- Connect with our licensed Canadian insurance advisors

- Schedule a Call

Basics

- What Is the Maturity Period of Term Insurance?

- Understanding the Uses of a Term Insurance Calculator

- What Is Underwriting in Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- How Do You Choose Term Insurance?

- Can You Cash Out a Term Life Insurance Policy?

Reviews

Common Inquiries

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What Happens When Term Life Insurance Expires?

- Options After Expiry

- Consider Final Expense Insurance

- Do You Still Need Life Insurance?

- Key Takeaways

- When Does Term Life Insurance Payout?

- When Does Term Life Insurance Start?

- What Happens When the Life Insurance Term Ends?

- When Should You Stop Term Life Insurance?

- More on Term Life Insurance

What Happens When Term Life Insurance Expires?

By Pushpinder Puri

CEO & Founder

- 11 min read

- November 19th, 2024

SUMMARY

Term Life Insurance is one of the most popular choices for many people because it’s simple and relatively cheap. The Term Life Insurance financial protection is provided for a particular period, which varies from 10 to 50 years. At the end of the term, it is typically here when they are at a crossroads. Questions arise: Do I still need coverage? Shall I renew, convert, or acquire a new plan? These are some of the common problems we encounter at Canadian LIC, as we advise different people every day on such issues. Let’s address these points so that you can make the right decisions regarding your Term Life Insurance Plan.

Options After Expiry

Your coverage is terminated at the Term Life Insurance maturity date. No death benefit is paid, except if your policy includes special features, such as a Return-of-Premium (ROP) Rider. These are your choices:

Renew Coverage

Many Term Life Insurance Plans offer the option to renew coverage yearly, even after the original term ends.

- How it Works: You don’t have to undergo a new medical exam to renew again. The premiums, however, will be higher because it is re-computed based on your age at that time.

- Who It’s For: It is ideal for those who have developed health problems that might make it hard to obtain a new insurance policy. While the premiums are bound to increase annually, it certainly allows for their continued coverage.

- Key Considerations: The clients are mostly prone to high premium upgrades when their renewal period comes. If affordability becomes a concern, one should seek alternative Life Insurance options, either by converting or purchasing a new policy.

Convert to Permanent Insurance

If your policy includes a conversion rider, you can switch from Term to Permanent Coverage, such as Whole Life Insurance or Universal Life Insurance, without a medical exam.

- Why Invest?: Permanent Policies provide lifetime coverage and include a cash value component; therefore, they are more suited for individuals who require longer-term financial security or those who would like to build long-term savings.

- Who It’s For?: This is helpful in situations where an individual has long-term dependents, such as a child with special needs, or in cases where a person wants to leave a legacy that will help future generations.

- Know This: Converting usually costs more, but a few insurers- most of which our team at Canadian LIC has worked with- permit partial conversions. That is, you can take half of a $500,000 Term Policy and convert it to Permanent Policy so both your coverage needs are met, and it is not too expensive.

Buy a New Policy

If you are healthy and relatively young, purchasing a new Term Life Insurance Plan can be an affordable and effective solution.

- Benefits of a New Policy: Starting fresh allows you to customize your coverage according to your current needs. For example, a shorter term and a lower death benefit might suffice if your children are nearing financial independence.

- Challenges: A new policy requires a medical exam, and premiums will reflect your age and any health changes since your original policy. We’ve helped many clients in their 40s and 50s find affordable Term Life Insurance Quotes despite these factors.

Consider Final Expense Insurance

For those seeking minimal coverage, such as for funeral expenses, final expense insurance is a viable choice.

- How It Works: These are smaller Whole Life Policies, typically offering payouts of $10,000 to $25,000, and they often don’t require a medical exam.

- Who It’s For: Older adults or individuals with significant health issues may find this option suitable.

- Why Choose It? While not a substitute for income replacement, it can ease the financial burden on loved ones during a difficult time.

Do You Still Need Life Insurance?

The decision to extend or replace your Term Life Insurance hinges on your current financial responsibilities and future goals. Here’s how to evaluate your needs:

You Might Need Life Insurance If:

- Dependents Rely on Your Income: If your children or spouse depend on your earnings for living expenses, maintaining coverage ensures their financial stability.

- Outstanding Debts Remain: A mortgage, car loan, or other significant debts can become burdensome for your family without insurance.

- Business Obligations Exist: Entrepreneurs often use life insurance to secure business loans or ensure smooth succession planning.

- Special Needs Dependents Require Support: For a dependent who will always need financial care, insurance provides long-term security.

- You Want to Leave a Legacy: Life insurance can help cover estate taxes or provide an inheritance for your heirs.

You May Not Need Life Insurance If:

- Dependents Are Financially Independent: If your children are self-sufficient, your need for coverage diminishes.

- Debts Are Paid Off: With no major liabilities, you may not require additional protection.

- Retirement Savings Are Adequate: If you and your spouse have enough savings to sustain your lifestyle, the need for life insurance decreases.

- Your Spouse Is Financially Stable: A spouse who is financially secure may not need life insurance proceeds to maintain their standard of living.

Key Takeaways

When planning for the expiration of your Term Life Insurance, these strategies can guide your decision-making:

Renewability and Conversion Options

Ensure your policy includes features like guaranteed renewability and conversion riders at the time of purchase. These options offer flexibility and can safeguard your coverage when health issues arise.

Permanent vs. Term Policies

While Term Life Insurance is more affordable, permanent policies provide lifelong coverage and build cash value. The choice depends on your financial priorities and long-term needs.

Evaluate Your Needs

Assess your financial situation regularly to determine if extending or replacing your Term Life Insurance is necessary. Consulting with Canadian LIC’s experienced advisors can simplify this process.

When Does Term Life Insurance Payout?

Term Life Insurance pays a death benefit when a policyholder dies while the policy is still in effect. This tax-free money is distributed to the people the insured has named as beneficiaries of the policy. It can be used for several reasons, including paying off debts, covering living expenses, and funding children’s education.

When Does Term Life Insurance Start?

Term Life Insurance Coverage becomes effective only after the application is approved, the policy is issued, and the first premium payment is made. Some policies provide for temporary coverage while the application is being processed.

What Happens When the Life Insurance Term Ends?

The term ends, the policy expires, and consequently, coverage ceases. If no further features, like renewability or conversion riders, are activated at the end of the term, the insurer retains the premiums, and no payout is made.

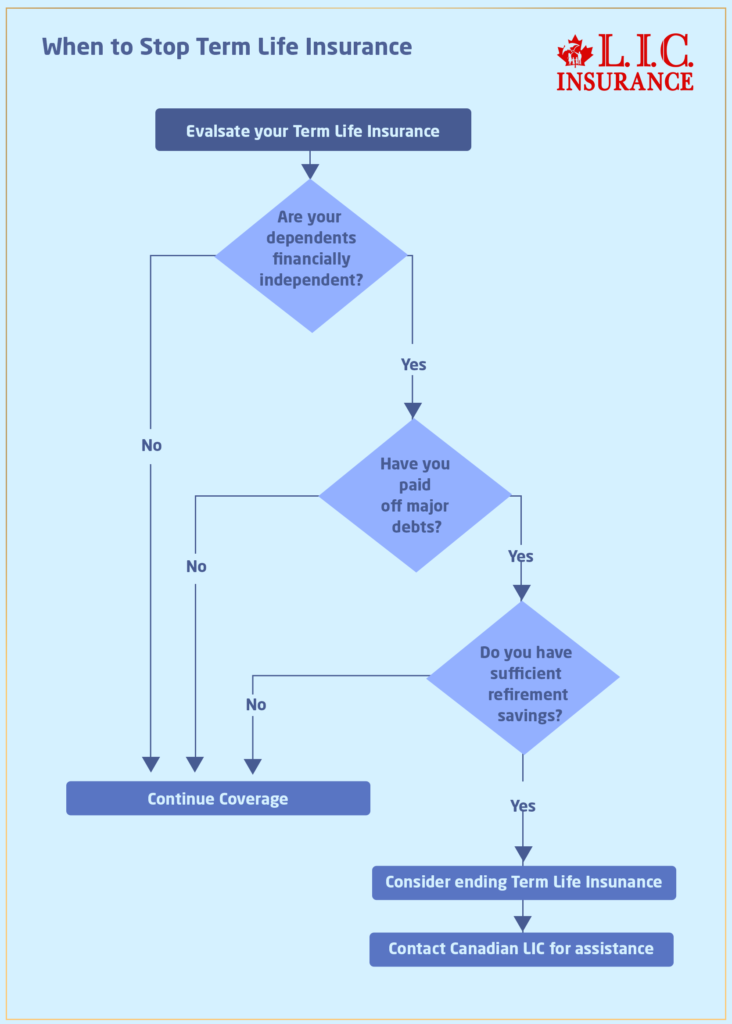

When Should You Stop Term Life Insurance?

Consider ending your Term Life Insurance if your financial situation no longer warrants coverage. Examples include:

- Dependents achieving financial independence.

- Paying off major debts like a mortgage.

- Amassing sufficient retirement savings.

Taking action today gives the chance of peace of mind tomorrow. Reach Out to Canadian LIC – the best insurance brokerage-for the most appropriate Term Life Insurance Plan that suits your unique needs. Compare the best Term Life Insurance Quotes, check eligibility for Term Life Insurance, and buy Term Life Insurance online with the guidance of advisors, who, above everything else, work for the financial security of your family.

More on Term Life Insurance

- Term Life Insurance Plan for All Age Groups

- What Does It Mean to Buy Term & Invest the Difference?

- How Do You Calculate Term Insurance Value?

- Why Is Term Life Insurance with a Return of Premium Option Not the Best Risk Coverage for You?

- Group Term Life Insurance & Individual Term Insurance: Know the Details

- What Is the Claim Period for Term Life Insurance?

- Can I Convert My Term Policy to Whole Life?

- Can You Use Term Life Insurance to Pay Off a Mortgage?

- Do Term Life Insurance Plans Offer Cash Value?

- What Happens to Term Insurance If the Nominee Dies?

- What Is the Shortest-Term Life Insurance Policy?

- What Is the Cheapest Term Life Insurance for Seniors Over 70?

- Who Benefits from Term Life Insurance?

- Can Term Insurance Be Rejected After Five Years?

- What Is the Longest Term Life Insurance?

- Does Term Insurance Automatically Renew?

- Can you extend a 20-Year Term Life Policy?

- Do I Get Money Back from Term Life Insurance?

- Can You Cash Out a Term Life Insurance Policy?

- Should Both Husband and Wife Get Term Life Insurance?

- What Is Underwriting in Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- What Is the Maturity Period of Term Insurance?

- Can I Purchase a Joint Term Life Insurance Policy or a Whole Life Insurance Policy?

- Best Term Life Insurance Companies in Canada: In-Depth Reviews & Essential Insights (2024)

- At What Age Should You Stop Buying Term Life Insurance?

- What are the advantages of Short Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- How Do You Choose Term Insurance?

- What’s the Longest Term Life Insurance You Can Get?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 844-542-4678 to speak to our advisors.

Get Quote Now

FAQs on What Happens When Term Life Insurance Expires

Term Life Insurance Eligibility depends on several factors including the age, health, and income level of the individual. Canadian LIC helps thousands of clients overcome their anxiety about the eligibility conditions. Most insurers consider applications from people ranging in age from 18 to 70 years. A medical test or health questionnaire is usually necessary, yet even those with minimum health problems are able to qualify.

Term Life Insurance Investments are nothing like traditional savings or market investments. Its true focus is to protect the future of your family through a certain death benefit. The clients often tell us at Canadian LIC that they initially thought term insurance would grow like savings, whereas it would act as an area of a financial safety net during working years when dependents rely on your income.

Getting term life quotes is very easy. Clients can get quotes online on our site or through one of our agents. Most of the clients we work with end up feeling overwhelmed by the variety, but we will walk them step-by-step through comparisons of quotes and find the best plan for their budget.

Buying Term Life Insurance can easily be done online, but any advisor would give you personal service. For many of our clients, it is essential to discuss their needs with us first, especially when they have questions about the long-term financial security of their family. We help you choose the right coverage amount and term length.

When a Term Life Insurance Plan expires, coverage ends, and no death benefit is paid. However, you can often renew your policy, convert it to Permanent Life Insurance Policies, or purchase a new term plan. At Canadian LIC, we’ve helped many clients explore these options, especially those concerned about protecting dependents after the policy ends.

However, most Term Life Insurance Policies are renewable without medical exams. Premiums do go up with age, which is very often a concern for clients when costs are rising; we work out for them if renewal, conversion, or a new policy best serves their interest.

Permanent Life Insurance Policy is appropriate when you want lifetime coverage or continuing financial obligations. Many clients have dependents or estate plans and find this valuable. It costs more, but there are many more benefits to permanent policies, including cash value.

For a healthy individual, we allow investing in a completely fresh Term Life Insurance Plan. New plans for younger clients will seem rather inexpensive; older clients will have to pay much more of a premium. We at Canadian LIC guide our clients to obtain the best plan suited at their age and financial condition at present.

Basic term life does not refund premiums. However, some plans offer the return-of-premium feature. This could be used at Canadian LIC, we have seen clients add this feature for peace of mind, although it increases your premium. Good option if you want some cash back after the term has ended.

Coverage depends on your financial goals. Consider your income, debts, and family’s future needs. Many clients at Canadian LIC choose 10x their annual income to ensure dependents are secure. We help calculate the right amount based on your unique situation.

Yes. Most insurers now offer coverage up to age 80. Premiums will be higher, but alternative products like reduced death benefits can help keep costs in check. We have had clients at Canadian LIC who wanted to make sure that, if they die, their family or final expenses will be taken care of.

Final expense insurance covers small costs like funerals very well. It’s ideal for someone who no longer needs significant coverage. Quite often, many older clients we work with find it a simple way to ease financial burdens on loved ones.

Most Term Life Insurance Plans offer add-ons, such as converting to permanent insurance or increasing coverage during key life stages. We get many requests from clients to adjust their existing plans as a result of experiencing major life events, and we facilitate changes that best fit their needs.

Term Life Insurance covers for a specified period, such as years or decades, but permanent insurance can be carried beyond one’s whole lifetime. The term is cheaper but doesn’t accumulate any cash value, whereas permanent insurance is more expensive but provides lifetime coverage and a savings component. We advise our clients at Canadian LIC concerning which would better suit their objectives.

Term insurance is cheaper because it covers a person for a particular period of time and does not provide any cash value. Many clients regard it as the cheapest means of securing their family’s future. Our advisors at Canadian LIC help our clients get the maximum coverage according to their budget.

Sources and Further Reading

When your Term Life Insurance policy expires, your coverage ends, and no death benefit is paid out. However, you have several options to consider:

Renew Coverage: Many term policies allow for yearly renewals without requiring a medical exam. Be aware that premiums will increase with age.

Convert to Permanent Insurance: If your policy includes a conversion option, you can switch to permanent coverage without undergoing medical underwriting. Permanent policies, such as whole or universal life insurance, offer lifetime coverage and may accumulate cash value, but they are generally more expensive.

Buy a New Policy: If you’re in good health, purchasing a new term policy might be cost-effective. Keep in mind that premiums may be higher due to increased age and any health changes.

Consider Final Expense Insurance: For minimal coverage, such as funeral costs, final expense insurance is an option, especially for older adults or those with health issues.

Key Takeaways

- Renewal Options:

Many Term Life Insurance Plans allow renewals without a medical exam, but premiums increase with age. This is helpful if you still need coverage but face health challenges.

- Convertibility:

If your policy includes a conversion rider, you can switch to permanent insurance for lifetime coverage and added benefits like cash value. This option avoids new underwriting but comes with higher premiums.

- Purchasing a New Policy:

Younger, healthy individuals may find it cost-effective to buy a new Term Life Insurance Plan. However, premiums may reflect any health changes and increased age.

- Final Expense Coverage:

Older adults or those with fewer financial obligations can consider final expense insurance to cover funeral or minimal expenses.

- Evaluate Your Need for Insurance:

Life insurance remains essential if you have dependents, debts, or long-term responsibilities. If you’re debt-free, financially secure, and without dependents, additional coverage may no longer be necessary.

- Plan Proactively:

Assess your policy’s features, such as renewability or conversion options, at the time of purchase. This foresight ensures smoother transitions when your term expires.

- Seek Guidance:

Consulting with experienced advisors at Canadian LIC can help tailor a solution based on your unique circumstances, ensuring you and your family remain protected.

Your Feedback Is Very Important To Us

We value your insights to help us better address your concerns and challenges. Please take a few moments to share your experiences.

Thank you for your input! Your responses will help us address the real struggles Canadians face with Term Life Insurance and provide tailored solutions.

IN THIS ARTICLE

- What Happens When Term Life Insurance Expires?

- Options After Expiry

- Consider Final Expense Insurance

- Do You Still Need Life Insurance?

- Key Takeaways

- When Does Term Life Insurance Payout?

- When Does Term Life Insurance Start?

- What Happens When the Life Insurance Term Ends?

- When Should You Stop Term Life Insurance?

- More on Term Life Insurance

Sign-in to CanadianLIC

Verify OTP