- How Much Do I Need to Retire in Canada?

- The Basics of Retirement Planning in Canada

- Determining Your Retirement Age

- Estimating Your Retirement Expenses

- Sources of Retirement Income

- Calculating Your Retirement Savings Goal

- Investment Strategies for Retirement

- Tax Considerations in Retirement

- Adjusting Your Retirement Plan Over Time

- Retirement Saving Rules

- Wrapping It Up

Retirement is a significant milestone in one’s life, representing the culmination of years of hard work and financial planning. For those planning to retire in Canada, determining how much money is needed for a comfortable retirement is a crucial question. The answer varies depending on various factors, including your lifestyle, location, retirement age, and financial goals. In this comprehensive guide, we will delve into the key considerations and calculations to help you estimate how much you need to retire in Canada.

The Basics of Retirement Planning in Canada

Retirement planning in Canada is a multifaceted endeavour that involves setting financial goals, assessing your current financial situation, and creating a roadmap to achieve those goals. Here are some fundamental steps to get started:

- Set Clear Retirement Goals: Begin by envisioning your retirement lifestyle. Do you plan to travel extensively, downsize your home, or engage in expensive hobbies? Your retirement goals will dictate your financial needs.

- Assess Your Current Finances: Take stock of your current financial situation, including your savings, investments, and any existing pension plans. This baseline assessment will help you determine how close you are to your retirement goals.

- Create a Retirement Budget: Develop a detailed budget that outlines your expected retirement expenses. Consider categories such as housing, healthcare, transportation, entertainment, and daily living expenses.

Determining Your Retirement Age

One critical decision in retirement planning is determining your retirement age. The age at which you choose to retire has a significant impact on how much you need to save. In Canada, the standard retirement age for receiving full Old Age Security (OAS) and Canada Pension Plan (CPP) benefits is currently 65. However, you can choose to retire earlier or later based on your preferences and financial circumstances.

- Early Retirement: Some Canadians opt for early retirement, which can be as early as age 55. However, early retirement usually means reduced government pension benefits, so it’s crucial to plan for additional sources of income.

- Delayed Retirement: Delaying retirement can have financial benefits, as government pension benefits increase for each year you delay taking them (up to age 70 for CPP). Delayed retirement also allows for more time to accumulate savings.

Estimating Your Retirement Expenses

To determine how much you need to retire comfortably, you must estimate your retirement expenses. These expenses can be categorized into essential and discretionary:

- Essential Expenses: These are the costs you must cover for basic needs, such as housing, food, utilities, transportation, and healthcare.

- Discretionary Expenses: Discretionary expenses include activities like travel, hobbies, dining out, and entertainment. While these expenses are not essential, they contribute to your overall quality of life in retirement.

To estimate your expenses accurately, consider factors like inflation, potential healthcare costs, and any existing debts that need to be paid off before retirement.

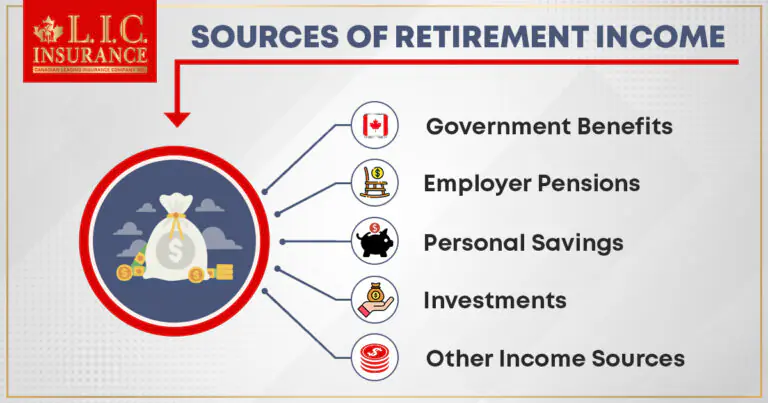

Sources of Retirement Income

In Canada, retirees typically rely on a combination of income sources to fund their retirement lifestyle. Understanding these sources is crucial when calculating how much you need to retire comfortably:

Government Benefits:

The Canadian government provides several retirement benefits, including the Old Age Security (OAS) and the Canada Pension Plan (CPP). The amount you receive depends on factors like your years of contribution and retirement age.

Employer Pensions:

If you have a workplace pension plan, it will provide a reliable source of retirement income. The amount you receive depends on your salary, years of service, and the plan’s terms.

Personal Savings:

Personal savings, including Registered Retirement Savings Plans (RRSPs) and Tax-Free Savings Accounts (TFSAs), play a significant role in retirement planning. These accounts allow you to save and invest money tax-efficiently.

Investments:

Investments such as stocks, bonds, and mutual funds can generate income through dividends, interest, and capital gains. Proper investment planning is essential to ensure a steady income stream.

Other Income Sources:

Consider any other sources of income you may have in retirement, such as rental income, part-time work, or business income.

Life insurance is another source of retirement income to take into account. Although a lot of individuals primarily consider pensions as a way to support their families when they pass away, they can also be used to supplement retirement income.

If you want to use life insurance for retirement, your options include whole life or universal life. Both are types of permanent life insurance, which means the protection is lifelong in nature. They also develop cash value, which can be accessed whenever you like and increases tax-deferred.

Cash value only becomes taxable upon withdrawal because it grows tax-deferred. If you use it after retirement, your tax burden will likely be lower because your taxable income will be smaller than it is now.

By surrendering your policy, you might get cash value all at once or in monthly installments. Only people under the age of 45 should consider using life insurance as a vehicle for retirement planning because cash value growth doesn’t accelerate until after 10 to 15 years.

Cash value from whole life insurance accrues interest at a certain rate set by the insurer. In contrast, with universal life insurance, the pace of cash value growth is not fixed. The performance of the metrics of the sub-accounts that are linked to it can also affect the cash value growth rate.

Calculating Your Retirement Savings Goal

To estimate how much you need to retire in Canada, you can follow these steps:

- Determine Your Retirement Income: Start by adding up your expected retirement income from government benefits, employer pensions, and other sources.

- Calculate Your Retirement Expenses: Create a detailed budget that outlines your expected expenses in retirement. Be realistic and consider inflation.

- Identify the Income Gap: Subtract your estimated retirement income from your projected expenses. This will reveal the income gap you need to fill with personal savings and investments.

- Estimate Your Withdrawal Rate: Determine a safe withdrawal rate for your investments. A common guideline is the 4% rule, which suggests withdrawing 4% of your initial retirement portfolio balance annually, adjusted for inflation.

- Calculate Your Savings Goal: To calculate your retirement savings goal, use the following formula: Savings Goal = (Income Gap ÷ Withdrawal Rate)

For example, if your income gap is $20,000 per year and your chosen withdrawal rate is 4%, your savings goal would be $500,000.

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Investment Strategies for Retirement

As you approach retirement, your investment strategy may shift from wealth accumulation to income generation and capital preservation. Here are some investment strategies to consider:

- Asset Allocation: Diversify your investment portfolio to manage risk. A mix of stocks, bonds, and cash equivalents can provide a balance of growth and stability.

- Income-Generating Investments: Consider investments that provide regular income, such as dividend-paying stocks, bonds, and real estate investment trusts (REITs).

- Tax-Efficient Withdrawals: Plan your withdrawals strategically to minimize taxes. This may involve withdrawing from taxable, tax-deferred, and tax-free accounts in a tax-efficient manner.

- Professional Advice: Consult a financial advisor to help you create an investment strategy tailored to your retirement goals and risk tolerance.

Tax Considerations in Retirement

Understanding the tax implications of your retirement income is essential for effective retirement planning. Key tax considerations include:

- Tax on Pension Income: Different types of retirement income are taxed differently. For example, OAS and CPP benefits are taxable, while withdrawals from RRSPs and TFSAs are generally not subject to income tax.

- Tax-Efficient Withdrawals: Plan your retirement withdrawals to minimize taxes. This may involve strategies like income splitting with your spouse or using the tax-free nature of TFSAs.

- RRSP Conversions: By age 71, you must convert your RRSP into a Registered Retirement Income Fund (RRIF) or use the funds to purchase an annuity. Both options have tax implications that should be considered.

- Estate Planning: Consider the impact of taxes on your estate and heirs. Proper estate planning can minimize the tax burden on your estate.

Adjusting Your Retirement Plan Over Time

Your retirement plan is not static; it should evolve as your circumstances change. Here are some considerations for adjusting your retirement plan:

- Regular Review: Periodically review your retirement plan to ensure it aligns with your current goals and financial situation.

- Healthcare Costs: Be prepared for potential increases in healthcare costs as you age. Consider long-term care insurance if needed.

- Inflation: Consider inflation in your retirement budget to maintain your purchasing power over time.

- Asset Allocation: Adjust your investment portfolio as you age and your risk tolerance changes. Shift towards more conservative investments if necessary.

- Legacy Planning: Continually assess your estate planning needs, including updating your will and beneficiary designations.

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Retirement Saving Rules

Let’s explore how these retirement saving rules can be applied in the context of Canada:

The 50/30/20 Rule:

The 50/30/20 rule is a budgeting guideline that can be adapted for retirement savings in Canada. Here’s how you can apply it:

50% for Needs: Dedicate 50% of your income to cover essential expenses, including housing, utilities, groceries, healthcare, and transportation. This ensures you can maintain a comfortable lifestyle during retirement.

30% for Wants: Allocate 30% of your income to discretionary spending, which includes non-essential expenses like dining out, entertainment, and travel. Reducing these expenses during retirement can free up funds for savings.

20% for Savings: Reserve at least 20% of your income for retirement savings. This includes contributions to retirement accounts like RRSPs (Registered Retirement Savings Plans) and TFSAs (Tax-Free Savings Accounts).

Adhering to this rule can help you balance your current lifestyle with your retirement savings goals.

Savings by Age (As a Multiplier of Income) Rule:

The “Savings by Age” rule provides a rough guideline for how much you should aim to have saved for retirement at various stages of your life. In Canada, the rule can be adapted as follows:

By Age 30: Target savings equivalent to about 1 times your annual income. For example, if your annual income is $50,000, aim to have saved around $50,000 for retirement.

By Age 40: Strive to have savings of about 3 times your annual income. With an income of $60,000, this would mean having around $180,000 saved.

By Age 50: Aim for savings of about 6 times your annual income. With an income of $70,000, this would translate to approximately $420,000 in retirement savings.

By Age 60: Target savings of approximately 8 times your annual income. If your income is $80,000, aim for savings of around $640,000.

These multipliers can serve as benchmarks, but remember that individual circumstances, such as lifestyle, retirement goals, and investment returns, can significantly impact your actual savings needs.

Years Multiplied by Annual Expenses Rule:

The “Years Multiplied by Annual Expenses” rule is a useful way to estimate your retirement savings requirements in Canada:

- Estimate your annual retirement expenses, considering factors like housing, healthcare, transportation, and leisure activities.

- Determine the number of years you expect to spend in retirement. In Canada, people are living longer, so consider a retirement period that covers your expected lifespan.

- Multiply your estimated annual expenses by the number of years in retirement. For instance, if you anticipate annual retirement expenses of $40,000 and plan for a 25-year retirement, your estimated retirement savings target would be $1 million ($40,000 x 25).

Keep in mind that these rules offer simplified guidance and should be adapted to your specific circumstances. Consulting with a financial advisor and using retirement planning tools can provide a more personalized and accurate retirement savings strategy tailored to the Canadian context. Additionally, consider the impact of government programs like the Canada Pension Plan (CPP) and Old Age Security (OAS) in your retirement planning.

Wrapping It Up

Planning for retirement in Canada requires careful consideration of your lifestyle, financial goals, and income sources. You can work towards a comfortable and financially secure retirement by estimating your retirement expenses, calculating your savings goal, and crafting an investment strategy. Keep in mind that retirement planning is an ongoing process that should adapt to your changing circumstances and financial landscape. With prudent financial management and a clear retirement plan, you can look forward to enjoying your retirement years with peace of mind.

Faq's

Ideally, you should start planning for retirement as early as possible. Many financial experts recommend beginning in your 20s or 30s. The earlier you start saving and investing, the more time your money has to grow, potentially resulting in a more substantial retirement fund.

Life expectancy can vary among individuals. You can use general statistics for Canadians, but it’s often more accurate to consider your family’s health history and your own lifestyle choices. A financial advisor can help you make a reasonable estimate.

While government pension benefits can be a significant part of your retirement income, they are typically not sufficient to maintain your desired lifestyle in retirement. It’s advisable to supplement these benefits with personal savings, investments, and possibly employer pensions.

The amount you should contribute to your RRSP depends on your income, tax situation, and retirement goals. The Canada Revenue Agency (CRA) sets annual RRSP contribution limits based on your income. A financial advisor can help you determine an appropriate contribution strategy.

RRSPs allow you to contribute pre-tax income and defer taxes until withdrawal, making them tax-advantageous if you expect to be in a lower tax bracket in retirement. TFSAs, on the other hand, use after-tax contributions but offer tax-free growth and withdrawals, making them flexible for various financial goals, including retirement.

Yes, it’s possible to retire early in Canada (as early as age 55), but it may result in reduced government pension benefits, such as OAS and CPP. Consider how early retirement may affect your overall retirement income and plan accordingly.

To account for inflation, you can use a rule of thumb that assumes an average annual inflation rate of around 2-3%. Adjust your projected expenses for each year of your retirement accordingly to maintain your purchasing power.

Investment strategies for retirement should balance growth and preservation of capital. This often involves a diversified portfolio that includes stocks, bonds, and other asset classes. Your asset allocation should reflect your risk tolerance and time horizon.

Yes, Canada offers programs like the Canada Pension Plan (CPP), Old Age Security (OAS), and the Guaranteed Income Supplement (GIS) to provide financial support in retirement. Additionally, there are incentives like RRSPs and TFSAs that offer tax benefits for retirement savings.

Creating a retirement budget involves estimating your expenses and matching them to your retirement income. Tracking your spending, having a buffer for unexpected expenses, and periodically reviewing and adjusting your budget can help you stay on track in retirement.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com