- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

10 Things You Didn’t Know Life Insurance Could Do

By Harpreet Puri

CEO & Founder

- 12 min read

- May 7th, 2026

SUMMARY

Life Insurance in Canada goes far beyond basic protection. The discussion covers how a Money Back Life Insurance Policy in Canada, Whole Life Insurance, and Term Insurance with Money Back Policy options can support income planning, cash value growth, retirement income, long-term care needs, and family security, while explaining benefits, coverage, premiums, and payout structures that many Canadians overlook.

Introduction

Why Life Insurance In Canada Is No Longer Just About Death

For decades, Life Insurance in Canada had been sold as a single-purpose product: one that is given out when a person dies. That view is outdated. Nowadays, Canadians are using Life Insurance as an extension of the wider financial plan supporting income planning, retirement, savings, and even long-term care.

Statistics given by CLHIA show that more than 22 million Canadians have some form of Life Insurance policy, and Permanent Life Insurance has been continually growing over the previous decade. Meanwhile, according to the report of Statistics Canada, household debt and retirement shortages continue to be a concern among families throughout the country.

In our daily advisory work, we observe one regular trend, which is that the vast majority of people possess Life Insurance, but very few know what it can possibly do. Failure to be knowledgeable of that will, in most cases, result in missed opportunities- particularly with such products as a Money Back Life Insurance Policy in Canada, Whole Life Insurance, or Term Insurance with Money Back Policy options.

Here are ten things that most Canadians do not know Life Insurance can actually do.

1. Life Insurance Policy Can Do More Than Protect Loved Ones

A Life Insurance Policy is one of the items that are commonly taken as a checkbox- buy coverage, file it, and forget. As a matter of fact, a structured Life Insurance scheme may serve various functions in the financial arrangements of a household.

Life Insurance in Canada is categorized into two broad categories, which are Term Life Insurance and Permanent Life Insurance. Term Life Insurance is aimed at temporary requirements, which normally come at low premiums in the initial years. Permanent Life Insurance, in contrast, offers lifelong cover and may include savings-like functions.

A Permanent Life Insurance Policy can be used to meet financial obligations when it is well structured.s, help with future planning, and even provide access to money during your lifetime.

2. The Death Benefit Isn’t Always The Only Benefit

The most popular aspect of Life Insurance is the death benefit, but this is not the only aspect. No, the death benefits of the Life Insurance are paid in terms of a lump sum to the beneficiaries, and yes, the amount of the lump sum may be used to replace income or pay off debts. However, there are numerous layers of value added to many policies.

There are policies whereby partial access to funds during the life of the insured can be granted without affecting beneficiaries, as is expected by the majority of people. Others enable the death benefit to be arranged so that it can be used in the case of estate planning or business succession.

Our services are to assist families in planning death benefit designs according to both short-term and long-term planning objectives.

3. Insurance Coverage Can Extend Into Your Lifetime

Insurance coverage does not necessarily wait until something occurs. In the case of a permanent policy, though not yet dead, the coverage can provide you with living benefits.

Such benefits can be used to cover their medical expenses, unexpected health issues, or lifestyle changes in the later days of life. Permanent policies mean that one is constructed based on lifelong coverage as opposed to term policies, which expire after a specified time as situations change.

This kind of insurance cover is flexible to the clients who are concerned with stability and long-term planning, not to mention the fact that many Canadians do not have such flexibility.

4. A Life Insurance Plan Can Build Cash Over Time

Among the least considered permanent insurance features is that it accumulates cash value. This money will grow within the policy in a tax-favoured manner and may prove to be an asset to be accessed.

With a long-term horizon, the policyholders will be able to accumulate cash, which will work like a savings account without necessarily being linked to the financial fluctuations of the market. The cash value is contained within the policy as an internal account, which is accessible under specific terms.

We tend to describe this as a gradual-but-steady method of accumulating funds, less glitzy than investments, but very sure.

5. Life Insurance Pays While You’re Still Alive

Some of the misconceptions are that Life Insurance is payable only in death. Most policies, in fact, permit the availability of money in terms of a loan or withdrawal as long as the policyholder is alive.

In a case where premiums are collected over time, certain policies enable policyholders to borrow on their cash value. One can use these funds in case of emergency, school fees, or large-scale purchases.

This is where the Money Back Life Insurance advantages usually come as a surprise. With the proper design, the value of premiums paid can be refunded well before the policy maturity.

6. Living Benefits Can Support Retirement Income

With the increased complexity of retirement planning, a great number of Canadians are seeking an alternative to conventional savings. The Permanent Life Insurance may serve as additional retirement income.

Since withdrawals or loaning of some of these policies may not be considered as taxable income, they can be synchronized with the RRSPs, TFSAs, and other investments. This can assist the retirees in better managing their taxes and have access to money.

This strategy is most effective in our experience as an advisor when initiated early and planned deliberately, not as an emergency measure.

7. Life Insurance Can Help Even If Health Isn’t Perfect

Health is one of the reasons why many Canadians put off Life Insurance because they believe they will not qualify or they cannot afford to pay the premium. It is not necessarily the case.

Although part of the underwriting process, medical history and health records are not always used to show that a health issue will lead to denial. There are those policies that demand a medical examination and other policies that depend on underwriting, which is simplified underwriting.

Persons with health issues or risky activities can also be covered, but on different terms and costs. The trick is to know what to do so as not to disqualify oneself.

8. Good Health Can Lock In Lower Premiums For Life

Timing matters. Getting insurance during good health results in reduced premiums, and these premiums do not change over decades.

With the shift in health, the premiums tend to shoot up, and so do the permanent policies. There are fewer choices in later life, but by paying higher premiums, the choices remain viable in early life because premiums can be maintained and controlled.

We have often seen clients succeed by doing something sooner and not waiting until a better time occurs, which does not.

9. Payout Amounts Can Help Cover Final And Long-Term Costs

Life Insurance income can actually exceed income. It may be utilized to finalize expenses, cover estate taxes, or provide long-term care.

Most families do not estimate the cost of end-of-life care and funeral costs, as well as settlement fees. Life Insurance may assist in making sure these expenses are not borne by those they love through an already challenging period.

Good financial capability of a well-known insurer also comes into play, and it ensures that the coverage will take off when it is most needed.

10. Most People Underestimate What Life Insurance Can Replace

The role of Life Insurance is wider, and most people believe that this is to replace income as opposed to protection. It has the ability to assist in continuing lifestyle, furthering and sustaining family objectives as well as guarding the loved ones through the shifts, such as switching of occupations.

Life can also serve as a means of saving or financing an education or as a backup fund that can be used in times of need. The pliability exists–only that most folks are unacquainted with the proper utilization of it.

First Two Years Matter More Than You Think

The initial 2 years of a Life Insurance policy are very crucial. This time has been characterized by contestability clauses and stipulated policy omissions as requirements in the small print.

Knowing what occurs in these first years makes you well-informed, and you will not be caught unaware. It should be transparent in its application process, and particularly on personal information.

This is an important step that we lay stress on with each client to maintain long-term stability in the policies.

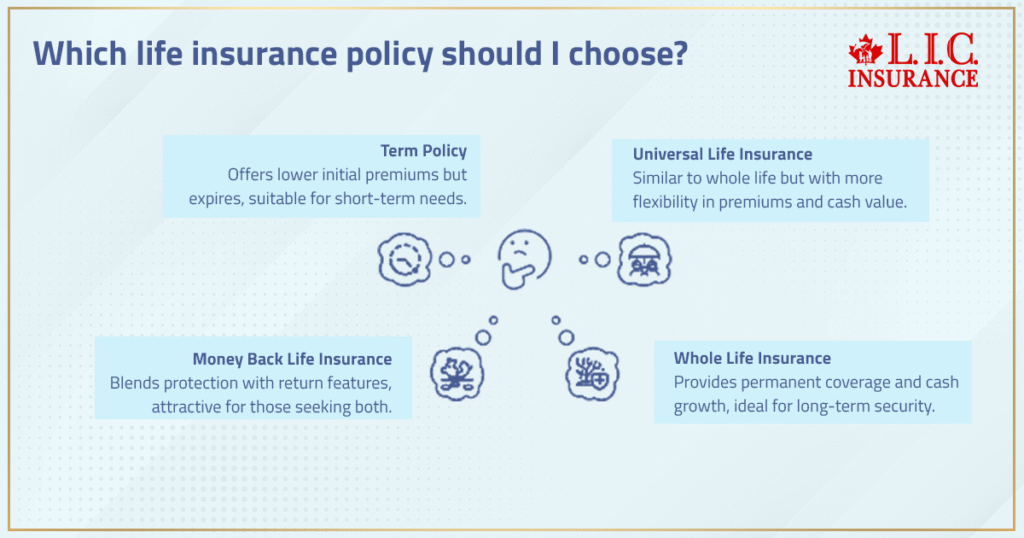

Comparing Term, Money Back, And Whole Life Insurance

When comparing options, Canadians often look at price alone. That’s a mistake.

- Term Policy options offer lower premiums initially but expire.

- Money Back Life Insurance blends protection with return features.

- Whole Life Insurance and Universal Life provide permanent coverage and cash growth.

Each option serves different goals. A Money Back Life Insurance quote online might look attractive, but suitability depends on income, goals, and time horizon.

Key Takeaways For Canadians Planning Long-Term Security

The biggest lesson is straightforward: Life Insurance is not a product with no dimensions.

The majority of the policies are much more adaptable than individuals think they are. The selection of the appropriate insurer, knowledge of the coverage details, and matching policies with the long-term objectives are very different.

Our mandate is to make sure that clients are safe, educated, and placed to utilize Life Insurance as a financial tool and not a payout in the case of an emergency.

The best thing about Life Insurance is that it should be grasped and not hurried.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Yes. A money-back life policy in Canada can be used to supplement registered savings and not to replace them. It is most effective when it is a constant stratum in a more comprehensive strategy. It is used by many Canadians to maintain the insurance cover at the expense of risk balancing. The issue of coordination is more important than product choice.

The quote for a Money Back Life Insurance online displays the price and not the suitability. It does not include the behaviour of long-term cash values, flexibility of premium payments, and benefit organization of the insurer. Quations are a point of departure and not a decision-making tool. Planning must be contextualized.

Money Back Policy Term Insurance can be used to fund set time horizons as long as it is set up the right way. It is commonly applied in cases where financial commitments have a time limit. The trick is setting the premiums paid on the milestones anticipated. It is not simplistic because of its short-term nature.

Whole Life Insurance may require higher premiums in the beginning, but this is not all. Premiums remain constant, and coverage and cash value are increased. In the long run, this stability can balance initial expenses. Value is determined by time, but not necessarily cost.

Yes, there are some permanent policies that permit access to funds without an immediate increment in taxable income. This is capable of coordinating the retirement income and other sources. Form and time are of vital importance. It does not happen, but it is possible.

A change in the health records can typically have no impact on the preexisting coverage upon approval. That is the reason qualifying to be in good health is important. The future medical issues will not change premiums and death benefits. Timing defends the long-term security.

Life Insurance plans that are owned individually have no connection with employment. A change in employment does not count regarding coverage or beneficiaries. This consistency is useful during periods of fluctuation in income. It is the policy that builds stability, not your employer.

Underwriting is not conducted after medical history and high-risk activities are evaluated by underwriters. The companies determine different criteria. This impacts premium payments and policy exclusion. It is equally important to match the insurer with the right one as it is to qualify.

Long-term care needs are backed up by some permanent policies. These advantages do not substitute dedicated coverage, but may relieve the savings pressure. Early planning enhances flexibility. Waiting limits options.

The majority of the population is interested in short-term expenses rather than the effects of long-term coverage. The replacement of income is not the entirety of the equation. Final expenses, family needs, and future obligations are underestimated. Proper planning bridges that inefficiency.

Sources and Further Reading

Life Insurance Basics & Types (Term vs Permanent)

- Term Life Insurance Explained — Sun Life Canada

https://www.sunlife.ca/en/insurance/life/term-life-insurance/

— Covers how term Life Insurance pays a death benefit and how coverage works. Sun Life - Term vs Permanent Life Insurance — Canada Life

https://www.canadalife.com/insurance/life-insurance/term-life-insurance/term-vs-permanent-life-insurance.html

— Compares term and permanent coverage features, including cash value. Canada Life

Permanent & Whole Life Insurance (Cash Value & Living Benefits)

- Permanent Life Insurance — Canada Life

https://www.canadalife.com/insurance/life-insurance/permanent-life-insurance.html

— Describes whole and universal life, lifelong coverage, and cash value access. Canada Life - Whole Life Insurance — Sun Life Canada

https://www.sunlife.ca/en/insurance/life/permanent-life-insurance/whole/

— Explains whole life cash value and how funds can be accessed during life. Sun Life - Universal Life Insurance — Canada Life

https://www.canadalife.com/insurance/life-insurance/permanent-life-insurance/universal-life-insurance.html

— Discusses flexible permanent coverage and cash value. Canada Life - What Is Cash Value In Life Insurance — Sun Life Canada

https://www.sunlife.ca/en/tools-and-resources/money-and-finances/understanding-life-insurance/cash-value-in-life-insurance-how-does-it-work/

— Clarifies how cash value grows inside a policy. Sun Life

Death Benefit & Tax Treatment

- Death Benefits & Taxation — Canada Revenue Agency (CRA)

https://www.canada.ca/en/revenue-agency/services/tax/individuals/life-events/doing-taxes-someone-died/prepare-returns/report-income/death-benefits.html

— Government page explaining how death benefits are treated for tax purposes.

Key Takeaways

- Life Insurance in Canada is no longer just about a payout after death. When structured properly, it can support cash value growth, retirement income, and long-term financial stability for families.

- A Money Back Life Insurance Policy in Canada and Whole Life Insurance offer more flexibility than most people expect, especially for those balancing protection with disciplined savings.

- Term Life Insurance works well for time-bound needs, but Permanent Life Insurance policies are often better suited for lifelong coverage, estate planning, and predictable premium payments.

- Cash value inside permanent policies can become a usable financial resource, helping policyholders manage expenses, opportunities, or income gaps later in life.

- The death benefit remains central, but understanding how Life Insurance pays during life through living benefits changes how coverage is viewed and used.

- Health, timing, and policy structure matter more than age alone. Securing coverage in good health often leads to lower premiums that stay stable over time.

- Many Canadians underestimate how Life Insurance can protect loved ones, cover final expenses, support retirement goals, and reduce pressure on other savings.

- The most effective Life Insurance plans are built intentionally, aligned with financial obligations today and future needs, rather than chosen solely on price or online quotes.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- 10 Things You Didn't Know Life Insurance Could Do

- 1. Life Insurance Policy Can Do More Than Protect Loved Ones

- 2. The Death Benefit Isn’t Always The Only Benefit

- 3. Insurance Coverage Can Extend Into Your Lifetime

- 4. A Life Insurance Plan Can Build Cash Over Time

- 5. Life Insurance Pays While You’re Still Alive

- 6. Living Benefits Can Support Retirement Income

- 7. Life Insurance Can Help Even If Health Isn’t Perfect

- 8. Good Health Can Lock In Lower Premiums For Life

- 9. Payout Amounts Can Help Cover Final And Long-Term Costs

- 10. Most People Underestimate What Life Insurance Can Replace

- First Two Years Matter More Than You Think

- Comparing Term, Money Back, And Whole Life Insurance

- Key Takeaways For Canadians Planning Long-Term Security

Sign-in to CanadianLIC

Verify OTP