- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

What Happens If You Outlive Your Term Life Insurance?

By Harpreet Puri

CEO & Founder

- 11 min read

- April 10th, 2025

SUMMARY

The blog explains what happens if you outlive your Term Life Insurance Policy and explores your next steps. It covers Term Life Insurance renewal options, converting to Whole Life Insurance, evaluating financial needs, and considering new life insurance strategies. It also discusses how health status affects your choices and highlights the importance of comparing Term Life Insurance Policy quotes to get the right coverage at the right cost.

Introduction

Term Life Insurance is among the most common and least expensive forms of life insurance, providing coverage for a set period of time — usually 10 to 30 years. It is meant to offer financial protection for your family or beneficiaries if something happens to you while the policy is in effect. Yet, many policyholders do wonder about one thing in particular: “What happens when you outlive Term Life Insurance?”

There are a few things you can do if you outlive your term life insurance. In this blog, we will go over the options that you have when your term expires, as well as renewal options, how to convert to Whole Life Insurance, and other helpful information. We’ll also walk you through what you can do next to make sure your loved ones still have the protection they need.

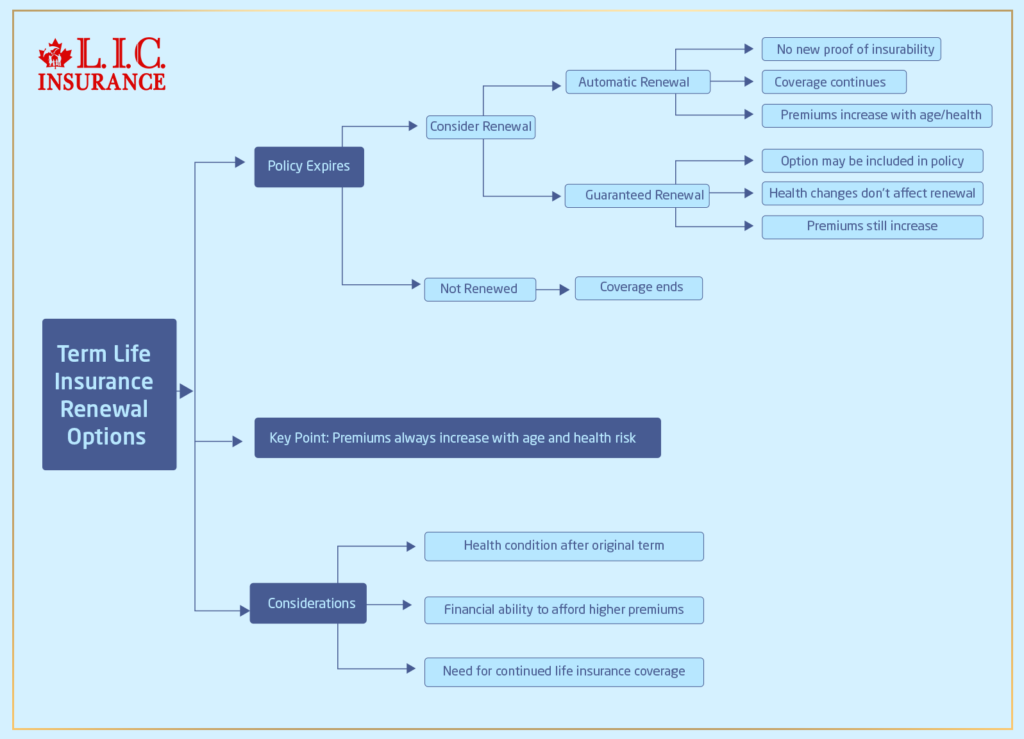

Renewal Options After Outliving Term Life Insurance

After your Term Life Insurance Policy expires, you may be able to renew it for another term. Most Term Life Insurance coverage includes a renewal provision in the policy. Here’s how it works:

- Automatic Renewal: Each year, your policy may include an automatic renewal feature, which means you can continue your coverage without the requirement for new proof of insurability. This ensures you can keep life insurance coverage even if your health has changed over the years. But this means you’re facing higher premiums as you get older since insurers generally raise your fees to match your actual age and health.

- Guaranteed Renewal: The policy may provide an option for guaranteed renewal in certain instances. This means you can renew the policy for another term without fear of a change in your health status. Not only do premiums still increase, but coverage can be continued despite any health conditions developed during the previous term.

- Increased Premiums: Although having Term Life Insurance Renewal Options brings peace of mind, business owners must remember that renewals will typically feature premiums that are higher than the original policy. The older you are, the more likely you are to have health problems and insurance premiums are determined partly by age and health risk factors. So, although you may appreciate the convenience of renewing your policy, expect to pay more.

Converting Term Life Insurance to Whole Life Insurance

The other option if you outlive your Term Life Insurance is to convert it to a Whole Life Insurance policy. Most Term Life Insurance Policies will have a conversion clause built into them that allows you to convert your Term Policy into a whole life policy without needing a medical exam. It’s also a useful option for those who may become sick while their Term Policy is in force and can’t get new insurance.

- How Conversion Works: If your policy has a conversion option, you can typically convert it into a Whole Life Policy at any time during the term period — often until a designated age limit (often about 65). This means that even if your health has deteriorated, you won’t have to fear being denied coverage or hit with sky-high premiums when you convert to Whole Life Insurance.

- Advantages of Converting to Whole Life: The biggest advantage of converting to Whole Life Insurance is lifetime coverage. Unlike Term Life Insurance, which ends when the policy period is finished, Whole Life Insurance covers you for life as long as you keep paying the premiums. So, Whole Life Insurance has a cash value that accumulates over time and allows you to borrow against the policy or use it for other financial needs.

The Takeaway: Converting to Whole Life Insurance can be a great option for obtaining coverage that lasts a lifetime, but keep in mind that the cost of Whole Life Insurance is usually far more expensive than term life insurance. So, while you’ll benefit from lifelong protection, your premiums will be much higher.

What to Do Next if You Outlive Your Term Life Insurance

If you’ve already reached the end of your Term Life Insurance without any renewal or conversion to Whole Life Insurance, here are a few extra steps to take:

- Evaluate Your Financial Needs

Before you create a plan, take the time to assess where you currently stand financially. Evaluate your age, health, dependents, and other financial obligations. Do you still need life insurance coverage? If your finances have changed, and you no longer have much in the way of financial dependents, you may make the call that it no longer makes sense to keep your coverage and let it lapse.

- Discover New Life Insurance Strategies

If you require ongoing coverage and would like to obtain a new policy, you can look into other types of life insurance. Although it can be pricier to buy a new Term Policy as you get older, it may still wind up being lower in cost than converting your plan to whole-life insurance. Quote life terms from multiple insurers to compare prices and find the best deal.

- Look at Permanent Life Insurance

If you’ve outlived your term life policy and want lifelong coverage, it might be time to look at permanent life insurance, such as whole or universal life insurance. They are lifelong and can act as an important tool for estate planning and wealth transfer. One note on permanent insurance: It typically will cost more than term life, but if you’re looking for peace of mind and some long-term security, it could be worth it.

- Evaluate Your Current Health Condition

You must check your health status before taking a new policy or converting your Term Policy. If your health has improved or stabilized, you may be eligible for better rates on a new policy. If your health has deteriorated, on the other hand, a conversion option may be the best option for you because it helps you avoid going through a medical exam and secures coverage regardless of your health status.

Understanding Your Options for the Future

Life insurance is vital to protecting your family’s financial future, and it’s important to understand what to expect when your Term Life Insurance ends. Whatever you decide when it comes to renewing the insurance policy, converting the policy to Whole Life Insurance, or seeking new life insurance coverage, understand the benefits and costs associated with each option.

If you do choose to explore new providers, keep in mind you can always fill term life and get Term Life Insurance Policy Quotes from multiple providers to find which will provide the best coverage and rates for your financial needs. Getting multiple quotes can help you get the most favourable price, but it makes sure you keep the proper level of protection when your needs change.

The End

Outliving Term Life Insurance Policy doesn’t mean you need to go without coverage entirely. And if the term runs out, there are renewal options, conversions to whole life, and other alternatives that can provide peace of mind that you will still be able to protect your loved ones. Knowing your options, assessing your needs, and seeking the best life insurance solutions allow you to keep financial security and peace of mind at every stage of your life. Suppose you are not sure how best to proceed from here. Consult an insurance professional who can help you navigate the options while advising you on the best next step based on your particular situation.

More on Term Life Insurance

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

If you outlive a Term Life Insurance Policy, your coverage simply ends when the term expires. You will no longer be protected under that policy. However, you may have several options: you can renew the policy, convert it to a whole life plan, or purchase new coverage based on your current financial needs and health status.

Yes, most policies include Term Life Insurance renewal options. Depending on your policy, you may be able to renew annually or for another fixed term without undergoing a medical exam. Keep in mind that premiums typically increase with age and health risks.

If your policy includes automatic renewal, you can continue your coverage each year after the term ends—no new medical exams are required. While this ensures coverage regardless of health changes, it also comes with higher premiums, as you’re older and may be at more health risk than when you first purchased your policy.

Guaranteed renewal is a feature that lets you renew your policy even if your health has declined. With this option, your insurer cannot deny coverage, though premiums will increase. This is a good option for someone outliving their Term Life Insurance Policy but who cannot qualify for new coverage due to health issues.

Yes, most term life policies include a conversion clause. This allows you to convert your policy into a permanent Whole Life Insurance policy without needing a medical exam. It’s a solid option if your health has worsened and you want lifelong coverage after outliving your Term Life Insurance Policy.

Whole Life Insurance provides lifetime coverage and builds cash value over time. After converting, you can borrow against the policy or use it for estate planning. Just remember, Whole Life Insurance premiums are much higher than term life premiums.

It depends on your health and budget. If you’re in good health, buying a new policy might get you better rates than renewing your existing one under the Term Life Insurance renewal options. But if your health has declined, renewal or conversion might be safer choices.

Start by evaluating your current financial situation. Do you still have dependents, a mortgage, or other responsibilities? If yes, it might make sense to either renew or apply for a new policy. If not, you may decide to let the Term Life Insurance Policy lapse.

You can compare Term Life Insurance Policy quotes online from different insurance providers. This helps you find the best rates and coverage options based on your age, health, and coverage needs. Getting multiple quotes ensures you’re not overpaying after outliving your Term Life Insurance Policy.

Speak with a licensed insurance advisor. They can help you compare Term Life Insurance renewal options, explain the pros and cons of converting to whole life, and walk you through Term Life Insurance Policy quotes so you can make the best decision for your needs.

Sources and Further Reading

- Government of Canada – Life Insurance

https://www.canada.ca/en/treasury-board-secretariat/services/benefit-plans/management-insurance-plan/public-service-management-insurance-plan-life-insurance-glance.html

(Covers basics of term and whole life insurance, including expiry options.) - Canadian Life and Health Insurance Association (CLHIA)

https://www.clhia.ca

(Provides consumer guides and insights into life insurance products and conversions.) - Investopedia – Term Life Insurance Explained

https://www.investopedia.com/terms/t/termlife.asp

(Breaks down Term Life Insurance mechanics, renewals, and conversions in simple terms.) - Insurance Bureau of Canada (IBC)

https://www.ibc.ca

(General insurance guidance, including understanding policy coverage and renewal factors.) - Sun Life Canada – Life Insurance FAQs

https://www.sunlife.ca/en/insurance/life/

(Offers details on what happens at term expiry and conversion opportunities.) - Manulife – Life Insurance Options

https://www.manulife.ca/personal/insurance/life-insurance.html

(Covers various types of life insurance and what to do as policies mature.)

Here’s a feedback questionnaire designed to gather information about the struggles people face when trying to understand if Term Life Insurance can be considered a business expense. This version also collects the name and email address of the person filling it out.

Feedback Questionnaire: Term Life Insurance as a Business Expense

We’d love to hear from you! Please help us understand your challenges around using Term Life Insurance as a business expense by answering the questions below.

Thank you for your feedback! It helps us create more helpful content tailored to your needs.

IN THIS ARTICLE

Sign-in to CanadianLIC

Verify OTP