- Connect with our licensed Canadian insurance advisors

- Schedule a Call

Basics

- What Is the Maturity Period of Term Insurance?

- Understanding the Uses of a Term Insurance Calculator

- What Is Underwriting in Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- How Do You Choose Term Insurance?

- Can You Cash Out a Term Life Insurance Policy?

Reviews

Common Inquiries

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What happens after 20 years of Term Life Insurance?

- Why a 20-Year Term Policy?

- What Happens When the 20 Years Are Over?

- Option 1: Renew Your Term Life Insurance Policy

- Option 2: Convert Your Term Policy to a Permanent Life Insurance Policy

- Option 3: Purchase a New Term Life Insurance Policy

- Option 4: Let the Policy Expire

- Understanding Term Life Insurance Cash Value

- Option 1: Renew Your Term Life Insurance Policy

- Option 2: Convert Your Term Policy to Permanent Life Insurance

- Option 3: Purchase a New Term Life Insurance Policy

- Option 4: Let the Policy Expire

What Happens After 20 Years Of Term Life Insurance?

By Harpreet Puri

CEO & Founder

- 11 min read

- November 18th, 2024

SUMMARY

Term Life Insurance is possibly the simplest way to provide financial security for a term, but most policyholders have tended to think about what really happens when their term ends over the years. Being in the 20th year of your Term Life Insurance, it is likely that you are now at a crossroads and making some critical decisions regarding your next course of action. Canadian LIC is a very reliable name in insurance circles and, over time, has guided many clients to better solutions when faced with the same type of dilemma. Here, we shall take you through some common struggles and the options available so you are ready for what lies ahead.

Why a 20-Year Term Policy?

Many people opt for a 20-year Term Life Insurance Policy because it aligns with their financial milestones. Policies are opted for and designed to last throughout major points in a person’s life, often raising children, paying off a mortgage, or beginning to build some sort of financial safety net.

For example, a young family may choose a 20-year policy to guard the growing household and enable mortgage payments or other financial obligations to be paid if there is an untimely death. However, a period of 20 years is very quick, and at the end of the term, there might be new issues and priorities.

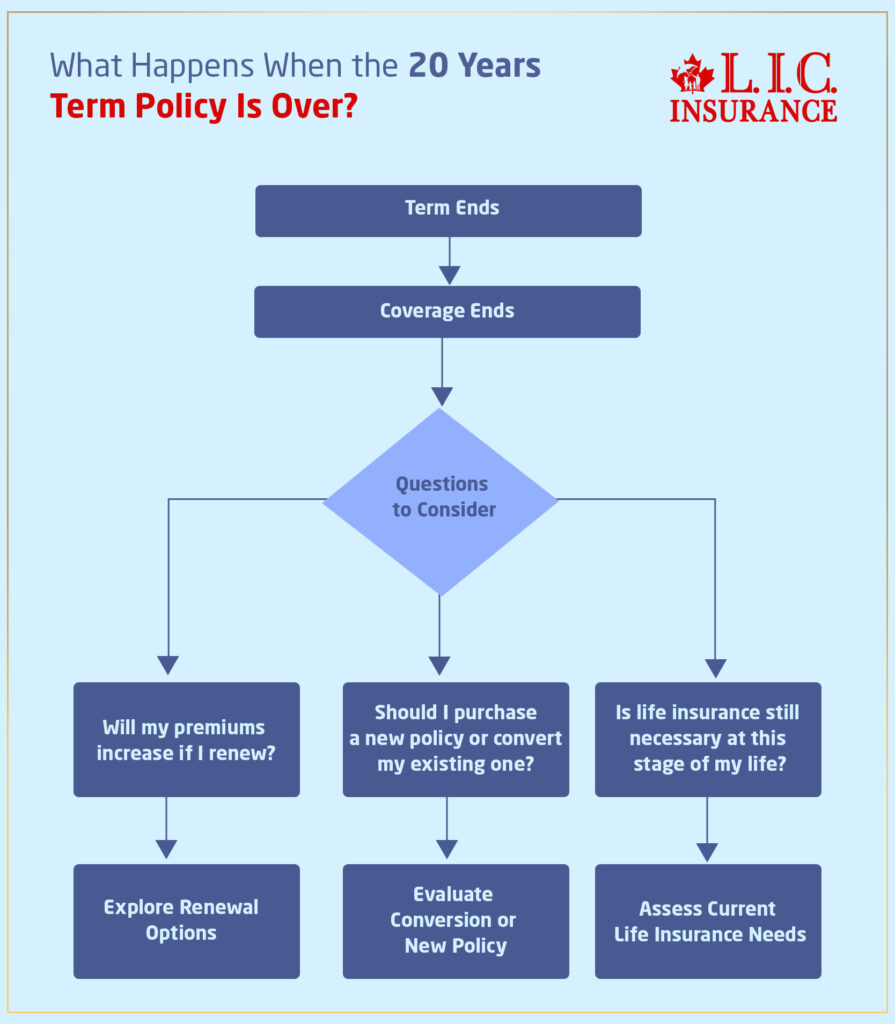

What Happens When the 20 Years Are Over?

Once the term ends, your coverage ends. This means that the protection that was in place for the last twenty years is no longer there. A lot of customers come to Canadian LIC with questions about what happens next. Questions asked include:

- Will my premiums increase if I renew the policy?

- Should I purchase a new policy or convert my existing one?

- Is life insurance still necessary at this stage of my life?

These are valid concerns that deserve careful consideration. Let’s dive into the options you have when your 20-year term ends.

Option 1: Renew Your Term Life Insurance Policy

One of the easiest options you have, in case your Term Life Insurance Policy ends, is renewal. Most policies allow you to renew it for another term without requiring you to take any kind of medical examination. However, renewal premiums are higher than the previous premium payments because the premium amount gets recalculated according to your present age.

Quite often, clients at Canadian LIC are surprised by the big price increase coming at renewal. For instance, a 35-year-old policyholder, who may have been paying $30 per month on a half-a-million-dollar policy, may be surprised that it now costs a staggering amount of at least $150 by age 55. So, although renewal is convenient, the option becomes less attractive when the cost is much higher.

Option 2: Convert Your Term Policy to a Permanent Life Insurance Policy

A Term Life Insurance Policy that has a conversion option can be converted to permanent insurance without the need for any medical exam. This is particularly valuable for individuals whose health has declined, as it guarantees continued coverage.

Permanent Life Insurance not only provides lifetime coverage but also accrues cash value over the years. The cash value of a term life can be contributed to fund additional retirement income or long-term goals.

A Canadian LIC client in their late 50s shared their experience of converting their policy. Initially, they purchased a 20-year Term Policy to cover their children’s education and mortgage. By the time the policy ended, their children were independent, but the client wanted to ensure they left a financial legacy. The conversion allowed them to maintain coverage while also building cash value for future needs.

Option 3: Purchase a New Term Life Insurance Policy

New-Term Life Insurance Policy purchases are another option if they are in good health. This is the best time to begin fresh with a new coverage period, which is usually less expensive than renewing the old policy.

The Canadian LIC has worked with many clients to come under this scheme. For example, one client in their mid-40s wanted to purchase a new policy to cover a newly bought second home. The other client chose to extend their cover so that the spouse’s financial stability came through into retirement.

Term Life Insurance Brokers at the Canadian LIC often recommend that you compare online Term Life Insurance quotes to ensure you get a competitive quotation for the best rates for a new policy. This way, you would be ensuring that you obtain a competitive value for your money while maintaining a standard amount of coverage.

Option 4: Let the Policy Expire

At other times, it simply makes sense to allow policy coverage to lapse. If your financial obligations have diminished and your dependents no longer rely on your income, you may not need life insurance anymore.

Canadian LIC is seeing the same thing with the empty nesters- the people who have paid up their mortgages and saved enough to live decently in their retirement. By reallocating the funds that would have gone toward premiums, they’re able to focus on other priorities, such as travel, hobbies, or charitable giving.

Understanding Term Life Insurance Cash Value

One of the basic misconceptions is about whether Term Life Insurance can create cash value. Term life policies do not establish cash value like Permanent Policies. At the end of the term, no payout will be made unless there was a claim during the period of cover.

What Happens After 20 Years of Term Life Insurance?

Term Life Insurance is one of the most straightforward ways to secure financial protection for a fixed period. However, as the years go by, many policyholders begin to wonder what happens when the term ends. If you’ve reached the 20-year mark of your Term Life Insurance Policy, you’re likely facing critical decisions about your next steps. Canadian LIC, a trusted name in the insurance industry, has helped many clients in similar situations, guiding them toward the most suitable solutions. In this blog, we’ll address the common struggles and explore your options to ensure you’re prepared for the journey ahead.

Why a 20-Year Term Policy?

Many people opt for a 20-year Term Life Insurance Policy because it aligns with their financial milestones. These policies are designed to provide coverage during crucial stages of life, such as raising children, paying off a mortgage, or building a financial safety net.

For example, a young family may choose a 20-year policy to protect their growing household while ensuring the mortgage and other financial obligations are covered in case of an untimely death. However, 20 years can pass quickly, and by the end of the term, new challenges and priorities often emerge.

What Happens When the 20 Years Are Over?

Once the term expires, the coverage provided by your policy comes to an end. This means you no longer have the protection that was in place for the past two decades. Many clients at Canadian LIC share their concerns about what happens next. Common questions include:

- Will my premiums increase if I renew the policy?

- Should I purchase a new policy or convert my existing one?

- Is life insurance still necessary at this stage of my life?

These are valid concerns that deserve careful consideration. Let’s dive into the options you have when your 20-year term ends.

Option 1: Renew Your Term Life Insurance Policy

Renewal is one of the most straightforward options available when your Term Life Insurance Policy ends. Most policies allow you to renew for another term without a medical exam. However, the renewal comes at a higher cost, as premiums are recalculated based on your current age.

At Canadian LIC, we’ve worked with clients who were surprised by the significant increase in premiums upon renewal. For instance, a 35-year-old policyholder who initially paid $30 per month for a $500,000 policy might find that the cost has jumped to $150 or more at age 55. While the convenience of renewal is appealing, the higher cost often prompts people to explore alternative options.

Option 2: Convert Your Term Policy to Permanent Life Insurance

If your Term Life Insurance Policy includes a conversion option, you can convert it to a Permanent Policy without undergoing a medical exam. This is particularly valuable for individuals whose health has declined, as it guarantees continued coverage.

Permanent Life Insurance not only provides lifelong coverage but also builds cash value over time. This Term Life Insurance Cash Value can be used for various financial purposes, such as supplementing retirement income or funding long-term goals.

A Canadian LIC client in their late 50s shared their experience of converting their policy. Initially, they purchased a 20-year Term Policy to cover their children’s education and mortgage. By the time the policy ended, their children were independent, but the client wanted to ensure they left a financial legacy. The conversion allowed them to maintain coverage while also building cash value for future needs.

Option 3: Purchase a New Term Life Insurance Policy

For those in good health, purchasing a new Term Life Insurance Policy is another option. This allows you to start fresh with a new coverage period, often at a lower cost than renewing the old policy.

Canadian LIC has worked with many clients who opted for this route. For example, one client in their mid-40s decided to buy a new policy to protect a second home they had recently purchased. Another client chose to extend their coverage to ensure their spouse’s financial stability through retirement.

Term Life Insurance Brokers at Canadian LIC often recommend comparing Term Life Insurance Quotes Online to find the most competitive rates for a new policy. This approach ensures you’re getting the best value for your money while maintaining adequate coverage.

Option 4: Let the Policy Expire

In some cases, letting the policy lapse is a practical decision. If your financial obligations have diminished and your dependents no longer rely on your income, you may not need life insurance anymore.

Canadian LIC has seen this scenario play out with empty nesters who have paid off their mortgage and saved enough for retirement. By reallocating the funds that would have gone toward premiums, they’re able to focus on other priorities, such as travel, hobbies, or charitable giving.

Understanding Term Life Insurance Cash Value

One common point of confusion is whether Term Life Insurance Policies build cash value. Unlike permanent policies, Term Life Insurance does not accumulate cash value. Once the term ends, you do not receive any payout unless a claim was made during the coverage period.

At Canadian LIC, clients often express disappointment when they realize their premiums didn’t result in a financial return. That is why you must know the alternatives in advance and consider switching to a product which can provide a cash value if it meets your needs.

Planning for the Future

The end of a 20-year Term Life Insurance Policy is not just an endpoint—it’s an opportunity to reassess your needs and plan for the future. Here are some things you can do to make a good decision:

- Assess Your Current Financial Situation: Review your existing financial obligations, such as a mortgage, children’s education, or retirement savings.

- Explore Conversion Options: If you want lifelong coverage and cash value accumulation, talk to Term Life Insurance Brokers about converting your policy.

- Compare New Policy Quotes: Use Term Life Insurance Quotes Online to explore the cost of purchasing a new Term Policy.

- Consult with Experts: Canadian LIC provides personalized guidance, helping you navigate the complexities of insurance and find the best solution for your unique needs.

Common Misconceptions

“I don’t need life insurance after 20 years.”

While it’s true that some people may not need life insurance anymore, others may find that new priorities have emerged, such as ensuring their spouse’s financial security or leaving a legacy.

“Renewal is always the best option.”

You need to explore alternatives to renew your policy to avoid unnecessarily high premiums. Comparing options can help you find a more affordable solution.

Real Experiences

One client, a Canadian LIC customer, has a 20-year Term Policy that he says helped him sleep far better at night, knowing his family was protected. When it ended, he felt lost and unsure of what to do. Upon discussion with our broker, he determined that he needed a much smaller Permanent Policy that would give him not only coverage but also cash value.

Another customer, a business owner, purchased a Term Policy in an effort to eliminate any outstanding loans at the time of death so that the family would not have to deal with them upon his death. These are just two examples of people who needed Term Insurance for various reasons, which explains why customized advice and planning can often be so worthwhile.

Take the Next Step with Canadian LIC

The approaching end of a 20-year Term Life Insurance Policy is definitely one of the most critical events in one’s life. Knowing all options and consulting an expert can be your first step in providing the best choice for your future. Renew, convert, or buy a new one—Canadian LIC is there to help. Our team of experienced Term Life Insurance Brokers is dedicated to finding the right solution for unique needs.

Your finances deserve nothing but the best. Reach out to Canadian LIC today and take control of your insurance journey.

More on Term Life Insurance

- Term Life Insurance Plan for All Age Groups

- What Does It Mean to Buy Term & Invest the Difference?

- How Do You Calculate Term Insurance Value?

- Why Is Term Life Insurance with a Return of Premium Option Not the Best Risk Coverage for You?

- Group Term Life Insurance & Individual Term Insurance: Know the Details

- What Is the Claim Period for Term Life Insurance?

- Can I Convert My Term Policy to Whole Life?

- Can You Use Term Life Insurance to Pay Off a Mortgage?

- Do Term Life Insurance Plans Offer Cash Value?

- What Happens to Term Insurance If the Nominee Dies?

- What Is the Shortest-Term Life Insurance Policy?

- What Is the Cheapest Term Life Insurance for Seniors Over 70?

- Who Benefits from Term Life Insurance?

- Can Term Insurance Be Rejected After Five Years?

- What Is the Longest Term Life Insurance?

- Does Term Insurance Automatically Renew?

- Can you extend a 20-Year Term Life Policy?

- Do I Get Money Back from Term Life Insurance?

- Can You Cash Out a Term Life Insurance Policy?

- Should Both Husband and Wife Get Term Life Insurance?

- What Is Underwriting in Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- What Is the Maturity Period of Term Insurance?

- Can I Purchase a Joint Term Life Insurance Policy or a Whole Life Insurance Policy?

- Best Term Life Insurance Companies in Canada: In-Depth Reviews & Essential Insights (2024)

- At What Age Should You Stop Buying Term Life Insurance?

- What are the advantages of Short Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- How Do You Choose Term Insurance?

- What’s the Longest Term Life Insurance You Can Get?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 844-542-4678 to speak to our advisors.

Get Quote Now

FAQs: What Happens After 20 Years of Term Life Insurance?

After 20 years, your Term Life Insurance Policy ends, and coverage stops unless you renew, convert, or purchase a new policy. Many Canadian LIC clients find this is a good time to evaluate their current financial needs and decide on the best course of action for their future.

Yes, most Term Life Insurance Policies offer a renewal option. However, the premiums will increase significantly because they are based on your age at renewal. Canadian LIC often advises clients to compare renewal costs with other options, such as purchasing a new policy.

No, Term Life Insurance Policies do not build cash value. They are designed to provide financial protection during the term. At Canadian LIC, we help clients explore alternatives like converting to permanent policies that build cash value over time.

Yes, many Term Life Insurance Policies include a conversion option. You can convert to Permanent Life Insurance without a medical exam. Canadian LIC has helped clients secure lifelong coverage by converting their policies, especially when their health has changed over the years.

If you’re in good health and still need coverage, buying a new Term Policy might be a practical solution. Canadian LIC brokers can help you compare Term Life Insurance Quotes Online to find affordable options that meet your needs.

Term Life Insurance Brokers like Canadian LIC simplify the process by offering personalized advice and access to multiple insurance providers. They help you find the best policy based on your financial goals and current situation.

It depends on your circumstances. If you have dependents or financial obligations, life insurance may still be necessary. Many Canadian LIC clients reassess their needs at the end of a term and choose coverage options that match their current priorities.

Yes, comparing Term Life Insurance Quotes Online is an easy way to explore your options. Canadian LIC helps clients find competitive rates from top insurance companies, saving time and effort while ensuring the right coverage.

If you let your policy expire without renewing or replacing it, you’ll lose the financial protection it offers. Canadian LIC often recommends carefully evaluating your needs before making this decision to avoid gaps in coverage.

Canadian LIC provides expert advice tailored to your unique situation. Whether you want to renew, convert, or buy a new policy, their experienced brokers guide you through every step, ensuring you make the best decision for your future.

If you miss renewing your policy, your coverage will end, and your beneficiaries will no longer receive a death benefit. Canadian LIC brokers often help clients avoid this by providing reminders and exploring renewal or replacement options ahead of time.

Renewing may be worth it if you still need coverage and are not eligible for a new policy due to health reasons. Canadian LIC brokers analyze your situation and compare renewal costs with other options, ensuring you make the best decision.

Most insurance companies set age limits for Term Life Insurance renewals and new purchases, often capping them at 70 or 75 years old. Canadian LIC helps clients understand these limits and find suitable options based on their age and needs.

Some policies allow you to reduce the coverage amount at renewal, which can help lower premiums. Canadian LIC brokers guide clients in choosing the right coverage to match their current financial obligations.

Renewing allows you to extend your existing policy without a medical exam but at higher premiums. Buying a new policy might require a medical exam but often offers lower premiums for the same coverage. Canadian LIC brokers explain these differences to help clients make informed choices.

Brokers like Canadian LIC work with multiple insurance providers, giving you access to competitive Term Life Insurance Quotes Online. They simplify the process by doing the research for you, ensuring you find the best policy for your needs.

Yes, you can switch providers by purchasing a new policy. Canadian LIC brokers assist clients in comparing policies from various providers, ensuring a smooth transition without losing coverage.

Your health can impact your options. Renewals don’t require a medical exam, but new policies usually do. If your health has changed, converting to a Permanent Policy might be a better choice. Canadian LIC frequently helps clients in such situations.

Assess your current financial responsibilities, such as debts, dependents, and future goals. Canadian LIC brokers provide personalized advice to help you determine the right coverage amount based on your situation.

Permanent Life Insurance provides lifelong coverage and builds cash value, which term policies don’t offer. However, premiums are higher. Canadian LIC brokers help clients weigh the pros and cons of both options to find the right fit.

Most insurance providers offer flexible payment options, including monthly or annual premiums. Canadian LIC ensures clients understand their payment choices and select the one that suits their budget.

If your financial needs have decreased, you can opt for a smaller policy or let your coverage lapse. Canadian LIC helps clients evaluate their current needs to decide if coverage is still necessary.

It’s best to start planning a year or two before your policy ends. Canadian LIC recommends early planning to avoid last-minute decisions and secure the most suitable coverage.

Canadian LIC provides personalized guidance, helping clients understand their options, compare Term Life Insurance Quotes Online, and choose the best solution for their financial goals.

Sources and Further Reading

To deepen your understanding of Term Life Insurance and its role in financial planning, consider exploring the following resources:

- Canada Life: Offers detailed explanations of 20-year Term Life Insurance Policies and their features.

Canada Life - Sun Life Canada: Provides insights into Term Life Insurance options and considerations for Canadians.

Sun Life - Canadian Life Insurance Company: Discusses the differences between term and cash value life insurance, helping you understand which may suit your needs.

Canadian Life Insurance Company - MoneySense: Offers comparisons of various life insurance options in Canada, including Term Life Insurance.

MoneySense - Canada.ca: The official government website provides an overview of life insurance types and considerations for Canadians.

Government of Canada

Key Takeaways

- Coverage Ends Without Action: When your 20-year Term Life Insurance Policy expires, the coverage stops unless you renew, convert, or purchase a new policy.

- Renewal Comes at a Cost: Renewing your policy is an option, but premiums will increase significantly as they are based on your current age.

- Conversion Offers Lifelong Coverage: Converting to a Permanent Life Insurance policy allows you to maintain coverage without a medical exam and build cash value over time.

- Buying a New Policy May Save Money: If you’re healthy, purchasing a new Term Policy often provides more affordable premiums than renewing an older policy.

- Term Policies Don’t Build Cash Value: Unlike Permanent Life Insurance, term policies provide protection but do not accumulate cash value.

- Assess Your Current Needs: Reevaluate your financial situation, dependents, and future goals to decide if life insurance is still necessary and in what form.

- Brokers Simplify the Process: Working with Term Life Insurance Brokers like Canadian LIC helps you compare Term Life Insurance Quotes Online and find the best solutions tailored to your needs.

- Start Planning Early: Begin reviewing your options a year or two before your policy ends to ensure a smooth transition without gaps in coverage.

- Health Affects Your Options: Your current health can impact whether renewing, converting, or purchasing a new policy is the best path forward.

- Canadian LIC Provides Expert Guidance: Their experience and personalized approach help you make confident decisions for continued financial security.

Your Feedback Is Very Important To Us

We value your feedback! Please take a few minutes to share your thoughts and experiences related to what happens after your 20-year Term Life Insurance Policy ends. Your responses will help us address the most common concerns and provide better solutions.

Thank you for your input! Your responses will help us address the real struggles Canadians face with Term Life Insurance and provide tailored solutions.

IN THIS ARTICLE

- What happens after 20 years of Term Life Insurance?

- Why a 20-Year Term Policy?

- What Happens When the 20 Years Are Over?

- Option 1: Renew Your Term Life Insurance Policy

- Option 2: Convert Your Term Policy to a Permanent Life Insurance Policy

- Option 3: Purchase a New Term Life Insurance Policy

- Option 4: Let the Policy Expire

- Understanding Term Life Insurance Cash Value

- Option 1: Renew Your Term Life Insurance Policy

- Option 2: Convert Your Term Policy to Permanent Life Insurance

- Option 3: Purchase a New Term Life Insurance Policy

- Option 4: Let the Policy Expire

Sign-in to CanadianLIC

Verify OTP