- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

5 Essential Insurance Steps Every Canadian Should Take Before Buying a Home

By Pushpinder Puri

CEO & Founder

- 12 min read

- April 13th, 2026

SUMMARY

Home buyers in Canada get a clear path to protect their purchase using insurance for home buyers in Canada, Mortgage Insurance Plans in Canada, and Life Insurance for homeowners in Canada. The content explains key steps for securing mortgage payments, preparing for closing costs, strengthening financial readiness, and ensuring long-term protection when buying a home.

Introduction

Extreme sports athletes require a financial safety net designed to handle unpredictable terrain, sudden changes of weather, and physical demands that far exceed those associated with the average lifestyle. “Insurance is not a product; it is a blueprint for protection.” Instead of one insurance, imagine if you had coordinated coverage that protects you at every level. Unless you are paying for your house in cash (not recommended because prices would increase once we review our financial situation buying a house in cash could likely debilitate most families’ income generation. In Canada, buying a home is one of the biggest financial commitments most individuals and families will make. And as prices increase, so too do the risks. The national average home price was up more than 8% year-over-year, according to the Canadian Real Estate Association (CREA), and mortgage debt in Canada surpassed $2.1 trillion, according to CMHC data. Throw in a dynamic interest rate cycle, varying closing costs, and unexpected mortgage payment surprises — and you see why smart insurance planning is necessary to protect every decision.

We meet homebuyers daily – families who’ve outgrown their first home, newcomers to Canada navigating the real estate world, online workers looking for a new place to live, and investors keeping an eye on rising markets. They all ask themselves the same question, she said: “What happens to my home if something happens to me?”

This is precisely where home buyers’ insurance Canada becomes more than just a box to tick. It’s the basis that all of your home buying, income, mortgage, and family decisions are safeguarded by in the long term.

Here are the five key insurance steps every Canadian should take before they buy a home—fueled by actual financial planning, real positioning within our industry, and the experience we bring to you.

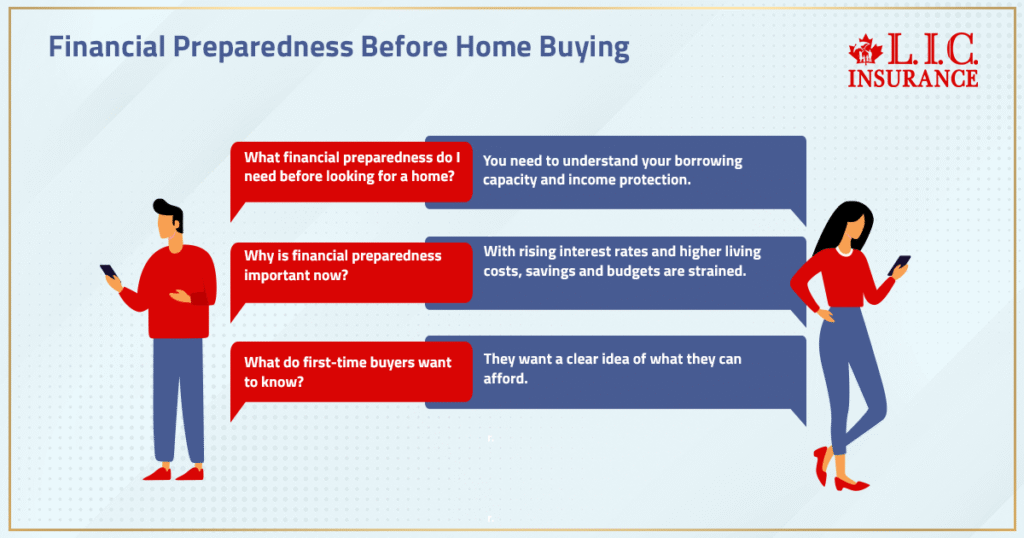

Understanding Financial Readiness Before Buying A Home

Before you start looking for a home, you’ve lost this financial preparedness. With interest rates rising, adjustable bi-weekly mortgage payments, and the higher costs of everyday life, there is a lot of strain on savings and budgets, as well as affordability.

When we drill into motivations, many first-time buyers tell us they want to “get a clear idea” of what they can afford. The clarity starts with two items: borrowing capacity and income protection.

Reviewing Income Stability And Long-Term Planning

When your mortgage payment is your largest monthly expense, a temporary gap in income can throw everything into disarray. When the typical mortgage payment in some major cities exceeds $3,000 — and that’s before adding a penny for utilities, property taxes, insurance, or other housing-related costs — it makes protecting your income less of an option.

This is precisely where life insurance for homeowners in Canada comes into play. Mapping out your risk exposure even before the purchase offer stage is there to ensure that you have the financial means for both short-term and long-term home ownership.

And the work-from-anywhere trends also affect affordability, savings, and its capacity to pay future obligations. That fickle income, as thousands of our clients have shown us, is the fuel that should power responsible home ownership.

Estimating Borrowing Capacity And Budget Management

How much you can borrow depends on your income, credit rating, current debt ratios, and the interest rate environment, as well as your long-term financial goals. A good credit score allows you to get a better mortgage, which grants more flexibility in your buying process.

As lenders are crunching your ratios, yours is to make certain your budget, monthly outlays, and long-term money matters can handle the unforeseen irregular events of life — say an accident or chronic illness that prevents work; a job change; a turn in the economy.

This is one reason that our clients may combine Canadian Term Life Insurance rates with budgeting based on mortgage payment, property tax, and the cost of living for long-term financial stability.

Step 1: Prepare For Your Down Payment With Proper Insurance Planning

Your down payment is likely the product of years of saving money, making sacrifices, and planning — an especially daunting reality for first-time buyers grappling with increasing home prices and minimum down payment requirements.

Whether you are saving in personal accounts, transferring RESPs for planning down the road, or optimizing tax-efficient financial readiness strategies, the risk is still there:

If you get hit by a bus, who finishes buying the house?

This is when insurance becomes the shield that defends your largest savings milestone.

Why Insurance Matters Before You Pay The Down Payment

Families who are entering into the process of saving for a down payment often don’t realize how much financial risk they are taking here. Surprise medical emergencies, accidents, or income interruptions can screw it all up in weeks.

This is why many families include Life Insurance for homeowners early on in the process, and even Term Life Insurance for homeowners prior to making an offer.

This coverage also reduces the strain of potentially having to pay for property taxes, unanticipated unforeseen repairs, or other financial concerns at a time when you’re least suited to cover these costs.

How Term Life Insurance Protects Your Down Payment

One of the most affordable ways for homeowners to protect their savings is with Term Life Insurance. And if something were to happen to a primary wage earner, your family still has the financial ability to go on with buying the home.

Whether you’re keeping property equity or covering incidental expenses that arise during purchase planning, these polices offer instant security while ensuring premiums are manageable.

Step 2: Explore Mortgage Options And Protect Yourself With The Right Coverage

Choosing the right mortgage is one of the most involved decisions in the entire home-buying journey. There are dozens of variables:

Fixed vs variable, amortization, Mortgage Loan Insurance, mortgage pre-approval, lender terms, and more.

Comparing Mortgage Products In Canada

Whether you’re navigating mortgage payment structures, calculating long-term mortgage payments, or reviewing different mortgage options, insurance planning should happen in parallel—not afterward.

During this stage, many buyers also review:

- Canada mortgage rules

- Pre-approved lender requirements

- Future mortgage payment increases

- How financing shifts affect affordability

This is where a strategic lens becomes essential.

Insurance You Need While Exploring Mortgage Options

During the mortgage selection stage, the most important protection tools include:

1. Mortgage Insurance Plans In Canada

These plans ensure your mortgage is covered if a major life event threatens your income.

2. Critical Illness Insurance For Mortgage Payments

With rising medical costs in Canada, this coverage protects your payment obligations if a serious illness stops you from working.

3. Disability Income Protection (Optional Add-On)

Essential during financing transitions or uncertain income periods.

As lenders evaluate your borrowing capacity, insurance becomes the safety net supporting your mortgage decision-making.

Step 3: Insurance Protection During The Buying Process

The buying process is where risks multiply. From inspection surprises to financing conditions, appraisals, delays, and negotiations—every moving piece affects your financial well-being.

Understanding Risk While Buying A House

When Canadians begin buying a house, they often underestimate how much exposure they have until closing day. Your purchase contract, lender conditions, and pre-move expenses all add new layers of responsibility.

During this period, families often choose to activate:

- Term Life Insurance rates in Canada

- Term Life Insurance for homeowners

These protect mortgage approval strength, lender requirements, and family security.

This stage includes everything from the home-buying process to reviewing the sale agreement, managing the purchase, and finalizing the home-buying decisions.

Home Insurance And Additional Coverage During The Buying Stage

Before the purchase offer, some coverage becomes essential:

- Home insurance (often required by lenders)

- Additional coverage for valuables, liabilities, or repairs

- Reviewing coverage options

- Preparing for home purchase conditions

You’re protecting your investment before it’s officially yours—which is a crucial step many buyers skip.

Step 4: Covering Your Bases Before Closing Costs Arrive

No stage drains buyers faster than closing costs. These fees can climb quickly, especially when you include:

- Legal fees

- Additional costs

- Property tax adjustments

- Other costs associated with the transfer

- Municipal welcome tax (in certain provinces)

Many buyers experience shock at how high these can climb.

Insurance You Need Before Paying Your Final Closing Amount

Before you finalize your closing costs, you must prepare:

- Mortgage Insurance Plans in Canada (aligned with lender requirements)

- Protection for your process timeline

- Ability to document carefully

- Assurance during address changes, transitions, and update utilities steps

Insurance ensures any disruption doesn’t affect your ability to close on time.

Step 5: Prepare Insurance For The Closing Day And Move-In Stage

Closing day is the finish line—but also the most vulnerable day in the entire journey. Your new home, house, and new house all transition ownership, and liability officially transfers to you.

Insurance You Must Have Active On Closing Day

On closing day, essential protections include:

- Life Insurance for homeowners in Canada

- Critical Illness Insurance for mortgage payments

- Updated home insurance

This is also when your home ownership becomes official. No gaps. No risks.

What Happens After Move-In (Insurance Checklist)

Once you’re inside your new home, here’s what every responsible homeowner does:

- Review home inspection reports

- Reassess inspection results for future repairs

- Keep clean socks ready because movers will walk everywhere

- Do a safety walkthrough

- Confirm utility transfers

- Begin the list of must-haves

- Review repair costs

- Negotiate repairs where applicable

- Cross-check your home search expectations with reality

These steps help ensure stability during your transition.

Bonus Step: Estate Planning For Homeowners

Even though it’s often overlooked, estate planning for homeowners is one of the most important parts of long-term protection. Your home is an asset. It must be protected through:

- Life Insurance

- Will planning

- Transfer strategies

- Managing property taxes in long-term planning

- Protecting property for future generations

This ensures your home doesn’t become a financial burden for your loved ones.

Final Thoughts For First-Time Buyers

From beginning to end, the home-buying process is a lot for first-time buyers to undertake. Selecting the best real estate agent, searching top real estate trends, getting better mortgage rates, and finding an experienced realtor are all very significant—but without having a proper insurance foundation in place—none of these matters.

From the protection of your savings, to covering your mortgage, and even managing long-term risks – insurance is truly what can make or break a house purchase and other financial stability in the future.

Conclusion — Making Your Home A Wise Investment

Purchasing a home entails more than signing papers and agreeing on the purchase price. This is about protecting your family and your financial future, as well as the opportunity to bring hope to a land that isn’t blessed with what you have.

We make it easy to provide a protection strategy that touches every part of your journey—from the day you throw down your first payment until your closing day and beyond into home ownership.

Whether it’s:

- Life Insurance for homeowners in Canada

- Mortgage Insurance Plans in Canada

- Critical Illness Insurance for mortgage payments

- Long-term estate planning

—your protection plan should move with you, grow with you, and secure everything you’ve worked for.

Your home is more than a property.

It’s stability.

It’s family.

It’s your future.

And we’ll help you protect it.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Mortgage Insurance Canada for home buyers in Canada provides families with a cushion as they plan their down payment and estimate how much they can borrow. Unforeseen circumstances can affect you financially well before a mortgage approval. Being protected from early on enables you to glide through the ‘buying a home journey’ with many reduced risks. It also keeps your long-term affordability consistent as you pursue the goal of purchasing your first home.

Homeowners Life Insurance Canada provides permanent protection that will include more than just your mortgage. It gives families a way to stay put even when income changes, property taxes rise, and household costs shift. This is relevant when purchasing a home in an uncertain interest rate environment. It also boosts your financial preparedness, all while you are a homeowner.

It protects your budget in case health problems disrupt your income, with Critical Illness Insurance for mortgage payments. Large medical events may limit how much you’re able to cover with everyday expenses or updates on home insurance, or pay in closing costs. This safeguard helps to maintain your course toward owning a home, even through life-altering events. That’s a boon, especially for first-time home buyers who are trying to save for their first purchase.

Bundle products offer a way for first-time buyers to remove some of the complexities of buying and make their extra costs more manageable. It helps in establishing a budget for the long term as it reduces the pressure of payments during the first few months of owning a house. This is particularly helpful if you are saving to purchase a home, when closing day and on-going maintenance contributions will be part of the process. A programmatic approach to buying a home also helps bolster the safety net around realizing the American dream.

Getting the correct coverage plan in place early can be a confidence boost as home buyers navigate inspections, purchase timelines, and challenges finding homes. It secures your financial footing as you no longer have interest payments draining where your savings used to be. It also protects your capacity to borrow during lender assessments. This maintains your home-buying decisions both well-anchored and tough.

Extra expenses such as legal costs, property tax adjustments, or repairs can quickly strain your budget. Strategic coverage acts as a buffer in case unexpected expenses arise while buying a new home. Protection also protects your payment schedule and financing when they come under pressure. This ensures that the new homeowners can afford their homes through every step of the home-buying process.

Yes, because Mortgage Insurance covers only the lender’s interest — not your whole financial situation. Extra insurance protects your family in case income is halted, unexpected costs arise, or interest rates spike. It also assists you in preparing for the estate responsibilities that come with long-term property ownership. For many Canadians, that extends well beyond the mortgage itself.

Good coverage means getting the best prepared as you shop for mortgages and compare lenders. Insurance stabilizes your capacity to pay if interest rates move up or down, or if your income changes. That gives buyers more negotiating power to select the right mortgage for their long-term goals.” It also helps retain some predictability and control in the buying a home process.

Insurance spreads risk during your home-buying journey and allows you to avert the financial hardship of surprise events. And it leaves room in your budget and borrowing limits for new responsibilities. Consistent protection means affordable rates as you move into home ownership. This method makes purchasing a house a safer, long-term proposition.

Real estate markets are fast-moving, so buyers should expect quick changes in purchase conditions and in financing. Insurance provides financial security in case income, expenses , or mortgage costs change unexpectedly. This is particularly useful when project timelines are unpredictable. It protects your long-term home ownership goals through the ups and downs of the market.

Sources and Further Reading

1. Canada Mortgage and Housing Corporation (CMHC) – Homebuying Step-by-Step

Covers mortgages, down payment rules, closing costs, Mortgage Insurance, and the entire home-buying process.

🔗 https://www.cmhc-schl.gc.ca/en/consumers/home-buying

2. Financial Consumer Agency of Canada (FCAC) – Mortgages & Buying a Home

Government guidance on mortgages, interest rates, borrowing capacity, pre-approval, and budgeting.

🔗 https://www.canada.ca/en/financial-consumer-agency/services/mortgages.html

3. Insurance Bureau of Canada (IBC) – Home Insurance Explained

Covers home insurance, additional coverage, liability protection, and claims guidance.

🔗 https://www.ibc.ca/on/home

4. Government of Canada – Homeownership, Property Taxes & Programs

Complete overview of government programs, tax rules, homeowner benefits, and property-related responsibilities.

🔗 https://www.canada.ca/en/services/finance/manage/housing.html

Key Takeaways

1. Insurance Strengthens Your Financial Readiness Before Buying A Home

Protection helps home buyers in Canada handle unexpected income changes, rising expenses, and shifting interest rate conditions. It supports borrowing capacity while preparing for a down payment and stabilizes long-term affordability.

2. Mortgage Insurance Plans In Canada Protect Your Largest Payment Commitment

With mortgage payments becoming a major monthly responsibility, the right coverage shields your financing from sudden disruptions. It helps keep the buying process on track and supports first-time buyers managing early expenses.

3. Life Insurance For Homeowners in Canada Safeguards Family Stability

Coverage ensures your partner or family can stay in the new home even if unexpected events occur. It reinforces long-term home ownership goals and protects financial plans built around buying a house or securing your first home.

4. Critical Illness Insurance Supports Mortgage Payments During Health Crises

A serious illness can interrupt income and affect your ability to pay for closing costs, property taxes, and required home insurance. This coverage keeps your home-buying journey steady when health challenges impact your financial situation.

5. Insurance Reduces Stress During The Buying Process And Closing Day

Smart protection helps manage additional costs, legal fees, and unplanned repairs. It keeps the buying a home timeline organized, supports the closing day transfer, and protects families entering their new home with confidence.

Feedback Questionnaire:

We’d love to understand where you are in your home-buying journey and what challenges you’re facing. Your answers help us guide you with the right insurance support and financial readiness strategies.

IN THIS ARTICLE

- 5 Essential Insurance Steps Every Canadian Should Take Before Buying a Home

- Understanding Financial Readiness Before Buying A Home

- Reviewing Income Stability And Long-Term Planning

- Estimating Borrowing Capacity And Budget Management

- Step 1: Prepare For Your Down Payment With Proper Insurance Planning

- Why Insurance Matters Before You Pay The Down Payment

- How Term Life Insurance Protects Your Down Payment

- Step 2: Explore Mortgage Options And Protect Yourself With The Right Coverage

- Comparing Mortgage Products In Canada

- Insurance You Need While Exploring Mortgage Options

- Step 3: Insurance Protection During The Buying Process

- Understanding Risk While Buying A House

- Home Insurance And Additional Coverage During The Buying Stage

- Step 4: Covering Your Bases Before Closing Costs Arrive

- Insurance You Need Before Paying Your Final Closing Amount

- Step 5: Prepare Insurance For The Closing Day And Move-In Stage

- Insurance You Must Have Active On Closing Day

- What Happens After Move-In (Insurance Checklist)

- Bonus Step: Estate Planning For Homeowners

- Final Thoughts For First-Time Buyers

- Conclusion — Making Your Home A Wise Investment

Sign-in to CanadianLIC

Verify OTP