- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

How Much Does It Cost To Own A Home In 2026?

By Harpreet Puri

CEO & Founder

- 13 min read

- April 17th, 2026

SUMMARY

A complete look at the real costs of owning a home in 2026, covering Mortgage Insurance Canada, Mortgage Insurance monthly cost, home insurance, down payment requirements, property taxes, condo fees, utilities, and long-term expenses tied to home ownership. Buyers see how Mortgage Insurance Policy Coverage, market value trends, and ongoing maintenance shape overall affordability.

Introduction

The fact that one will own a home in 2026 is not the same as it was only several years ago. The real estate market in Canada changed once more following the interest rate cooling-down cycle of 2025. CMHC reported that purchase prices of residential properties in most provinces were at equilibrium, although the gradual reduction of the rates by the Bank of Canada made monthly mortgage payments slightly lower to new buyers. Statistics Canada also indicated that property taxes increased in some of the largest cities as the municipality responded to the increased operational costs.

We see this shift firsthand. The families come to our offices with feelings of hopefulness and nervousness. They want clarity. They desire to know the entire narrative, the actual expenses, and the financial obligations, as well as how features such as Mortgage Insurance Canada, home insurance, etc., are useful in maintaining their budget. What they do not desire is a surprise bill that is presented after six months of settlement.

We can then take this whole picture of owning a home in 2026, starting with that initial dollar of down payment, to the cost in the long run of owning and all the in-between.

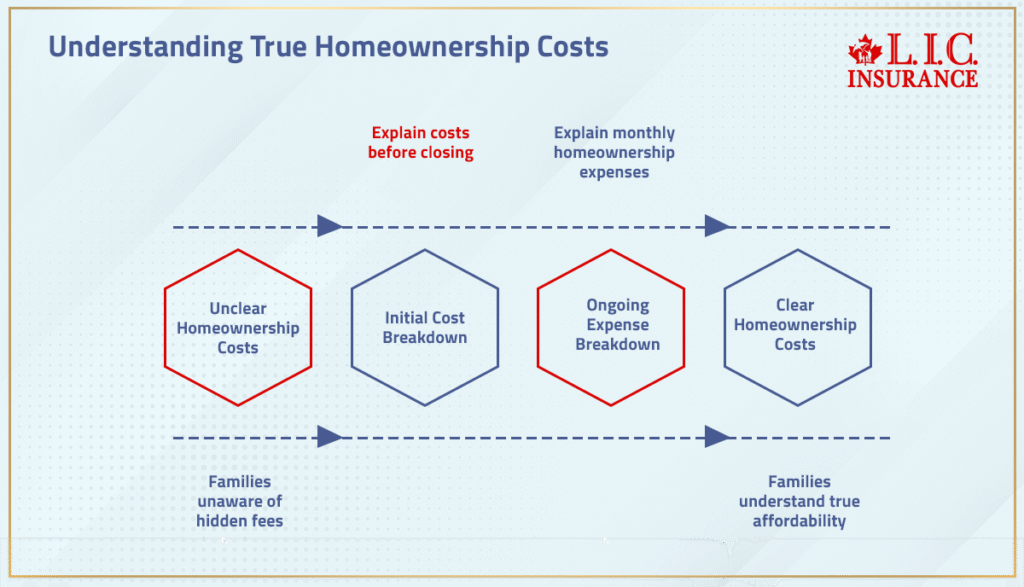

The True Costs Of Owning A Home

By 2026, families had understood one thing in a very clear way:

The entire story about your mortgage is not just that.

Affordability is determined by how well you know the true costs associated with your home, even with more stable interest rate conditions. And those fees go on long after you take your keys.

When we guide families through home-buying decisions, we break everything into two parts:

- Initial costs — the ones that hit before closing

- Ongoing expenses — the ones that hit every month

Both matter equally.

Down Payment: Your First Big Step In Home Buying

The amount of your down payment defines it all, including the amount of your loan and the price of your Mortgage Insurance.

The minimum down payment arrangement in 2026 will not be different for most first-time buyers, although increasing market value in the towns implies more initial requirements for purchasers.

The bigger the down payment, the less you borrow and the premium charged to Mortgage Insurance offered by lenders can be decreased should you put down less than 20. This is a mere procedure that can save you a lot in paying each month in the future.

This affects families who prefer one family home or semi-detached home the most since these types of homes often have a high market value, so that the down payment is forced to enter into an expensive territory.

Appraisal Fee: Confirming The Home's Purchase Price

It is possible that prior to your lender financing you, they might order an appraisal to determine the value of the home.

Here comes the appraisal fee, which is generally between 200 and 300.

As of 2026, lenders are still largely dependent on appraisals since the value of a home differs drastically based on the neighbourhood. As real estate trends vary, the lenders would wish to see that the value of the home, as assessed by them, matches the real market price.

Home Inspection Fees: The Smartest Money You’ll Spend

One of the shortcuts that Canadian LIC should never prescribe is the omission of an inspection.

The home inspection cost varies between $300 in the case of condos and up to $800 in the case of houses.

Inspectors find out structural problems, roof problems, plumbing problems and electrical problems that may cost thousands in future. Now, in the year 2026, as the old homes are growing old in various provinces, knowledge of inspection has become all the more significant, particularly to the buyers who are keen to relocate in a hurry.

Legal Fees: Protecting Your Most Important Transaction

Having a real estate attorney or notary cover you at the time of closing.

These are legal charges, which range between 900 and 3,000 dollars to review the contract, title search, adjustments, disbursements and compliance checks.

Each year, we receive clients who attempt to save money by not following the correct legal procedures and end up with problems down the road with respect to boundary issues, title issues, or the condition of the properties that were not recorded.

The lawyer can also not be flashy, but he or she spares you some costly mistakes.

Land Transfer Tax: The Up-Front Cost Everyone Forgets

All purchasers are subject to land transfer tax, which is charged on a percentage basis of the value of the property.

This will be applicable in most provinces and may vary between 0.5% and above 3%.

In 2026, the rise in the municipal budgets in larger cities caused some buyers to jump into different brackets, i.e., larger bills were received by the family shortly after the transaction was closed. It is also one of the most common expenses that are overlooked in the process of buying a home early.

Condo Fees: The Real Price Of Low-Maintenance Living

Condos are associated with condo fees when it comes to a dream home owned as a condo.

The fees normally vary between 250 and 1,000 per month, depending on the building, amenity and maintenance structure. In other current developments, the increase in the cost of energy and repair has increased the cost of fees in 2026.

It all depends on knowing what is covered: heating, water, utilities, snow removal, or common areas maintenance, as buildings are all vastly different.

Home Insurance: Your Safety Line In 2026

All homeowners require home insurance.

By the year 2026, the extreme weather conditions will have led to changes in insurance premiums all over the country. That is, a good number of homeowners were experiencing increased costs since they were not making claims.

Home insurance is a cover that covers fire, theft and accidental damage, besides covering liability.

We also take clients on a tour of coverage to ensure that the policy fits the value of his or her property and the truth of 2026.

Mortgage Insurance: Why It Matters More In 2026

This is one of the most common financial blind spots for buyers.

Lender-Required Mortgage Insurance (CMHC)

In case your down payment is less than 20%, the lender will need Mortgage Insurance Canada.

The lower the down payment, the higher the premiums are. The added premiums are added to the mortgage, and they have a direct effect on the monthly Mortgage Insurance cost.

As home prices stabilize, but continue to be high in most urban centers, a significant number of buyers in 2026 will be covered by CMHC insurance.

Mortgage Life Insurance Plan

This is not mandatory but significant.

It pays the mortgage in case of untimely death of the homeowner. One of the ways the families defend their investment is through it. We are comparing the difference between Mortgage Insurance and Life Insurance because our clients want to choose the one which will really protect their family, not only the lender.

When a person requires real numbers, we will offer them a personalized quote for the Mortgage Insurance, based on their income, the type of property, and their long-term objectives.

The Costs Of Owning A Home: What You’ll Pay Every Month In 2026

Once the housewarming balloons deflate, the real financial journey starts.

Your biggest long-term expenses fall into:

- Mortgage payments

- Property taxes

- Utilities

- Home insurance

- Condo fees (if applicable)

- Heating, water, and electricity

- Maintenance

- Snow removal

- Lawn care

Even with interest rates easing in 2026, these ongoing obligations remain steady. And because inflation impacts services, maintenance, and materials, the costs of owning continue to rise slightly each year.

Lawn Care: The Cost New Homeowners Forget

Regardless of whether you are making a purchase in the suburbs or you are moving into a quieter neighbourhood, lawn maintenance is expensive.

Pruning, clipping, cultivating, machinery, manure — every effort draws a little out of your purse.

This is particularly evident in families that are relocating into larger homes, with the yard size and maintenance increasing directly in proportion to the enthusiasm for having more space.

Hidden Costs: The Quiet Budget Drainers

The most financially stressful part of owning a home isn’t usually the mortgage — it’s the hidden costs that no one warns you about:

- Hot water tank issues

- Furnace maintenance

- Emergency plumbing

- Roofing patches

- Dryer vents

- Window resealing

- Appliance replacements

Everything inside a home eventually ages.

In 2026, these replacement costs are slightly higher than in previous years due to labour and supply chain pressures.

We encourage every homeowner to keep a small emergency fund specifically for these surprises.

Home Buying In The 2026 Market

By 2026, Canada’s real estate environment will feel calmer but not cheap.

Interest rates declined gradually through 2025, but not enough to return to pre-pandemic affordability. Buyers still face elevated expenses, especially in major cities.

CMHC’s 2026 outlook highlights:

- More stable home prices

- Stronger buyer confidence

- Slightly improved affordability

- Market conditions are shifting from “cooling” to “balanced.”

This is good news for buyers who felt priced out earlier.

But the financial responsibility remains serious.

Home Ownership: The Emotional And Financial Reality

It is satisfactory and challenging to own a home in 2026. People continue to experience the sense of pride, the feeling of being stable, and the happiness of having a place of their own. They are more aware of their responsibility than ever before, too.

We hear of homeowners each week who say the same thing:

When we got to know all the figures, it was all clear. Stress went down. Confidence went up.”

That is the strength of walking into home ownership with complete transparency.

Bigger Houses: Bigger Bills And Bigger Choices

To the family that is looking to buy larger homes, the most significant change in 2026 will be the utility and repair prices. Big houses imply more heating, more repairs, more water bills, and even larger tax bills.

This does not imply that you should not make huge purchases; it is only that you should enter into the venture knowing your own size.

Budget Planning: Your Best Protection In 2026

Budgeting is the backbone of successful home ownership.

We help families create plans that balance:

- Payment schedules

- Utilities

- Insurance

- Regular maintenance

- Emergency savings

- Property tax expectations

- Seasonal expenses like snow removal

This prevents homeowners from becoming house poor — a situation we work hard to protect clients from.

Home Buying + Insurance: Your Long-Term Safety Strategy

Your home is your biggest asset, and every part of your financial structure should protect it.

That’s why we emphasize the connection between:

- Mortgage Insurance Policy Coverage

- Mortgage Life Insurance Plan

- Home insurance

Together, these create stability for your family and safeguard your long-term value.

Home Ownership In 2026: The Clear Picture

Sum it all up: the initial costs, the monthly payments, the replacement costs over a long period of time, and the insurance costs, and you have a full picture of what it actually costs to own a home in the year 2026.

The families are successful when they do not enter into home ownership with surprises. We have taken thousands of buyers on this trip, and every year our message remains the same:

The correct strategy is everything.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

The monthly expenses keep increasing due to the fact that the cities are raising their property taxes to cover the increase in the operation costs, and the utility companies and repair companies are raising the prices of their services. Then add some seasonal spending, such as lawn care and snow removal, and your monthly expenses swell automatically. Homeowners, even with the stable rates, experience this pressure.

This is the reason why the appropriate Mortgage Insurance Canada structure can keep the bigger picture intact.

The good coverage of a Mortgage Insurance Policy covers your home loan in case of unexpected income breaks, particularly when you are still getting used to the initial expenses of owning. It provides you with breathing space as your savings increase and protects you against shocks in payments.

The families in 2026 rely on this to cushion the increasing service costs and the randomness of the repair process.

It is there as an insurance policy to make your home ownership plan stable.

Condo fees provide predictability and less individual responsibility when it comes to maintenance for many buyers. Common areas, upkeep, and seasonal activities are often dealt with in buildings; they would otherwise consume your time.

With all the utility and contractor costs increasing, the bundling of these services will, in fact, reduce your cost in the long run.

It is not a fee as such, but how to handle your property and not house the poor.

Surely, cosmetic improvements will not show more serious problems. The virtue of a good inspector is to assess structural sections that determine the long-term value and future costs of repair. Even new houses may conceal the issues that concern heating, water flow, or safety.

By not conducting the inspection, you will be saving money today and paying more tomorrow.

Smart checkup secures your home purchase price.

An individualized Mortgage Insurance quote makes you realize what you will actually commit to on a monthly payment before emotions come in during home purchasing. It explains the influence of your budget based on your loan amount, down payment and term.

This avoids shocking news that comes at the end of the day due to your mortgage lender.

It is a little step that will allow you to have more influence on the price you would pay each month.

The most effective tactic would be to calculate what is unknown, the increase in water bills, and continual maintenance prior to the deal being made.

Establish a realistic budget, which covers utilities, seasonal maintenance and repairs of the future.

Compare insurance- An insurance plan that is flexible, such as a life mortgage, can also be used to assist in protecting cash flow.

Rational planning helps to avoid turning your new house into an economic burden.

The property tax rates are adjusted by cities in accordance with inflation rates, infrastructure and increasing neighbourhood service requirements. The increase in the value of the assessed home is usually accompanied by higher taxes.

This change affects your annual cost if your mortgage payment remains constant.

It is one of the largest cost areas that buyers do not take into consideration during long-term planning.

It is important to update your budget on a yearly basis so that you can be ahead.

The bigger houses are associated with increased maintenance requirements, heating and water expenses.

You will also waste more time and money on keeping your lawn and seasonal maintenance.

Even your home policy can increase due to the fact that increased space usually equates to increased goods to cover.

The families are satisfied with the room, yet the constant costs should be clearly planned.

Yes — both will be able to stabilize your financial structure when costs increase.

A Mortgage Life Insurance Plan will also make sure that your family does not find it hard to pay the loan in the event that something unforeseen occurs.

Mortgage Insurance is mandated by the lender to ensure your financing becomes available with a reduced down payment.

They combined would assist in maintaining your long-term home ownership experience.

The rates are stabilizing, and the growth of prices is moderate, which means that 2026 will be more predictable compared to the past few years.

The wait is not necessarily the way to reduce the market value, not to mention that the real estate cycles change rather rapidly.

Concentrate on the fact that your monthly expenditures are comfortably covered by your budget, and not the time when you are going to buy it.

Even with a well-balanced income and savings, the right home will remain a good long-term investment.

Sources and Further Reading

Statistics Canada (Housing, Prices, Property Taxes)

https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=3410015801

https://www.statcan.gc.ca/en/subjects-start/housing

CMHC – Mortgage Insurance, Housing Outlook, Affordability

https://www.cmhc-schl.gc.ca/en/consumers

Bank of Canada – Interest Rates, Economic Indicators

https://www.bankofcanada.ca/rates/

https://www.bankofcanada.ca/core-functions/monetary-policy/

CREA (Canadian Real Estate Association) – Market Value & MLS Trends

https://www.crea.ca/housing-market-stats/

https://www.crea.ca/publications/

FCAC – Mortgages, Home Buying Costs, Budgeting

https://www.canada.ca/en/financial-consumer-agency/services/mortgages.html

https://www.canada.ca/en/financial-consumer-agency/services/buying-home.html

Insurance Bureau of Canada – Home Insurance

MPAC (Ontario) – Property Assessments & Tax Factors

Provincial Land Transfer Tax Resources

Ontario – https://www.ontario.ca/document/land-transfer-tax

BC – https://www2.gov.bc.ca/gov/content/taxes/property-taxes/property-transfer-tax

Canadian Bar Association – Legal Fees & Real Estate Guidance

https://www.cba.org/For-The-Public/Buying-a-Home

https://www.cba.org/For-The-Public

Royal LePage – Housing Reports

Key Takeaways

- Owning a home in 2026 involves more than mortgage payments; buyers must prepare for rising property taxes, utilities, maintenance, and seasonal lawn care costs that affect long-term affordability.

- A stronger down payment can lower your Mortgage Insurance premium and reduce what you pay per month, especially when purchasing a single-family home or semi-detached home with a higher market value.

- Protection tools like Mortgage Insurance Canada, a personalized Mortgage Insurance quote, and the right home insurance plan give families stability as ongoing expenses shift through the year.

- A clear budget that factors in condo fees, legal fees, repair cycles, and hidden costs helps prevent buyers from becoming house poor and supports confident, long-term home ownership in 2026.

Feedback Questionnaire:

A quick check-in to understand what you’re dealing with and how we can guide you better.

IN THIS ARTICLE

- How Much Does It Cost To Own A Home In 2026?

- The True Costs Of Owning A Home

- Down Payment: Your First Big Step In Home Buying

- Appraisal Fee: Confirming The Home's Purchase Price

- Home Inspection Fees: The Smartest Money You’ll Spend

- Legal Fees: Protecting Your Most Important Transaction

- Land Transfer Tax: The Up-Front Cost Everyone Forgets

- Condo Fees: The Real Price Of Low-Maintenance Living

- Home Insurance: Your Safety Line In 2026

- Mortgage Insurance: Why It Matters More In 2026

- The Costs Of Owning A Home: What You’ll Pay Every Month In 2026

- Lawn Care: The Cost New Homeowners Forget

- Hidden Costs: The Quiet Budget Drainers

- Home Buying In The 2026 Market

- Home Ownership: The Emotional And Financial Reality

- Bigger Houses: Bigger Bills And Bigger Choices

- Budget Planning: Your Best Protection In 2026

- Home Buying + Insurance: Your Long-Term Safety Strategy

- Home Ownership In 2026: The Clear Picture

Sign-in to CanadianLIC

Verify OTP