- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Avoid RESP Withdrawal Penalties In Canada: Smart Strategies For Parents In 2026

By Pushpinder Puri

CEO & Founder

- 10 min read

- April 24th, 2026

SUMMARY

Canadian parents planning education savings in 2026 need clarity on RESP withdrawal penalties that Canada enforces and on changes to RESP withdrawal rules. The discussion covers Canada Education Savings Grant rules, government grants, RESP contribution limit in Canada, and how educational assistance payments are taxed. It also explains RESP funds for the apprenticeship program, RESP trends in Canada, and strategies to protect education savings while supporting a child’s post-secondary education.

Introduction

Canadian parents have done nothing in vain. According to recent federal statistics, over 60 percent of families with children are now enrolled in a registered education savings plan, and cumulative RESP assets in the nation have now broken into tens of billions of dollars. That is one thing that makes it clear that Canadians consider the education of their children very seriously. However, here is the bad news we witness annually, that is, many families lose grant money or incur the unwarranted income tax merely because they do not comprehend the rules of RESP withdrawal.

We come across parents who had done everything right over the years, and then dropped at the finish line. With stricter control, rising cost of living, and evolving trends of RESP in Canada, the cost of withdrawal errors is on the increase. This guide dissects the working reality of the penalty consequences on RESP withdrawal that the Canadian government implements, and how canadian parents can prevent them without panic, but through planning.

Understanding RESP Withdrawal Penalties In Canada Before They Hit Your Tax Return

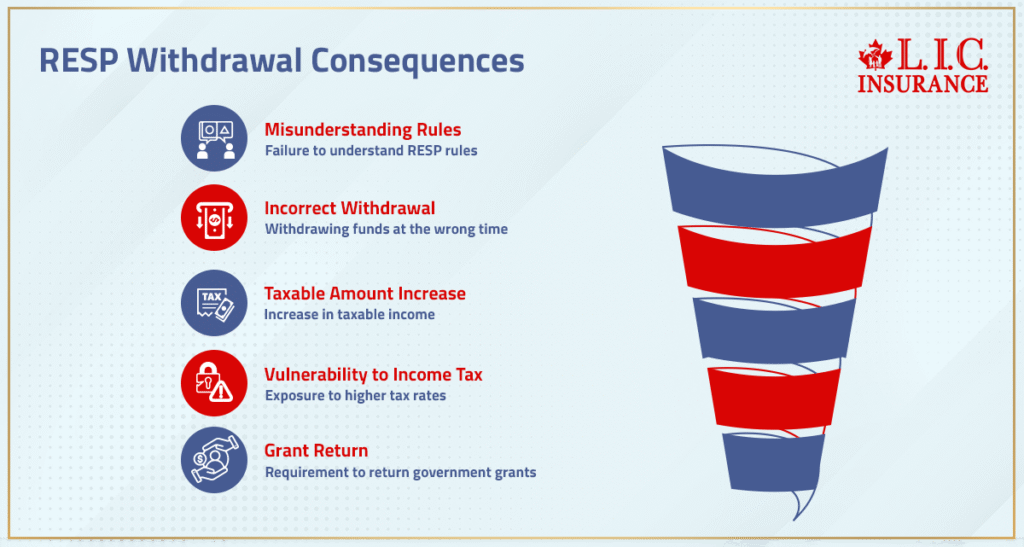

The penalties applied to RESP withdrawal are hardly described as such in Canada. They manifest themselves in silence, in your tax return. As soon as parents neglect the rules of RESP withdrawal, things begin to go wrong. The misunderstanding is usually because of failure to know that an RESP account has three buckets of cash.

First is your personal savings – the RESP that you had been contributing to over the years. Second is grant money, which is given by the government. Third is the earnings of investments that are made within the plan. Every bucket has varying tax consequences, and combining the two wrongly will result in varying tax consequences which are not anticipated by many families.

Pulling out money at the wrong time and place can raise the taxable amount of money, make the family vulnerable to annual income tax, or result in the return of grants. This does not seem dramatic in its early stages at all, until the CRA sends a notice.

Canada Education Savings Grant: How Government Grants Change Withdrawal Math

The Canada Education Savings Grant is, in a way, referred to as free money, and in several ways, it is so. Government handouts have conditions attached to them. The federal government makes contributions in the form of CESG that are pegged to the annual contributions and lifetime maximum contributions. In case of mishandling of withdrawals, grant money which increased the education savings could be recovered.

Victimized families are regularly observed to be taking out the RESP funds prior to a child even starting post-secondary education. The one timing mistake may evoke the refunds of the Canadian Education Savings Grant sums, despite the fact that the child enters school many months later. The grants given by the government are not based on intent, but on eligibility.

The CESG rules also have a strong level of interaction with the RESP contribution limit in Canada. The problem of making an excess contribution in excess of annual limits or neglect of carried-forward room can also make future withdrawals difficult. Whereas the resp contributions may be pliable on a year-to-year basis, CESG is not.

Canada Learning Bond And Lower Income Families: Avoiding Silent RESP Penalties

The families with low incomes are frequent beneficiaries of the RESP – and suffer most when errors occur. Canada Learning Bond is a federal program aimed at low-income families and provides money free, even in cases where families do not contribute any annual. Nevertheless, CLB has its tough withdrawal regulations.

We have also witnessed situations when families unintentionally collapse RESP accounts or withdraw early, and this leads to the loss of Canada Learning Bond sums that will have been used to fund the post-secondary education of a child in future. Since CLB is only accessible to canadian residents who qualify based on the amount of income, once lost, it is usually lost permanently.

In the case of the lower-income families, the RESP planning is not only beneficial but also critical.

Educational Assistance Payments Explained: The Line Parents Cross Without Knowing

Most of the penalties with respect to withdrawing the RESP in Canada are related to educational assistance payments or EAPs. EAPs are made up of grant funds and investment earnings. They are liable to taxation, not to parents. They are deducted from the student’s income.

That does not sound bad, and the income of a student is still taxable. Most students do not pay any tax or very minimal tax, but huge amounts of EAP withdrawn in one year can push income much above average. Then, suddenly, what the parents thought was tax-free is a reportable income tax.

One of the most intelligent RESP strategies that we would suggest is to spread educational assistance payments across years. The idea is to employ lower tax rates without evoking unwarranted tax considerations.

Using RESP Funds For Apprenticeship Programs, Trade Schools, And Non-Traditional Paths

RESPs can be found not only in universities. The apprenticeship program, trade schools and some professional certifications all qualify under the Resp funds as long as the school satisfies the post-secondary education requirements.

This is relevant in 2026, with an increasing number of students seeking post-secondary education under skilled trades and technical education programs and hybrid forms of education. Parents, who make assumptions on the basis of the processing of the RESP in the case of traditional higher education, tend to dispose of the funds improperly or significantly delay the funds inappropriately.

Depending on the status of enrolment, educational fees that are considered eligible can cover tuition, equipment, and even certain living costs. The knowledge of what falls under post-secondary definitions also ensures that the accessibility of resp funds is not eliminated when the families do not need them.

Contribution Rules Every Canadian Parent Must Respect In 2026

There has not been a significant change in the rules of contribution in regards to RESPs, but their enforcement has increased. The lifetime contribution limit is fixed on a beneficiary basis, and no annual limit is strictly applied to the contribution, although annual contributions would still be of importance in obtaining a grant.

Carried-forward CESG room is usually missed by such families who fail to do annual contributions planning. Some of them have surpassed the lifetime limit, and penalties have already taken effect before they can go to withdrawals. Patience and planning are rewarded in the RESP fund rather than last-minute financing.

Knowing the contribution room, thresholds of annual limits, and lifetime contribution limit guidelines would help parents avoid creating issues that would face them years down the line when accessing their withdrawals.

Asset Allocation Inside RESP Accounts: How Bad Investments Create Tax Problems

The withdrawal results of the RESP accounts are directly affected by the allocation of assets within the accounts. At very early stages, RESP can accept returns on growth-centred investment, but towards the withdrawal, risk tolerance has to change.

We have witnessed families remain so intensively invested in volatile holdings until the withdrawal years. Market movement may also bring a sudden capital gain or decrease investment capital at a time when its services are most required. Later conservative investments in the RESP lifecycle have less withdrawal stress.

RESP strategy is not a matter of pursuing returns – it is a matter of stability in time.

Mutual Funds, GICs, And ETFs Inside RESPs: What Creates The Least Tax Friction

The majority of the RESP accounts contain a combination of mutual funds, guaranteed investment certificates, exchange-traded funds, and, in some cases, money market funds. Each plays a role.

Mutual funds offer long-term growth and diversification but may also cause volatility. GICs provide a sense of stability, particularly at the time of withdrawals. Exchange-traded funds may be efficient and need discipline. Money market funds would be used to maintain capital over transitional years.

Investing based on the timing of withdrawal can help reduce the tax burden and save the education funds in case they are needed when they are required.

Family Plans And Family RESP Strategies For Multiple Children

Family plans are attractive to canadian parents who have more than one child. A family RESP enables flexibility in cases when one of the children does not proceed to receive post-secondary education or when a child postpones it. But there is complexity that is attached to family resp planning.

There are different rules when the shares of funds of many children exist. The fact that more than one beneficiary has to make withdrawals implies that they have to do it wisely to prevent the implementation of penalties or grant money. Professional RESP planning can help avoid the pitfalls of raising lots of children.

There are cases when multiple resp accounts may be more lucid, based on family composition and objectives.

Accumulated Income Payments: The Nuclear Option Parents Should Avoid

Accumulated income payments are made where investment earnings in the RESP accumulations would not be utilized, and the beneficiaries are not entitled to the withdrawals. These payments are taxed heavily, combining the standard tax on income with other charges.

In certain instances, accumulated income may be invested in RRSP contributions, provided the circumstances are followed. This is just a restricted and misconstrued option. One of the most costly errors made by parents is to leave RESP accounts to fall without planning.

RESPs are also meant to be kept open to the extent that they assist a child in the education process, as opposed to premature termination.

Choosing The Right RESP Provider And Financial Institution

Not all RESP providers offer the same flexibility. Banks, credit union options, and independent financial institution platforms differ widely. Some restrict investment choices. Others complicate withdrawals.

Parents increasingly request RESP quote online tools, but quotes alone don’t show withdrawal support quality. We help families assess RESP providers based on service, transparency, and withdrawal efficiency — not just growth illustrations.

Even major institutions like Royal Bank structure RESP services differently across branches. Choosing the right resp provider early simplifies everything later.

Education Savings Strategy For Canadian Families Heading Into 2026

RESP benefits are still considered one of the effective education savings instruments of canadian parents. RSPES continues to be superior to most other options, especially between Canada Education Savings Grant support, government grants, tax-free growth, and flexible withdrawal structures.

The system rewards knowledge, however. Family members can avoid the penalty of withdrawal of lifetime retirement savings in Canada by knowing the rules, making distributions, and keeping to the schedule. When assumptions are substituted with strategy, education savings are successful.

Canadian families making planned withdrawals to an RESP in 2026, based on the education choices of the child, the exposure to income tax, and the structure of their investments, ensure that more money is in its proper place: in the future of their child.

We do not feel that RESPs are merely accounts. They’re commitments. And when managed properly, they are all efficient, silent, and to the advantage of your family.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Yes, the living expenses like rent and food may be paid by using the RESP funds after a student is pursuing a qualified post-secondary education. The payments of educational assistance can be used on living expenses, but timing is important. It is also well structured to avoid any hidden costs that one would face due to taxation on income, and the child is also taken care of.

RESPs are able to stay open through a gap year without occasioning the penalty that Canada charges on the withdrawal of an RESP. None of the withdrawals must be made before the eligibility is determined. Conservative investment of the RESP funds this period assists in saving for education, but the plans are not fixed.

Yes, RESP funds can be invested in tuition and other education costs after one becomes eligible. The payments of educational assistance are non-obligatory, but subject to the regulations of RESP withdrawal. This is because clear records assist in guaranteeing that various tax implications are addressed appropriately during the tax return period.

In other instances, the RESP income can impact the benefits based on the income limits of the student. Although numerous withdrawals are not subjected to tax or only a small amount is taxed, the high educational assistance payments may be subject to taxable income. Spreading the withdrawals over a period of time can be a way of reducing the effect.

Yes, even within RESP accounts, one can still make adjustments to their asset allocation once the withdrawals have begun. Most of the canadian parents move towards conservative investments to lower the volatility. Risk tolerance should be aligned with the education savings left so that investment returns can be stabilized throughout the payout years.

Family friends or another family member’s contribution is permitted, but has to comply with the rules of contribution. Any contribution made annually will be added to the lifetime contribution limit. Linking with the RESP subscriber will avoid excessive funding and withdrawal problems in the future.

RESP funds can be provided in case the institution meets the conditions of post-secondary education. The eligibility regulations are different, and documentation is essential. Early confirmation of requirements can help canadian families to avoid grant money clawback and compliance problems.

Absolutely. RESP strategy ought to change to withdrawals approaching. Assessment of RESP advantages, investment income, and withdrawal sequence assists in lowering the taxation. Efficient planning ahead ensures that education savings remain efficient and in line with the education route of the child.

Sources and Further Reading

- Government of Canada – Employment and Social Development Canada (ESDC)

Official RESP rules, Canada Education Savings Grant (CESG), and Canada Learning Bond details

https://www.canada.ca/en/services/benefits/education/education-savings.html - Canada Revenue Agency (CRA)

Tax treatment of RESP withdrawals, educational assistance payments, accumulated income payments, and income tax reporting

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/registered-education-savings-plans-resps.html - Statistics Canada

Data on education savings participation, RESP adoption among Canadian families, and post-secondary education trends

https://www.statcan.gc.ca - Office of the Superintendent of Financial Institutions (OSFI)

Oversight and regulatory guidance affecting financial institutions offering RESP accounts

https://www.osfi-bsif.gc.ca

Key Takeaways

- RESP withdrawal penalties Canada applies often result from timing errors, not overspending, making planning as important as saving.

- RESP withdrawal rules treat contributions, government grants, and investment earnings differently, and mixing them incorrectly increases income tax exposure.

- Canada Education Savings Grant and Canada Learning Bond funds can be lost if withdrawals occur before post-secondary eligibility is confirmed.

- Educational assistance payments are taxed in the student’s income, and spreading withdrawals over multiple years often reduces taxable income.

- RESP funds for the apprenticeship program, trade schools, and other approved post-secondary paths remain eligible when institutions meet federal criteria.

- Ignoring the RESP contribution limit in Canada rules can create problems years later, even if early savings felt manageable.

- Asset allocation inside RESP accounts should shift as withdrawals approach to protect education savings from volatility.

- Family plans require extra care when more than one child or beneficiary is involved to avoid grant money clawbacks.

- Accumulated income payments carry heavy tax implications and are best avoided through early RESP strategy adjustments.

- Canadian parents who review RESP trends in Canada and coordinate withdrawals proactively keep more education savings working for their child’s future.

Your Feedback Is Very Important To Us

Avoid RESP Withdrawal Penalties In Canada: Smart Strategies For Parents In 2026

IN THIS ARTICLE

- Avoid RESP Withdrawal Penalties In Canada: Smart Strategies For Parents In 2026

- Understanding RESP Withdrawal Penalties In Canada Before They Hit Your Tax Return

- Canada Education Savings Grant: How Government Grants Change Withdrawal Math

- Canada Learning Bond And Lower Income Families: Avoiding Silent RESP Penalties

- Educational Assistance Payments Explained: The Line Parents Cross Without Knowing

- Using RESP Funds For Apprenticeship Programs, Trade Schools, And Non-Traditional Paths

- Contribution Rules Every Canadian Parent Must Respect In 2026

- Asset Allocation Inside RESP Accounts: How Bad Investments Create Tax Problems

- Mutual Funds, GICs, And ETFs Inside RESPs: What Creates The Least Tax Friction

- Family Plans And Family RESP Strategies For Multiple Children

- Accumulated Income Payments: The Nuclear Option Parents Should Avoid

- Choosing The Right RESP Provider And Financial Institution

- Education Savings Strategy For Canadian Families Heading Into 2026

Sign-in to CanadianLIC

Verify OTP