- Connect with our licensed Canadian insurance advisors

- Schedule a Call

Basics

- What Is the Maturity Period of Term Insurance?

- Understanding the Uses of a Term Insurance Calculator

- What Is Underwriting in Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- How Do You Choose Term Insurance?

- Can You Cash Out a Term Life Insurance Policy?

Reviews

Common Inquiries

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What Are the 4 Types of Term Life Insurance?

- Understanding Term Life Insurance and Its Importance

- Why is it important to explore different types of Term Life Insurance?

- Type 1: Level Term Life Insurance

- Type 2: Decreasing Term Life Insurance

- Type 3: Renewable Term Life Insurance

- Type 4: Convertible Term Life Insurance

- Comparing the Four Types of Term Life Insurance

- Factors to Consider When Choosing Term Life Insurance

- Canadian LIC's Approach to Helping Clients

What Are The 4 Types Of Term Life Insurance?

By Harpreet Puri

CEO & Founder

- 11 min read

- December 2nd, 2024

SUMMARY

Choosing the right Term Life Insurance Plan can feel overwhelming, especially when faced with different types of policies and varying rates. Many just wonder which of these will serve their requirements or if that certain policy would make a secure future for their family members, all fitting into their budget. These, and many others, are the kinds of challenges Canadian LIC’s clients witness daily. Knowing the four types of Term Life Insurance can clear the confusion, thus allowing you to provide for your loved ones.

Understanding Term Life Insurance and Its Importance

Term Life Insurance gives financial protection for a given period. This type of policy does not run a lifetime, unlike Permanent Policy, but it runs for a certain number of years. Its cost and simplicity have made it very popular with clients seeking simple cover.

Why is it important to explore different types of Term Life Insurance?

Because everyone’s situation is unique. Some individuals prioritize affordability, while others seek comprehensive coverage tailored to their long-term goals. Canadian LIC often guides clients through these decisions, ensuring their Term Life Insurance Investments align with their priorities.

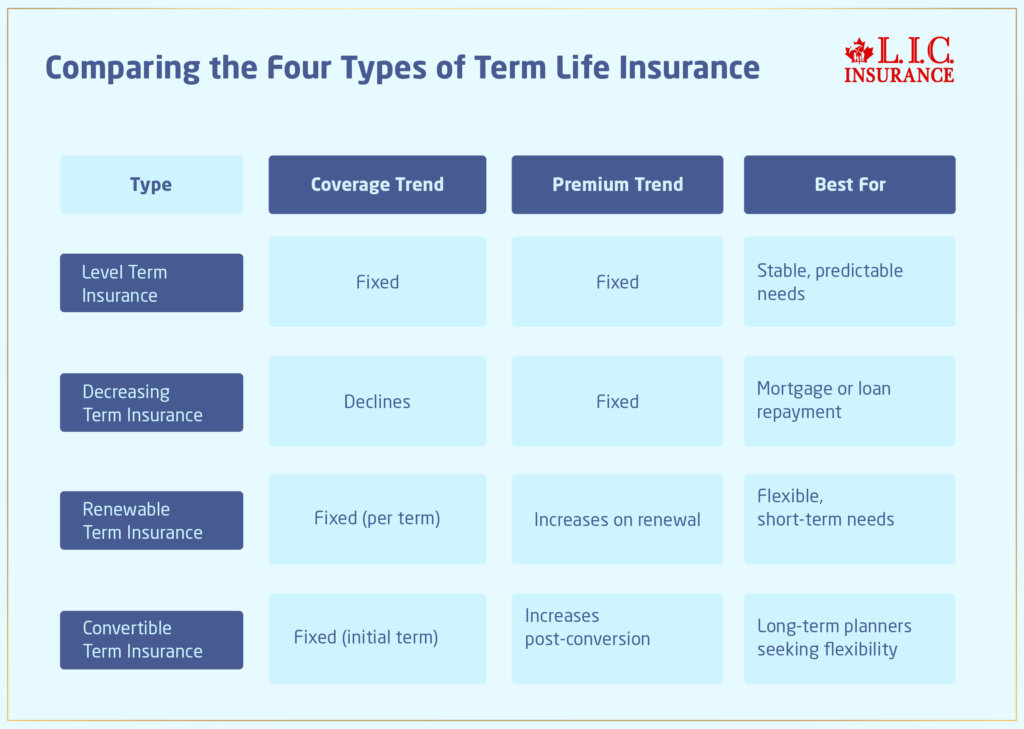

Type 1: Level Term Life Insurance

Level Term Life Insurance is one of the most common and straightforward options. The coverage amount and the premium payment will remain constant with this policy throughout the term. It is an excellent choice for people who want stability and predictability.

Who benefits most from Level Term Life Insurance?

- Families with young children need consistent financial protection for a set period.

- Individuals with long-term financial obligations, such as a mortgage.

For example, a couple came to Canadian LIC worried about securing their children’s education costs if something were to happen to them. A Level Term Life Insurance Plan gave them peace of mind, knowing their kids’ future was secure, and they wouldn’t have to worry about fluctuating premiums.

Why consider Level Term Life Insurance?

- Predictable Term Life Insurance Rates.

- Reliable coverage for financial planning.

Type 2: Decreasing Term Life Insurance

Decreasing Term Life Insurance is designed for those individuals whose financial obligations decrease over time. The coverage amount decreases each year, which is usually aligned with a mortgage or loan repayment. However, the premium payments often stays the same.

Who benefits most from Decreasing Term Life Insurance?

- Homeowners who want their insurance to match their decreasing mortgage balance.

- Individuals are paying off large loans over a set period.

A recent Canadian LIC client successfully served a homeowner who wished to have his family pay off the mortgage if he died. A Decreasing Term Life Insurance was just what he needed, as his decreasing debt matched the financial protection it would give.

Why consider Decreasing Term Life Insurance?

- Tailored to specific financial obligations.

- Typically more affordable than Level Term Life Insurance.

Type 3: Renewable Term Life Insurance

The Term Life Insurance renewed without medical exams allows the insured person to continue his coverage, but his premium will rise on renewal as per his age at renewal.

Who benefits most from Renewable Term Life Insurance?

- Individuals are uncertain about their future insurance needs.

- People who want flexibility can extend their coverage without requalifying.

A client at Canadian LIC, not knowing how long she would need coverage, took a Renewable Term Life Insurance. When her initial term ended, she was allowed to renew her coverage smoothly, though at higher premiums, which she expected.

Why consider Renewable Term Life Insurance?

- Flexibility to extend coverage without additional medical exams.

- It is ideal for those anticipating changes in their life circumstances.

Type 4: Convertible Term Life Insurance

The Convertible Term Life Insurance option allows policyholders to convert their Term Policy into a Permanent Life Insurance Policy without requiring a medical examination. It is very convenient for people who may have long-term coverage needs in the future.

Who benefits most from Convertible Term Life Insurance?

- Young professionals who currently need affordable coverage but foresee long-term needs.

- Families who may later want to build cash value through Permanent Policies.

With this product, Canadian LIC worked with a young couple who actually started with convertible-Term Life Insurance. With the increasing needs of the family and changing financial objectives, the advantage is well appreciated, as it provides more options for securing their future along with additional benefits.

Why consider Convertible Term Life Insurance?

- Provides a bridge between short-term affordability and long-term security.

- Allows policyholders to adjust their coverage as their needs evolve.

Comparing the Four Types of Term Life Insurance

Factors to Consider When Choosing Term Life Insurance

When deciding on a Term Life Insurance Plan, it’s essential to evaluate your financial goals, family needs, and future plans. Here are a few considerations:

- Term Length: Choose a term that aligns with your financial obligations, such as a mortgage, children’s education, or retirement planning.

- Premium Affordability: Compare Term Life Insurance Rates to ensure you select a policy within your budget.

- Conversion Options: If you anticipate long-term insurance needs, prioritize policies with convertible features.

- Renewal Flexibility: Look for renewable options if you expect your needs to change over time.

Canadian LIC's Approach to Helping Clients

Canadian LIC has enabled many people and families to select Term Life Insurance Plans that best suit their conditions. With this understanding of each client’s goals and challenges, Canadian LIC makes sure that they invest in a plan that offers the right balance of affordability and coverage.

For example, a young entrepreneur approached a Canadian LIC agent as they were unsure how to secure their family’s future while managing their business expenses. After assessing his needs, Canadian LIC recommended a renewable and Convertible Term Life Insurance Policy, giving him both flexibility and peace of mind.

Why Term Life Insurance is a Smart Investment

Investing in Term Life Insurance is about protecting your loved ones and securing their future. Whether you’re paying off a mortgage, saving for your child’s education, or ensuring your family’s financial stability, Term Life Insurance provides an affordable and effective solution.

How can you make the most of your Term Life Insurance investment?

- Work with a trusted brokerage like Canadian LIC to compare policies.

- Assess your needs thoroughly and choose a term length that aligns with your goals.

- Regularly review your policy to ensure it continues to meet your evolving needs.

Act Today with Canadian LIC

Don’t make choosing the right Term Life Insurance Plan complicated for yourself. Canadian LIC simplifies the process by showing clients every step of the process so that they can choose confidently. Focusing on your needs, Canadian LIC provides Term Life Insurance Plans that protect and give you peace of mind.

Whether you’re ready to buy Term Life Insurance online or need expert advice, Canadian LIC is here to help. Take the first step today and secure your family’s future with a policy that fits your life perfectly.

More on Term Life Insurance

- Which Is Better, Term Insurance or SIP?

- What types of death are not covered in Term Insurance?

- Can I Pay Term Insurance Monthly?

- Pros and Cons of Buying Term Life Insurance Plans

- Can Term Life Insurance Be a Business Expense?

- What Happens When Term Life Insurance Expires?

- What Happens After 20 Years of Term Life Insurance?

- Can Term Life Insurance Be an Investment?

- Term Life Insurance Plan for All Age Groups

- What Does It Mean to Buy Term & Invest the Difference?

- How Do You Calculate Term Insurance Value?

- Why Is Term Life Insurance with a Return of Premium Option Not the Best Risk Coverage for You?

- Group Term Life Insurance & Individual Term Insurance: Know the Details

- What Is the Claim Period for Term Life Insurance?

- Can I Convert My Term Policy to Whole Life?

- Can You Use Term Life Insurance to Pay Off a Mortgage?

- Do Term Life Insurance Plans Offer Cash Value?

- What Happens to Term Insurance If the Nominee Dies?

- What Is the Shortest-Term Life Insurance Policy?

- What Is the Cheapest Term Life Insurance for Seniors Over 70?

- Who Benefits from Term Life Insurance?

- Can Term Insurance Be Rejected After Five Years?

- What Is the Longest Term Life Insurance?

- Does Term Insurance Automatically Renew?

- Can you extend a 20-Year Term Life Policy?

- Do I Get Money Back from Term Life Insurance?

- Can You Cash Out a Term Life Insurance Policy?

- Should Both Husband and Wife Get Term Life Insurance?

- What Is Underwriting in Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- What Is the Maturity Period of Term Insurance?

- Can I Purchase a Joint Term Life Insurance Policy or a Whole Life Insurance Policy?

- Best Term Life Insurance Companies in Canada: In-Depth Reviews & Essential Insights (2024)

- At What Age Should You Stop Buying Term Life Insurance?

- What are the advantages of Short Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- How Do You Choose Term Insurance?

- What’s the Longest Term Life Insurance You Can Get?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 844-542-4678 to speak to our advisors.

Get Quote Now

FAQs About the Four Types of Term Life Insurance

The four main types of Term Life Insurance Plans are:

- Level Term Life Insurance

- Decreasing Term Life Insurance

- Renewable Term Life Insurance

- Convertible Term Life Insurance

Each type is catered to specific needs; it may be predictable coverage, reducing debt obligations, flexible renewal, or transition to a Permanent Life Insurance Policy. Canadian LIC typically helps clients choose the right Term Life Insurance Plan based on their financial goals and family responsibilities.

Level Term Life Insurance has the most stable rates. The premiums remain constant for the entire term of the policy, which makes it easier for people to budget their payments. Most clients of Canadian LIC prefer Level Term Life Insurance because it is simple and predictable.

Yes, Decreasing Term Life Insurance is usually cheaper than other plans because the coverage amount decreases with time. Many Canadian LIC clients use this plan to match their declining financial obligations, such as mortgage payments, while keeping their Term Life Insurance Investments affordable.

Renewable Term Life Insurance provides you with an option to extend your coverage at the end of a term without requiring a medical exam. It is convenient for individuals who are unsure how long they will require their coverage. Canadian LIC often works with clients who value this flexibility, particularly as their family and financial circumstances change.

Homeowners often find Decreasing Term Life Insurance the best choice for them. The amount covered goes down with the mortgage balance. Canadian LIC often advises clients who wish to secure their families from mortgage debt in case something happens to take up this kind of insurance.

This is the most common choice for homeowners. The amount covered decreases with your mortgage balance. Canadian LIC usually advises this option to clients who wish to safeguard their families against mortgage debt in case of an unexpected event.

Renewable Term Life Insurance premiums are usually higher at the time of renewal since they are based on your age at renewal. Canadian LIC always advises clients to factor these increases into their considerations when making decisions about renewable policies.

Yes, you can buy Term Life online through the easy-to-use platform provided by Canadian LIC: lots of clients like that can easily compare Term Life Insurance Rates and choose a certain offer without visiting an office.

Term Life Insurance Investments offer cost-effective peace of mind protection for your family during any specific period. Though the investment does not create a cash value like Permanent Insurance, Term Life Insurance is a smart choice for a temporary financial obligation. Canadian LIC often recommends terms for young families and working professionals looking for affordable protection.

If you survive the Term Life Insurance Policy, it will lapse, and neither you nor your beneficiaries will get paid. You can then either renew, convert, or allow the coverage to lapse. Canadian LIC assists its clients in reviewing their options before the term lapses to ensure they remain covered.

Your term should agree with your financial obligations. For instance, if you have a 20-year mortgage, then a 20-year Term Life Insurance Plan ensures that period. Canadian LIC often works with clients, determining the best term length based on their goals and responsibilities.

Yes, if you have a Convertible Term Life Insurance Policy, you can convert to Permanent Coverage without a medical. Many of Canadian LIC’s clients come to this realization when their circumstances change regarding estate taxes or maintaining a legacy for family members.

Yes, your health will impact your Term Life Insurance Rates. People in good health tend to qualify for lower premiums. Canadian LIC helps clients understand how their medical history might affect their options and guides them toward the best plans.

Canadian LIC provides expert guidance to help clients compare Term Life Insurance Policies, find competitive rates, and make confident decisions. With years of experience, they ensure every policy is tailored to your needs.

This means that a lot of clients may need several policies to deal with various needs, like perhaps a level term policy with long-term obligations and a decreasing-term policy for mortgage protection. Canadian LIC regularly helps a client make their Term Life Insurance investment suitable for different financial circumstances.

Sources and Further Reading

- Investopedia: Term Life Insurance

This article provides an in-depth look at Term Life Insurance, including its types, benefits, and considerations.

Investopedia - MoneySense: Your Complete Guide to Life Insurance in Canada

This guide offers comprehensive information on various life insurance options available in Canada, helping you make informed decisions.

MoneySense - TD Insurance: Types of Life Insurance in Canada

TD Insurance explains the different types of life insurance policies they offer, including Term Life Insurance, to help you choose the right coverage.

TD Insurance - Canada Life: Main Types of Life Insurance

This resource outlines the primary types of life insurance available, providing insights into which might best suit your needs.

Canada Life - Sun Life Canada: Term Life Insurance

Sun Life discusses Term Life Insurance options, detailing how they work and who they are best suited for.

Sun Life - Blue Cross of Canada: What Is Term Life Insurance & How Does It Work?

This article explains the fundamentals of Term Life Insurance, including its benefits and how it operates.

Blue Cross - Canadian LIC: 2024 Average Term Life Insurance Rate Chart by Age

This blog provides insights into Term Life Insurance Rates in Canada, helping you understand how age and other factors influence premiums.

Canadian Lic - MoneySense: What Is Term Life Insurance and How Does It Work?

This piece offers a clear explanation of Term Life Insurance, its benefits, and considerations for Canadians.

MoneySense - RBC Insurance: Term Life Insurance in Canada

RBC Insurance provides details on their Term Life Insurance offerings, including coverage options and benefits.

RBC Insurance - PolicyMe: Types of Life Insurance in Canada Explained

PolicyMe breaks down the different types of life insurance available in Canada, helping you understand your options.

PolicyMe

Key Takeaways

- Four Types of Term Life Insurance

The four main types are Level, Decreasing, Renewable, and Convertible Term Life Insurance, each catering to different financial needs and goals. - Level Term Life Insurance

Offers fixed premiums and consistent coverage throughout the term, making it ideal for stable financial protection. - Decreasing Term Life Insurance

Coverage reduces over time, matching declining debts like mortgages, making it a cost-effective option for specific obligations. - Renewable Term Life Insurance

Allows policyholders to extend coverage without a medical exam, providing flexibility for changing life circumstances. - Convertible Term Life Insurance

Enables a seamless transition from term to permanent insurance without new underwriting, ensuring long-term security. - Affordable Term Life Insurance Rates

Term policies are typically more affordable compared to permanent insurance, offering excellent value for short- to medium-term financial needs. - Tailored Coverage

Term Life Insurance Plans can be customized to align with your goals, such as securing education funds, mortgage payments, or business debts. - Smart Term Life Insurance Investments

Term Life Insurance is a wise financial choice to protect your loved ones during key life stages, offering peace of mind at affordable rates. - Online Accessibility

You can easily buy Term Life Insurance online, compare rates, and find plans that fit your needs conveniently. - Canadian LIC’s Expertise

Canadian LIC provides expert guidance to help clients choose the right Term Life Insurance Plan based on their financial goals, ensuring tailored protection.

Your Feedback Is Very Important To Us

Thank you for taking the time to share your feedback! Your insights help us better understand your challenges and provide tailored solutions for your Term Life Insurance needs.

Thank you for your valuable feedback! We will use your responses to provide better support and resources tailored to your needs. If you have further questions, please don’t hesitate to reach out!

IN THIS ARTICLE

- What Are the 4 Types of Term Life Insurance?

- Understanding Term Life Insurance and Its Importance

- Why is it important to explore different types of Term Life Insurance?

- Type 1: Level Term Life Insurance

- Type 2: Decreasing Term Life Insurance

- Type 3: Renewable Term Life Insurance

- Type 4: Convertible Term Life Insurance

- Comparing the Four Types of Term Life Insurance

- Factors to Consider When Choosing Term Life Insurance

- Canadian LIC's Approach to Helping Clients

Sign-in to CanadianLIC

Verify OTP