- Connect with our licensed Canadian insurance advisors

- Schedule a Call

Basics

Reviews

Common Inquiries

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What Is the Maturity Period of Term Insurance?

- What Is the Maturity Period in Term Life Insurance Policy?

- Why Understanding the Maturity Period Matters

- Common Struggles with the Maturity Period

- Options When Your Term Life Insurance Reaches Maturity

- Choosing the Right Term Length for Your Needs

- Planning Ahead: When Should You Start Thinking About the Maturity Period?

- The Role of Term Life Insurance Brokers

- Addressing Health Changes and Term Insurance Maturity

- When Should You Consider Conversion?

- Keeping Coverage Affordable

- Planning for the End of Your Term: What's Next?

- Take Action Today with Canadian LIC – The Best Insurance Brokerage

What Is the Maturity Period of Term Insurance?

By Pushpinder Puri

CEO & Founder

- 11 min read

- October 9th, 2024

SUMMARY

The blog explains the maturity period of term life insurance, addressing common concerns about how long coverage lasts and what happens when it ends. It discusses policy renewal, conversion to permanent insurance, and purchasing a new term policy as available options. The importance of planning ahead—ideally five years before the policy matures—is emphasized to avoid high renewal costs. The blog also highlights the role of brokers in navigating options and how health changes impact term life insurance quotes online.

introduction

The major confusion regarding the terminology of life insurance policy arises regarding the maturity period. Most of the clients ask Canadian LIC about how long their Term Insurance would last, what happens when it reaches its maturity period, and if it would be extended or not. All this uncertainty creates an element of fear in the minds of such people considering securing their family’s future. The good news is that once the maturity period is determined, the selection process for Term Life Insurance becomes somewhat easy.

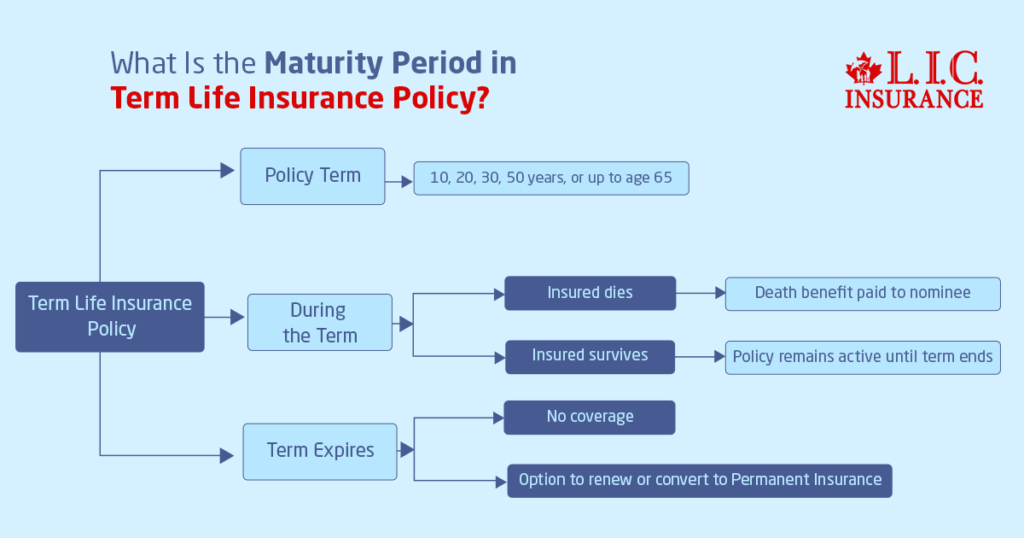

What Is the Maturity Period in Term Life Insurance Policy?

It is the time duration for which the Term Life Insurance Plan will continue to remain active. In simple terms, it refers to the length of time when the policy will give protection. In Canada, the policy can be availed in terms of years, which can be 10, 20, 30 or 50 years or until a certain age, such as up to 65. In case the insured dies during the term, and the life insurance company pays the death benefit to the nominee. In case the term expires and the insured person dies, no maturity benefit is paid to him/her, and no coverage is given unless he/she renews or changes over to a Permanent Insurance Policy.

This is rather hard to understand since not everyone plans ahead for what happens once the term of their insurance is up. Most of the clients who share stories of buying Term Insurance when very young owe it to this thinking that they will always have it, and later in life, find out that they need to extend or renew the policy. Addressing these concerns early on helps prevent financial stress later in life.

Why Understanding the Maturity Period Matters

Therefore, in the case of taking a Term Life Insurance Plan, it is very crucial to know how long the term is because that relates to long-term planning. People usually get confused that they will be able to renew the policy at the same rate at the time of maturity of the initial term. According to several Term Life Insurance Brokers, the cost can be very high as age increases. This is more so the case if an individual has health problems in the initial term. It may thus change the Term Life Insurance Quotes Online.

Suppose you purchased a 20-year term life plan when you were 30 years old. When the policy matures at age 50, your insurance needs may have changed entirely. You may have paid off your mortgage, while children may be self-sufficient and financially healthy. Conversely, you may need coverage if you are nearing retirement or want to leave behind a legacy. In such circumstances, one can refresh the term of coverage, convert it to a Permanent Coverage, or pursue some other form of coverage.

Common Struggles with the Maturity Period

Many clients complain when they realize that their Term Life Insurance does not automatically renew under the same terms. People often come too late, realizing that the policy has matured without protection. For example, one client brought up a case where he could not renew coverage for 20 years after completion when just about retiring. He found that the new premiums were much higher and that his age had added complications to the whole process, partly because of a fresh health condition.

This is a far too common tale: people tend to wait until nearly the end of a Term Insurance product’s life before planning for it. If you wait till your policy is near maturity to begin looking at your options, that could put you behind the eight ball, especially in case your health has altered in the interim. Canadian LIC Term Life Insurance Brokers typically suggest that clients begin evaluating their options about five years prior to the policy’s near maturity.

Options When Your Term Life Insurance Reaches Maturity

When a Term Life Insurance policy reaches its maturity period, there are several options to consider:

Renewing the Policy:

One of the most straightforward options is to renew the existing policy. However, it’s essential to be aware that the premiums will increase, sometimes dramatically, based on your age and health. Renewing may be ideal if you still need coverage for a short period and are not ready to switch to a different plan.

Converting to a Permanent Life Insurance Policy:

Many Term Life Insurance Plans in Canada offer a conversion option. This allows you to switch your term policy to a permanent one without undergoing a new medical exam. While the premiums will be higher than your original term rates, converting can provide lifelong coverage and even accumulate cash value over time. Clients at Canadian LIC often find this to be a worthwhile option, especially if they want coverage to last indefinitely or use the policy for estate planning.

- Purchasing a New Term Policy:

If you are in relatively good health and want a fresh start, you may opt to buy a new Term Life Insurance Plan. By comparing Term Life Insurance Quotes Online, you can find a new policy that meets your budget and coverage needs. While starting a new term plan may be more expensive than your previous rates, it can still be more affordable than renewing an existing one if you are young and healthy enough.

- Letting the Policy Expire:

In some cases, you may no longer need life insurance coverage once your term ends. If your financial obligations are fulfilled, such as paying off debts and ensuring that your family is financially secure, allowing the policy to lapse might be the right choice for you.

Choosing the Right Term Length for Your Needs

The length of the maturity period should align with your financial responsibilities and life goals. Here’s a closer look at how different term lengths can fit various needs:

- 10-Year Term: Ideal for temporary needs, such as covering a short-term debt or providing security while your children finish college. Clients who approach Canadian LIC often opt for 10-year term policies to cover a gap until their retirement savings kick in.

- 20-Year Term: Commonly selected by families with young children who want to ensure financial protection while their kids grow up. This term length is often enough to cover major life expenses like education and mortgage payments.

- 30-Year Term: Best suited for individuals who are seeking long-term security, such as protecting their family for the majority of their working years. Many people who are in their 20s and 30s choose a 30-year term to lock in lower premiums for a longer duration.

Planning Ahead: When Should You Start Thinking About the Maturity Period?

It is essential to start considering your alternatives at least five years before when your Term Life Insurance ends. At this time, you will be able to assess your financial status, look for different Term Life Insurance quotes on the web, and even seek opinions from Term Life Insurance Brokers on the potential conversion or renewal options. Waiting until the last minute will significantly limit your alternatives, primarily if your health status has changed.

Canadian LIC often encounters clients who wish they had started planning earlier. Those who plan ahead of time can secure coverage at more affordable rates and avoid last-minute surprises. Early planning also gives you adequate time to compare various plans and determine whether it makes more sense to renew, convert, or purchase a new policy altogether.

The Role of Term Life Insurance Brokers

Brokers play an important role in helping you overcome the intricacies of Term Life Insurance. Canadian LIC Term Life Insurance Brokers work with clients, setting targets to review previous policies, assess future needs, and work out suitable options. With many insurance products available, Term Life Insurance Brokers can help you find and compare Term Life Insurance Quotes Online and ascertain the right coverage for you.

Many clients share stories of how brokers helped them understand the implications of letting a policy mature without renewing or converting. The personalized advice provided by brokers ensures you’re making informed choices about your coverage and financial future.

Addressing Health Changes and Term Insurance Maturity

Illnesses that develop over time may be too problematic to refinance or acquire a new Term Life Insurance policy. An example of this is when one client was diagnosed with diabetes just when their policy was about to mature. Their term life broker from Canadian LIC advised them on alternative plans that did not require a medical exam and options for conversion. Changes in health do have implications on your Term Life Insurance Quotes Online, but working with someone who would understand the situation is usually what does the trick.

When Should You Consider Conversion?

Converting your Term Life Insurance Plan to a permanent policy can be an ideal choice if you want lifelong coverage. It is an excellent option, especially when you get lifetime coverage. For instance, if perhaps you are getting close to retirement and wish to put security for your family, you may end up realizing that this is the best. In some cases, health issues are what disqualify you from qualifying for a new Term Life Insurance Plan, thus making this the best choice. Most of the customers of a Canadian LIC opt for conversion during important life events, for example, retirement or when they become grandparents.

Keeping Coverage Affordable

Most people concern themselves with the cost when considering renewal, conversion, or purchasing a new term policy. One of the easiest ways to discover competitive policies that fit your budget, therefore, is through comparison shopping for Term Life Insurance Quotes Online. Many Canadian LIC Term Life Insurance Brokers recommend their clients to consider options where death benefits are smaller should that be a concern of theirs. Another way of keeping premiums affordable is by reducing your term coverage.

Planning for the End of Your Term: What's Next?

When planning for the maturity period, take time to evaluate your evolving needs. Consider questions like:

- Do I still have outstanding debts, such as a mortgage, that need coverage?

- Are my children financially independent, or will they still require support?

- Am I nearing retirement, and how will my life insurance plan fit into my overall financial strategy?

Take Action Today with Canadian LIC – The Best Insurance Brokerage

The maturity of Term Life Insurance need not be a daunting experience, especially if you plan ahead and seek the assistance of experienced Term Life Insurance Brokers. Be guided now by us at Canadian LIC through your transition, which will ensure continued protection and peace of mind for you and your loved ones. Do not wait for the term to run out. Begin now for the best possible rate as well as the best coverage on your Term Insurance.

Determine Term Life Insurance Quotes Online or seek a Canadian LIC financial advisor so you’ll know how to get the most out of your Term Life Insurance. You will thank yourself for taking proactive steps today.

More on Term Life Insurance

- Can I Purchase a Joint Term Life Insurance Policy or a Whole Life Insurance Policy?

- Best Term Life Insurance Companies in Canada: In-Depth Reviews & Essential Insights (2024)

- Should Both Husband and Wife Get Term Life Insurance?

- What Is Underwriting in Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- At What Age Should You Stop Buying Term Life Insurance?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- How Do You Choose Term Insurance?

- What’s the Longest Term Life Insurance You Can Get?

- Do I Get Money Back from Term Life Insurance?

- Can You Cash Out a Term Life Insurance Policy?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 844-542-4678 to speak to our advisors.

Get Quote Now

Frequently Asked Questions About the Maturity Period of Term Insurance Plan in Canada

The maturity period refers to the length of time a Term Life Insurance Plan remains active. For example, a 20-year term policy will provide coverage for 20 years. If the policyholder passes away within this time, the insurance provider pays the death benefit to the beneficiary. After the maturity period ends, the policy expires unless it’s renewed, converted, or replaced with a new term.

Yes, you can renew your Term Insurance policies, but it will usually come with higher premiums. At Canadian LIC, clients often share their experiences of facing premium hikes after their original term expired. Renewal costs increase due to factors like age and health. It’s a good idea to explore renewal options with Term Life Insurance Brokers to find the most affordable choice for your situation.

When the Term Life Insurance Plan reaches maturity and is not renewed, the coverage ends. This means there will no longer be a death benefit payout if something happens to you. Many people are surprised to learn this when they come to Canadian LIC looking for options after their policy expires. Planning ahead helps avoid gaps in coverage.

Yes, most Term Life Insurance Plans in Canada offer a conversion option. This allows you to switch to a permanent policy without a new medical exam. At Canadian LIC, we often see clients take advantage of this option, especially if their health has changed during the term. Conversion ensures continuous coverage and can provide lifelong benefits.

Yes, if you wait until your Term Life Insurance Plan reaches maturity, your Term Life Insurance Quotes Online may be higher. Age and any new health conditions can increase the cost of a new policy. Clients who start exploring new coverage options early often find better rates, so it’s wise to plan ahead.

Term Life Insurance Brokers guide you through the process, whether you’re considering renewing, converting, or buying a new policy. At Canadian LIC, brokers frequently help clients compare options and find Term Life Insurance Quotes Online that fit their needs. Our brokers’ insights can make the transition smoother and help you make informed decisions.

The choice depends on your financial goals and responsibilities. A shorter term may be suitable for temporary needs, like covering a small debt, while a longer term may protect your family during the majority of your working years. Clients at Canadian LIC often share stories about choosing longer terms to cover big expenses like mortgages or to ensure their children’s future.

If your health has changed, converting your Term Life Insurance Plan to a permanent policy may be your best option. At Canadian LIC, we help many clients who have developed health conditions during their term find suitable coverage without needing a new medical exam. Exploring this option can help you maintain coverage at a manageable cost.

Some Term Life Insurance Plans allow you to extend coverage. However, this may involve higher premiums. Clients who work with Canadian LIC brokers often get personalized advice on whether extending their policy is the best choice or if a new term would be more affordable. It’s helpful to discuss these options with Term Life Insurance Brokers to find the right solution.

If your financial responsibilities have decreased, you may choose to let the policy expire. Many clients at Canadian LIC decide this when they have paid off debts or their children are financially independent. However, it’s crucial to assess your situation carefully, as your needs may still warrant some form of coverage for other reasons, such as leaving a legacy.

It’s advisable to start planning at least five years before the maturity period. This gives you enough time to explore Term Life Insurance Quotes Online, consider conversion options, or purchase a new policy if needed. Clients who begin planning early with Canadian LIC often find better deals and avoid last-minute stress.

Yes, converting your Term Life Insurance Plan to a permanent policy typically results in higher premiums than the original term policy. However, the advantage is that you won’t need a new medical exam, and the coverage will last for your entire life. Canadian LIC’s Term Life Insurance Brokers often help clients find a balance between coverage and cost when considering this option.

Yes, you can switch to a new Term Life Insurance Plan from a different insurer. Comparing Term Life Insurance Quotes Online will help you find a plan that suits your needs and budget. Canadian LIC’s clients often explore different options through our brokers, who provide access to a variety of insurers to ensure the best match.

While the maturity period itself does not directly affect eligibility, factors such as age and health at the time of renewal do. As Term Life Insurance Brokers often advise, renewing at an older age may involve higher costs and possible medical requirements. Starting the renewal process early can give you more flexibility.

When renewing a Term Life Insurance Plan, your premiums may increase based on your age, health changes, and the length of the new term. Canadian LIC helps clients find affordable options by comparing Term Life Insurance Quotes Online, even when these factors come into play.

FAQs on the Maturity Period of Term Life Insurance in Canada give you helpful insights based on the real-life experiences of clients. Plan ahead and consult with the Term Life Insurance Brokers of Canadian LIC for confident decisions that keep your coverage secure.

Sources and Further Reading

- Canadian Life and Health Insurance Association (CLHIA) – Provides information on various types of life insurance plans available in Canada, including Term Life Insurance.

CLHIA Website - Government of Canada – Life Insurance Guide – Offers an overview of life insurance options, including Term Insurance and renewal options.

Government of Canada: Life Insurance - Insurance Bureau of Canada (IBC) – Discusses the different types of insurance policies and advice on choosing the right term length.

Insurance Bureau of Canada - Canadian LIC Blog – Regularly updated with real-life stories and advice on selecting Term Life Insurance, converting policies, and planning for maturity.

Canadian LIC Blog - Financial Consumer Agency of Canada – Provides tips on managing life insurance policies, including the pros and cons of renewing versus converting.

Financial Consumer Agency of Canada - Manulife Canada – Term Life Insurance – A resource for understanding Term Life Insurance Quotes Online, coverage options, and renewal processes.

Manulife Canada - Sun Life Financial – Life Insurance Options – Offers insights into Term Life Insurance Brokers, policies, and choosing the appropriate term length.

Sun Life Financial - TD Insurance – Understanding Term Life Insurance – Discusses different Term Life Insurance Plans and factors affecting premiums.

TD Insurance

These resources provide additional guidance on Term Life Insurance Plans, renewal options, and industry insights in Canada.

Key Takeaways

- Maturity Period Explained: The maturity period of a Term Life Insurance Plan is the duration the policy provides coverage, commonly set for 10, 20, or 30 years.

- Options at Maturity: When the policy reaches maturity, you can renew, convert to a permanent policy, buy a new term, or let it expire depending on your needs.

- Renewal Costs May Rise: Premiums typically increase when renewing a Term Life Insurance Plan due to age and potential health changes.

- Early Planning Is Crucial: Start evaluating your options at least five years before the policy matures to avoid last-minute surprises and secure better rates.

- Conversion Can Be Beneficial: Converting to a permanent policy without a medical exam is an option if continuous coverage is needed, especially when health has changed.

- Consult Term Life Insurance Brokers: Working with brokers can help you find the most suitable plan, compare Term Life Insurance Quotes Online, and understand your choices.

- Tailor Coverage to Your Needs: Choose the term length based on financial responsibilities, such as mortgage payments or providing for dependents.

Your Feedback Is Very Important To Us

We value your insights and would like to understand your experiences related to the maturity period of Term Insurance in Canada. Your feedback will help us better address the challenges Canadians face. Please take a few minutes to answer the following questions.

Thank you for your time and valuable insights! Your feedback will help us address Canadians’ struggles and provide better solutions for Term Life Insurance.

IN THIS ARTICLE

- What Is the Maturity Period of Term Insurance?

- What Is the Maturity Period in Term Life Insurance Policy?

- Why Understanding the Maturity Period Matters

- Common Struggles with the Maturity Period

- Options When Your Term Life Insurance Reaches Maturity

- Choosing the Right Term Length for Your Needs

- Planning Ahead: When Should You Start Thinking About the Maturity Period?

- The Role of Term Life Insurance Brokers

- Addressing Health Changes and Term Insurance Maturity

- When Should You Consider Conversion?

- Keeping Coverage Affordable

- Planning for the End of Your Term: What's Next?

- Take Action Today with Canadian LIC – The Best Insurance Brokerage

Sign-in to CanadianLIC

Verify OTP