- Connect with our licensed Canadian insurance advisors

- Schedule a Call

Basics

- What Is the Maturity Period of Term Insurance?

- Understanding the Uses of a Term Insurance Calculator

- What Is Underwriting in Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- How Do You Choose Term Insurance?

- Can You Cash Out a Term Life Insurance Policy?

Reviews

Common Inquiries

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- Joint Term Insurance VS. Two Separate Term Plans

- Understanding Joint Term Insurance Plans

- Understanding Separate Term Plans

- Comparing Costs: Joint vs. Separate Plans

- Flexibility and Customization

- Claims and Benefits

- Who Should Consider Joint Life Insurance Plans?

- Who Should Consider Separate Plans?

- The Role of Canadian LIC's Expertise

- Common Misconceptions

- Making the Decision

Joint Term Insurance VS. Two Separate Term Plans

By Pushpinder Puri

CEO & Founder

- 11 min read

- January 2nd, 2025

SUMMARY

The blog clarifies the differences that exist between Joint Term Life Insurance Plans and two Separate Term Life Insurance Plans. It shows the features, benefits, costs, flexibility, and how they suit different kinds of people. The blog further points out real-life examples, key decision factors, and how Canadian LIC brokers help clients compare their Term Life Insurance Quotes, buy Term Life Insurance online, and choose the right Term Life Insurance for their needs.

Introduction

Mostly, it is not easy for couples to make such a decision when selecting the Term Life Insurance Plan required by them. The dilemma normally comes in deciding whether one would go for a Joint Term Life Insurance Coverage or opt for two Separate Term Plans. In our best insurance brokerage, Canadian LIC, we constantly have clients who are in such dilemmas. It becomes easier to get overwhelmed with scenarios such as full coverage of needs, costs of gathering such info, and even understanding of terms. Let’s break it down a little more to help you make the right decision for your own case.

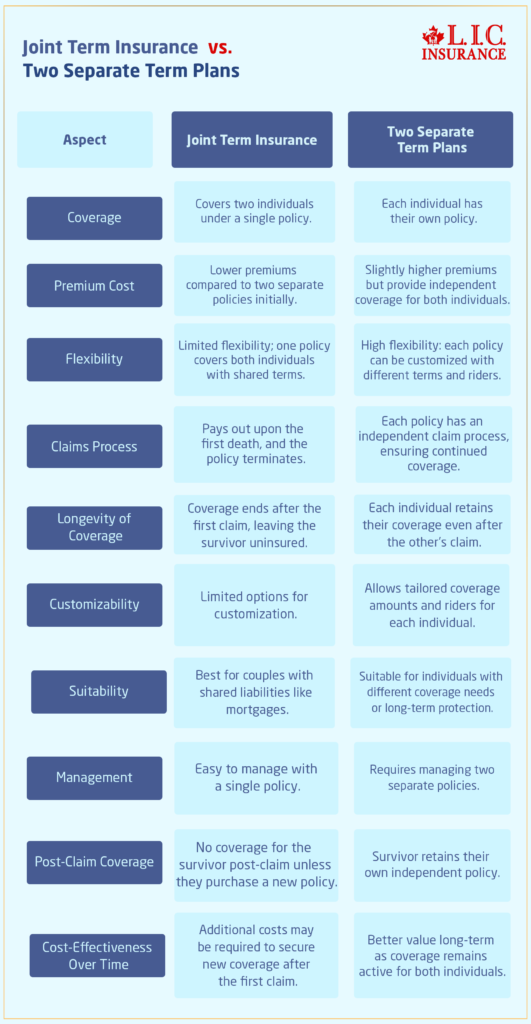

Understanding Joint Term Insurance Plans

It’s a Term Life Insurance in Canada for two people, usually spouses or partners, that is put under one policy. Its main objective is to deliver a death benefit to the surviving partner or beneficiaries when the insured person dies.

Key Features of Health Insurance

- Single Premium Payment: Both individuals are covered under a Term Life Insurance Plan, which requires only one premium payment.

- First Death Payout: Most joint policies payout upon the death of one insured individual, with this ending the policy.

- Cost-Effectiveness: Joint policy will probably cost less than if two plans were undertaken.

- Simplified Management: Having just one policy to manage reduces administrative complexity.

Understanding Separate Term Plans

On the other hand, two Separate Term Plans involve purchasing individual policies for each person. These policies operate independently and offer unique benefits for each policyholder.

Key Features of Separate Term Plans:

- Independent Coverage: Every policyholder has his own coverage amount and terms.

- Flexibility: Policies may be adjusted according to needs.

- Greater Overall Coverage: A higher total coverage can be obtained with two policies.

- Survivor Protection: If one policyholder passes away, the surviving partner is still covered.

Comparing Costs: Joint vs. Separate Plans

Discussing Term Life Insurance Quotes often revolves around cost. In our experience at Canadian LIC, many clients assume that Joint Plans are always cheaper. Though this may be true initially, long-term implications are important to consider.

Cost Analysis:

- Joint Plans: In general, a Joint Life Insurance Coverage premium will cost less than two individual policies added together. At the time of the first death, the policy automatically terminates, and the survivor goes uncovered unless they buy another policy that may be significantly higher because of age and possibly changed health.

- Separate Plans: These are a bit costlier at the outset but ensure that each individual will be covered independently in the event of one’s demise.

Canadian LIC’s Perspective:

We had another couple, Alex and Priya, come to seek our advice. They were newlywed and wanted affordable coverage. Their initial preference was for the joint policy because it carried lower premiums. However, after discussing the long-term benefit of Separate Policies, they opted for individual plans to ensure proper and long-lasting coverage for them. This approach allowed Priya to have her peace of mind, knowing she would be covered no matter what the future holds.

Flexibility and Customization

Individual Life Insurance Plans offer unparalleled flexibility. Each policyholder can choose coverage amounts, term lengths, and riders that suit their unique needs.

Flexibility in Action:

- Riders and Add-ons: Under the two different plans, a person can add a critical illness rider, whereas another can opt for a waiver of a premium rider.

- Tailored Terms: For example, if one of the spouses is an entrepreneur, then he may require a higher coverage level than his working spouse.

The Joint Plan Trade-Off:

Joint Plans offer less room for customization. Since the coverage is shared, options are limited to what works for both individuals as a unit.

Claims and Benefits

A major distinction between joint and Separate Plans arises at the time of filing claims.

Claims in Joint Plans:

Joint policies typically pay out at the first death, and the policy is then closed. This can leave the surviving spouse without coverage, which only serves to add to the difficulty of the situation.

Claims in Separate Plans:

Each policy has its own separate life. If one of the policyholders dies, the survivor’s coverage remains in effect, providing ongoing protection for dependents or liabilities.

Real Client Experiences:

Ravi, a client, shared his story of how, even after his wife’s passing, the Separate Policy paid for his family’s sake. If he had taken it as a Joint Plan, there would have been a blank cheque for him at a later stage of life when that was required to be covered by the plan.

Who Should Consider Joint Life Insurance Plans?

Joint Term Life Insurance Plans work well for:

- Joint Term Life Plans: These plans are very effective for couples with tight budgets who may find them attractive due to lower premiums.

- Newlyweds or Young Families: Newlywed couples or young families, perhaps, will need simplicity and affordability.

- Temporary Needs: If coverage is needed for a particular shared liability, such as a mortgage, Joint Plans can be sensible.

Who Should Consider Separate Plans?

Separate Term Plans are best suited for:

- People with Special Needs: When every person has different needs for terms or coverage levels.

- Long-term Security Seekers: Those who need protection that will continue indefinitely in case one of the covered individuals dies.

- Flexibility Enthusiasts: If you would like to customize your policy, Separate Plans are the way to go.

The Role of Canadian LIC's Expertise

It doesn’t have to be an alarming process where people have to compare between Joint Term Insurance and Separate Plans. Canadian LIC, the best insurance brokerage, has made it easy by providing personalized guidance. We compare Term Life Insurance Quotes and help you buy Term Life Insurance online. We connect you with experienced Term Life Insurance Brokers who completely understand what you need.

Why Clients Trust Canadian LIC:

- Expert Guidance: We have helped numerous couples find the best policies to fit their circumstances.

- Transparent Comparisons: Our agents make sure you know the good and bad of each option.

- Ongoing Support: Whether it’s purchasing a policy, updating it, or filing a claim, we’re here every step of the way.

Common Misconceptions

Joint Plans are Always Cheaper:

While joint policies may have lower premiums, they can cost more in the long run if additional coverage is needed later.

Separate Plans are Complicated:

With the right broker, managing two policies is straightforward. Canadian LIC ensures seamless policy management for clients.

Making the Decision

When choosing between Joint Term Insurance and two Separate Term Plans, it’s important to:

- Evaluate your present and future financial requirements.

- Consider the flexibility and independence you require.

- Review how a potential claim may impact long-term coverage.

Joint Term Insurance vs. Two Separate Term Plans

Wrapping Up

No decision is a one-size-fits-all when it comes to choosing between a Joint Term Life Insurance Plan and two Separate Term Plans. There are always strengths to the option and situations where the other will be more favourable. The Canadian LIC team recognizes the different challenges couples experience when choosing between these two options. With our assistance, you’ll be able to get that Term Life Insurance Policy that you need and enjoy long-lasting protection with peace of mind. No more waiting around— contact us today for Term Life Insurance Quotes, buy Term Life Insurance online, or get in touch with Term Life Insurance Brokers. The right coverage is just one step away.

More on Term Life Insurance

- Why Are Term Life Insurance Claims Rejected

- What Type Of Risk Is Covered By Short Term Insurance?

- What Happens If You Can’t Pay Your Term Life Insurance?

- What Will Disqualify You From Term Life Insurance?

- Can Riders Be Added To Term Life Insurance?

- Why Buy Term Life Insurance From An Insurance Broker?

- Why Not Buy Term Life Insurance From Banks?

- What Is The Difference Between Term Insurance And Group Term Insurance?

- Is There 10-Year Term Life Insurance?

- Does the Term Life Cover Accidental Death?

- Is Buying a Term Plan Online Safe?

- When Does Term Life Insurance Payout?

- Who Should Not Get Term Life Insurance?

- What Is the Maximum Limit in Term Insurance?

- What Are the 4 Types of Term Life Insurance?

- Can a Child Be the Owner of a Term Life Insurance Policy?

- Which Is Better, Term Insurance or SIP?

- What types of death are not covered in Term Insurance?

- Can I Pay Term Insurance Monthly?

- Pros and Cons of Buying Term Life Insurance Plans

- Can Term Life Insurance Be a Business Expense?

- What Happens When Term Life Insurance Expires?

- What Happens After 20 Years of Term Life Insurance?

- Can Term Life Insurance Be an Investment?

- Term Life Insurance Plan for All Age Groups

- What Does It Mean to Buy Term & Invest the Difference?

- How Do You Calculate Term Insurance Value?

- Why Is Term Life Insurance with a Return of Premium Option Not the Best Risk Coverage for You?

- Group Term Life Insurance & Individual Term Insurance: Know the Details

- What Is the Claim Period for Term Life Insurance?

- Can I Convert My Term Policy to Whole Life?

- Can You Use Term Life Insurance to Pay Off a Mortgage?

- Do Term Life Insurance Plans Offer Cash Value?

- What Happens to Term Insurance If the Nominee Dies?

- What Is the Shortest-Term Life Insurance Policy?

- What Is the Cheapest Term Life Insurance for Seniors Over 70?

- Who Benefits from Term Life Insurance?

- Can Term Insurance Be Rejected After Five Years?

- What Is the Longest Term Life Insurance?

- Does Term Insurance Automatically Renew?

- Can you extend a 20-Year Term Life Policy?

- Do I Get Money Back from Term Life Insurance?

- Can You Cash Out a Term Life Insurance Policy?

- Should Both Husband and Wife Get Term Life Insurance?

- What Is Underwriting in Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- What Is the Maturity Period of Term Insurance?

- Can I Purchase a Joint Term Life Insurance Policy or a Whole Life Insurance Policy?

- Best Term Life Insurance Companies in Canada: In-Depth Reviews & Essential Insights (2024)

- At What Age Should You Stop Buying Term Life Insurance?

- What are the advantages of Short Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- How Do You Choose Term Insurance?

- What’s the Longest Term Life Insurance You Can Get?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 844-542-4678 to speak to our advisors.

Get Quote Now

FAQs: Joint Term Insurance vs. Two Separate Term Plans

A Joint Term Life Insurance Plan is a single policy that covers two people, usually a couple. It pays out a death benefit when one person passes away, and the policy typically ends after that.

A Joint Term Life Insurance Policy is actually a single policy that covers two individuals, such as a married couple. The death benefit is paid if one of the individuals dies and generally terminates at that point.

The Joint Life Insurance Policy is usually cheaper upfront as it only requires one policy. However, Separate Term Life Insurance Policies may prove better in the long run as they will provide both people with individual coverage.

The Joint Term Life Insurance Plans have some limitations regarding customization because, under one policy, there are two people covered under the same terms. Separate Term Life Insurance Plans allow more flexibility, such as different coverage amounts or riders for each person.

Most Joint Plans pay the death benefit and then end. The surviving partner will need to buy a new policy, which might be more expensive due to age or health changes.

Yes, Separate Plans are more flexible. Each person can choose their coverage amount, term length, and additional riders like critical illness coverage or accidental death benefits.

Separate Term Life Insurance Plans provide better long-term security. They ensure both individuals have independent coverage, even if one passes away.

Yes, you can compare Term Life Insurance Quotes for both joint and Separate Plans. Canadian LIC’s brokers can help you review the options and find the best fit.

Absolutely. Many people choose to buy Term Life Insurance online for convenience. Canadian LIC makes the process simple and helps you understand all your options.

Joint Plans are very good for couples on tight budgets who do not wish to have complicated coverage. They might not be very ideal if you want each partner to have independent and permanent coverage.

We make customized approaches to our clients so they can trust the Canadian LIC. We guide the comparison of options, clearly explain terms, and help find the right Term Life Insurance Plan to meet the requirements of each individual.

You can contact Canadian LIC’s experienced Term Life Insurance Brokers to discuss your options. They will guide you through the process and help you make an informed choice.

If you have children, Separate Term Life Insurance Plans might be better. They ensure continued coverage for the surviving partner, providing more stability for your family.

Switching can be challenging and may involve higher premiums. It’s best to carefully consider your needs before choosing a Joint Plan.

Consider your budget, long-term needs, and the level of flexibility you want. Speaking with a knowledgeable Term Life Insurance broker can help clarify which option suits you better.

Yes, many Life Insurance Companies in Canada offer Joint Term Life Insurance Plans. Canadian LIC can help you find the right plan and compare it to separate options.

With Canadian LIC, the process is streamlined. Whether you’re buying a Joint Plan or two Separate Plans, our brokers work to ensure you get covered as quickly as possible.

Adding riders to a Joint Plan depends on the provider. Separate Plans, however, offer more options for individual riders.

Most brokers, including Canadian LICs, earn commissions from the insurance providers. This means you get expert advice at no extra cost to you.

Think about your current and future needs, including dependents, financial goals, and budget. Canadian LIC’s brokers can help you assess your situation and guide you toward the best decision.

Most Joint Term Life Insurance Policies don’t permit changing coverage amounts once the policy begins. With separate term policies, however, you can typically modify the coverage to match the fluctuating needs in your life.

The payout of a Joint Term Life Insurance Plan is tax-free to the beneficiary, just like a Single Life Insurance Policy. However, there are specific tax implications in certain cases; that is when Canadian LIC’s brokers are present to make everything understandable.

It is sometimes difficult to deal with a Joint Term Life Insurance Policy if a relationship ends. Some policies have a split option, while others do not. A Separate Term Life Insurance avoids the issue altogether since every policy is independent.

Brokers at Canadian LIC work on your choice by explaining the pros and cons of each Term Life Insurance option; you’ll save time comparing Term Life Insurance Quotes and choosing the best Term Life Insurance Plan that fulfills your particular requirements.

No, Joint Term Life Insurance Plans can also cover common-law partners or business partners. Discuss your situation with a broker to see if this option works for you.

Some Joint Term Life Insurance Plans offer the option to convert to a Permanent Policy. Check with your provider or broker to see if this is available.

While Separate Plans may cost more initially, they often provide better value over time because they ensure individual coverage for both partners, even if one passes away.

Choose a Term Life Insurance Plan with adequate coverage for your family’s financial needs. Canadian LIC’s brokers can help you calculate the right coverage and find affordable options.

Many providers offer discounts for buying Term Life Insurance online. Canadian LIC’s brokers can guide you to these savings and help you find the best deals.

With Joint Plans, claims are processed after the first death, and the policy ends. With Separate Plans, each policy has a separate claims process, where the survivor continues to remain covered.

Joint Term Life Insurance typically covers two individuals. For multiple people, separate policies or a group insurance plan may be more appropriate.

Eligibility depends on factors like age, health, and your relationship with the other insured person. Brokers at Canadian LIC can guide you through the requirements and application process.

Most providers have age limits for Joint Term Life Insurance Plans. Discuss with a broker to understand the options available for your age group.

Riders like accidental death benefits or critical illness coverage are often limited in Joint Plans. Separate Policies usually allow riders to customize their rides more.

Renewing a Joint Term Life Insurance Plan depends on the provider. Some policies automatically renew, while others require reapplication. Canadian LIC’s brokers can assist with renewal details.

Yes, brokers at Canadian LIC can help you compare Term Life Insurance Quotes for both options. This helps you make an informed decision.

If one of the partners has medical issues, then Separate Term Plans might be the most suitable. This way, each of the partners can make the coverage their own without affecting the other’s policy.

Joint Plans are easier to manage because there is only one policy. However, this simplicity may come at the cost of reduced flexibility compared to Separate Plans.

But that is not all; Canadian LIC’s insurance brokers help you buy Term Insurance online or through a more streamlined process, ensuring the best policy for your needs.

Determine the family’s needs, from debts to future and income replacements, for them to spend. Brokers from the Canadian LIC would be there to assist in developing the necessary coverage.

Sources and Further Reading

Canadian Life and Health Insurance Association (CLHIA)

Website: https://www.clhia.ca

Explore detailed information about life insurance products and industry standards in Canada.

Government of Canada – Life Insurance Basics

Website: https://www.canada.ca/en/financial-consumer-agency

Provides guidance on understanding life insurance and choosing the right coverage.

Insurance Bureau of Canada (IBC)

Website: https://www.ibc.ca

Offers resources to help consumers make informed decisions about insurance policies.

Insureye Consumer Insurance Reviews

Website: https://insureye.com

A platform for insurance reviews and insights, helping consumers compare options effectively.

Sun Life Canada – Term Life Insurance

Website: https://www.sunlife.ca

Learn about Term Life Insurance Plans and their benefits from a leading Canadian provider.

Manulife Canada – Life Insurance Options

Website: https://www.manulife.ca

Offers in-depth resources on term and permanent life insurance policies in Canada.

TD Insurance – Life Insurance Basics

Website: https://www.tdinsurance.com

Provides clear explanations about Term Life Insurance Plans and coverage options.

Key Takeaways

- Joint Term Life Insurance Plans: These are single policies covering two people, offering lower initial premiums but ending after the first death, leaving the survivor uninsured.

- Separate Term Life Insurance Plans: These provide independent coverage for each partner, ensuring flexibility and long-term protection even if one policyholder passes away.

- Cost Considerations: Joint Plans are more affordable upfront but may require additional coverage later. Separate Plans are slightly costlier but offer better individual security.

- Flexibility: Separate Plans allow for customization of coverage amounts, term lengths, and riders, while Joint Plans have limited options.

- Claims Process: Joint Plans terminate after the first claim, whereas Separate Plans continue, ensuring coverage for the surviving partner.

- Expert Assistance: Canadian LIC brokers help clients compare Term Life Insurance Quotes, evaluate options, and buy Term Life Insurance online to suit their unique needs.

Your Feedback Is Very Important To Us

We value your feedback! This short questionnaire will help us understand your struggles when choosing between Joint Term Insurance and two Separate Term Plans. Please fill in your details and answer the questions honestly. Your input will help us improve our guidance and services.

Thank you for sharing your feedback! Your insights are invaluable to us.

IN THIS ARTICLE

- Joint Term Insurance VS. Two Separate Term Plans

- Understanding Joint Term Insurance Plans

- Understanding Separate Term Plans

- Comparing Costs: Joint vs. Separate Plans

- Flexibility and Customization

- Claims and Benefits

- Who Should Consider Joint Life Insurance Plans?

- Who Should Consider Separate Plans?

- The Role of Canadian LIC's Expertise

- Common Misconceptions

- Making the Decision

Sign-in to CanadianLIC

Verify OTP