BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

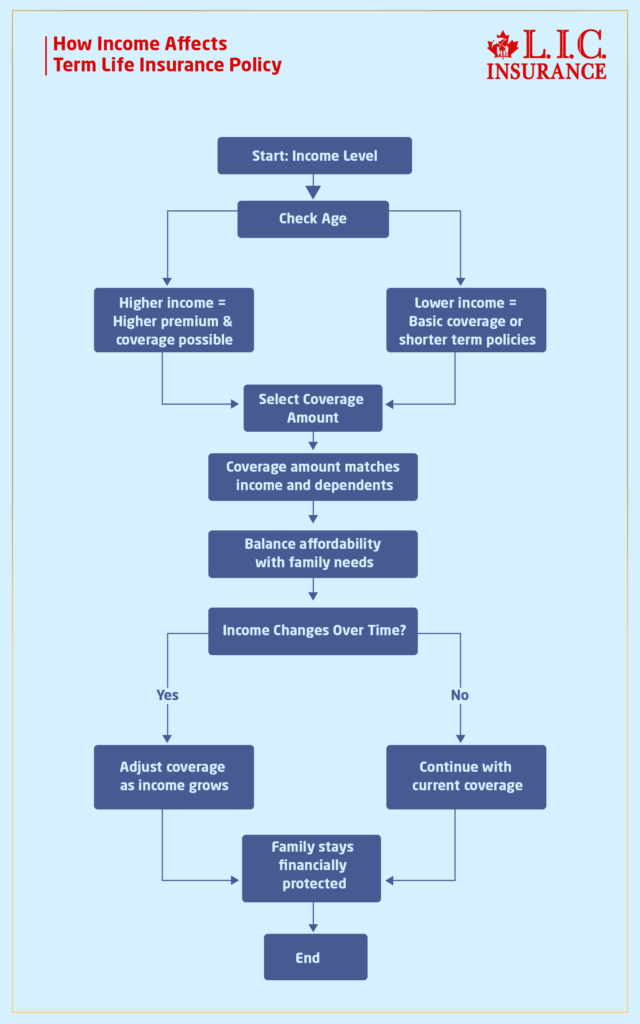

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

The Predictability Advantage: How Whole Life Insurance Builds Lifelong Financial Stability In Canada

By Pushpinder Puri

CEO & Founder

- 15 min read

- March 24th, 2026

SUMMARY

A detailed look at how a Whole Life Insurance Policy in Canada provides lifelong coverage, guaranteed cash value, and a tax-free death benefit. Explains differences between participating and Non-Participating Plans, highlights benefits for estate planning and seniors, covers tax advantages, and shows how Whole Life Insurance builds lasting financial stability and supports long-term financial goals.

Introduction

Predictability. It’s that one thing all Canadians wish for in the quiet of their hearts when it comes to money. We are putting that to the test today: We want to know what tomorrow looks like, not hope for it, not guess. Just know. In a financial world that seems more uncertain than ever, there is one product that has withstood the test of time – the Whole Life Insurance Policy in Canada.

We know that this kind of policy can silently become the bedrock for a family’s financial security. It does not scream or sway with the market. It does simply, year after year, punctured by none of these faddish excursions that the modern novel is prone to taking, what it’s supposed to.

Canadians have trillions in Life Insurance Coverage held on the books, according to data from the Canadian Life and Health Insurance Association (CLHIA), and yet they still love short-term or low-cost term plans. They miss the reality of what Permanent Life Insurance is — a contract that not only protects your family for their entire lives, but also grows in value, assists with estate planning, and produces a legacy that doesn’t rely on tomorrow’s interest rates.

So we thought we’d take a closer look at how Whole Life Insurance offers that predictability benefit — and why it is still one of the essential tools in lifelong financial planning.

Understanding Whole Life Insurance: The Foundation of Predictability

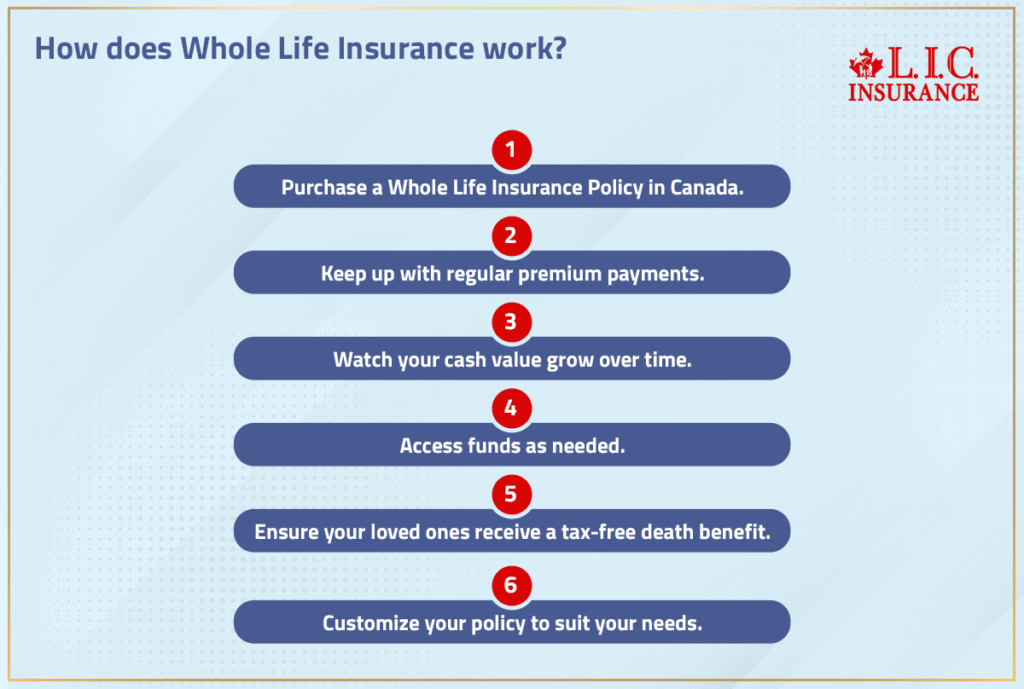

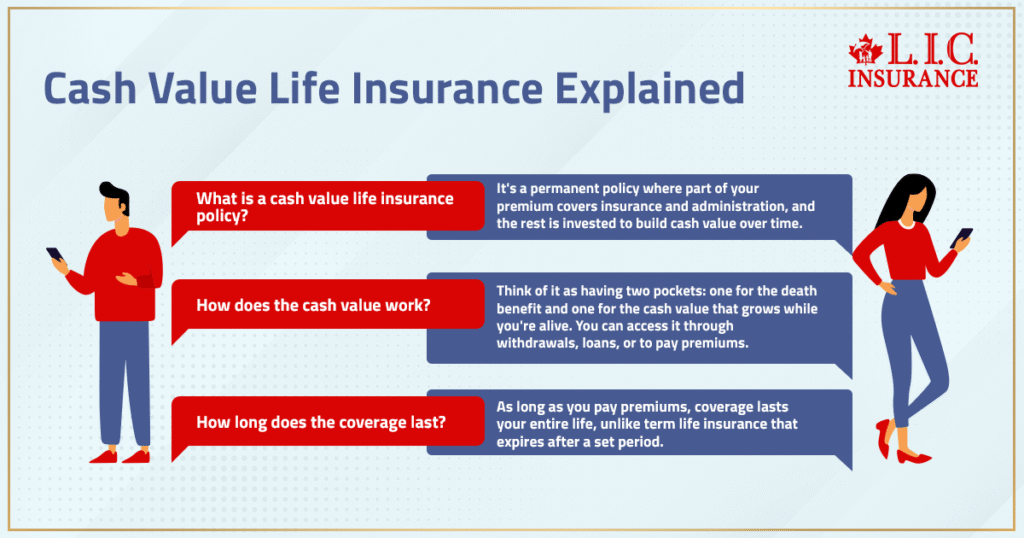

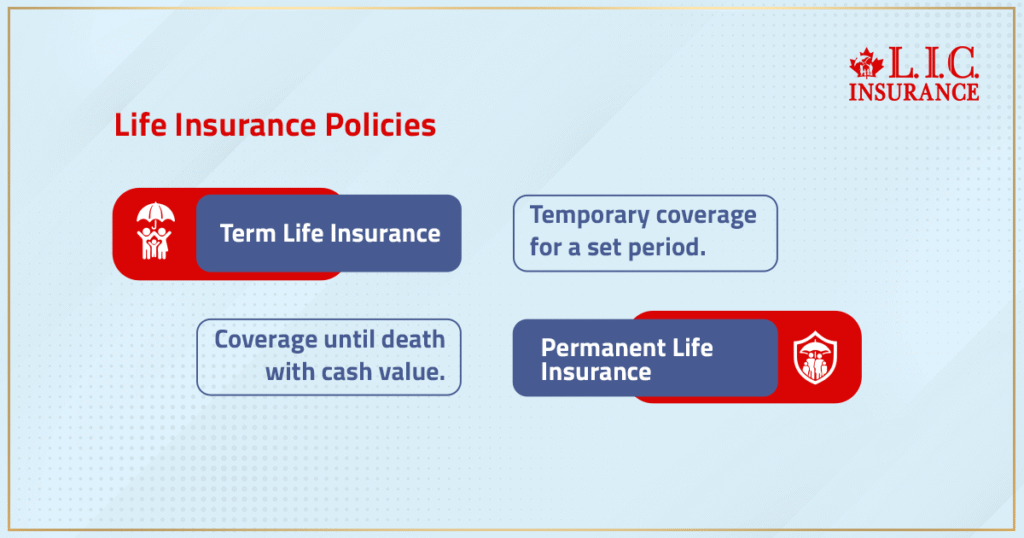

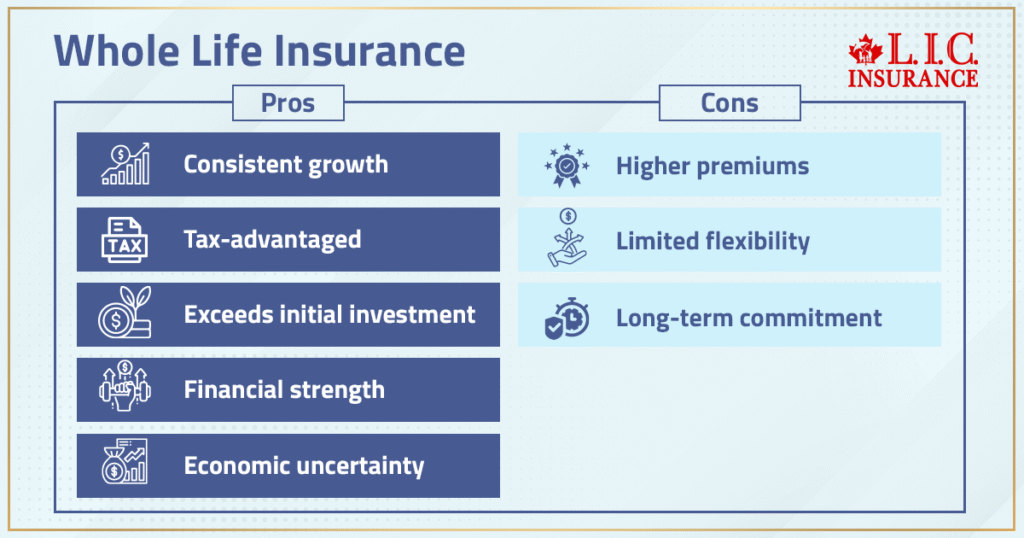

A Whole Life Insurance Policy in Canada is a guarantee that is good for as long as you are. It’s not built to expire. It’s built to stay.

Unlike Term Life Insurance, which offers coverage for a specified time frame, whole life is a type of Permanent Coverage. Which is to say, it pays out — whenever the person who is insured dies — and offers a cash value that can be tapped even while he or she (the policyholder) is still living.

Here’s what makes it unique:

- Guaranteed death benefit: The policy guarantees that your beneficiaries will receive the death benefit no matter when the insured passes away.

- Cash value accumulation: A portion of each premium goes toward building cash value, which acts like a savings element inside the policy.

- Fixed premiums: You pay the same premium throughout the life of the policy — no surprises, no jumps, no renewals.

- Tax advantages: The death benefit is typically tax-free, and the cash value grows tax-deferred under Canadian tax rules.

- Estate planning benefits: The policy provides the liquidity needed to cover estate taxes, final expenses, or equalize inheritances.

When markets drop, housing slows, or inflation rises, these guarantees don’t move. That’s the beauty of predictability — and the reason so many families rely on it as a foundation for their financial security.

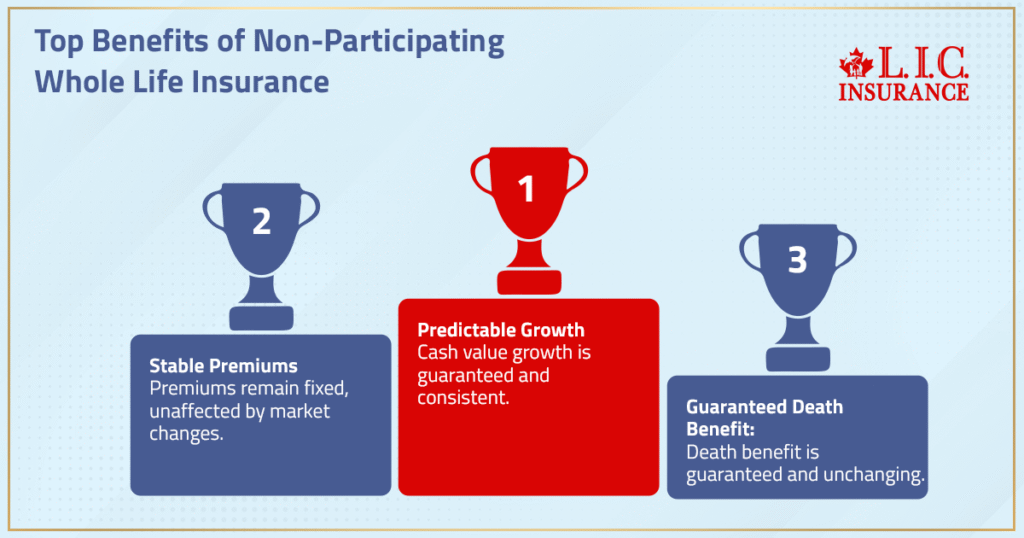

The Predictability Factor: Why Non-Participating Whole Life Matters

The most stable version of Whole Life Insurance is what’s known as Non-Participating Whole Life (Non-Participating). In these policies, the insurer guarantees every key element — from the growth rate to the guaranteed cash value — right at the start.

Here’s why clients love them:

- They know exactly what their cash value growth will look like each year.

- Their fixed premiums stay level, regardless of market or interest-rate changes.

- Their guaranteed death benefit never fluctuates.

- They’re not exposed to the insurer’s investment returns or expense performance.

In short, the insurer carries most of the risk — not the policyholder. That makes Non-Participating whole life ideal for anyone who values financial stability, wants a tax-free death benefit, and prefers to plan around known numbers rather than assumptions.

We often call this the predictability advantage. It’s the comfort of knowing that no matter what happens in the markets or the economy, your plan stays intact.

Participating Whole Life: Opportunity Meets Uncertainty

Then there’s the Participating Whole Life (par). This version lets policyholders share in the insurance company’s profits through dividends. Those dividends aren’t guaranteed — they depend on the insurer’s investment returns, expenses, and mortality experience.

Dividends can be:

- Used to reduce premiums,

- Left to accumulate interest,

- Taken in cash, or

- Used to buy paid-up additions (PUAs) that increase both cash value and death benefit.

Participating Life Insurance Policies can do even better than Non-Participating Policies when the insurer is doing well, though they may also underperform if rates fall or expenses rise.

Consider this actual reality that we looked at. A policy from the 1970s led to a $29,000 death benefit being projected at age 82. By 2019, that estimate had sunk to $27,000. Why? Dividend scales were reduced, and the hurdle rate — in effect, the minimum return required before dividends are distributed — wasn’t reached. The lesson is plain: participating policies demand a tougher stomach for variability.

They’re powerful tools, unless they’re not. Some like that extra layer of predictability Non-Participating Whole Life provides — particularly for an estate plan or retirement planning.

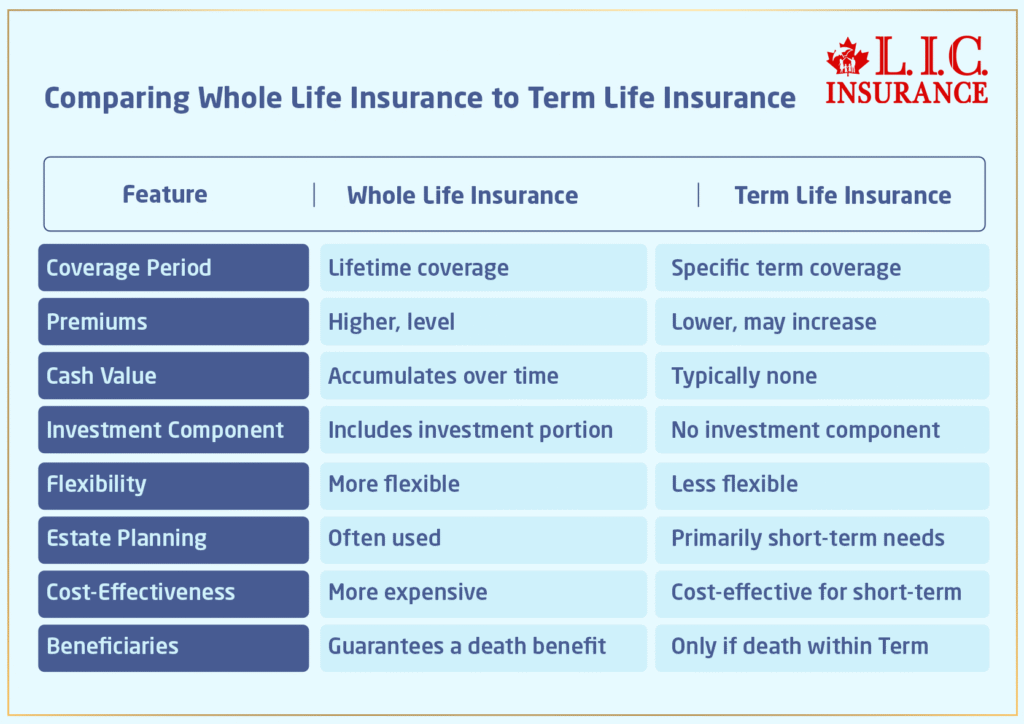

Participating vs. Non-Participating: Understanding the Difference

| Feature | Participating (Par) Whole Life | Non-Participating (Non-Participating) Whole Life |

|---|---|---|

| Crediting rate guaranteed? | No | Yes |

| Dividends | Yes, variable | No |

| Performance sensitivity | High | Low |

| Insurer risk exposure | Shared with policyholder | Fully borne by the insurer |

| Ideal for | Growth seekers | Predictability seekers |

Participating plans rely on market performance, while Non-Participating Plans rely on guarantees. We help clients weigh these two forces — opportunity vs. stability — and determine which better supports their financial goals and risk comfort.

The Advisor’s Lens: Choosing the Right Plan

Our advisors see every case differently. There’s no one-size-fits-all solution. Every recommendation begins with three key questions:

- What’s the goal? Is it estate liquidity, income protection, or generational wealth transfer?

- What’s the timeline? Younger clients might prioritize long-term cash value accumulation; older clients may need guaranteed lifetime coverage.

- What’s the risk tolerance? Some clients prefer the steady path of Non-Participating Policies; others want exposure to dividends for higher potential growth.

Our job is to translate science into action. That involves breaking down complicated concepts like guaranteed cash value, death benefits, and premium payments into plain English — in a way that consumers actually grasp what they’re purchasing.

We also show how a policy can supplement retirement income, provide emergency funds, or be used as a tax-efficient wealth transfer vehicle. But it’s not exactly insurance — it’s structured protection with flexibility built in.

Tax and Growth Considerations: Clearing Up Misconceptions

Is Whole Life Insurance Taxable?

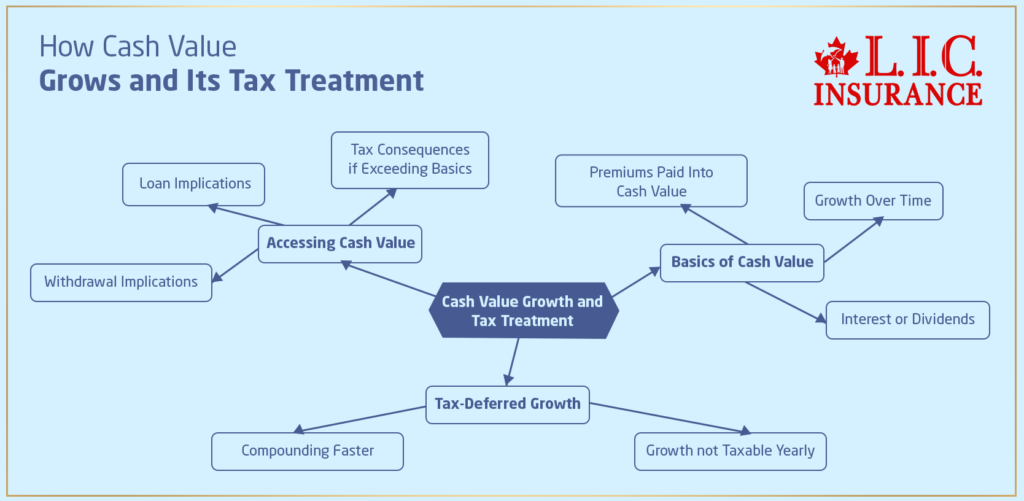

Here’s the thing: Whole Life Insurance is usually paid out tax-free in Canada. The cash value within the policy grows tax-deferred, so you don’t pay annual taxes on that growth unless you withdraw more than your adjusted cost basis.

That’s a big deal. It enables the money to compound quietly, behind the scenes, without producing annual tax slips. The result? A tax-efficient shelter to protect your estate and the financial security of your family.

Why It’s a Powerful Tax Planning Tool

Whole Life Insurance is a common estate planning tool for that very reason. It also offers a tax-free death benefit, which can pay off estate taxes, business buyouts or even go toward charitable donations, without having to change plans for other investments.

It can also double as a retirement plan; you can borrow on the cash value or use It to keep premiums down on your policy later in life. The trick lies in balance — both between your savings and the other living costs to which you need to apply cash over time, and between growth potential, liquidity, and tax efficiency.

Why Some Older Policies Aren’t Performing as Expected

We have had plenty of Canadians show us old participating policies that had failed to perform as illustrated. But the cause isn’t misspending — it’s a change in economic circumstances.

In the 1970s and ‘80s, policies were priced in an era of double-digit interest. In today’s low-rate economy, those assumptions don’t hold. Even some of the old par policies can’t keep up with those original assumptions or projections, given increasing costs, longevity, and falling dividend scales.

Still, even under these policies, cash value is guaranteed, and it can grow tax advantaged. And even if the non-guaranteed part underperforms, there is still that guaranteed core. That’s the beauty of whole life — it makes good when the market does not.

We frequently change the topic of conversation for clients. It’s not what the policy can no longer do; it’s what the policy can still provide: lifetime coverage, guaranteed values, and a solid base for estate planning.

Whole Life Insurance for Seniors and Estate Planning

With Canadians living longer, the demand for lifelong protection is greater. And many seniors simply want to make sure their estates will be settled smoothly, without leaving sons and daughters to pay any taxes or debts, funeral expenses, or other outlays.

Whole Life Insurance offers a guaranteed payout to help with final expenses, estate taxes, or simply provide for your loved ones. The best Whole Life Insurance for seniors will be simple: level premiums, guaranteed growth, and predictable results.

We recommend that many retirees who don’t want market-type returns consider Non-Participating Plans. These policies offer the peace of mind that their family’s future will be taken care of regardless of what comes next.

For business owners, whole life can be used to finance shareholder agreements or provide liquidity for succession planning. It’s not just about safeguarding assets — it’s about ensuring stability.

Integrating Whole Life Into a Broader Financial Strategy

Whole Life Insurance is more than a policy; it’s a financial instrument that can complement other strategies. Here’s how we help clients integrate it effectively:

- Compare Whole Life Insurance quotes from reputable Canadian insurers.

- Match policy type to purpose — Non-Participating for predictability, par for growth.

- Blend with other products: Some clients use Universal Life Insurance for flexibility and whole life for guarantees.

- Coordinate with investments: Whole life provides a stable component that balances out market-based assets.

- Review regularly: Policy reviews help track cash value growth and adapt to changing family needs.

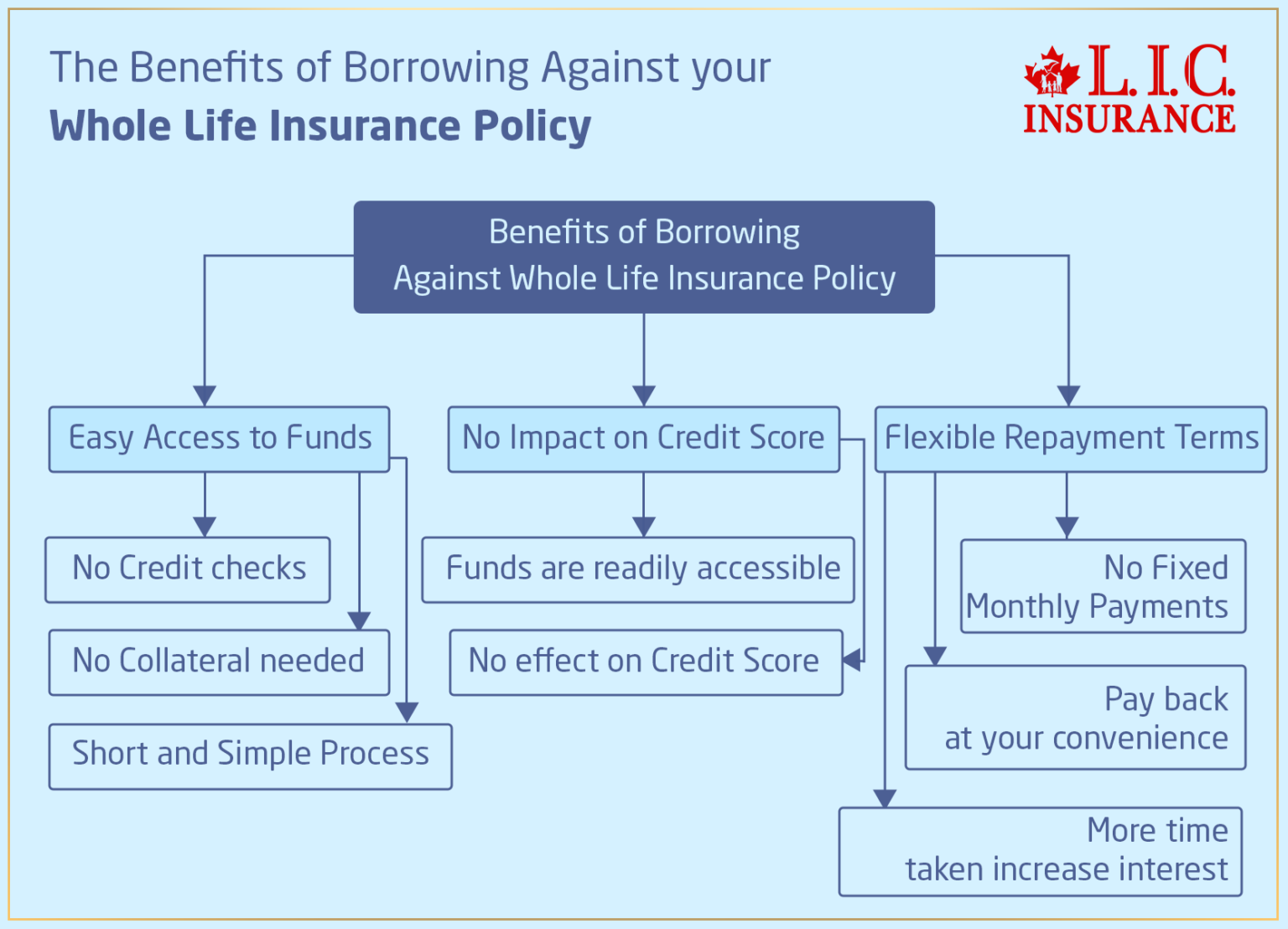

A well-structured policy can even accumulate cash that serves as collateral for loans or emergency funding — a valuable feature during uncertain times.

Common Client Questions

Q: Isn’t term life cheaper?

Yes, but it’s temporary. Term Life Insurance covers you for a set period and expires. Whole life lasts forever, offering lifelong protection and cash value that grows every year.

Q: How do we justify the higher cost?

You’re buying guarantees — a fixed premium, a guaranteed cash value, and a tax-free death benefit. It’s not a cost; it’s a long-term asset that protects your financial future.

Q: Is the cash value an investment?

Not in the traditional sense. Think of it as a built-in savings feature that earns steady, tax-deferred returns. It’s meant to enhance stability, not replace your portfolio.

Q: Can whole life support retirement planning?

Absolutely. The cash value component can be borrowed against or used to supplement retirement income later in life — without interrupting the policy’s protection.

Q: What if market rates change?

That’s the best part. Your Whole Life Plan isn’t tied to the market. Whether rates rise or fall, your guaranteed cash continues to grow.

The Predictability Advantage: Why It Still Matters

There’s just something deeply reassuring about realizing that your plan will not collapse when the economy feels wobbly. Whole Life Insurance provides that foundation — unslippable, unwavering and structured for the long haul.

I’ve helped many other families protect their wealth and type proseoniovepol well-designed Life Insurance policies that get stronger over time. We personally believe financial freedom is not just about growth, but rather it’s about consistency.

Whole life provides that. It’s not about chasing returns; it’s about ensuring your financial legacy lives on — for your children, for the business and generation that follow.

So whether you’re shopping around for Whole Life Insurance quotes, evaluating your coverage or laying out your estate plans, remember this: predictability isn’t boring — it’s powerful.

Because when your policy is built right, it doesn’t just protect your life.

It protects your entire life.

Understanding these elements helps families manage expectations and choose the right level of insurance coverage.

FAQs

Whole Life Insurance builds financial stability through fixed premiums, guaranteed cash value, and a tax-free death benefit. Its structure provides lifelong coverage, allowing Canadians to plan confidently for their family’s future. Over time, the policy’s cash value growth becomes a dependable reserve that strengthens overall financial security.

A Whole Life Insurance Policy in Canada helps cover estate taxes and ensures heirs receive a tax-free death benefit without delays or asset liquidation. Its guaranteed cash value and lifetime protection make it a strategic cornerstone of financial planning, preserving wealth across generations while maintaining liquidity in the estate.

Yes. The cash value component of a Whole Life Insurance Policy can be accessed later in life to supplement retirement income. Because it grows tax deferred, Canadians can tap into this guaranteed cash during slower investment periods—providing flexibility that Term Life Insurance simply doesn’t offer.

Both are Permanent Life Insurance options, but whole life focuses on guaranteed coverage and predictable cash value growth, while universal Life Insurance offers flexibility tied to market performance. Whole life prioritizes stability, making it ideal for clients seeking long-term financial security rather than variable investment returns.

The death benefit of Whole Life Insurance is typically tax-free, but the policy’s cash value may have tax implications if withdrawn above its adjusted cost basis. For estate strategies, this design helps maintain financial security and transfer wealth efficiently while minimizing exposure to capital gains or income tax.

Whole Life Insurance offers Permanent Coverage, building guaranteed cash value that grows over your lifetime. Term Life Insurance, on the other hand, expires after a set period and doesn’t accumulate any cash value. Canadians who want long-term financial security and predictable death benefits often choose whole life for its stability.

With fixed premiums, your payments never increase—even as you age or your health changes. This makes budgeting easier and supports consistent financial planning. Over decades, predictable costs combined with a growing cash value give families confidence that their Whole Life Insurance Policy will always stay affordable and reliable.

A well-designed Whole Life Insurance Policy in Canada can pass down a tax-free death benefit, creating a lasting financial legacy. Families use it to protect assets, pay estate taxes, and fund education or businesses for future generations. It’s more than insurance—it’s lifelong protection that keeps wealth flowing forward.

If you stop paying, most Permanent Life Insurance contracts offer options such as using your guaranteed cash to keep coverage active or converting to a paid-up policy. The policy won’t vanish instantly—but its cash value growth and death benefit may reduce. Always review options with an insurance advisor before deciding.

Absolutely. The death benefit of Whole Life Insurance can cover funeral costs and other final expenses, ensuring your family isn’t burdened during an emotional time. Because it’s a tax-free death benefit, every dollar paid to beneficiaries can go directly toward maintaining their financial security.

Each premium contributes to both insurance costs and a cash value accumulation fund that grows tax-deferred. Over time, this investment component compounds steadily, supported by the insurer’s financial performance. Clients often use it to supplement retirement income or access guaranteed cash when needed.

Yes, the best Whole Life Insurance for seniors prioritizes stability, guaranteed death benefits, and Permanent Coverage without market risk. Since premiums remain fixed, seniors can maintain affordable protection while ensuring a tax-free death benefit is passed to loved ones—ideal for estate planning or legacy creation.

An experienced insurance advisor helps tailor your Whole Life Insurance Policy to your goals, ensuring the right balance between cash value growth, tax advantages, and financial security. Our role is to simplify complex terms and design coverage that fits your lifestyle, business needs, and family priorities.

Some Participating Whole Life Policies allow dividends to reduce premiums or purchase paid-up additions, effectively lowering long-term costs. While Non-Participating options don’t share profits, they guarantee stable premiums for life—ensuring your financial plan stays predictable and manageable year after year.

Both offer tax advantages, but Whole Life Insurance focuses on guarantees, while universal life ties performance to investment returns. Whole life’s guaranteed cash value grows consistently, making it a reliable companion for tax planning and retirement strategies. It’s the stable counterpart in your financial future toolkit.

Paid-up additions (PUAs) are mini policies purchased with dividends in a Participating Whole Life Plan. They increase both cash value and the death benefit, enhancing long-term performance. Over time, PUA contribute to cash value accumulation and builds stronger financial security without requiring extra premium payments.

Sources and Further Reading

“What Is Participating Life Insurance Policy?” — Aflac : https://www.aflac.com/resources/life-insurance/what-is-a-participating-life-insurance-policy.aspx Aflac

“Understanding Whole Life Insurance in Canada: A Guide to …“ — Katsen Insurance (Canadian blog) : https://www.katseninsurance.com/blog-1/params/post/4987076/understanding-whole-life-insurance-in-canada-a-guide-to-participating-and-n katseninsurance.com

“What Is Cash Value in Life Insurance, And How Does It Work?” — Sun Life Financial : https://www.sunlife.ca/en/tools-and-resources/money-and-finances/understanding-life-insurance/cash-value-in-life-insurance-how-does-it-work/ Sun Life

“Whole Life Insurance in Canada” — RBC Insurance : https://www.rbcinsurance.com/en-ca/life-insurance/whole-life-insurance/ RBC Insurance

“Participating vs Non-Participating Whole Life Insurance [3 Key Differences]” — Insurance & Estates : https://www.insuranceandestates.com/participating-life-insurance/ I&E Banking Strategies

Key Takeaways

- A Whole Life Insurance Policy in Canada offers lifelong coverage, guaranteed premiums, and a tax-free death benefit that ensures predictable protection.

- Non-Participating Whole Life Insurance provides fixed growth and guaranteed cash value, ideal for those seeking stability and certainty.

- Participating Whole Life includes dividends that can enhance cash value but it depends on the insurer’s financial performance and market conditions.

- The cash value component grows tax deferred, offering flexibility to supplement retirement income or handle unexpected expenses.

- Whole Life Insurance serves as a powerful estate planning and generational wealth tool, covering estate taxes and ensuring the family’s financial future.

- Older participating policies may show reduced growth due to changing interest rates, but their guaranteed values and lifelong protection remain strong.

- Whole Life Insurance balances protection and savings, creating a reliable foundation for long-term financial stability and financial planning.

Feedback Questionnaire:

We’d love your input to help us understand your financial planning challenges and improve our future content. Please take a moment to share your thoughts below.

Thank you for sharing your feedback!

Your insights help us continue creating valuable, easy-to-understand financial education for Canadians planning their secure futures.

IN THIS ARTICLE

- The Predictability Advantage: How Whole Life Insurance Builds Lifelong Financial Stability In Canada

- Understanding Whole Life Insurance: The Foundation of Predictability

- The Predictability Factor: Why Non-Participating Whole Life Matters

- Participating Whole Life: Opportunity Meets Uncertainty

- Participating vs. Non-Participating: Understanding the Difference

- The Advisor’s Lens: Choosing the Right Plan

- Tax and Growth Considerations: Clearing Up Misconceptions

- Why Some Older Policies Aren’t Performing as Expected

- Whole Life Insurance for Seniors and Estate Planning

- Integrating Whole Life Into a Broader Financial Strategy

- Common Client Questions

- The Predictability Advantage: Why It Still Matters