- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Find The Best 5-Year Fixed Mortgage Rates In Canada

By Harpreet Puri

CEO & Founder

- 20 min read

- January 28th, 2026

SUMMARY

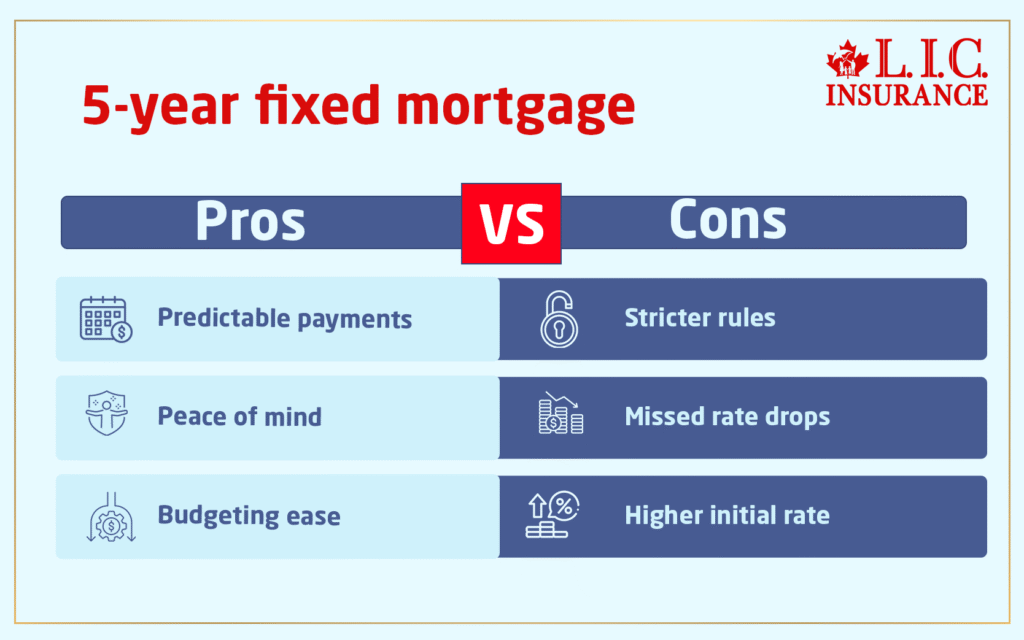

Most of the people who come to us are juggling enough already—job security, family needs, household budgets—and they don’t want to worry about interest rate spikes. That’s where the 5-year fixed mortgage fits in.

We recently sat down with a single mom in Hamilton who had just been approved for a mortgage. She said, “I just need to know that my fixed monthly payments aren’t going to change next year.” A fixed-rate gave her that sense of control.

Fixed means regular mortgage payments. You lock in your interest rate for five years, so you don’t have to keep an eye on rate announcements from the Bank of Canada. That helps with planning, especially after the elevated rate volatility Canadians experienced between 2022 and 2025.

But—and this is something we always point out—that fixed rate might come with stricter rules. Some lenders limit your ability to pay extra or get out early. So, you need to weigh that against the comfort of predictable payments.

Introduction

You’d be surprised how often people walk into Canadian LIC with a simple question that turns out to have a very layered answer: “Can you help me find the best 5-year fixed mortgage rate?” And while it seems like it should be as easy as looking up today’s rate on a bank’s website, the truth is, it’s never that straightforward.

We work with homeowners and first-time buyers every day—from Mississauga to Halifax—who want the same thing: a steady, reliable mortgage that won’t leave them guessing month to month. What they don’t always realize is that mortgage rates are only one part of the story. You’ve got to look at insurance premiums, your debt ratios, the mortgage lender’s policies, and even small legal details in the mortgage agreement.

Here’s what we’ve learned: the lowest rate doesn’t always save you the most money. And if you’re not careful, a fixed mortgage could cost you more than you expected, especially if life throws you a curveball halfway through the term. Let’s walk through what we tell our own clients when they ask about 5-year fixed mortgage rates—and how you can avoid the common traps.

Why People Lean Toward the 5-Year Fixed Mortgage

Most of the people who come to us are juggling enough already—job security, family needs, household budgets—and they don’t want to worry about interest rate spikes. That’s where the 5-year fixed mortgage fits in.

We recently sat down with a single mom in Hamilton who had just been approved for a mortgage. She said, “I just need to know that my fixed monthly payments aren’t going to change next year.” A fixed-rate gave her that sense of control.

Fixed means regular mortgage payments. You lock in your interest rate for five years, so you don’t have to keep an eye on rate announcements from the Bank of Canada. That helps with planning, especially when you’re watching every dollar.

But—and this is something we always point out—that fixed rate might come with stricter rules. Some lenders limit your ability to pay extra or get out early. So, you need to weigh that against the comfort of predictable payments.

Let's Talk About Mortgage Insurance

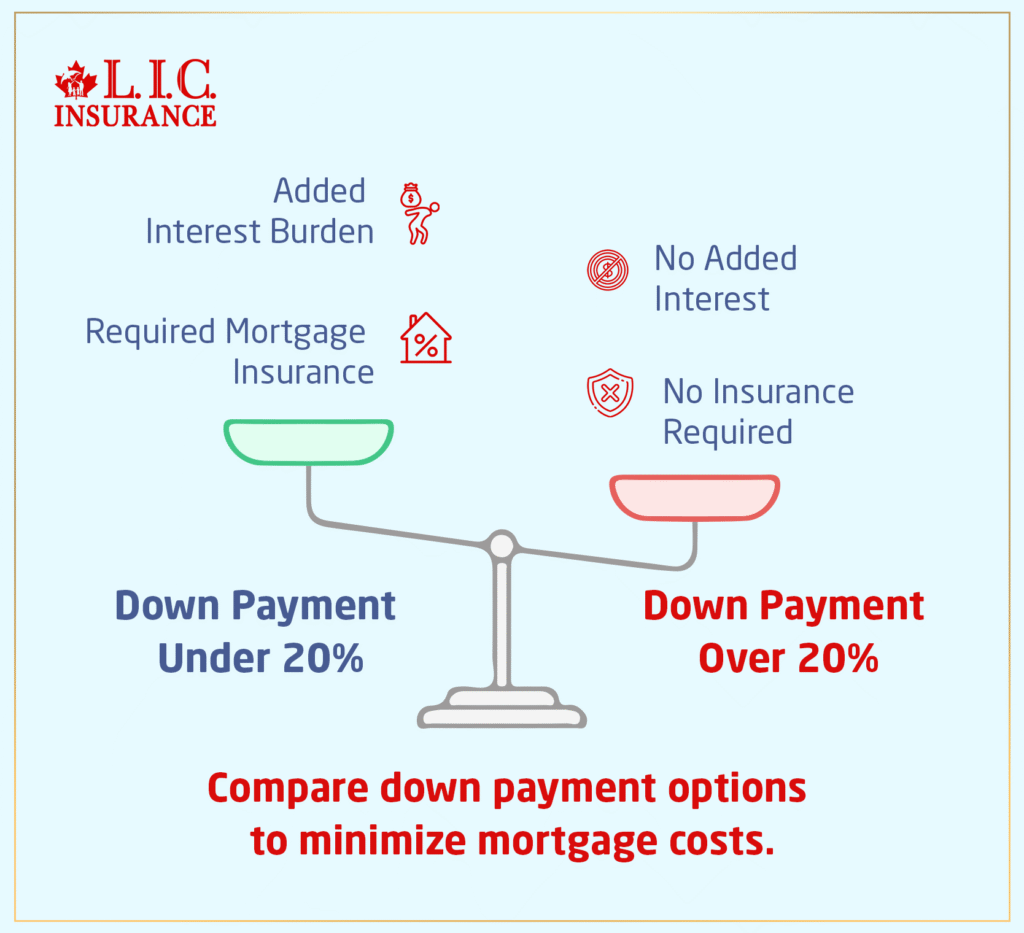

Here’s a common situation: A young couple walks into our office, excited to close on their first home. They’ve managed to put together a 10% down payment on a $600,000 home in the GTA. But when we look at the numbers, we notice something—they’re going to need Mortgage Insurance.

Most people don’t realize that if your down payment is under 20%, you’re required to pay for default insurance. It protects the lender in case you default, but you’re the one footing the bill. And that premium? It’s not a small mortgage amount—it gets added to your mortgage and compounds interest just like the rest of your loan.

We helped that couple work through their options:

- Could they increase their down payment even slightly to reduce the insurance cost?

- Should they go ahead and compare default mortgage insurance premiums through approved insurers rather than assuming lender-assigned pricing?

Ultimately, they saw how the average cost of Mortgage Insurance could affect their long-term payment structure. We made sure they understood the math and the impact.

When people search for the mortgage rate 5 year or compare 5 year fixed rates, they often focus only on the interest percentage. But the true cost of a 5 year fixed mortgage also depends on insurance and payment structure. In 2026, home loan rates 5 year fixed vary by lender, credit profile, and down payment size, which is why the best Canadian 5 year mortgage rates aren’t always the lowest advertised ones.

One question we hear constantly is: how much is Mortgage Insurance per month? The answer depends on your loan amount and down payment. For most insured mortgages in Canada, Mortgage Insurance payments aren’t billed monthly. Instead, the premium is added to the mortgage balance and spread across your regular payments. On a typical insured loan, this can increase monthly payments by anywhere from $80 to $200, depending on the size of the mortgage.

Understanding both 5 year fixed mortgage rates Canada and how Mortgage Insurance payments per month affect affordability helps buyers avoid surprises later. That’s why we always look beyond headline rates and break down the full five-year cost before our clients commit.

Why don't the Banks just set rates

Clients often assume that their bank controls their mortgage rate, but that’s not exactly true. Behind the scenes, fixed Mortgage Insurance rates are tied to government bond yields, which react to economic signals. So if inflation is expected to rise, bond yields usually go up, and so do mortgage rates.

A few months ago, a couple from Edmonton came to us after being pre-approved at a certain rate. They were still shopping around and weren’t in a hurry. But bond yields increased, and suddenly, their rate jumped by 0.45%. That’s the kind of thing that adds thousands over five years.

We helped them move quickly with another lender that hadn’t adjusted yet, and they locked in a better rate just in time. It’s a reminder that mortgage rates in Canada move with more than just bank policies—they’re tied to bond markets, inflation expectations, Bank of Canada guidance, and lender-specific risk pricing, all of which remain key factors in 2026.

Comparing Lenders Isn't Just About the Rate

Every week, we compare Canadian mortgages from banks, credit unions, and private lenders. And it’s not just about who offers the lowest number. We’re looking at:

- Prepayment privileges

- Portability

- How penalties are calculated

- Whether your mortgage is compounded monthly or semi-annually (most Canadian mortgages continue to use semi-annual compounding by default in 2026)

One client, a teacher in Vancouver, nearly signed with her primary bank until we showed her a better offer through a credit union. It wasn’t just a lower rate—the terms were more flexible. She could pay up to 20% more per year without penalty, and her mortgage default insurance cost was slightly lower, too.

Fixed vs. Variable: What's the Risk?

When people ask us about fixed versus variable, we start with this: “How would you feel if your monthly payment jumped by $150 next year?”

Variable rates can be lower upfront, but they carry uncertainty. We had a freelance designer from Ottawa who chose variable because she wanted the freedom to break her mortgage early. It worked out for her, but we made sure she understood the risks.

For someone with tight margins or a young family, fixed usually makes more sense—especially as lenders in 2026 continue to apply stricter stress-test buffers and tighter variable-rate qualification rules.

What About Penalties and Prepayment?

This part always surprises people: you might get a great rate, but if you need to break your mortgage early, you could face steep penalties.

A client in Calgary had to relocate for work just two years into their 5-year fixed mortgage. The lender calculated a penalty based on the interest rate differential, not just three months’ interest. That cost them over $7,000.

That’s why we always ask:

- Is your mortgage portable?

- Can you pay it off early without huge penalties?

- What’s your lender’s prepayment limit?

These questions matter more than many people think. We make sure our clients read the fine print before they sign anything.

Debt Ratios and Stress Testing: Can You Qualify?

Getting approved is tougher than it used to be. The government’s stress test means you have to qualify for your mortgage at a higher rate than what you’re actually offered (the contract rate plus the federally mandated buffer, which remains in effect in 2026).

We help people calculate their gross debt service (GDS) and total debt service (TDS) ratios before they even apply. It’s not about how much you earn—it’s about how your income compares to your debts.

Last month, we helped a nurse in Windsor whose bank denied her. Her TDS was slightly too high. We found a lender with more flexible guidelines and helped her pay down a small credit card balance. Two weeks later, she qualified.

Final Word from Our Team

If there’s one thing we try to help every client understand, it’s this: mortgage decisions should be personal. There’s no universal best rate or perfect lender. The right mortgage is the one that fits your life.

We’re here to walk with you through that process—from reviewing 5-year fixed mortgage rates in Canada for 2026 to understanding your insurance options, comparing lenders, and reading through every clause in your mortgage contract.

And yes, we’ll help you find a competitive rate. But more importantly, we’ll help you get the right mortgage, with the right conditions, so you’re protected no matter what the next five years bring.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

Frequently Asked Questions

Not necessarily. A 5-year fixed mortgage works well for many people who want stability in their monthly payments, but it isn’t the best fit for everyone. At Canadian LIC, we always ask about your income, future plans, and comfort level with risk. For some, a shorter term or even a variable rate mortgage makes more sense depending on where rates and your life are heading.

Mortgage Insurance covers the lender in case you default on the loan, not you. If your down payment is under 20%, it’s mandatory. The Mortgage Insurance rate depends on the size of your down payment and loan. We walk clients through the average cost of Mortgage Insurance and how it affects their monthly payments and interest over time. It’s often an overlooked cost until it shows up in the final numbers.

Yes, and we often encourage clients to compare. You can buy a Mortgage Insurance Policy online and sometimes get better mortgage term lengths or premiums. The key is understanding how that policy fits your mortgage and financial situation. At Canadian LIC, we help clients review their options before choosing one that matches their goals.

Fixed mortgage rates move with government bond yields, which react to economic factors like inflation and interest rate forecasts. We’ve had clients watch their quoted rate jump within days. That’s why we track market conditions daily and guide people on when to lock in. It’s not just about watching the news—it’s about knowing how lenders will respond.

That’s where prepayment penalties come in—and they can be expensive. Depending on your lender, the penalty could be based on a few months of interest or a more complex interest rate differential formula. We’ve helped clients reduce costs by choosing more flexible mortgage terms upfront, especially if there’s even a small chance they’ll move or refinance before the 5-year term is done.

We’ve seen clients miss approval by a small margin. The stress test makes sure you can handle payments even if rates rise. If your debt service ratios are too high, we help you adjust—whether that means paying down a loan, extending the amortization, or adding a co-applicant. The goal is to qualify without overextending yourself.

Banks offer convenience, but mortgage brokers like us at Canadian LIC offer options. We pull rates from dozens of lenders, including credit unions and alternative lenders, and compare terms, penalties, and flexibility. We’ve helped many clients save thousands by looking beyond their usual bank’s offer, and we make sure they understand every detail before signing anything.

Fixed rates give you payment stability. Variable rates can save you money—but only if you’re comfortable with changing monthly amounts. We help clients weigh both based on their risk tolerance, emergency savings, and lifestyle. It’s not about choosing what’s trending—it’s about choosing what fits your reality.

Key Takeaways

- 5-year fixed mortgage rates offer stability and predictable monthly payments, ideal for buyers who value certainty over potential savings from variable options.

- Mortgage Insurance rates apply if your down payment is under 20%, adding to your total mortgage cost. It’s important to understand how the average cost of Mortgage Insurance affects your repayment plan.

- Clients can buy Mortgage Insurance Policies Online, allowing them to compare terms and potentially reduce overall costs.

- Fixed mortgage rates in Canada are influenced by government bond yields, inflation expectations, and Bank of Canada policies—not just lender discretion.

- Choosing the right lender matters—credit unions, banks, and mortgage brokers each offer different rates, terms, and flexibility.

- Always read the fine print. Prepayment penalties, compounding interest rules, and portability clauses can significantly impact the total cost of your mortgage.

- Passing the mortgage stress test and maintaining strong debt service ratios are key to qualifying for the best rates.

- The lowest rate isn’t always the best fit—personal financial goals, flexibility needs, and long-term plans should drive the decision.

- Working with a knowledgeable broker like Canadian LIC helps you evaluate your full financial picture before committing to any mortgage term.

Sources and Further Reading

Explore these authoritative resources for more in-depth information on each main topic and subtopic discussed in this blog about 5-year fixed mortgage rates in Canada:

Compare Current 5-Year Fixed Mortgage Rates

- TD Canada Trust Mortgage Rates

- RBC Royal Bank Mortgage Rates5

- CIBC Mortgage Rates6

- Scotiabank Fixed Rate Mortgages7

- BMO Mortgage Rates8

- Best Mortgage Rates in Canada – Ratehub.ca4

Mortgage Insurance (CMHC Insurance) and Down Payments

How Mortgage Rates Are Determined in Canada

Fixed vs. Variable Mortgage Rates: Pros and Cons

Feedback Questionnaire:

IN THIS ARTICLE

- Find The Best 5-Year Fixed Mortgage Rates In Canada

- Why People Lean Toward the 5-Year Fixed Mortgage

- Let's Talk About Mortgage Insurance

- Why don't the Banks just set rates

- Comparing Lenders Isn't Just About the Rate

- Fixed vs. Variable: What's the Risk?

- What About Penalties and Prepayment?

- Debt Ratios and Stress Testing: Can You Qualify?

- Final Word from Our Team

Sign-in to CanadianLIC

Verify OTP