As time goes on, the savings part of Permanent Life Insurance grows. This type of insurance covers you for the rest of your life. This kind of insurance costs more than Term Life Insurance, but it has both a death payment and a savings part that earns interest without being taxed.

Two fundamental types of spiritual journeys are whole life and universal life Whole Life Insurance guarantees that the cash value will grow over time, while Universal Life Insurance lets you change your payments, and the growth depends on market rates. With changes like variable life and variable universal life, you can put the cash value into a number of different financial investments.

Once you’ve chosen the right policy, research the insurance companies thoroughly to get the best insurance available.

Understanding Permanent Life Insurance

Permanent Life Insurance is a lifelong coverage plan. Permanent Life Insurance covers you for all of your life, while Term Life Insurance only covers you for a certain amount of time. As long as the payments are paid on time, this insurance will cover the policyholder for their whole life. The regular payments are what keep the insurance going. They pay for both the death benefit and the cash value.

The best thing about this insurance is that it serves two purposes at once: it protects loved ones financially after the policyholder dies and also builds up a cash balance over time. This savings account, called the “cash value,” grows slowly with each insurance payment. Like a savings account related to insurance, this cash value keeps going up over time.

What’s interesting about this cash value is how flexible it is. It’s not just there; it’s there for you when life throws you a cash curveball you didn’t see coming. You can borrow money against this cash value or even take money out of it if you need to. It’s like having an emergency fund that grows along with your insurance. This cash value can be your reliable source of cash in case of emergency hospital costs, your child’s college fees, or any other pressing need.

The fact that this strategy is always the same is one of its excellent features. Permanent Life Insurance goes with you for the rest of your life, while Term Life Insurance ends. As long as those premiums keep coming in, the insurance will stay in place and protect you while building up your cash reserve.

The cash value gives you extra financial security that Term Life Insurance doesn’t offer by letting you borrow money or take it out like having a safety net to protect you from the sudden turns and changes that life can take. This freedom gives you a sense of financial security and peace of mind, knowing that you have extra money in case you need it.

In addition, the accumulation of cash value in a Permanent Life Insurance Policy can help you save money on taxes. The cash value grows tax-deferred, which means that as long as the money stays in the policy, you won’t have to pay taxes on the money that has grown. In addition, payments up to the total amount of premiums paid are often tax-free, which can help you with your financial planning.

For the most part, Permanent Life Insurance not only protects your family’s financial future but also acts as a long-term financial tool that changes with your wants and provides extra money when life takes an unexpected turn.

Tax Advantages

Permanent Life Insurance policies come with appealing tax advantages that make them an attractive long-term financial tool for many individuals. Understanding these tax benefits is crucial when considering the purchase of a Permanent Life Insurance policy.

One significant benefit is the tax-deferred growth of the cash value component. The cash value in a Permanent Life Insurance policy accumulates over time, and the interest it earns isn’t subject to immediate taxation. This tax-deferred growth allows the cash value to increase faster since taxes are deferred until you withdraw the funds. It’s like growing your savings without having to worry about yearly tax deductions.

Another notable advantage is related to withdrawals from the policy. Typically, withdrawals up to the total premiums paid into the policy are not taxed. This means that if you’ve contributed more in premiums than the value of the policy, withdrawing that amount is typically tax-free. It’s like accessing a portion of your savings without any tax implications.

However, it’s essential to note that beyond the total premiums paid, withdrawing additional funds could trigger taxes. Any amount taken out beyond what you’ve contributed may be subject to taxation. These withdrawals are generally considered as income and are subject to regular income tax rates. Moreover, if you surrender or cancel the policy entirely, any gains you’ve made above and beyond the premiums paid may also be taxable.

These tax advantages make Permanent Life Insurance policies not just a means of providing a financial safety net for your loved ones but also an efficient way to grow savings over time. The ability to accumulate tax-deferred funds and access them later without incurring immediate tax liabilities is a significant benefit for policyholders.

However, while the tax advantages of a Permanent Life Insurance policy are attractive, it’s crucial to consult with a financial advisor or tax professional. They can provide personalized guidance based on your individual circumstances and ensure you fully understand the tax implications of any withdrawals or policy surrenders.

In summary, the tax advantages associated with Permanent Life Insurance policies, such as tax-deferred growth and tax-free withdrawals up to the total premiums paid, can make them an appealing financial option for long-term planning and savings.

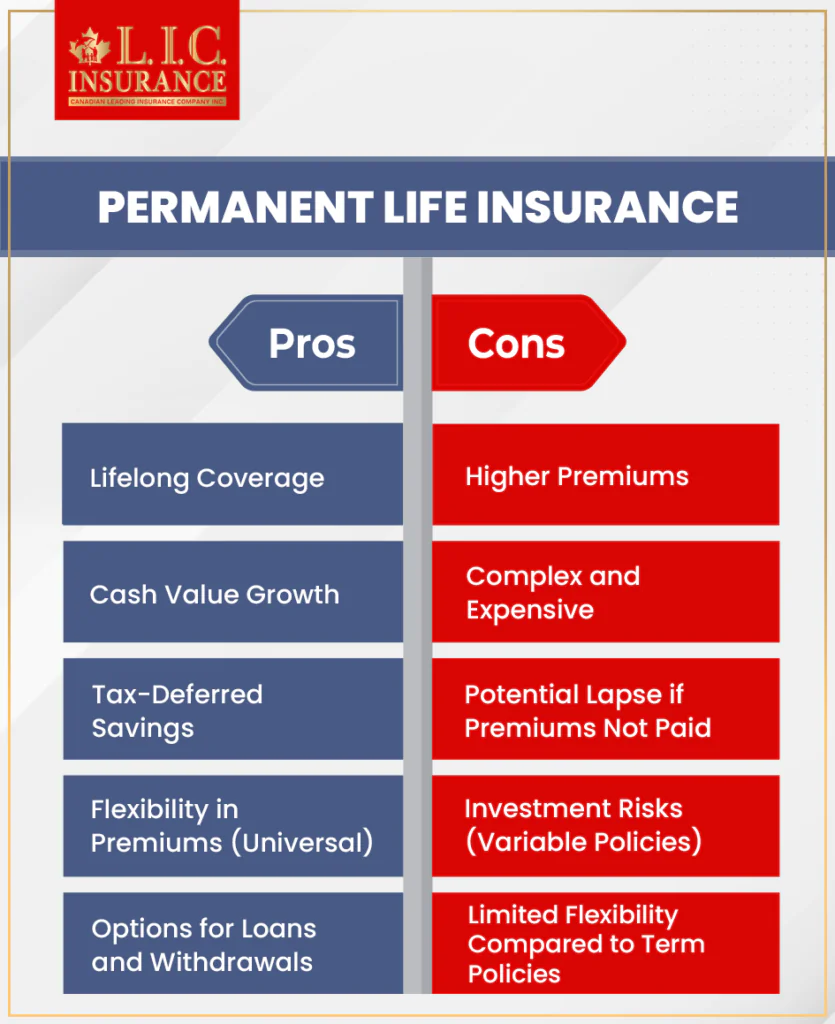

Pros and Cons

Pros:

Lifelong Coverage: Unlike term insurance, which has a specific duration, Permanent Life Insurance stays in force throughout your life as long as premiums are paid. This guarantees financial protection for your beneficiaries whenever you pass away. Savings Component: One of the notable features of Permanent Life Insurance is the cash value it accumulates over time. This cash value grows on a tax-deferred basis, meaning you don’t pay taxes on the earnings as long as they remain within the policy. This savings component acts as a financial cushion that policyholders can access during their lifetime. Tax Advantages: The cash value growth within a Permanent Life Insurance policy enjoys favourable tax treatment. The tax-deferred growth allows your money to grow faster since you’re not paying taxes on the earnings annually. Additionally, withdrawals up to the total amount of premiums paid are generally not subject to income tax.Cons:

Higher Premiums: Compared to Term Life Insurance, Permanent Life Insurance typically comes with higher premiums. These higher costs may make it less affordable for some individuals, especially those seeking significant coverage amounts. Reduced Death Benefits: While the cash value within a Permanent Life Insurance policy can be accessed through withdrawals or loans during your lifetime, doing so might decrease the death benefit. If you withdraw funds from the policy’s cash value or take a loan against it, it could reduce the amount your beneficiaries receive upon your death.Understanding these aspects can help in making a smart decision when considering a Permanent Life Insurance policy. It’s crucial to assess your financial situation and future needs before committing to a policy. While the lifelong coverage and savings feature is attractive, the higher premiums and potential impact on death benefits upon cash value withdrawals should be carefully evaluated.

Ultimately, consulting with a knowledgeable insurance advisor or financial professional can provide valuable insights into whether a Permanent Life Insurance policy aligns with your long-term financial goals and offers the security and coverage you seek for your family.

Permanent Life Insurance offers lifelong coverage and a cash value savings feature. It pays a guaranteed benefit upon death and provides tax advantages. While it involves higher premiums and potential reductions in death benefits upon cash value withdrawal, it can be a valuable long-term investment.

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Faq's

Permanent Life Insurance is a policy designed to cover you for your entire life, unlike term insurance, which has a set coverage duration. It includes a savings component called cash value, which grows over time.

There are various types: Universal life offers flexibility in premiums and benefits, whole life guarantees a cash value growth, while variable life and variable universal life allow investment options.

It depends on your needs. Term life is more affordable and covers a specific period, whereas permanent life lasts a lifetime and accumulates cash value but has higher premiums.

Yes, after a certain time, you can withdraw cash, take a loan against the policy’s cash value, or surrender the policy. However, these actions may incur fees and taxes.

As long as you keep paying the premiums and the policy remains active, Permanent Life Insurance provides coverage throughout your life.

Permanent Life Insurance offers a death benefit and a savings component. However, its investment aspect might not yield as high returns as other investment avenues.

If you stop paying premiums, the policy might lapse, and the coverage and cash value might be affected. Some policies may have a grace period before this happens.

Yes, some policies allow modifications or additions, such as adjusting coverage amounts or adding riders to tailor the policy to your changing needs.

Premiums for Permanent Life Insurance policies can be fixed or flexible, depending on the policy type and its terms. Some policies offer flexible payment options.

Yes, you can have multiple Permanent Life Insurance policies, but the total coverage across all policies should align with your financial needs and eligibility.

Cash value in a Permanent Life Insurance policy grows over time based on premiums and interest. It can be used for policy loans, withdrawals, or to pay premiums.

Yes, most permanent life policies have a surrender value, which is the amount you receive if you surrender the policy before its maturity or death benefit payout.

Upon the insured’s death, the beneficiaries receive the death benefit. The policy’s cash value is generally not paid out with the death benefit.

Some term policies offer the option to convert to Permanent Life Insurance without a medical exam. It’s a way to transition to lifelong coverage if needed.

The cash value growth is tax-deferred, and withdrawals up to the total premiums paid are typically tax-free. However, consult a tax advisor for specifics.

For certain policies, the cash value growth rate may be guaranteed, but it varies based on the policy type and insurer.

Yes, you can take a loan against the cash value of your policy, but it’s essential to understand the interest rates and potential impacts on the policy’s value.

Many permanent life policies offer riders that provide additional benefits, such as a waiver of premium or an accelerated death benefit.

Permanent Life Insurance can be a valuable tool for estate planning, offering tax benefits and liquidity to cover estate taxes or provide inheritance.

Premiums for Permanent Life Insurance tend to be higher as you age, so purchasing it when you’re younger might result in lower premiums.

Depending on the policy, you may have options to increase the death benefit by purchasing additional coverage or adjusting the policy.

Policyholders can cancel their Permanent Life Insurance policies, but doing so may involve surrender fees and a loss of coverage and cash value.

Your health can impact the premiums for Permanent Life Insurance. Generally, better health conditions lead to lower premiums.

Yes, you can name multiple beneficiaries for your Permanent Life Insurance policy, specifying the percentage of the death benefit each will receive.

In some cases, you might be able to transfer the ownership of a Permanent Life Insurance policy, but it’s subject to certain conditions and may require approval from the insurer.

Premiums for Permanent Life Insurance tend to be higher as you age, so purchasing it when you’re younger might result in lower premiums.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com