurance Coverage

Canadians often put off to buy Life Insurance online since they feel they do not need it at a younger age. But waiting means the premiums will be higher. As per figures provided by the Canadian Life and Health Insurance Association (CLHIA), younger applicants receive rates that are a fraction of what seniors get quoted. Policies get more costly as you get older.

By delaying, you could be hit with higher premiums thanks to undiagnosed health problems or because you’ve aged into a different rate class. Early coverage is a tremendous saving and peace of mind.

- Purchase your policy early to lock in lower rates.

- Even if your current obligations are minimal, early coverage is beneficial.

- Early insurance provides financial security during life’s unpredictable events.

Mistake #2: Choosing Policies Based Only on Cost

Opting for the least expensive policy may appear to be a good idea at first, but it typically leads to insufficient coverage. Some of these policies may look cheap at the outset, but do not necessarily cover your family’s financial future.

Too many individuals in Canada are willing to pay the price and overlook the value, and it makes their families more financially insecure. Low-cost policies often have fine print limitations, few benefits and inadequate payouts.

- Evaluate your family’s specific financial needs thoroughly.

- Choose Life Insurance Plans that cover all essential expenses, not just the cheapest premium.

- Analyze the long-term benefits versus immediate cost savings.

Mistake #3: Not Fully Disclosing Your Health History

Incomplete medical disclosures frequently lead to claim denials. Insurance companies meticulously review health records, and undisclosed conditions can jeopardize your coverage.

Transparency is vital. Canadians often underestimate the seriousness of omitting minor medical conditions, which later results in claim rejections. Full disclosure prevents future disputes and ensures smooth claim processing.

- Always provide full, honest medical information.

- Clarify uncertainties upfront with your insurer to avoid problems later.

- Discuss your medical history openly with insurance representatives.

Mistake #4: Forgetting to Update Beneficiaries

Beneficiary listings are one of the easiest things to overlook as life moves quickly. Unintentionally, payments end up in the hands of outdated recipients, leading to tragic unintended consequences for families.

Such insufficient oversight of beneficiary information may lead to negative consequences. Canadians also tend to forget about making updates after major life changes have occurred, causing disputes between family members and financial challenges, she adds.

- Regularly review your beneficiaries, especially after major life events such as marriage, divorce, or childbirth.

- Set an annual reminder to check your Life Insurance details.

- Inform beneficiaries clearly about their roles and rights.

Employees have the right to paid vacation based on their years of service. Companies working with Canadian LIC often ask us how to balance operational needs with providing generous vacation leave—we help them draft smart policies that meet both needs.

Mistake #5: Neglecting Regular Policy Reviews

Your Life Insurance Policy isn’t something you set once and ignore. As your life evolves, your coverage should evolve, too. Families often realize too late that their insurance coverage no longer matches their Life Insurance needs.

Regular policy reviews ensure that your coverage aligns with your current financial responsibilities. Many Canadians neglect periodic assessments, leading to significant coverage gaps over time.

- Schedule annual policy evaluations.

- Update your coverage based on changing debts, family needs, and responsibilities.

- Maintain an active dialogue with your insurance provider for regular check-ins.

Mistake #6: Ignoring Policy Details and Exclusions

There are many Canadians who don’t pay attention to the details of the policy, in particular, exclusions for certain conditions or high-risk activities. This is a detail not to overlook, because you won’t know just how much of a surprise it is when it comes to claims.

Failure to thoroughly read the policy fine print may result in misunderstandings. Canadians often believe their policy is all-encompassing without questioning where they stand in relation to the terms, conditions and limitations, only to become upset at a time when they can least afford the added stress.

- Carefully read your entire policy document.

- Ask your provider about any unclear terms or specific exclusions.

- Request clarification or a summary of exclusions to avoid future surprises.

Mistake #7: Overlooking the Effects of Inflation

Inflation significantly erodes your policy’s value over time. Canadians frequently underestimate inflation’s impact, resulting in insufficient coverage as time passes.

Ignoring inflation leads to the gradual erosion of your policy’s purchasing power. The amount you initially deem sufficient may prove inadequate years later, leaving your beneficiaries financially exposed.

- Factor inflation into your initial coverage calculation.

- Regularly review and adjust your policy to match rising living costs.

- Use inflation calculators to reassess your financial coverage requirements regularly.

Additional Insights to Maximize Your Life Insurance Coverage

Mistake #8: Not Considering Your Debt Obligations

Canadians don’t always take their debt into account when deciding how much Life Insurance to buy. One must take into account mortgages, car loans, student loans, credit card balances and the like. If these responsibilities are not well localized, your heirs may inherit financial obligations.

- Figure out the sum total of what you owe.

- Make certain your coverage will be adequate to discharge these responsibilities.

- Revisit your insurance needs as your debts and dependents evolve.

Mistake #9: Overestimating Employer Coverage

Employer-provided Life Insurance often gives Canadians a false sense of security. Typically, such coverage is limited and ends when employment terminates.

- Treat employer insurance as supplemental rather than primary coverage.

- Purchase individual coverage independently for continuous protection.

- Assess your employer’s coverage regularly to understand its limitations.

Mistake #10: Relying on Temporary Solutions

Temporary or short-term policies might seem attractive due to lower initial costs. However, long-term financial protection requires policies that don’t expire prematurely.

- Evaluate permanent Life Insurance for lifelong coverage.

- Balance term and permanent policies strategically.

- Seek expert advice for a balanced insurance portfolio.

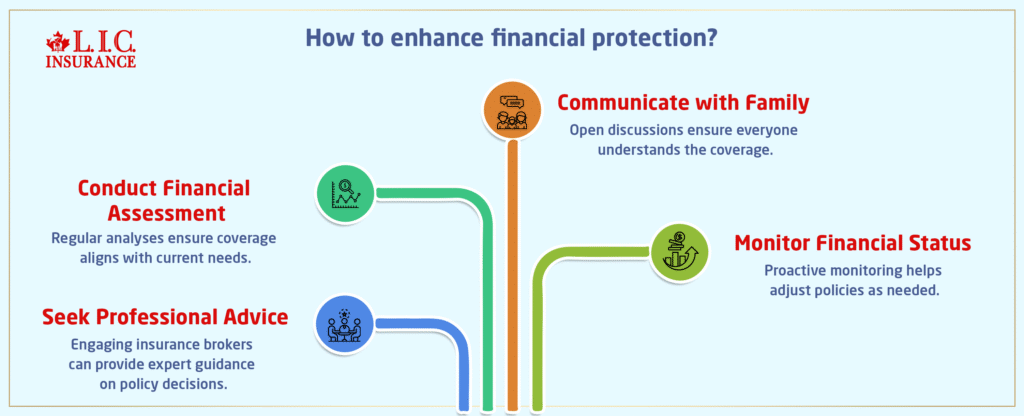

Practical Steps for Enhanced Protection

- Utilize Professional Advice: Engage experienced insurance brokers to guide your decisions.

- Comprehensive Assessment: Conduct thorough financial needs analyses regularly.

- Open Family Communication: Clearly discuss policy details and coverage with family members.

- Proactive Monitoring: Regularly monitor your financial status and policy performance.

By taking these steps proactively, you can be sure that your Life Insurance Plans deliver sufficient and ongoing financial assistance for your family. Sound life insurance planning requires constant monitoring, thoughtful refinements, and cohesive coordination.

By intentionally steering clear of these typical insurance errors, you set yourself up for strong financial risk management. Life Insurance is not just about planning for a worst-case scenario, it’s about giving your family the ability to stay on their feet and flourish even when the going gets tough.

Remember to:

- Buy your Life Insurance Policy just as soon as you can.

- Consider coverage holistically, not just in terms of price.

- These people need to answer questions about their health completely and accurately.

- Keep your beneficiaries and coverage information current.

- Know policy exclusions and fine print.

- Make sure you adjust your coverage periodically for inflation and life changes.

As a well-informed, proactive and comprehensive decision maker around Life Insurance, ready your family for any eventuality.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs: Common Life Insurance Mistakes People Don't Talk About Enough in Canada

No, not really. We’ve seen too many couples assume that one policy is enough for the household. But if something happens to the uninsured partner, there’s no financial cushion. Each adult should have their own Life Insurance Plan based on their income, debts, and responsibilities, not just shared assumptions.

This depends on the type of policy and how the funds are structured. For instance, permanent policies with cash value might impact means-tested programs, but term life usually doesn’t. It’s worth checking with a financial advisor before committing if you receive or may apply for government aid.

That depends on your goals. Life Insurance isn’t only for people with kids. If you want to leave money behind to help your parents, pay off joint debts, donate to a cause, or cover funeral costs so no one else has to, it’s still worth considering. Think legacy, not just dependents.

Not necessarily. But don’t cancel your current policy until the new one is approved and active. People make the mistake of chasing lower premiums without reading the new terms properly—or worse, they get denied and end up uninsured. Comparison is smart, but timing is everything.

It can. If a child under 18 is named directly, the payout might be delayed or tied up in a trust until a legal guardian is appointed. It’s better to set up a trustee or legal guardian in the policy so everything moves smoothly if the unexpected happens.

Yes. Good health means you’ll likely qualify for lower premiums. And while savings are great, they’re not always liquid or protected from taxes or probate. Life Insurance delivers a lump sum—fast and tax-free—which isn’t something all assets can do.

Yes, especially if it’s a change from what you initially disclosed. A few clients working in construction or aviation learned this the hard way. If your new activities fall under exclusions and you don’t notify your provider, claims can be jeopardized later.

Unfortunately, yes. If there are discrepancies in your application, questionable beneficiary designations, or family disputes, claims can be delayed or denied. Being clear, honest, and organized with your policy details can make a huge difference for those left behind.

It depends on your provider and policy terms. Some Canadian policies remain in force internationally, others don’t. If moving abroad is in your plans, you’ll want to confirm portability—or consider switching to a global insurer before the move.

It can be, but only if the discounts are real and the products suit your situation. We’ve seen bundling packages that looked attractive but were packed with features people didn’t actually need. Always review each product on its own merits before bundling.

Key Takeaways

- Delaying Life Insurance leads to higher premiums—buy Life Insurance online early to save more long-term.

- Cheapest isn’t always best—choosing a policy based solely on price often results in gaps in Life Insurance Plans.

- Full health disclosure is essential—missing medical details can cause claim denials.

- Beneficiaries must be updated—outdated names on policies can cause delays or disputes.

- Annual policy reviews matter—your needs change, and so should your Life Insurance.

- Inflation erodes value over time—reassess coverage to keep it aligned with rising costs.

- Employer Life Insurance is not enough—treat it as a bonus, not your main plan.

- Temporary fixes can be risky—mix term and permanent policies for balanced protection.

- Policies may need updating if your lifestyle changes—like moving abroad or changing jobs.

- Avoid minor technical errors—missteps in naming minors as beneficiaries or bundling the wrong products can create future issues.

Sources and Further Reading

1. Putting Off Buying Life Insurance Coverage

- Canadian Life and Health Insurance Association (CLHIA): Life Insurance Basics

- Why Buy Life Insurance Young? – Canada Life

2. Choosing Policies Based Only on Cost

- Government of Canada: Types of Life Insurance

3. Not Fully Disclosing Your Health History

- CLHIA: The Importance of Full Disclosure

- Sun Life: What Happens If You Lie on Your Life Insurance Application?

4. Neglecting Regular Policy Reviews

- Sun Life: How Often Should You Review Your Life Insurance?

5. Ignoring Policy Details and Exclusions

- Government of Canada: Understanding Insurance Policies

Feedback Questionnaire:

IN THIS ARTICLE

- 7 Common Life Insurance Mistakes To Avoid

- Mistake 1: Putting Off Buying Life Insurance Coverage

- Mistake 2: Choosing Policies Based Only on Cost

- Mistake 3: Not Fully Disclosing Your Health History

- Mistake 4: Forgetting to Update Beneficiaries

- Mistake 5: Neglecting Regular Policy Reviews

- Mistake 6: Ignoring Policy Details and Exclusions

- Mistake 7: Overlooking the Effects of Inflation

- Additional Insights to Maximize Your Life Insurance Coverage

- Practical Steps for Enhanced Protection

Sign-in to CanadianLIC

Verify OTP