BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

What Is Guaranteed Universal Life Insurance In Canada?

By Pushpinder Puri

CEO & Founder

- 10 min read

- June 18, 2026

SUMMARY

Guaranteed Universal Life Insurance in Canada offers lifelong protection with a guaranteed death benefit and predictable premiums. Coverage details, costs, and benefits are compared with Whole Life Insurance and Term Insurance, along with Universal Life Insurance Policy options and cash value considerations. Insights from Canadian LIC highlight estate planning, financial security, and Long Term Life Insurance Plans in Canada for wealth preservation and legacy planning.

Introduction

As per the Canadian Life and Health Insurance Association (CLHIA), Canada has more than $5 trillion in Life Insurance Coverage, and a large percentage of this is in the form of permanent Life Insurance Policies for estate and wealth management strategies. Over the last ten years, we have seen a growing requirement for Long Term Life Insurance Policies in Canada, especially for those looking for coverage for their lifetime without having to invest in high-risk investment products.

Some of our common questions from clients include:

- What is a Universal Life Insurance Policy?

- How does Universal Life Insurance work?

- Is Guaranteed Universal Life Insurance worth it?

- How does it compare to other types of Life Insurance?

Guaranteed Universal Life Insurance, also referred to as GUL Insurance, is one type of insurance that has gained popularity among Canadians looking for coverage for their entire lives, along with fixed expenses and a guaranteed death benefit. Now, let’s break this down for you strategically.

What Is Guaranteed Universal Life Insurance And How Does It Work

The Guaranteed Universal Life Insurance Plan is a kind of permanent Life Insurance Plan that provides the insured with the benefit of a guaranteed death benefit for a specified period of time up to and including the ages of 100, 110, and even 121 years, as long as the premium payments are made.

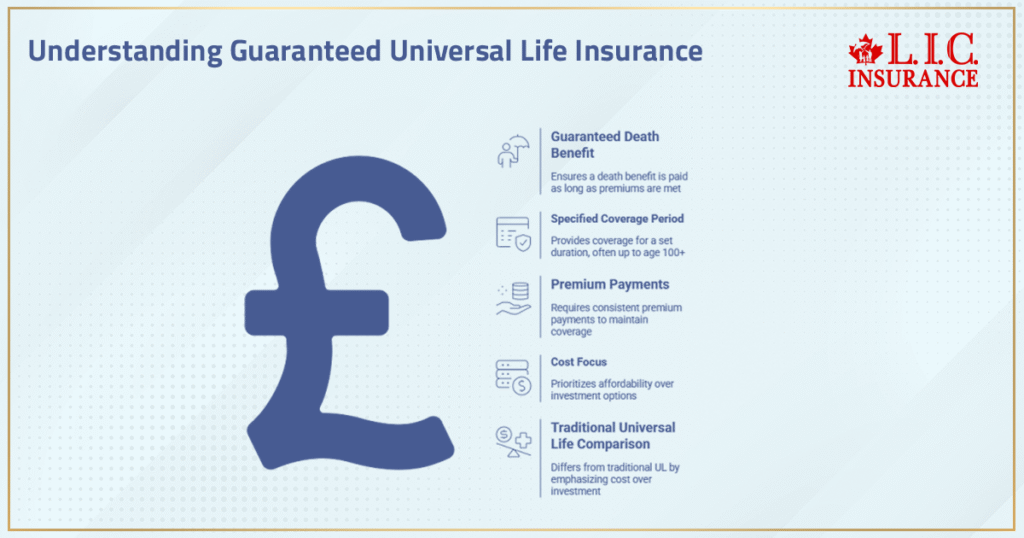

Unlike the Traditional Universal Life Insurance Plan, in which much importance is given to the investment options and cash value features of the insurance plan, in the case of the Guaranteed Universal Life Insurance Plan, much importance is given to the cost aspect.

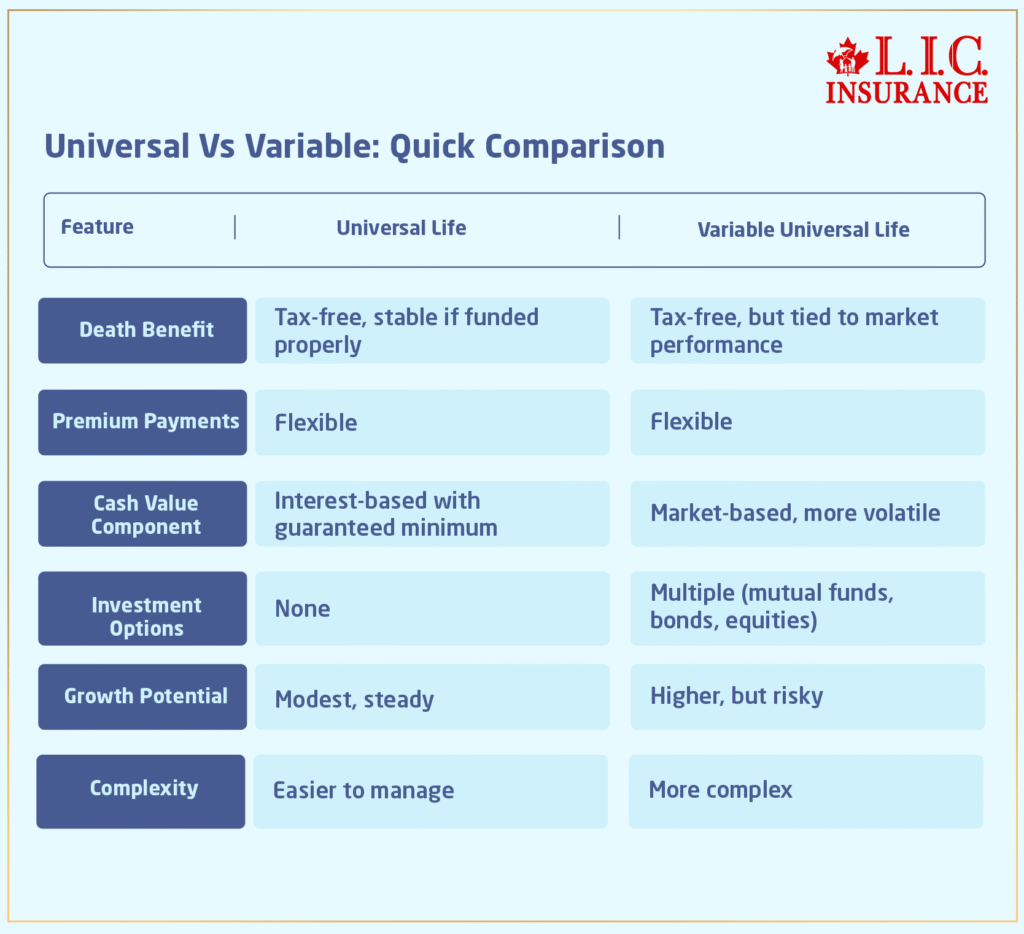

How Universal Life Insurance Works

To properly understand Guaranteed Universal Life Insurance, it helps to first understand how Universal Life Insurance works.

A typical Universal Life Insurance Policy contains:

- A death benefit

- A cash value component

- Flexible premium payments

- Investment components within an investment account

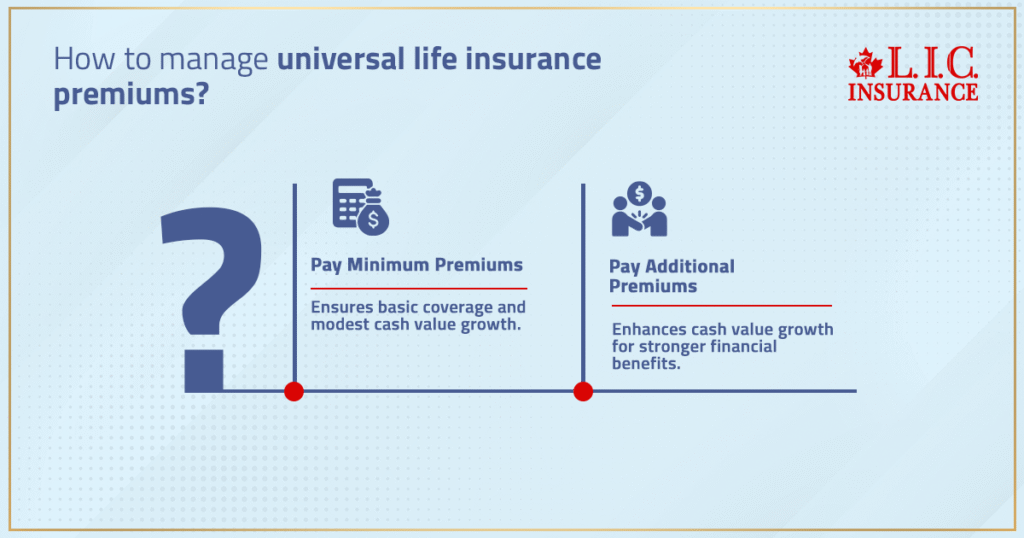

In Universal Life, a portion of your premium is used to pay for the cost of insurance, and the rest is invested. The results of this investment portfolio will dictate how much your cash value will grow.

In Guaranteed Universal Life, there is no reliance on investment savings elements, and it provides a guaranteed death benefit, provided that you have paid the minimum premium.

This makes Guaranteed Universal Life different from Indexed Universal and Variable Universal, which demand a more hands-on investment approach.

Key Features Of Guaranteed Universal Life Insurance

We are offering Guaranteed Universal Life Insurance Policies with a focus on simplicity and stability.

Guaranteed Death Benefit

The first and most important aspect of this insurance policy is the guarantee of the death benefit. As long as the premium is paid on time, the insurance policy guarantees the payment of the stipulated death benefit.

It is because of this guarantee that this insurance policy is best used for estate planning and final expenses planning.

Lifetime Coverage

The other important aspect of the insurance policy is the lifetime coverage provided by the policy. Guaranteed Universal Life Insurance Policies cover the policyholders up to the age of 121. This is important for the Canadian population because they are able to have insurance coverage for the rest of their lives without the cost of Whole Life Insurance.

Predictable Premium Structure

Unlike the Universal Life Insurance Policy, the Guaranteed Universal Life Insurance Policy has a fixed premium structure. A minimum premium has to be paid on the insurance policy in order to have the guarantee of the death benefit.

Medical Underwriting

Most policies require medical underwriting. Depending on the age and the amount of insurance to be covered, medical examinations may be necessary. Premiums are based on health records and risk classification.

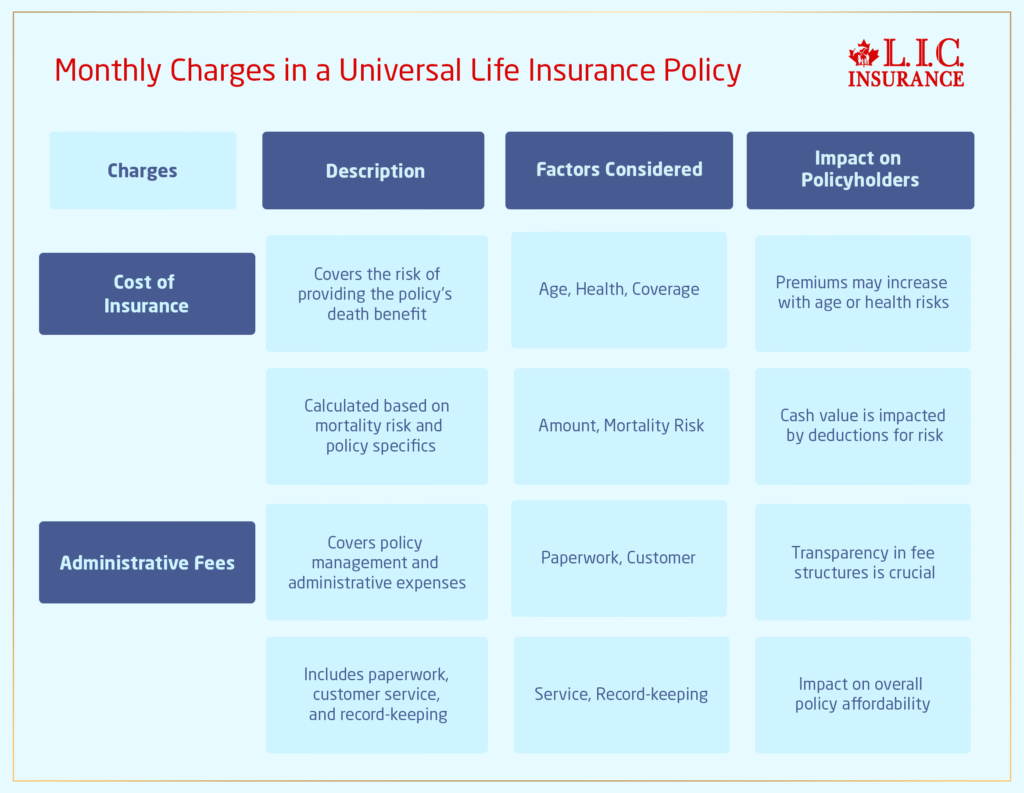

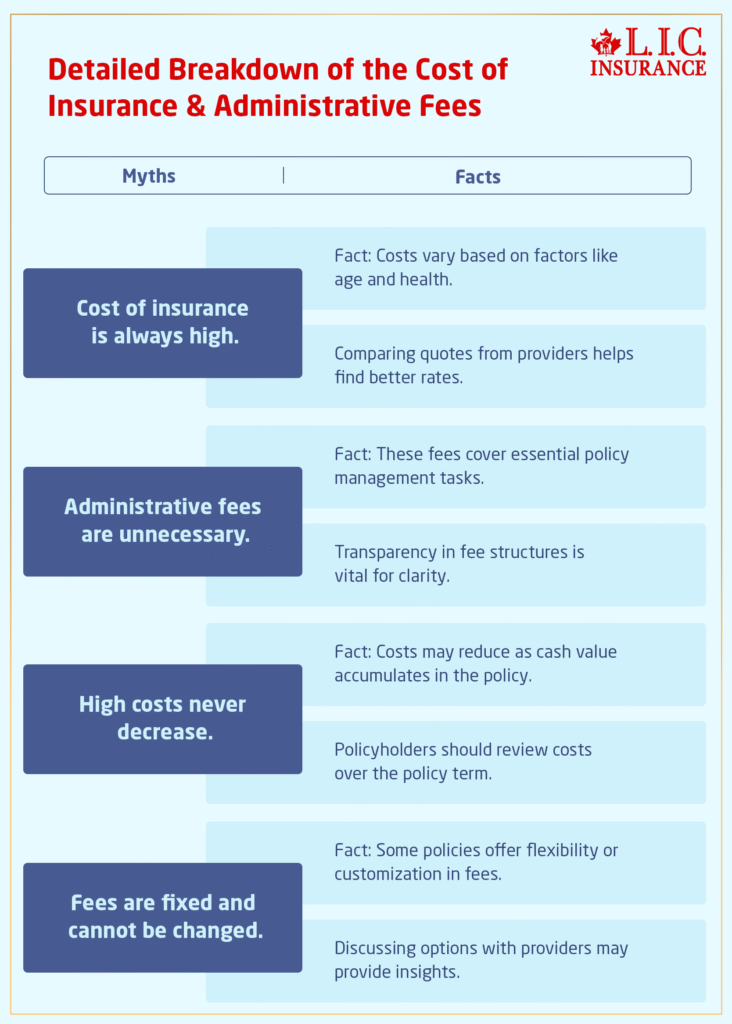

Administrative Fees And Insurance Cost

Similar to other Life Insurance Policies, Guaranteed Universal Life Insurance Policies have administrative fees and costs of insurance that are taken from the cash value.

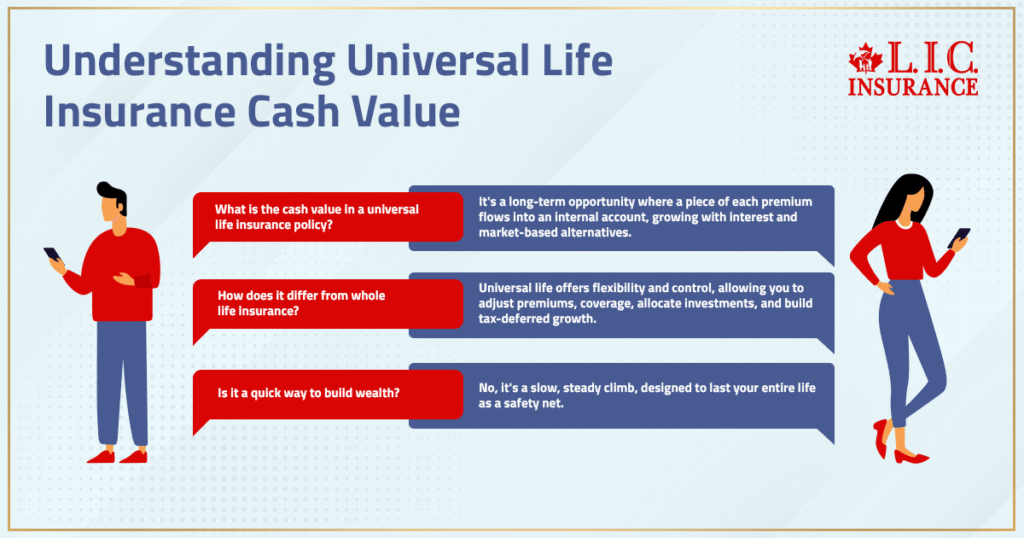

Cash Value And Cash Value Growth Explained

One of the biggest misconceptions about Guaranteed Universal Life Insurance revolves around its cash value component structure.

Cash Value Life Insurance Canada Context

In any Cash Value Life Insurance Canada conversation, clients may believe that all permanent Life Insurance products build substantial wealth. This, however, is not the focus of Guaranteed Universal Life Insurance when compared to Whole Life Insurance.

Cash Value Component Structure

Guaranteed Universal Life Insurance does have a cash value component. The focus of this component, however, is not to build wealth but to sustain the policy.

Cash Value Growth Expectations

The cash value growth in a Guaranteed Universal Life Insurance Policy is normally low. It can grow slowly, but does not emphasize high growth in investments.

If clients need high growth in investments, they can also consider Indexed Universal Life Insurance and Variable Universal Life Insurance.

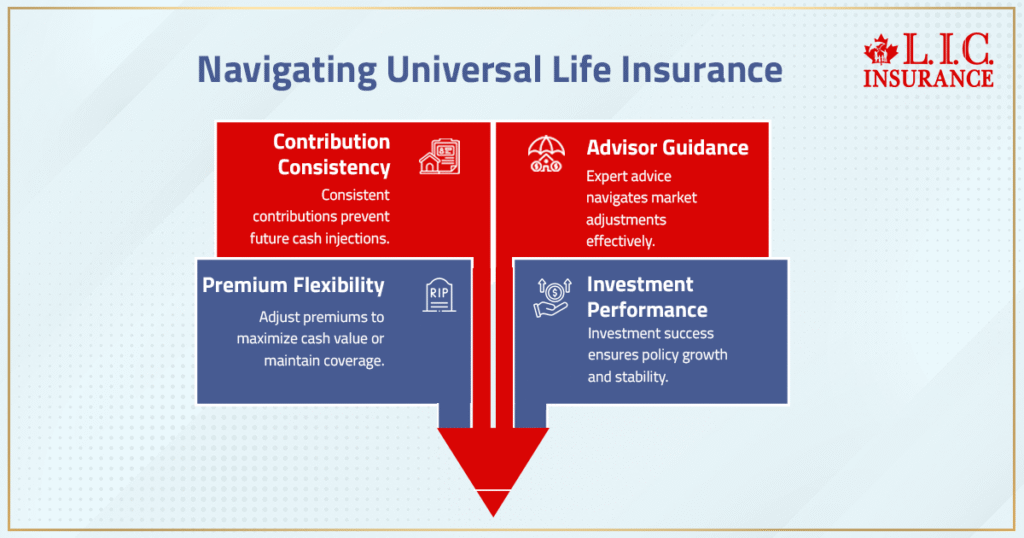

Policy Loans And Partial Withdrawal

It is also important to note that some Universal Life Insurance Policies can be used to make a loan from the cash value. However, if the client withdraws too much from the cash value, it can reduce the death benefit.

It is important to ensure that there is cash value remaining in the insurance policy to ensure lifetime protection.

Cash Surrender Value And Market Value Adjustments

If the client decides to cancel the insurance policy, they can be entitled to the cash surrender value.

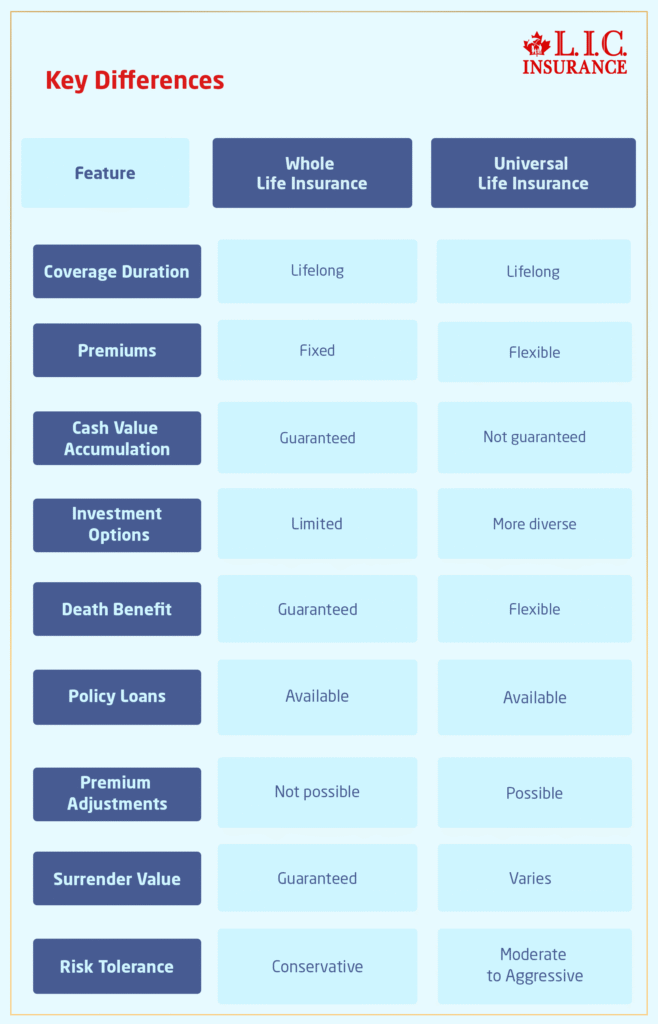

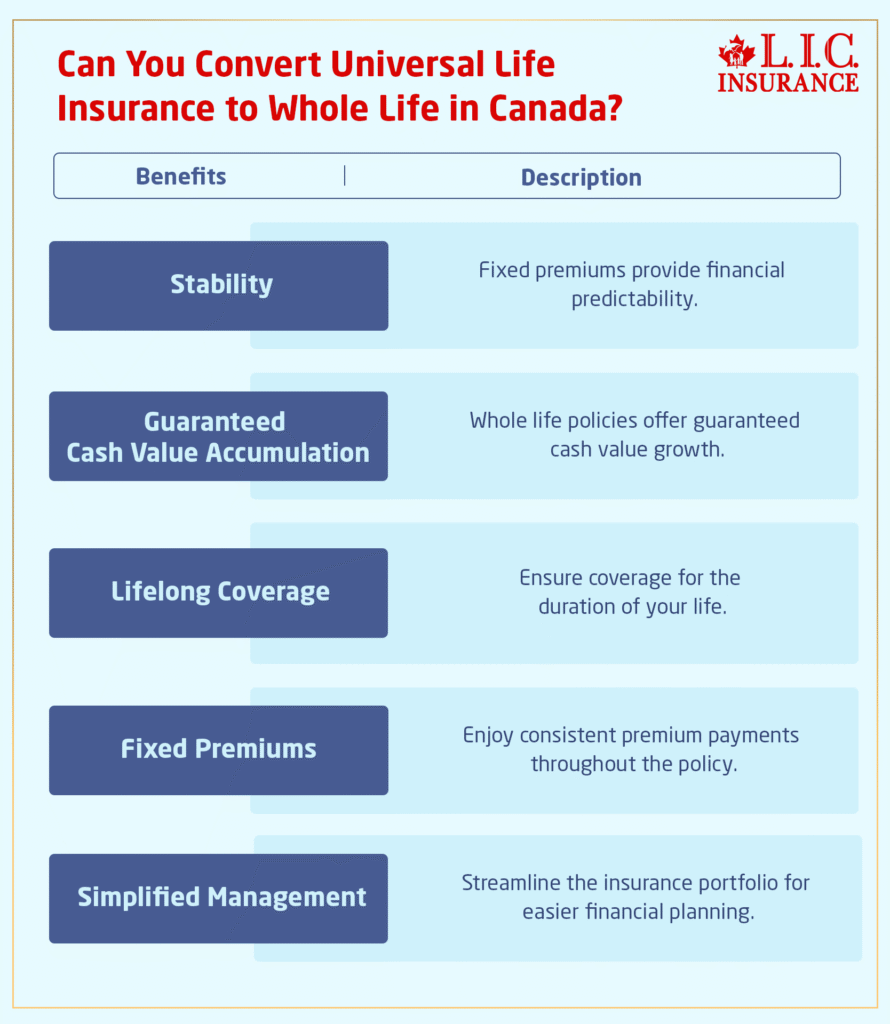

Guaranteed Universal Life Insurance Vs Whole Life Insurance

Many clients ask us about Universal Life Insurance vs Whole Life Insurance.

Whole Life Insurance:

- Builds stronger cash value accumulation

- Often includes dividend potential

- Offers entire life coverage

- Generally has higher premiums

Guaranteed Universal Life:

- Offers lower insurance cost than whole life

- Prioritizes guaranteed death benefit

- Has minimal investment savings elements

- Maintains lifetime coverage

Whole Life is often chosen by clients who want stronger wealth-building tools. Guaranteed Universal Life is selected by clients focused primarily on stable lifelong protection.

Guaranteed Universal Life Insurance Vs Term Life Insurance

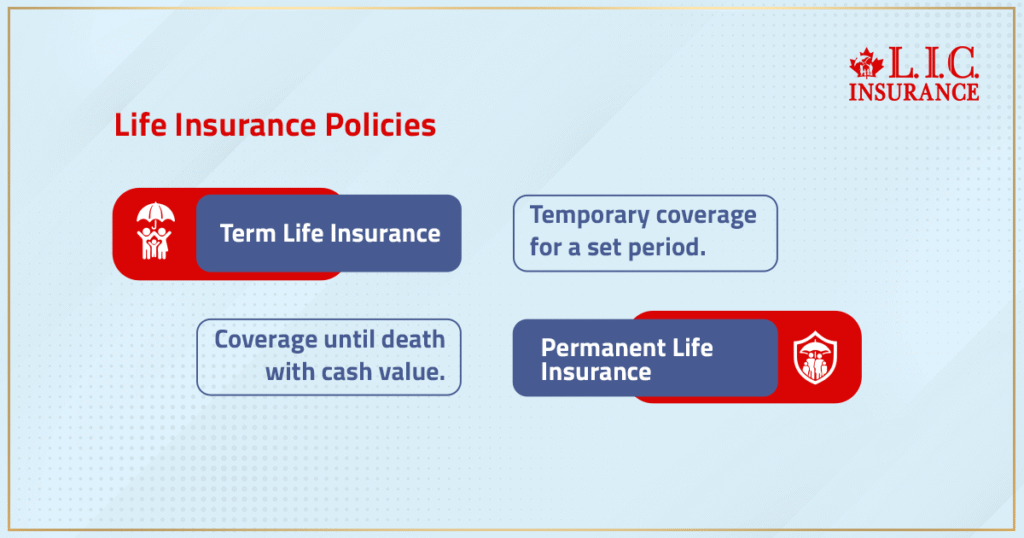

Term Life Insurance is temporary in nature; it is offered for 10 years, 20 years, or 30 years.

Term Insurance is cheap in the initial years but lapses after the completion of the term period.

Unlike Term Insurance, Guaranteed Universal Life Insurance is offered as long as you live.

Term Life Insurance vs Universal Life Insurance comparison:

- Term Life Insurance: Temporary insurance; premiums are cheap

- Guaranteed Universal Life Insurance: Long-Term Insurance; the death benefit is guaranteed

- Term Insurance: No cash values

- Guaranteed Universal Life: Limited cash values

For those who need to cover long-term financial obligations such as estate taxes, business succession, and funeral expenses, permanent Life Insurance is much better.

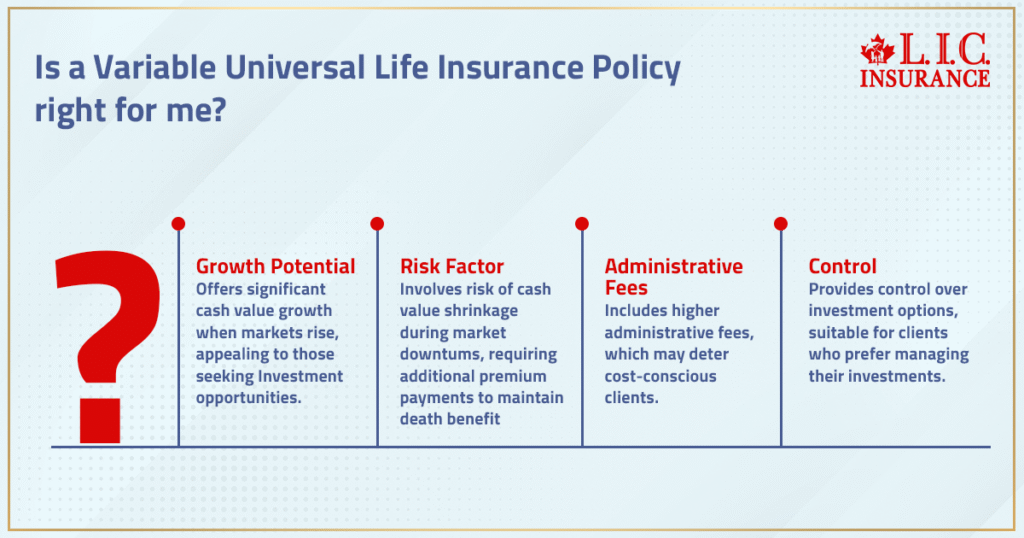

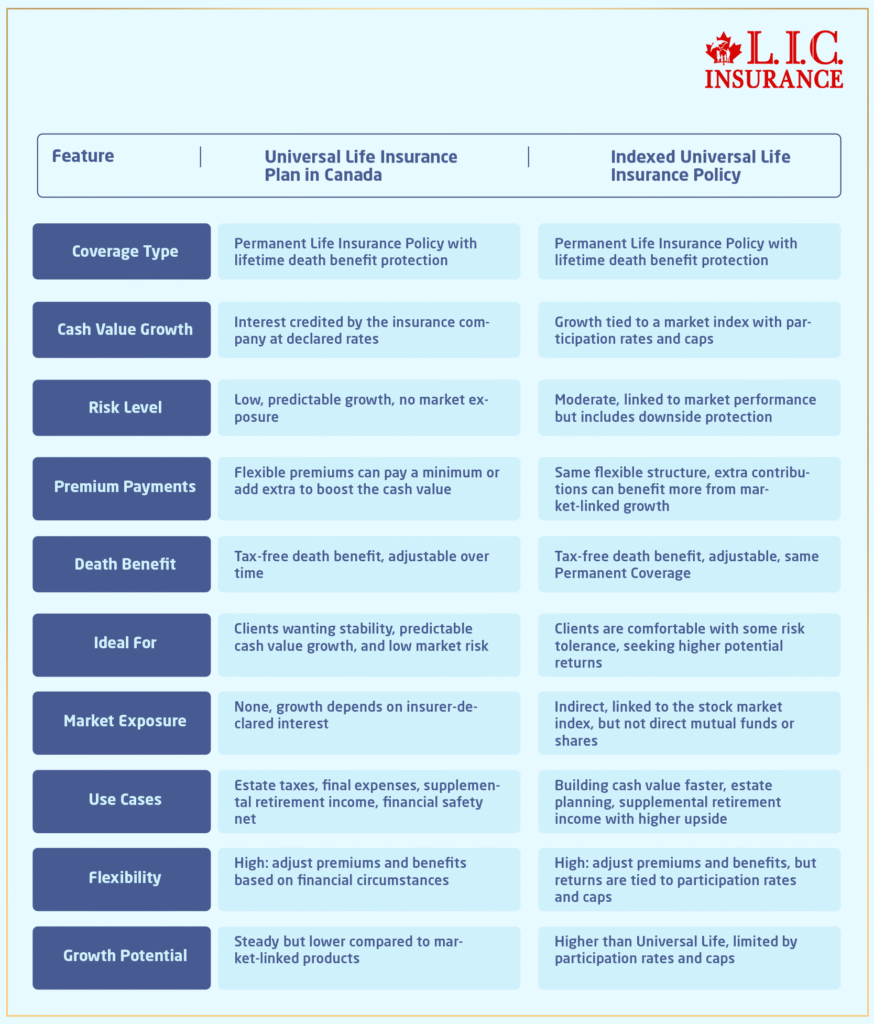

Indexed Universal Life Insurance And Variable Universal Life Insurance

Indexed Universal Life Insurance links growth to market indexes. Variable Universal Life Insurance allows policyholders to allocate funds into investment options such as equity-based investment funds.

Both offer:

- Investment account flexibility

- Potential investment growth

- Exposure to market performance

However, these policies include management fees and a higher risk.

Guaranteed Universal Life removes market dependency, providing stability without requiring active investment strategy oversight.

Guaranteed Universal Life Insurance Pros And Cons

Understanding Guaranteed Universal Life Insurance pros and cons is essential.

Pros

- Guaranteed death benefit

- Lifetime protection

- Lower premiums than whole life

- Predictable structure

- Effective for estate tax planning

- Suitable for final expenses

Cons

- Limited cash value growth

- Higher premiums than Term Life Insurance

- Missed premium payments can cause a lapse

- Less investment growth potential

Is Guaranteed Universal Life Insurance Worth It

Is Guaranteed Universal Life Insurance worth it? The answer to that varies based on one’s financial objectives.

For Canadians who want:

- Long-Term Life Insurance Plans in Canada

- Estate preservation

- Lifelong coverage

- Financial security

- Stable insurance protection

GUL insurance can be very effective for them.

Unlike the RRSP, Universal Life Insurance does not offer tax deduction benefits. However, it can offer tax-efficient wealth transfer and minimize estate taxes. Some withdrawals and loans can result in income taxes for beneficiaries.

Who Should Consider GUL Insurance In Canada

We recommend Guaranteed Universal Life Insurance for:

- Seniors who do not qualify for Term Insurance

- Those who need guaranteed Life Insurance

- Business owners who need succession planning

- Those who need final expense planning

- Those who need long-term protection

Permanent Life Insurance provides guarantees that Term Insurance cannot offer.

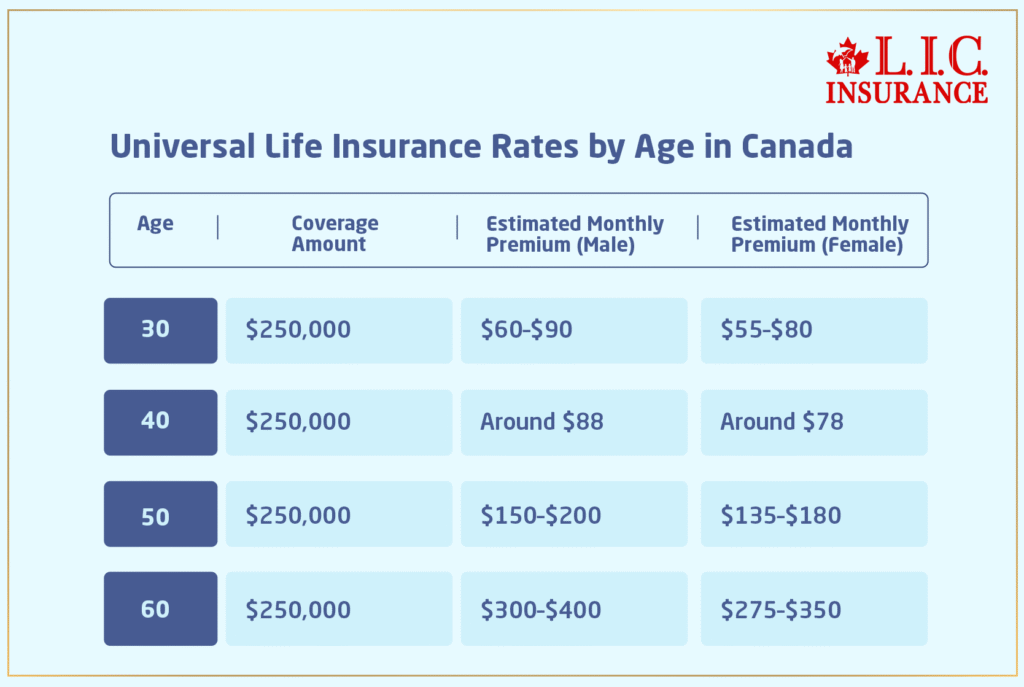

Costs Of Guaranteed Universal Life Insurance In Canada

Pricing depends on:

- Age

- Health status

- Smoking classification

- Coverage amount

- Medical underwriting results

Over a decade, Guaranteed Universal Life premiums may remain stable, whereas premiums for renewable Term Life Insurance may increase substantially.

The justification for premiums that are higher than Term Insurance is based on lifetime coverage and guaranteed stability of death benefits.

How Canadian LIC Structures Guaranteed Universal Life Policies

We structure Guaranteed Universal Life policies to align with:

- Financial future planning

- Estate tax efficiency

- Retirement income strategies

- Flexible protection solutions

- Comprehensive insurance protection

We evaluate:

- Coverage amount requirements

- Policy loans risk

- Cash value sustainability

- Financial obligations

- Long-term wealth transfer goals

Our structured approach ensures every Life Insurance Policy supports clients across their entire lives.

Conclusion: Choosing The Right Life Insurance Policy

Guaranteed Universal Life Insurance stands between Term Life Insurance and Whole Life Insurance.

It provides:

- Lifetime coverage

- Guaranteed death benefit

- Predictable premium payments

- Lower cost than whole life

- More stability than variable Universal Life Insurance

For Canadians who need solid permanent Life Insurance products without high levels of investment risk, Guaranteed Universal Life Insurance is still an effective financial planning solution.

Our goal is to assist clients in making the correct Life Insurance product choices to secure their future financially.

FAQs

Yes. Guaranteed Universal Life Insurance is often used in estate equalization, and this helps the family receive the insurance proceeds without the need to sell assets. This permanent Life Insurance Plan helps offset estate taxes and protect the family financially. Our Guaranteed Universal Life Insurance Policies facilitate the transfer of wealth in the most efficient manner.

The Universal Life Insurance quote helps the client understand the premium payments, the coverage amount, and the affordability of the policy in the long run. With the Universal Life Insurance quote, the clients are able to compare the different Universal Life Insurance Policy options and also make the best choice of investment and Life Insurance products. We offer customized quotes to the clients to make the best choice of Long Term Life Insurance Plans in Canada.

Yes. Guaranteed Universal Life Insurance can be employed in the financing of charitable donations by naming the charity as the beneficiary of the insurance policy. This has the advantages of providing lifetime coverage and also leaves a legacy and income tax savings. This is a viable way of matching insurance needs with philanthropic financial goals.

Cash Value Life Insurance Canada can facilitate business succession planning by providing liquidity to fund an ownership change. A Universal Life Insurance Plan might offer access to policy loans or partial withdrawals.

Guaranteed Universal Life provides a guaranteed death benefit after undergoing medical underwriting, while guaranteed Life Insurance provides no medical exams and offers a graded death benefit. GUL insurance may be more beneficial for elderly individuals looking for long-term coverage and predictable premium costs, especially when eligibility is met for GUL.

Yes. A Universal Life Insurance Policy with a cash value accumulation can provide a source of income for retirement via policy loans or partial withdrawal, which can be used in conjunction with a Registered Retirement Savings Plan to provide greater flexibility for the long-term.

The best Guaranteed Universal Life Insurance Plans in Canada are available from the leading insurance companies, including Manulife, Canada Life, Sun Life, and Equitable Life. The Guaranteed Universal Life Insurance Plans provide a guaranteed death benefit, lifetime coverage, and flexible coverage amount options. We compare multiple Life Insurance Plans to recommend the best Long Term Life Insurance Plans Canada according to your financial requirements and budget.

Guaranteed Universal Life Insurance Policies are based on the death benefit guarantee and premium predictability, whereas Whole Life Insurance Policies are based on cash value accumulation and the growth of dividends. Whole Life Insurance Policies are based on higher premiums and higher cash value growth. We can help clients decide on the difference between Universal Life Insurance and Whole Life Insurance.

There are insurance companies in Canada that offer Guaranteed Universal Life Insurance with structured premium payments and coverage options. Insurance companies like Manulife, Canada Life, and Empire Life offer Universal Life Insurance Policy solutions with flexible coverage options. We work with the best insurance companies to obtain competitive Universal Life Insurance quotes according to the coverage amounts, financial obligations, and planning needs.

Yes. Many Term Life Insurance Policies have conversion privileges that permit the policyholders to convert to Guaranteed Universal Life Insurance without the need for further medical examinations or underwriting. This guarantees the policyholders lifelong coverage and insurability. We help our clients convert their Term Insurance policies to permanent Life Insurance Policies and thereby enjoy financial security and insurance protection.

Guaranteed Universal Life Insurance is not recommended as a primary investment tool but provides secure financial protection with no investment risk. Although the cash value accumulation and investment options are limited compared to other Universal Life Insurance products, this type of insurance provides predictable insurance costs and lifetime protection. Canadian LIC recommends GUL Insurance to clients who are focused on estate planning, funeral expenses, and other financial needs.

The premiums for a Guaranteed Universal Life Insurance Policy are affected by age, health condition, smoker classification, amount of coverage, and the outcome of the medical underwriting process. Other factors include administrative fees, minimum premiums, and policy design. We help clients compare Life Insurance quotes from the top insurance companies to obtain a cost-effective Guaranteed Universal Life policy that suits each client’s objectives and requirements.

Sources and Further Reading

- Manulife – Universal Life Insurance (Canada)

Explains Universal Life Insurance features (guaranteed coverage options and long-term protection context) relevant to Guaranteed Universal Life.

https://www.manulife.ca/personal/insurance/our-products/life-insurance/permanent-life-insurance/manulife-universal-life.html - Canada Life – Universal Life Insurance Overview

Provides product insight on Universal Life Insurance with lifetime coverage potential — relevant context for Guaranteed Universal Life structures.

https://www.canadalife.com/insurance/life-insurance/permanent-life-insurance/universal-life-insurance.html - Sun Life – Universal Life Insurance (Permanent Coverage)

A Canadian insurer’s permanent universal life offering with details on flexible premiums and long-term planning, which underpins Guaranteed Universal Life.

https://www.sunlife.ca/en/insurance/life/permanent-life-insurance/universal/

Key Takeaways

- Guaranteed Universal Life Insurance Offers Lifelong Protection:

Guaranteed Universal Life Insurance in Canada provides lifetime coverage with a guaranteed death benefit, making it a reliable option for long-term financial security and estate planning. - Predictable Premiums Ensure Financial Stability:

Unlike other Universal Life Insurance Policies, GUL insurance features consistent premium payments, helping Canadians plan their financial future with confidence and stability. - Cost-Effective Alternative To Whole Life Insurance:

Guaranteed Universal Life Insurance typically has lower premiums than Whole Life Insurance while still offering permanent Life Insurance protection and dependable coverage. - Ideal For Estate Planning And Wealth Transfer:

This type of Life Insurance Policy is widely used to cover estate taxes, support beneficiaries, and preserve wealth across generations through tax-efficient wealth transfer strategies. - Limited Cash Value But Strong Protection Focus:

Although cash value accumulation is minimal compared to other permanent Life Insurance products, GUL insurance prioritizes guaranteed coverage and financial protection. - Suitable For Individuals Seeking Long Term Life Insurance Plans Canada:

Guaranteed Universal Life is a practical choice for clients who want stable insurance protection without the complexity of managing investment options or market-linked returns. - Conversion Options Enhance Long-Term Flexibility:

Many Term Life Insurance Policies can be converted into Guaranteed Universal Life Insurance without medical underwriting, ensuring continued coverage and lifelong protection. - Premiums Depend On Key Personal And Policy Factors:

Age, health condition, smoking status, coverage amount, and medical underwriting significantly influence Guaranteed Universal Life Insurance premiums in Canada. - Canadian LIC Provides Expert Guidance And Policy Structuring:

Our licensed advisors compare Life Insurance companies and Universal Life Insurance quotes to help clients choose the most suitable Guaranteed Universal Life Insurance Policies aligned with their financial goals.

Your Feedback Is Very Important To Us

Thank you for taking a moment to share your feedback. Your responses will help us better understand your financial goals and provide tailored guidance on Guaranteed Universal Life Insurance solutions.

Privacy Note

Your information will be kept confidential and used solely to provide personalized guidance and insurance solutions. Canadian LIC respects your privacy and adheres to Canadian data protection and anti-spam regulations.

IN THIS ARTICLE

- What Is Guaranteed Universal Life Insurance In Canada

- What Is Guaranteed Universal Life Insurance And How Does It Work

- How Universal Life Insurance Works

- Key Features Of Guaranteed Universal Life Insurance

- Cash Value And Cash Value Growth Explained

- Guaranteed Universal Life Insurance Vs Whole Life Insurance

- Guaranteed Universal Life Insurance Vs Term Life Insurance

- Indexed Universal Life Insurance And Variable Universal Life Insurance

- Guaranteed Universal Life Insurance Pros And Cons

- Is Guaranteed Universal Life Insurance Worth It

- Who Should Consider GUL Insurance In Canada

- Costs Of Guaranteed Universal Life Insurance In Canada

- How Canadian LIC Structures Guaranteed Universal Life Policies

- Conclusion: Choosing The Right Life Insurance Policy