Have you ever thought about the cost of your mental peace? Specifically when it comes to ensuring your loved ones are cared for after you’re gone? In the world of financial security, Whole Life Insurance policies can be trusted with full faith. But, many of you might be wondering, at what cost? Today, let’s understand the monthly cost of Whole Life Insurance.

A Warm Welcome to the World of Whole Life Insurance

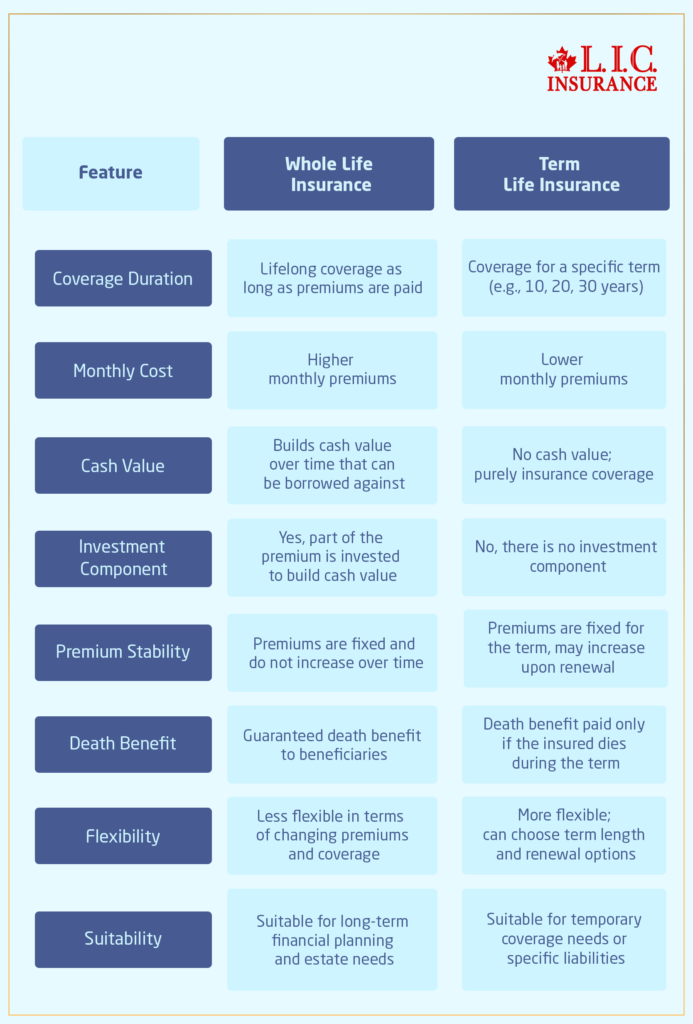

Can you think of financial protection that stays with you from the moment you grab onto it until your very last breath? That’s what a Whole Life Insurance Policy offers. It’s not just about the payout upon death; it’s about building cash value over time, a feature that distinguishes it from Term Life Insurance Plans. But with great benefits come great questions: “Is it too expensive for me?” Now, let’s get to know about this together.

Understanding Whole Life Insurance Monthly Cost

When talking about Whole Life Insurance, it’s essential to know that the monthly cost can vary widely. Several factors influence this, such as your age, health, the policy’s death benefit, and any additional riders you choose to add. But don’t let the complexity scare you!

Here’s a simplified table to give you a rough idea:

Age GroupApproximate Monthly Cost for a $100,000 Policy

| Age Group | Approximate Monthly Cost for a $100,000 Policy |

|---|---|

| 20s | $80 – $100 |

| 30s | $100 – $130 |

| 40s | $130 – $170 |

| 50s | $170 – $230 |

| 60s | $230 – $300+ |

Note: These are approximate figures to give you an idea. Actual rates can vary.

Is It Worth the Investment?

But you might say, “Those numbers look a little high! And yes, Whole Life Insurance can be more expensive than Term Life Insurance. But do you remember that cash value we discussed? That is a portion of your premium that accrues tax-deferred. As time passes, this becomes a considerable investment, which would not be available in Term Life Insurance.

Enter Maria, a 30-something young professional. Well, she decides to talk to an Expert who suggests her investing in a Whole Life Insurance Policy. Yes, she pays a higher premium every month than she would for a term policy, but she sleeps well at night knowing she’s building a financial cushion that her family can draw on or that she can borrow against if need be.

A Closer Look

Let’s try to do it with some more real stories to understand how this works:

- John, 40s, healthy: John buys a Whole Life Insurance Policy for $150 per month. Now, fast forward to 30 years later, John has a $200,000 death benefit for his family as well as a large cash value that he can tap into at any time, strengthening his financial safety net.

- Sara, 50s, with some low-level health issues: Sara pays a little over $220 a month for a premium. That sounds high, but given her health condition as well as the blanket coverage, it’s a strategic play for her peace of mind and her family’s financial future.

- Alex, 30s, super healthy: Alex started Whole Life Insurance in the early part of his career. He pays around $120 a month for a $250,000 policy. As the years go by, Alex not only receives the death benefit to his loved ones but also accumulates cash value that continues to grow, allowing him to access it for future financial needs, such as purchasing a home or paying for his children’s education.

- Linda, late 50s, smoker: Understanding the increased risks involved with her smoking, Linda chooses a Whole Life Insurance Policy. Her premium is about $350 a month for a $150,000 policy. Though the premium is expensive because of her age and smoking status, the policy will ensure her family has financial support in the event of an untimely death, and she likes that there is cash value accumulation she can access as another safety net.

These scenarios illustrate the versatility and lifetime advantages of Whole Life Insurance, demonstrating how policies can be customized to fit the individual situations of policyholders. But like we talked about before, the premiums sound high (especially for people like Linda), but the guaranteed death benefit together with cash value potential give you a dynamic way of planning for financial security.

Key Takeaways

Whole Life Insurance is a combination of insurance that gives you death benefit security and the chance to accumulate cash value over time. If you’re in tip-top shape, have increased risk factors, or are somewhere in between, there is a policy structure that should correlate to your financial goals and needs. It makes sense before explaining the entire process that better understanding these few examples can give you an insight into how people in every age group or with every history of health can reap the security and financial planning benefits of Whole Life Insurance.

Realize that these scenarios are simplified to illustrate the potential impacts and benefits. Actual premiums and policy values will vary based on many factors including your specific health status and lifestyle choices and which insurance provider’s policies you apply for. Always a good idea to reach out to a financial advisor or insurance specialist for a personalized quote and advice specific to your situation.

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Making the Decision

Now, you might be thinking, “Is Whole Life Insurance right for me?” It’s a valid question and one that deserves careful attention. Think about your long-term financial goals, your family’s needs, and how a Whole Life Insurance Policy fits into that situation. Yes, the premiums are higher, but the benefits extend well beyond your lifetime, offering a blend of financial security and growth potential.

Find Out: What is the biggest risk for Whole Life Insurance?

Concluding Thoughts: Time to Take Action

In conclusion, Whole Life Insurance is definitely more expensive than other forms of insurance, but the long-term benefits can be priceless. Not only is it insurance, but it is a financial strategy that scales with you, bringing peace and security to your dependents.

If you still haven’t taken the plunge, keep in mind that the sooner you buy, the cheaper your policy is likely to be. And how does that translate to what the world sees in general? Speak to a financial adviser if you pay to you line some numbers and decide if a Whole Life Insurance Policy is appropriate or not for you.

Because Whole Life Insurance is much more than Whole Life Insurance monthly costs. But perhaps Whole Life Insurance coverage may be the answer to that peace that we all seek.

Note: The numbers provided are for illustrative purposes only. For a detailed quote and more information, consult with a licensed insurance professional in Canada.

Find Out: The Benefits of Whole Life Insurance

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

FAQs on Whole Life Insurance Policy and Monthly Cost

Think of it as a safety net that’s always there, from the moment you say “yes” to it, till your very last day. A Whole Life Insurance Policy is just that. Unlike a winter coat that you outgrow or wear out, this policy sticks with you for your entire life, offering your loved ones financial protection and even growing a little savings pot (cash value) on the side. It’s like having a loyal friend who’s always got your back.

It works just like a subscription service, like your favorite streaming platform, but you’re getting contentment instead of movies. You pay a fixed monthly amount, which doesn’t change, making it easy to plan your finances. Part of this payment goes towards keeping your insurance active (so your family is protected), and part of it goes into a savings account within your policy, which grows over time.

It’s just like a subscription service, like your favourite streaming platform, except you’re getting contentment instead of the movies. You have to pay a certain amount of fixed price every month, which remains the same, making the planning of your finances easier. A portion of this payment is allotted to keep your insurance active (therefore protecting your family) and a portion of it goes to a savings account within your policy which grows, over time.

The awesome thing is that it absolutely does not! Your rate is locked in when you sign up, and it doesn’t change. So whether you’re just getting started or you’ve been with us for decades, your monthly cost is stable.

If you’re trying to live off the land using discount coupons, you’ll pay less, no? Similarly, although the monthly cost is fixed, you can “lower” your overall expenses by staying healthy (lower rates for non-smokers and healthy people) or choosing a plan that fits just so—not too big, not too small. It’s about striking the right balance that works for your needs and budget.

Like comparing an all-weather coat to a summer jacket, it may cost more to invest in the coat now, but you’ll get an extra layer of protection and a garment that lasts you through every season. In the same way, Whole Life Insurance provides lifetime coverage and accumulates cash value over time. So, compared to term insurance (the summer coat), it may seem more expensive, but actually, you are getting much more value for every rupee.

Absolutely! Consider your policy as a piggy bank. It grows when you continue to build on it over time. If you ever need to borrow, you can borrow against the cash value you’ve built. It’s like you are loaning money to yourself — with the intention to pay it back, of course. It is one of the unique perks that make Whole Life Insurance so different.

If you’re going to take an expensive trip. You’d need a map, right? Likewise, Whole Life Insurance needs some planning before the decision. Think about your long-term financial goals, your family’s needs and whether you want more than just insurance (such as a savings component). It’s somewhat like selecting the most suitable travel partner who’s on board for the long term with you.

That’s a roller-coaster ride, if you may. A word of caution: If you hit a bump in the road and struggle to pay your premium, relax. Most policies allow for a grace period, and you can catch up. Or, if your policy has accrued enough cash value, you could use it to fund your premiums for a time. It’s like having a spare battery for your phone.

Yes, it does! So, think of it like opening a seed in your garden. With some sunlight and water , over time, it blossoms into a huge, incredible tree. Just like that, the cash value in your policy accumulates as you pay it down with interest. This part of your policy is actively working, accumulating wealth, and providing future security.

Absolutely! When you retire, you can draw on the cash value you’ve accumulated over the years, treating it as a private pension to help fund your retirement.

Simply put, the death benefit is the money upon your death that your family gets, and the cash value is a savings component you can access while you’re alive.

Not always. It’s like applying to be a member at a club. Some clubs may want to greet you first; others will embrace you immediately. Like Whole Life Insurance, some plans may require you to take a health test before determining your monthly cost, though these plans also have “no exam” options. These may be slightly more expensive because the insurer is taking a greater risk by not assessing your health upfront.

A Whole Life Insurance Policy offers life coverage for the lifetime as the name itself suggests. It is your steadfast companion that remains at your side through thick and thin, from the policy’s inception to the end of your journey. The permanency of this benefit is part of why Whole Life Insurance is such a valuable component of long-term financial planning.

Yes, there are! It’s like a tiny financial canope. The cash value in your Life Insurance Policy grows tax-deferred, which means you do not pay taxes on the growth as it accumulates. And, if properly managed, the death benefit to your beneficiaries is generally tax-free.

Planting Seeds: Your Whole Life Insurance Policy With regular injections (which is your Whole Life Insurance monthly cost), this seed develops into a powerful tree. This tree gives here things important to you: A stable shade (protection of your family if you’re not here) and fruits (uncovering a method of saving something named cash value). It’s a lifelong commitment with lasting rewards.

Not only does whole life insurance provide lifelong financial protection for your family, but it also creates a cash value that grows slowly as you put money in it. It’s ideal for anyone who’s interested in long-term security and financial growth in one place.

Riders are like add-on components (for example, moon roofs) to your Whole Life Insurance Policy. Key options include:

- Accidental Death Rider: An Additional payout in case of an accident.

- Waiver of Premium Rider: This allows you to keep your policy in force if you are unable to work as a result of illness.

- Critical Illness Rider: It pays a lump sum when you are diagnosed with a serious illness.

These tailor your policy to better suit your needs.

Even if you are single, a Whole Life Insurance Policy can be a smart move. It makes sure your final expenses are paid and also saves up a cash reserve you can tap into later in life. These savings also lower the cost of Whole Life Insurance / monthly payments if you get insured while you are younger and prepare you for whatever comes next, alone or not.

We’re far from the only questions you might have here; however, the FAQs answered above are merely scratching the surface. We hope you’re now properly informed about Whole Life Insurance policies and their monthly costs. And, of course, everybody’s experience is different, so it’s a bit like searching for a glove that fits perfectly. If you’re interested or have further questions, you can ask an expert who can assist you and guide you toward making the right decision for you and your family.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com