Basics

- What Is The Waiting Period For Term Insurance?

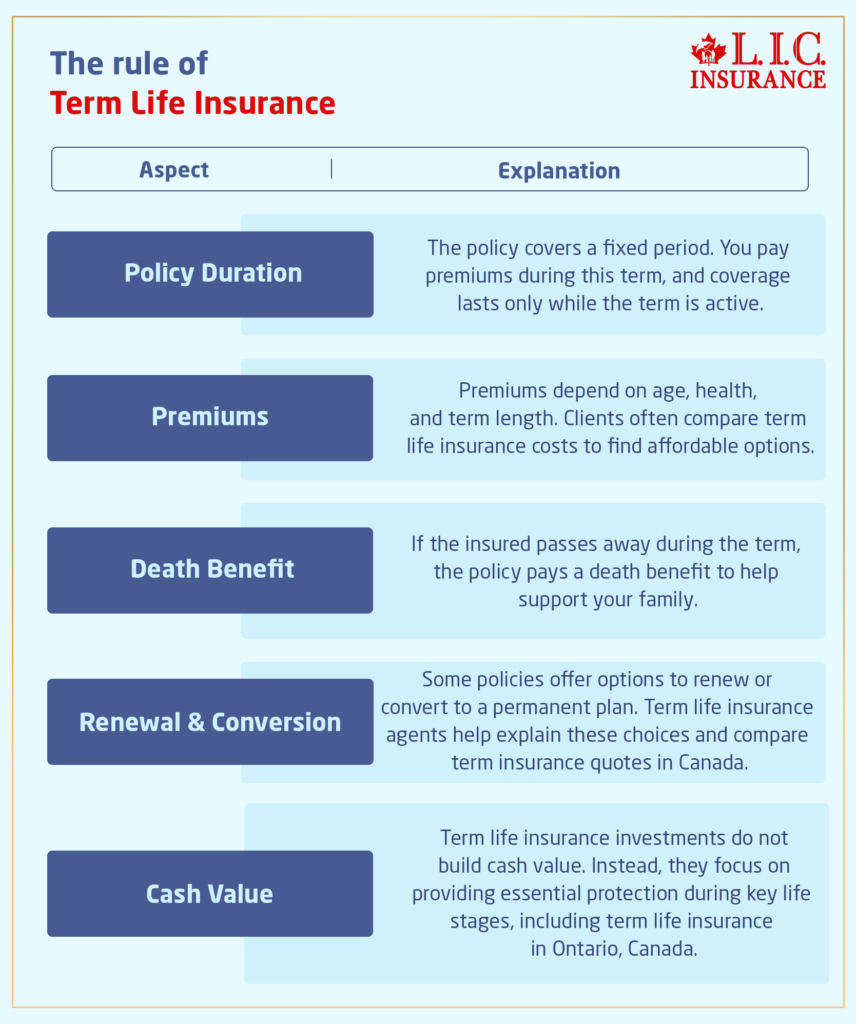

- What Is The Rule Of Term Life Insurance?

- Understanding the Uses of a Term Insurance Calculator

- What Is Underwriting in Term Life Insurance?

- How Do You Buy Term Life Insurance?

- What Is the Main Disadvantage of Term Life Insurance?

- How Do You Choose Term Insurance?

- Can You Cash Out a Term Insurance Policy?

Reviews

Common Inquiries

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- Can A Smoker Get Term Life Insurance?

- Understanding Term Life Insurance

- How Smoking Affects Term Life Insurance

- The Medical Underwriting Process

- Higher Life Insurance Premiums: What to Expect

- Securing a Canadian Term Life Insurance Plan as a Smoker

- Real-Life Struggle Stories from the Field

- Benefits of Term Life Insurance for Smokers

- Navigating the Application Process

- Challenges and Considerations for Smokers

- Success Stories and Lessons Learned

Can A Smoker Get Term Life Insurance?

By Pushpinder Puri

CEO & Founder

- 11 min read

- February 19th, 2025

SUMMARY

This blog discusses how smokers can qualify for a Canadian Term Life Insurance Plan, how insurers classify smokers, and the impact on premiums. It covers ways to secure better Term Life Insurance Policy quotes in Canada, reduce costs, and switch to non-smoker rates. It also explains the role of Term Life Insurance Brokers in Ontario, Canada, in finding the best Term Life Insurance Plans and ensuring financial protection for smokers and their families.

Introduction: Overcoming the Hurdles of Smoking and Insurance

For many Canadians who smoke, a common issue when looking for financial protection is the question: “Can a smoker get Term Life Insurance? Every day, people ask this question when they search for Term Life Insurance Policy Quotes in Canada or turn to Term Life Insurance Brokers in Ontario, Canada. Smokers worry that their habit will disqualify them from good policy or make them pay exorbitantly high premiums. Fear not; if you have felt judged or misunderstood by insurance companies, you are not alone.

If you have done even a smidge of research on Term Life Insurance Plans, you have likely realized that smokers have to jump through a few hoops when pursuing coverage. Some Life Insurers may consider smokers at higher risk, resulting in higher rates or even rejections. Today, we’re going to break down Term Life Insurance Coverage for smokers, what it means for your chances of obtaining a favourable Canadian Term Life Insurance Plan, and life stories about the real struggles and successes of people just like you. After reading through this guide, you should be better equipped to understand your options and how to obtain the protection that you deserve.

Understanding Term Life Insurance

With Term Life Insurance, you get protection for either 10, 20, or 30 years. It provides a death benefit to your beneficiaries if you die during the term of the policy. That’s why people are increasingly using life insurance, especially families who want peace of mind knowing their loved ones are secure in case of premature death.

Key Points About Term Life Insurance:

- Temporary Coverage: Term Life Insurance provides coverage for a specified number of years. If you outlive the term, the policy usually ends without a payout.

- Low-cost premiums: Term Life Insurance has no cash value, so it generally has a lower cost than permanent life.

- Easy to Understand: Because the focus is totally on a death benefit, it is a straightforward process for those looking to protect their family financially.

- Flexibility: Many Term Life Insurance Plans allow you to renew or convert to a permanent policy without getting a new medical examination.

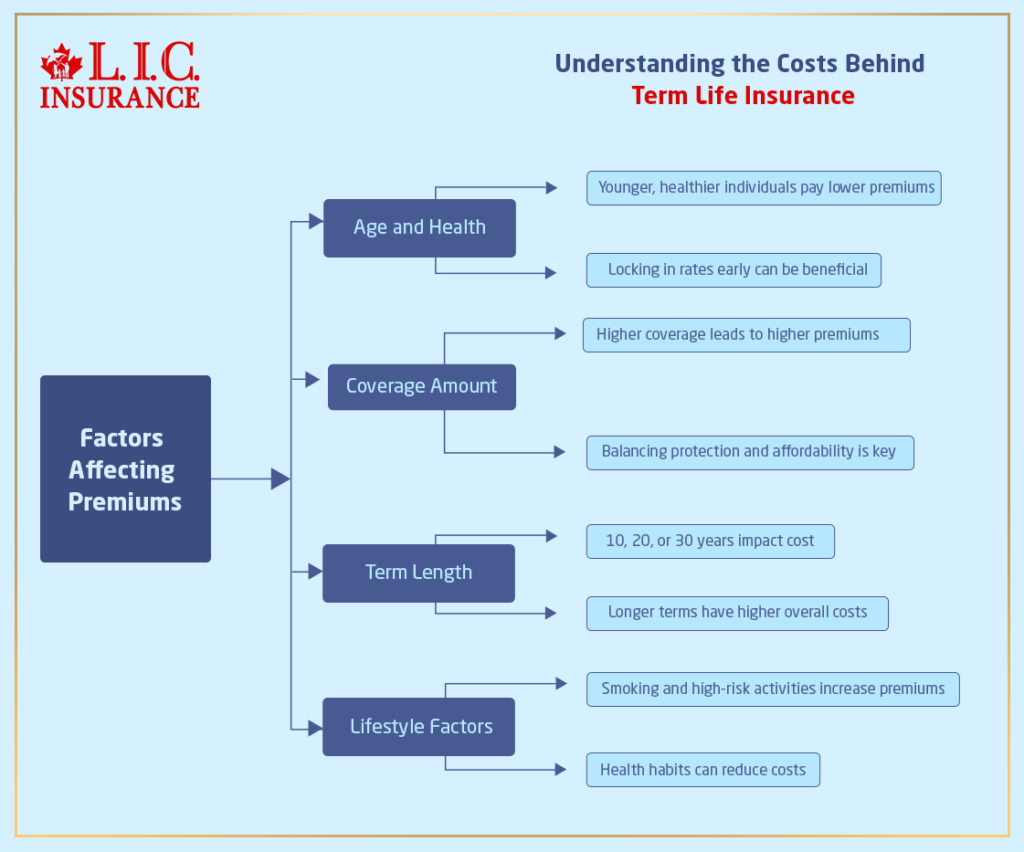

Term Life Insurance is easy to find; however, if you are looking for quotes on the best Term Insurance Policy available in Canada, premiums and prices vary depending on age, health, and smoking. Because smoking is riskier than non-smokers, smokers typically pay higher premiums than non-smokers.

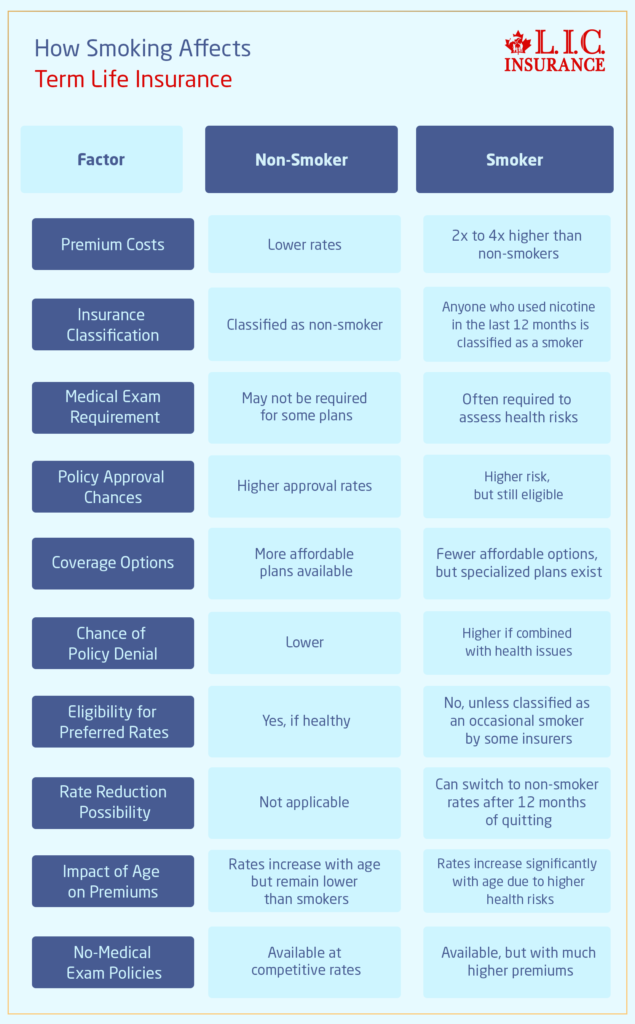

How Smoking Affects Term Life Insurance

Insurance companies evaluate risk before determining premiums. Because it is associated with a variety of medical problems, such as heart disease, lung cancer and respiratory diseases, smoking is one of the top risk factors. Because of this, smokers are statistically more likely to die sooner than non-smokers ultimately. This increased risk results in higher premiums on smokers’ term life insurance coverage.

The Medical Underwriting Process

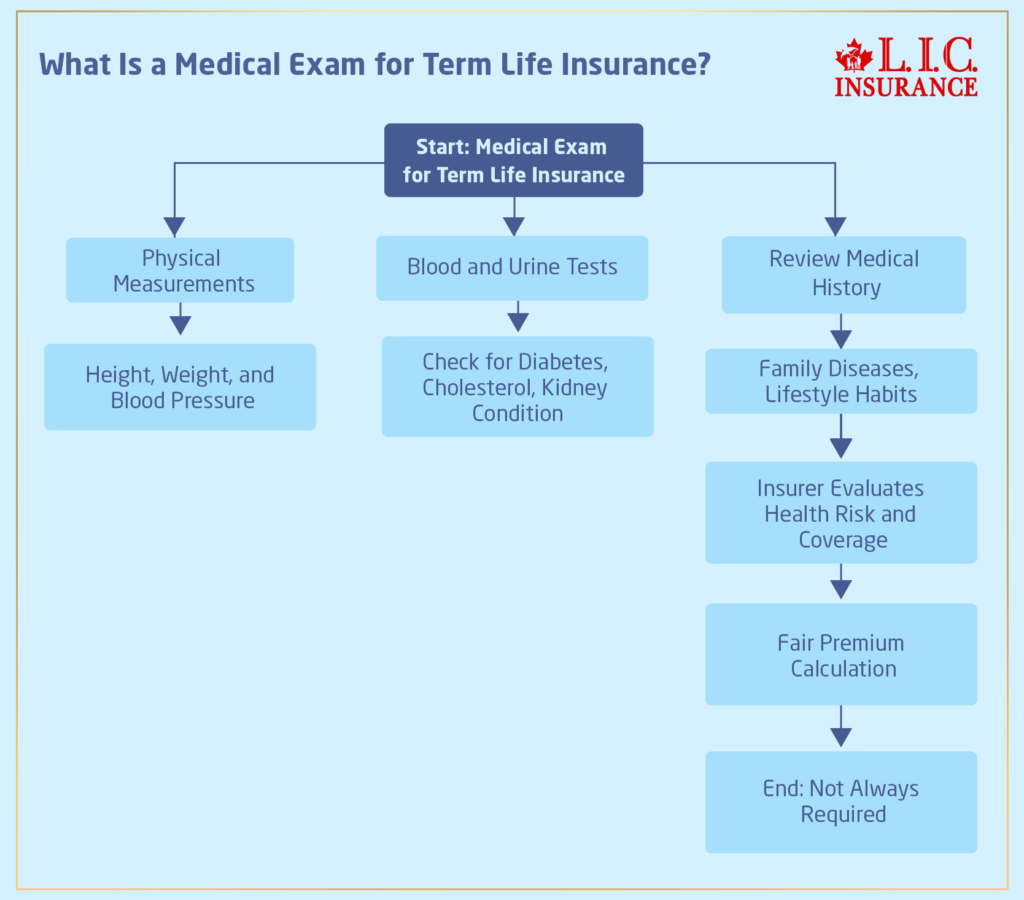

A Term Life Insurance Policy will require a medical underwriting process when you apply for coverage. This normally consists of:

- Some Medical Questionnaires: You respond to questions regarding your smoking habits, such as how often you smoke and how long you have been smoking.

- Medical Checks: Some insurers demand a physical exam, which might include blood tests, urine tests, and vital measurements.

- Medical Records Review: Insurance companies may want to see your medical history so that they can assess your overall health.

For smokers, these steps can expose conditions or habits that lead to an increased risk of dying early. So, you could be considered a high-risk applicant by the insurance company. While this may result in higher premiums, it doesn’t necessarily make you ineligible for coverage. However, most Life Insurance Companies in Canada will accept smokers with raised premiums.

Higher Life Insurance Premiums: What to Expect

If you smoke, expect premiums higher than you would pay as a non-smoker. How much it goes up specifically will depend on a few things:

- Frequency: The number of cigarettes or cigars you smoke on a daily basis.

- Duration: How long have you been a smoker?

- General Health: Other health factors that may exacerbate the negative effects of smoking.

- Age: Smokers over a certain age may pay significantly higher premiums.

If, for example, you smoke and are in your 30s or 40s, your 20-year term life policy premium may be considerably higher than that of someone the same age who does not smoke. However, many people have still been able to obtain Term Life Insurance even if they smoke cigarettes due to the breadth of products available in the marketplace.

Securing a Canadian Term Life Insurance Plan as a Smoker

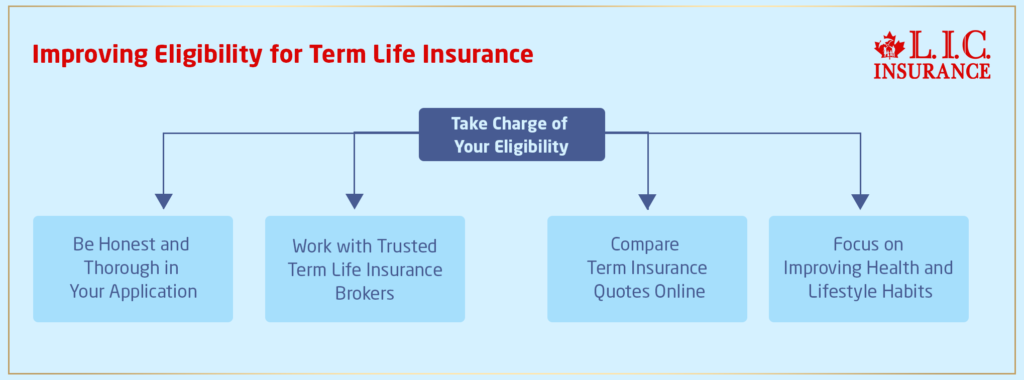

If you smoke, you can still find a Term Life Insurance Policy that suits your needs. It’s a matter of knowing the market and getting the right people on your side to help you find the best available option. So here are practical steps to get you started.

1. Gather Accurate Information

Make sure all your smoking habits and health details are accurate, and be honest before applying. Be truthful on the application because lying could lead to a denial of coverage or a later claim being denied. An up-to-date record of your health checkups, cessation attempts or even just details of your reduced smoking can occasionally help reduce your premiums if you make progress.

2. Compare Term Life Insurance Policy Quotes in Canada

In Canada, there are several online platforms that enable you to compare Term Life Insurance Policy quotations. These tools can explain how much more you could spend as a smoker and provide a menu of options. Look for:

They’re not trying to cover your expenses; they’re trying to make money, too!

- Multiple Quotes: Obtain several quotes to see the range of premiums.

- Smoker-Friendly Providers: You can compare Life Insurance companies to find the ones most lenient on smokers.

- Customization: Certain quotes let you modify things like term length and coverage amount to get an idea of how those changes affect your premiums.

3. Consult with Term Life Insurance Brokers in Ontario, Canada

This is where Term Life Insurance Brokers in Ontario, Canada, or anywhere else for that matter, can come in handy. These professionals have first-hand experience with smokers and know their way around underwriting. They can help you:

- Find Smoker-Friendly Providers: There are some insurers, for instance, that offer competitive rates for smokers.

- Negotiating Better Terms: Brokers may be able to negotiate terms or find discounts that aren’t readily available online.

- Train: They recast the medical underwriting process for you so that you know what to expect.

One customer, for example, remembered that his broker assisted him in navigating the application process by telling him to get a health checkup before applying, which ultimately resulted in a lower premium when his better metrics were recorded.

4. Consider Lifestyle Changes

If your goal is to get coverage as a smoker, supplemental insurance may help with that, but remember all of the long-term aspects of lowering or quitting altogether. Many insurers provide lower rates to people who scale back their smoking or stop altogether. Even if you’re not ready to quit smoking cold turkey, making a move toward a healthier lifestyle could result in lower premiums down the road.

5. Understand Your Options

There are different features of Term Life Insurance Plans. Some plans include a conversion option if your situation changes that allows you to turn the term policy into a permanent one without going through further underwriting. This can be especially advantageous if you intend to stop smoking eventually, as it may help you lock in a lower premium. Getting to know these benefits and talking to a broker can help you come up with a more personalized plan for your needs.

6. Review and Reassess Regularly

After you obtain a Term Life Insurance Policy, you should periodically evaluate your coverage and premiums. If you make lifestyle changes or your health improves, you may have chances to renegotiate your terms or convert your policy to a new plan that provides more favourable rates. In fact, regular reviews make sure that your Term Life Insurance Coverage still aligns with your current life.

Real-Life Struggle Stories from the Field

Many individuals have faced the challenge of obtaining Term Life Insurance as a smoker, and their experiences offer valuable lessons.

Story 1: Overcoming Initial Setbacks

One of these, a long-term smoker in his late 30s, encountered difficulty finding affordable Term Life Insurance Coverage on his first attempt. After receiving several quotes that were far out of his budget, He sought out the help of a Term Life Insurance broker in Ontario, Canada. But by submitting to a rigorous medical examination and communicating how frequently he smoked, the broker said he could be eligible for a better rate. After the examination and some slight changes to his lifestyle, we were able to secure him a 20-year Term Life Insurance Policy at a premium that he could afford, given his income level. This story illustrates the necessity of honest conversation and professional advice.

Story 2: Turning a Health Journey into Savings

Another person, a woman in her early 40s, had been a smoker for decades. When she applied for Term Life Insurance, her first coverage quotes were discouragingly high. But after attending a health program geared at reducing smoking, she was able to cut back drastically. She reapplied for coverage and saw much more competitive Term Life Insurance Policy Quotes in Canada based on her improved health metrics. This story is an illustration that even little positive lifestyle changes can make an enormous difference in your insurance costs.

Story 3: A Family’s Perspective

A young dad who worried about what would become of his family was eager to ensure they were protected in the event of his passing, even if he himself smoked. Worried over the soaring prices, he spoke with multiple Term Life Insurance Brokers. With their help, he learned that some providers were more lenient with smokers, particularly if the person also had evidence of regular health exams. By comparing many Term Life Insurance Plans, he was able to find one that had enough coverage at a reasonable price. This allowed him to support his family without compromising his business, which is a testament to the fact that with determination and the right advice, it is possible to succeed.

Benefits of Term Life Insurance for Smokers

Even with the higher premiums associated with smoking, Term Life Insurance remains an excellent option for smokers for several reasons:

Affordability for Short-Term Needs

Because Term Life Insurance provides coverage for a finite period, it’s great for helping your family stay financially afloat during high-risk years. If you are a smoker who could end up with higher premiums, a term plan helps you lock in needed coverage for much less than permanent policies would cost. This is especially helpful when you’re in a life stage that involves large expenses, such as a mortgage or raising children.

Flexibility and Conversion Options

Most Term Life Insurance Plans have a conversion offer, which means you can convert to a permanent policy without additional medical exams. This flexibility can be a godsend if you end up quitting smoking or if your health changes for the better. If you choose this option, you can get covered now and refine your plan later as your life changes.

Peace of Mind for Loved Ones

The main purpose of Term Life Insurance is to protect your loved ones financially. If you smoke, having a Term Life Insurance Policy means that your family will get a payout in case something unexpected happens. The money can be used to pay for things like funeral costs, outstanding debts, and daily living expenses, allowing your family to be taken care of when it matters most.

A Step Toward Better Health

Getting Term Life Insurance could also be an incentive to live a healthier life. Some smokers said the prospect of lower premiums motivated them to cut down on smoking. As time passes, you may find that your health picks up, resulting in lower rates, should you choose to apply to get the original action or perhaps convert your policy.

Competitive Options Among Life Insurance Providers

The Canadian Term Life Insurance market is also competitive despite the drawbacks smokers encounter. Some insurers have their own niche, and Term Life Insurance Brokers in Ontario, Canada, are skilled at negotiating favourable risk and cost scenarios. When comparing different Term Life Insurance Plans, you can find policies that meet your needs and fit your budget.

Navigating the Application Process

The application process for Term Life Insurance as a smoker can seem daunting, but breaking it down into clear steps can help you manage the process effectively.

Step 1: Research and Compare Quotes

You must begin with quotes on Canadian Term Life Insurance Policy. They use online comparison tools to see a variety of prices and coverage options. Also, note that terms such as “canadian Term Life Insurance Plan” would confirm that you mean a plan tailored for Canadians. Getting multiple quotes will allow you to see the premium differences between smoker and non-smoker policies.

Step 2: Prepare for the Medical Underwriting

Ensure you are prepared with all health documents and medical examinations (if any). This can involve things such as recent lab work, medical history, and/or smoking information. Providing accurate information is crucial to getting the best rate possible. Just remember that honesty with your application is going to save you from problems with claims down the road.

Step 3: Consult with a Broker

Get in touch with Ontario, Canada, and Term Life Insurance Brokers who have experience in serving smokers. This is where their expertise comes into play, as they will be able to help you understand the underwriting process and guide you in selecting a plan that will work for you. They can also help you see how small changes in your lifestyle may affect your premiums.

Step 4: Submit Your Application

After selecting a plan, you have to send in your application with proof-of-eligibility documents. The insurance company will then review your information, and in some cases, you’ll be required to take a medical exam. Keep your head in this process, asking if needed questions; follow up with your broker.

Step 5: Review the Offer

Once your application is processed, take the time to review the offer. Notice the premium amounts, the length of term, and if there are any other requirements. If the offer is too soft, negotiate additional alternatives with your broker. If it comes back with a premium that’s more than you can afford to pay, sometimes providers have riders or adjustments they can attach to get them within your budget.

Step 6: Finalize and Maintain Your Coverage

After accepting an offer, make sure you know the payment timeline and policy details. You should review your policy periodically, especially if you experience lifestyle changes that may qualify you for better rates down the road.

Challenges and Considerations for Smokers

While Term Life Insurance is accessible to smokers, there are several challenges and considerations that you should keep in mind.

Premium Costs

Higher premium cost is one of the biggest issues. As a smoker, the same coverage will likely cost you more than it will for a non-smoker. This increased expense is indicative of the greater risk that the insurer takes on. These premiums can be costly, so you need to plan for them and ensure they work with your financial plan.

Health Improvements and Rate Adjustments

Even if you want to make a move toward quitting or even just reduce smoking, note that these steps can lead to lower premiums over time. Some insurers are willing to re-rate your policy after a period of improved health. If this is a possible scenario for you, talk to your Term Life Insurance Brokers and take action today regarding your health because small improvements can have a considerable effect.

Limited Options for Heavy Smokers

If you smoke heavily and/or have a longstanding history of smoking-related health issues, you might discover that your options are more restricted. Some insurers may refuse to cover you — or cover you only through very expensive plans. In this instance, it can be worth contacting multiple brokers to see if any providers specialize in high-risk cases. Sometimes, just sticking with it and trying everything turns up something that works.

Understanding Policy Terms

Be clear on the terms of your policy. Request your broker to clarify confusing parts of the application or policy documents. Understanding your Term Life Insurance Coverage is critical to ensuring you have the protection you need and that you know your obligations as a policyholder.

Success Stories and Lessons Learned

Let’s share a few stories that illustrate how smokers have successfully navigated the process of securing Term Life Insurance Coverage in Canada.

Story 1: A Determined Smoker’sSmoker’s Journey

“The first few who quoted simply put prices so far outside of the budget of the man who smokes, it was pointless to even bother thinking about them,” she added. Unwilling to take no for an answer, he contacted an Ontario, Canada, Term Life Insurance agent. The broker recommended that he go for a full health checkup and keep a record of all health improvements. He waited a couple of months following these recommendations and reapplied, receiving considerably lower-term life insurance policy quotes from Canada. Overcoming his reluctance, his medical history, and his age led to a decision that gave him the protection that was right for him at a premium that he could afford.

Story 2: Turning a New Leaf for Financial Savings

In another case, a woman had been smoking most of her life. When she began planning for her family’s future, she discovered that her estimates of premiums were disheartening. In the hope of getting a secure canadian Term Life Insurance Policy, she started cutting down on her number of cigarettes. Her health gradually improved, and she made the decision to stop smoking altogether. When she reapplied for coverage, she was as happy as a claim to get back competitive Term Life Insurance Policy quotes from Canada. Her story is proof that even incremental lifestyle changes can be financially rewarding.

Story 3: A Family’sFamily’s Financial Security

A worried young dad concerned that his smoking habit left his family at risk of being unprotected after he died sought out a few Term Life Insurance Brokers. Thanks to their expertise, he compared several Term Life Insurance Plans, resulting in an appropriate choice of ample Term Life Insurance Coverage balanced by a premium he could afford. After all, this choice gave him peace of mind, knowing that if something happened to him, his family would be financially secure. His experience highlights the importance of seeking professional advice and exploring multiple options.

The Role of Professional Guidance

Working with knowledgeable professionals can make a world of difference when applying for Term Life Insurance as a smoker. Term Life Insurance Brokers in Ontario, Canada, and other regions bring expertise that simplifies the process and increases your chances of finding a suitable policy.

Benefits of Consulting Brokers

- Smoker-Specific Considerations: Brokers know about the trials involved in being a smoker and also which insurers provide the best rates and coverage options.

- Personalized Advice: They evaluate your unique health profile and financial situation, advising you on policies that suit your needs.

- Access to Multiple Providers: Brokers can take quotes from multiple insurers for Term Life Insurance Policies, so you can choose from many options.

- Streamlined Process: Their support will help you avoid the hassles of applying, get a better understanding of the medical underwriting process, as well as any follow-up questions that may come up.

Most clients had even thanked the Term Life Insurance Brokers. Their guidance often serves as a compass, leading to a path that turns an apparently unattainable target into a prize within reach, giving not just coverage but also a sense of agency in directing one’s financial trajectory.

Comparing Different Term Life Insurance Plans

When shopping for Term Life Insurance, it is essential to compare different plans to find the best match for your needs. Here are some factors to consider when comparing plans:

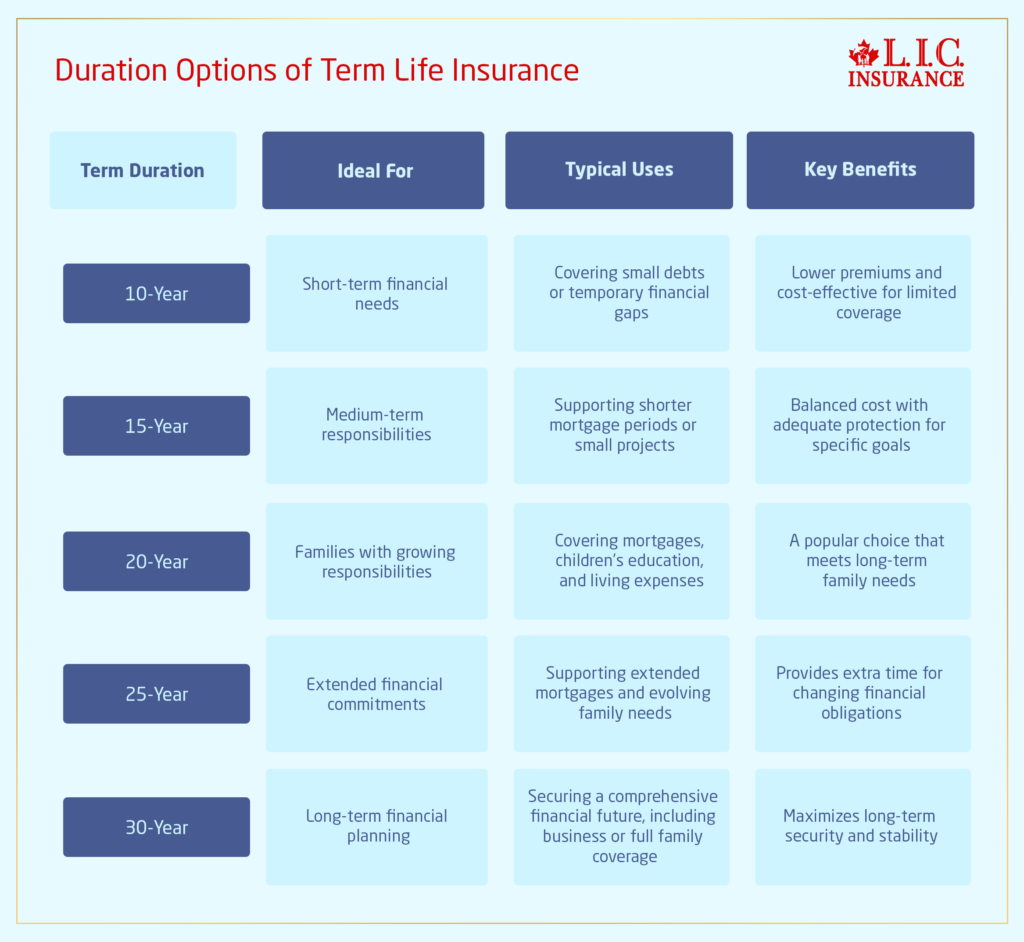

Coverage Duration

There are many different term lengths available with term life insurance policies. So, pick a term that mirrors your real-life financial responsibilities. For example, for a commitment until your children graduate or your mortgage is paid off, make a Term Insurance for those years.

Premium Costs

Premiums differ significantly from insurer to insurer and are based on age, health and smoking status. Go online and get quotes for the Term Life Insurance policies Canada provides and compare them. While people with other health issues may end up paying higher premiums, there are policies that could give you competitive rates with the right adjustments.

Conversion Options

Certain Term Life Insurance Plans include conversion options that let you switch to a permanent policy without undergoing more medical underwriting. It may be especially advantageous if your health improves or you make the decision to quit smoking. Assessing whether the plan provides this versatility and how it aligns with your long-term money lost.

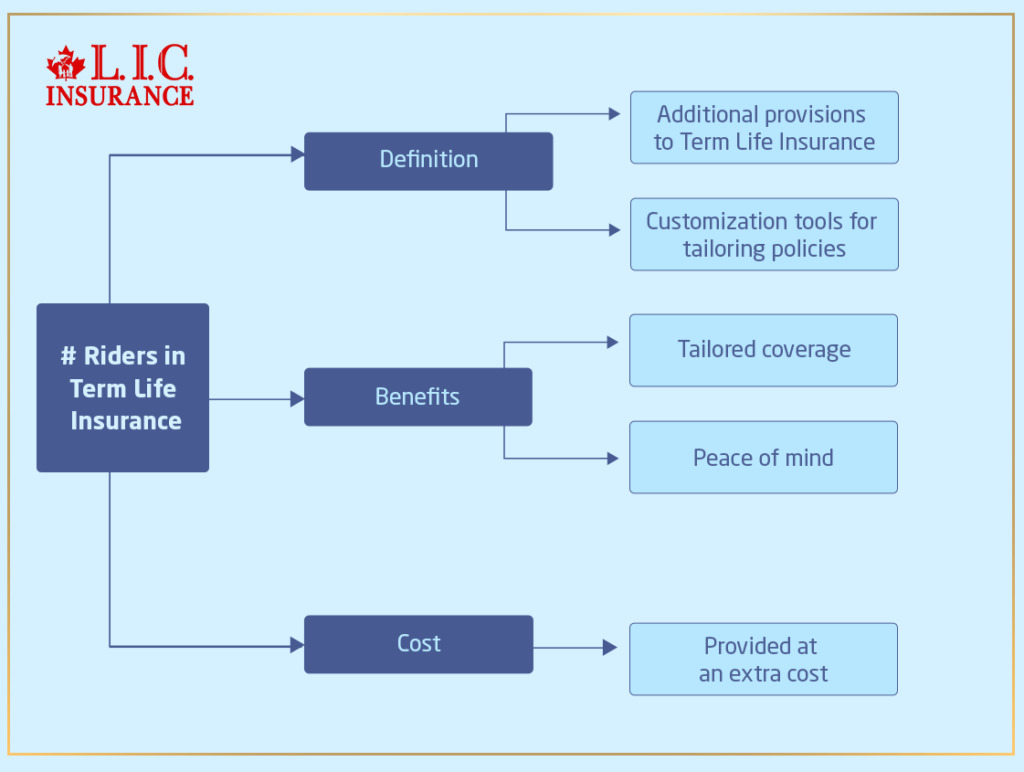

Additional Riders and Features

Riders are extra benefits you can attach to your policy. Some common riders are accelerated death benefits, waiver of premiums and critical illness coverage. See what riders are offered and whether they fit your needs. ExtensionsRM-PersonalProtect-R PatentsRP-RF-Personal Protect-Riders can offer additional protection and peace of mind, helping to make your policy more comprehensive.

Renewal and Termination Provisions

Know the renewal provisions of your Term Life Insurance Policy. Some policies do allow renewal at the end of the term, but the premium may go up. Review the termination terms and make sure you are aware of any penalties or restrictions that may apply if you choose to terminate the policy prior to the end of the term.

How to Improve Your Chances for Better Rates

Even as a smoker, there are steps you can take to improve your chances of securing a Term Life Insurance Policy at a reasonable rate:

Maintain Regular Health Checkups

Undertaking routine health assessments will also document any improvements in your health and should have a positive impact on your underwriting outcome. Document these checkups and provide them to your insurance broker if necessary.

Consider a Health Improvement Plan

Get involved in initiatives for better health. Even incremental efforts — cutting back on smoking, for example, or living a healthier lifestyle — can make a difference in what you pay for coverage. Having these changes documented can help when reapplying or negotiating with insurers.

Be Honest and Transparent

Always disclose truthful and complete information concerning your smoking habits and health history. Honesty in the application process is key. A denial of coverage is one of the most common ways misrepresentations can get you in trouble — and threaten your financial safety net.

Work with Experienced Brokers

By working with Term Life Insurance Brokers in Ontario, Canada, or other areas that specialize in smoker insurance, you get to know the Life Insurance providers who have positive paperwork for high-risk Life Insurance applicants. Having in-house or contracted specialists who know the ins and outs of the underwriting process can be invaluable.

Regularly Reassess Your Policy

After you have coverage, make sure to review your policy periodically. If your health situation improves or if you stop smoking, you may have the option to adjust your policy or convert it to a different type of plan with more favourable terms. The regular re-evaluation of your needs ensures your coverage evolves with them.

The Future of Term Life Insurance for Smokers in Canada

Important Changes in Canadians for a Smokers Term Policies. Improvements in medical underwriting and data analysis are enabling insurers to evaluate risk better. In turn, eventually, you may find a wider selection of competitive rates and innovative products for smokers.

Emerging Trends

- Technology-Driven Underwriting: Modern digital health records and AI-powered risk assessment tools help insurers accurately assess the health of an applicant. This would enable smokers who have shown improvement in their health to receive fairer premium rates.

- Specialized Products: However, one or two insurers are gradually making specialized Term Life Insurance Policies available for smokers. Such products consider the fact that the risks of smoking are unique and thus may offer better terms for the health proactive.

- More Flexibility: As consumer demand increases, insurers can introduce greater flexibility in Term Life Insurance Plans, which may permit coverage adjustments based on lifestyle changes. Conversion options and flexibility on renewals might become a staple.

Market Adaptation

The changing landscape of the insurance market means that even if you are a smoker now, you don’t have to be locked into one course of action. The market evolves with the changing profile of consumers and health trends. For those who are willing to put in the work required to improve their health, there are promising signs for better rates and more options in the future. If you stay informed and do what you can about working with your health, you can achieve better Term Life Insurance options as you age.

Building a Financial Safety Net

Term life insurance is key to creating a financial safety net for you and your family. Even if you were currently smoking, having coverage ensures that your family is financially safe from your premature death. This safety net may include expenses from mortgage payments, childcare costs, spending on education, and other everyday living expenses. Having peace of mind that your family is covered can help you focus on other areas of your life, such as becoming healthier and financially stable.

Integrating Insurance into Your Financial Plan

Think of your Term Life Insurance policy as a part of your larger financial picture. Here are some tools on the tools:

- Budget for Premiums: Be certain to budget for your insurance premiums in your monthly budget. Smokers may be charged more, but with planning, these expenses need not break the bank.

- Emergency Funds: set aside money for an unplanned expense. This “”bucket”” also serves as a financial safety net and a supplement to your Term Life Insurance Policy.

- Long-Term Objectives: Insurance should fit with your long-term financial objectives. Whether you’re hoping to purchase a home, save for retirement, or pay for your children’s education, your insurance policy should fit into your larger plan.

- Annual Check-ins: Come back to your financial plan on a yearly basis. As your health and financial situation changes, so should your insurance coverage. Regular reviews help make sure that, at all times, you have the right level of protection in place.

Advice from Industry Professionals

This is what many term brokers in Ontario, CA, and nationwide have shared with clients about obtaining coverage as a smoker. They underestimate the weight that you can be by knowing your risk profile and seeking professionals to help navigate that underwriting process. Here are some of the advice they frequently dispense:

- Be Honest: Be clear about your smoking habits. This truth means your policy is valid when you need it most.

- All Help Documentation: People can benefit from any evidence of smoke reduction efforts to improve their health. This documentation can sometimes drive better underwriting results.

- Acting without Delay: Begin the process of applying for coverage the minute you decide you want to be covered. And the sooner you apply, the better your chances of securing a rate that lines up with your budget.

- Make Sure You Ask Questions: Collaborate with your broker to ensure you have a comprehensive understanding of your policy. Inquire about the conversion options, renewal terms and whether or not premium rates will change.

- Defy Adverse Selection: If your rates are higher now, health improvements create the potential for better rates ahead. Take care of your health and keep in contact with your broker.

These tips aren’t just theoretical; they’re based on real-life experience. Countless clients have followed these guidelines, remained engaged with their insurance provider, and witnessed their premiums improve over time.

How to Evaluate Term Life Insurance Coverage

When evaluating Term Life Insurance Coverage, consider the following factors to ensure you choose the best policy for your needs:

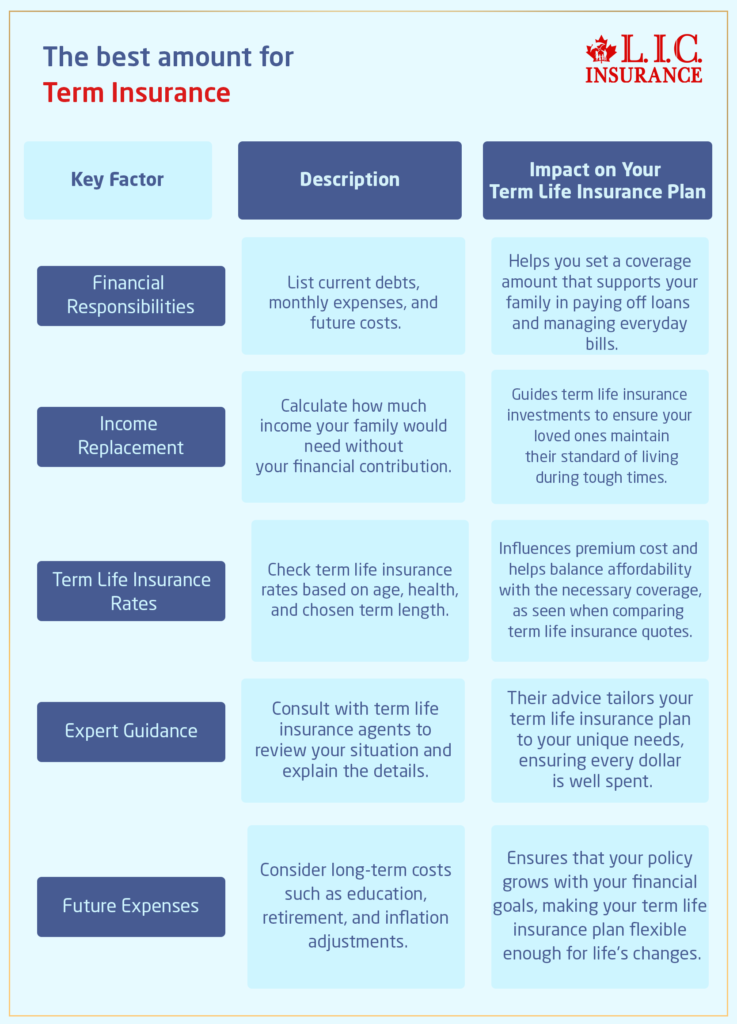

Coverage Amount

In order to figure out how much coverage your family would need to sustain their standard of living if you were no longer there as a breadwinner, This sum should be enough to account for current living expenses, debts and more distant requirements like education costs.

Term Length

Pick a term length that works for your financial obligations. If you have young children or sizable debts, longer terms may be appropriate. Conversely, if your major financial obligations are going to be reduced in the not-too-distant future, a shorter term may be enough.

Premium Stability

Consider if the policy includes level premiums during the policy term. Fixed premiums help you budget; with each month or year, you’ll you’ll know the amount you need to pay.

Renewal and Conversion Options

Seek out policies that have renewal or conversion options. These features are beneficial because if you decide to expand your coverage or wish to convert to a permanent plan, you won’t have to undergo additional medical tests; this can be valuable if your health situation improves.

Exclusions and Limitations

Read the policy’s exclusions and limitations carefully. Some policies have those little terms that can impact smokers differently — knowing them can spare you surprises down the line.

Customer Support and Service

Do the due diligence to check the reputation of the insurance provider and the level of support they offer to their customers. Reliable customer support is also essential when you have questions or need help with your policy over time.

The Impact of Smoking on Your Financial Future

In a variety of ways, smoking affects both your health and even your future financial stability. Higher insurance premiums are merely a single example. Health care costs: Smokers are likelier than non-smokers to require health insurance coverage, costing them (and potentially their employers) more money in the long term. Smokers may also lose their source of income due to poor health. Smoking can, in many instances, directly cause a life-threatening illness that will lead to chronic conditions that incur additional medical expenses to maintain the smoker’s health. One way to protect against some financial risks is to purchase Term Life Insurance to help ensure your loved ones are protected from the financial impact of your untimely death.

Getting a canadian term Life Insurance plan: This is a proactive approach to protect the future of your family. Higher premiums may seem scary at first, but knowing that your loved ones are protected is worth it. Ultimately, a smart Term Life Insurance Policy can be part of your financial safety net in the long run, offsetting some of the financial impacts of the economic cost of smoking.

Making the Decision: A Step-by-Step Approach

The decision of whether to apply for Term Life Insurance as a smoker is a critical one that follows several definitive steps. Here is a methodical way to represent the decision-making facets:

Evaluate Your Finances:

The first step is to look at your financial obligations established so far, which comprise debts, living expenses, and financial goals for the future. Having a clear sense of your financial situation will help you figure out how much coverage you need.

Gather Health Information:

Gather relevant medical records detailing your smoking habits and health improvements. This is important for accurate underwriting, and it might reduce your premiums if you’ve made positive changes.

Research and Compare Quotes:

Compare quotes for Term Life Insurance Policies Canada writes you online. Check with different providers for their options and note how premiums vary based on smoking status.

Consult with a Broker:

Speak with a Term Life Insurance broker in Ontario, Canada , or in your area. They will help you parse your options and find the best plan suited to your needs.

Review Policy Details:

Go through the terms and conditions intently for each policy. Watch for coverage amounts, term lengths, renewal options, and any special conditions regarding smoking.

Make a Decision:

Select the Term Life Insurance Plan that best fits your budget based on your research and consultations, and that provides the necessary coverage for your family.

Maintain Your Coverage:

When you land a policy, be sure to continue making your premium payments and do periodic reviews. If your health improves or if you quit smoking, talk to your broker about possible changes.

Tips for Smokers Seeking Term Life Insurance

Here are more tips to get the best possible Term Life Insurance rates as a smoker:

- Get Started Early: Don’t leave it until the last minute. The more quickly you apply, the better your odds of securing a rate that works for you.

- Underwriting Processmturing: Stay Updated Changes in technology and medical assessments could make it easier for smokers to get better rates over time.

- Switch to a Healthier lifestyle: More reduction in smoking even leads to better health reporting. If you stick to a good path, you may document and communicate this to your broker so that you can lower your premium in future reviews.

- Request a Review: If you have notable health improvements, ask your broker if you are eligible for a policy review. Certain insurers might reassess premium costs with new health information.

- Be Honest: You should always provide the correct information on your application. Transparency is critical to making sure that your policy holds up when you go to file a claim.

- Focus on Your Future Plan: Your Term Life Insurance accordingly. Supplement it with savings, investments, and other insurance products to build a complete entrepreneurial financial safety net.

The Broader Benefits of Term Life Insurance

Beyond providing financial security for your loved ones, Term Life Insurance offers broader benefits that contribute to your overall financial planning:

Financial Planning and Stability

Index universal life insurance is an important section of a comprehensive financial plan. It secures your family from unexpected financial struggles. The death benefit helps pay for funeral expenses, unpaid debts and future living expenses, giving you a financial cushion in difficult times.

Peace of Mind

You sleep easier at night knowing your loved ones will be taken care of with financial support in the event that something happens to you. This way, you can devote yourself to things you find essential, like taking care of your health, working towards your ambitions, and so forth.

Flexibility to Reallocate Resources

Since Term Life Insurance Policies generally have lower premiums than permanent Life Insurance, you may discover that you have more money to allocate toward other financial goals. These may be things such as saving for retirement, investing in education, or even setting up an emergency fund. Temporary coverage without compromising other financial goals makes Term Life Insurance Plans an appealing option due to their cost-effectiveness.

Complementary Coverage

Term Life Insurance Many people opt for a Life Insurance option that protects a defined period of risk. Other insurance and investment products can be added to this as a valuable combination. With some term Life Insurance, as well as savings and investment vehicles, you can create a safety net that covers these short-term and long-term needs.

Preparing for a Secure Future

When it comes to your options, remember that getting Term Life Insurance is a key step toward ensuring your family’s future — no matter what your smoking status may be. Although smokers might pay a higher premium, the positives of coverage—financial security, peace of mind, and a stable safety net—are priceless.

With the right planning, research, and partnership with experienced term life insurance brokers in Ontario, Canada, you can secure a policy that suits your needs. For every instance of forward motion, stopping yourself from completing a goal, or improving your lifestyle, you can have that explained to you in the future, often a lesson on your time.

You may be on a journey toward financial security that never ends. Periodically review your financial plan — and adjust your insurance as necessary — as you continue on this path. The Term Life Insurance marketplace is competitive, and new products and options are consistently coming onto the scene. Stay involved, ask questions and be willing to change your plan as your situation changes.

How Smoking Affects Term Life Insurance

Final Thoughts and a Call to Act

Getting Term Life Insurance as a smoker in Canada can be daunting, but when you take the right steps and seek help from an expert, you can end up finding a policy that offers the coverage you require and that won’t chalk up a number on your cost! Yes, you can get a Canadian Term Life Insurance Plan for smokers.

The above steps to gather the right health information and compare Term Life Insurance Policy Quotes Canada provides and advice from seasoned brokers, as well as the conversion options, will help you build a solid safety net for your family. The stories we hear highlight that many have managed to overcome early challenges and find coverage that meets their financial goals.

If you are a smoker looking for Term Life Insurance Coverage, there is hope for you. The process can be a bit of work, but it is well worth your time when you get a policy that will protect the ones you care about and potentially secure your future when done correctly. Be proactive about your health, connect with knowledgeable professionals, and keep looking for both the appropriate coverage and the right health care to suit your needs.

Providing your family with the sense of safety that comes from knowing you have secure financial protection in place. By selecting a Term Life Insurance Policy that meets your needs as well as those of your family, you can place it as a cornerstone of your financial plan so that no matter what may happen with your life, your family will be secure.

So let us help you secure your future by finding the right customized term Life Insurance plan today. Contact the proficient Term Life Insurance Brokers of Ontario, Canada—compare quotes for Term Life Insurance Policies and get the coverage you want! Your decision today will lay the foundation for tomorrow. Take action and protect your family now with the right Term Life Insurance for your situation.

So, that is the complete guide to determining if a smoker is eligible to take Term Life Insurance in Canada. This article should have opened your eyes and given you an idea of what steps you can take to get the protection you require. It is always better to be safe than sorry, so make sure you take that first step towards achieving financial security and take advantage of the resources and professional advice available. Grab this guide on how to better your future, keep your loved ones safe, AND create a financial safety net that lasts forever.

More on Term Life Insurance

- How Many Years Is A Term Life Insurance Policy?

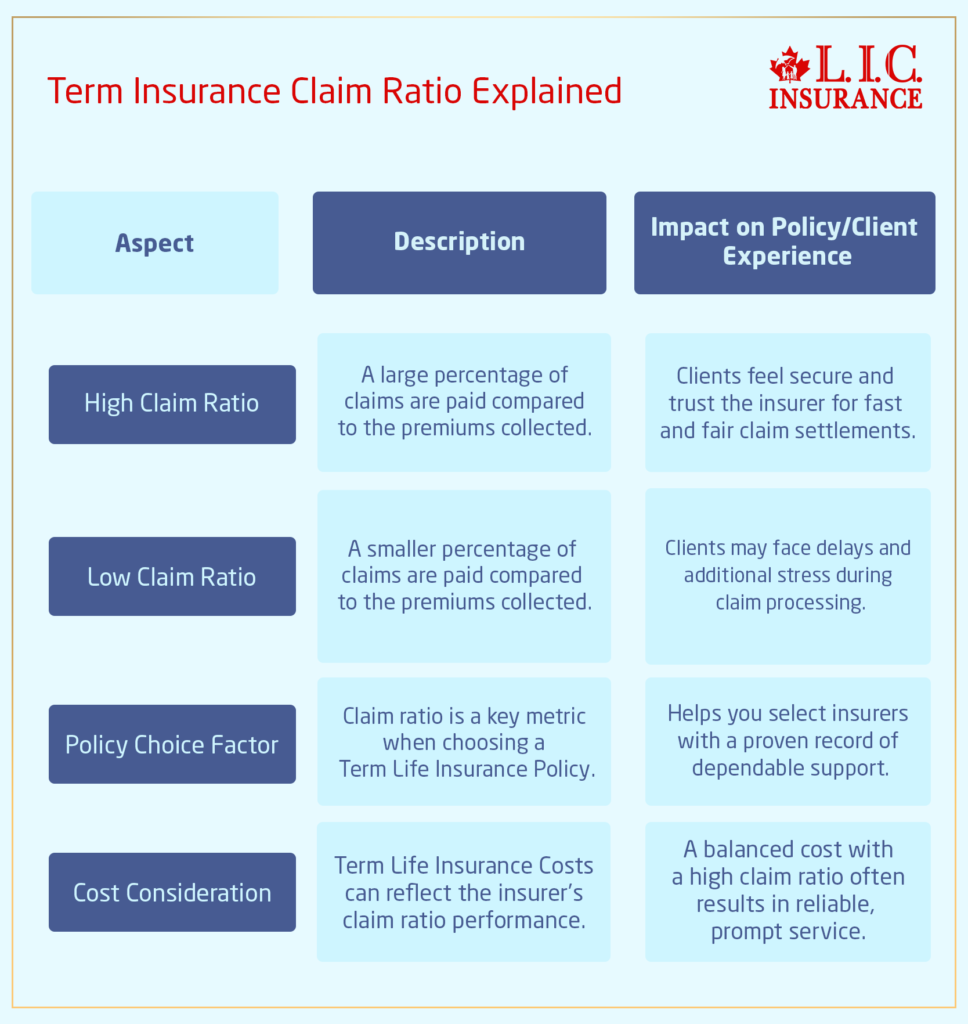

- Which Company Has The Highest Claim Ratio In Term Insurance?

- What Is The Best Amount For Term Life Insurance Policy?

- How Expensive Is Term Life Insurance?

- What Is The Rule Of Term Life Insurance?

- What Is The Waiting Period For Term Insurance?

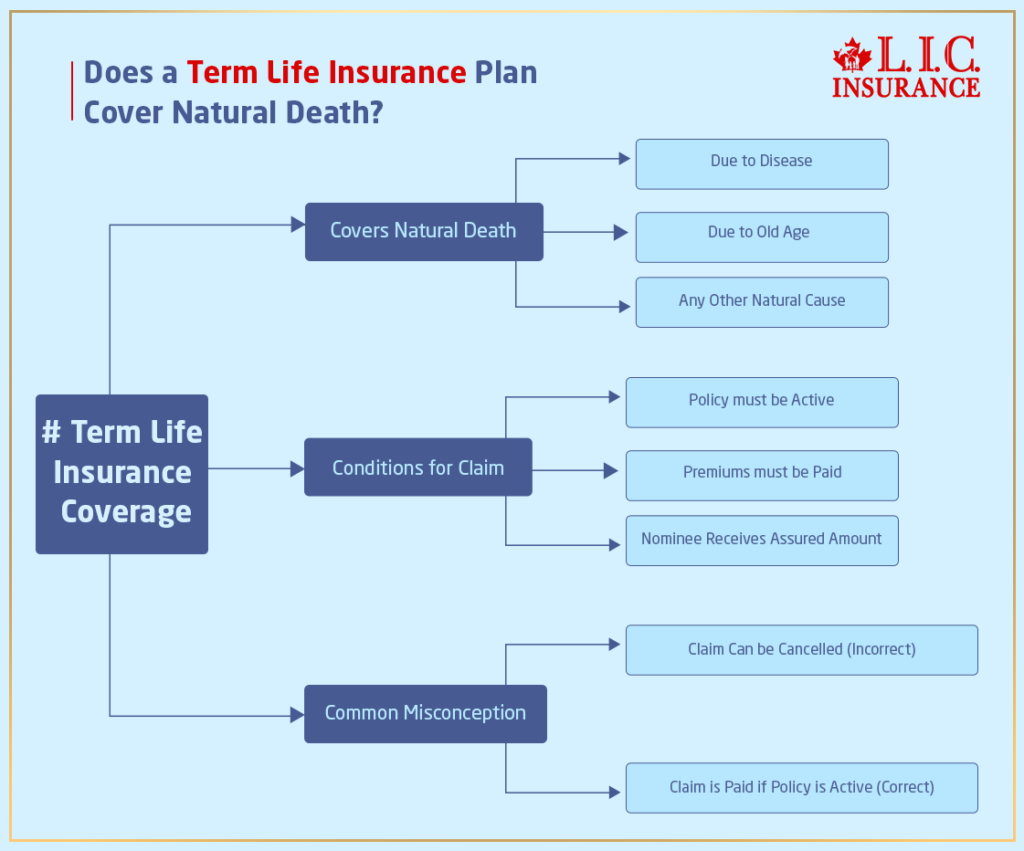

- Is Natural Death Covered In Term Insurance?

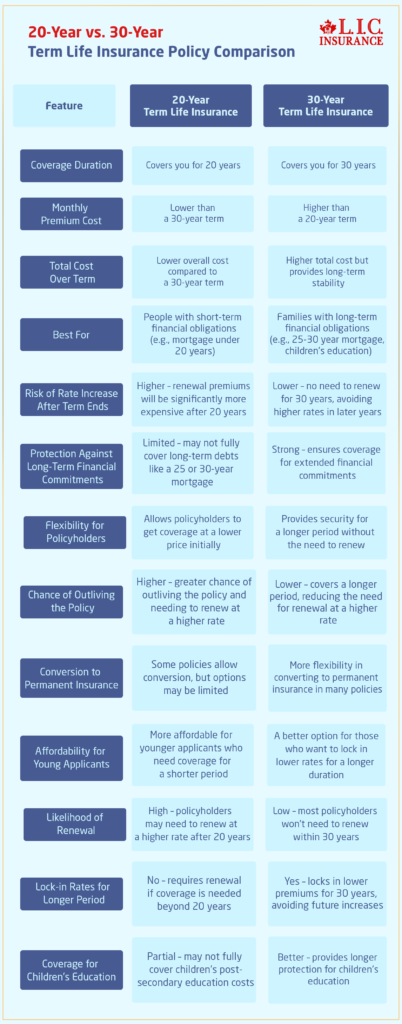

- Should I get a 20 or 30-year Term?

- How Do I Claim Term Insurance?

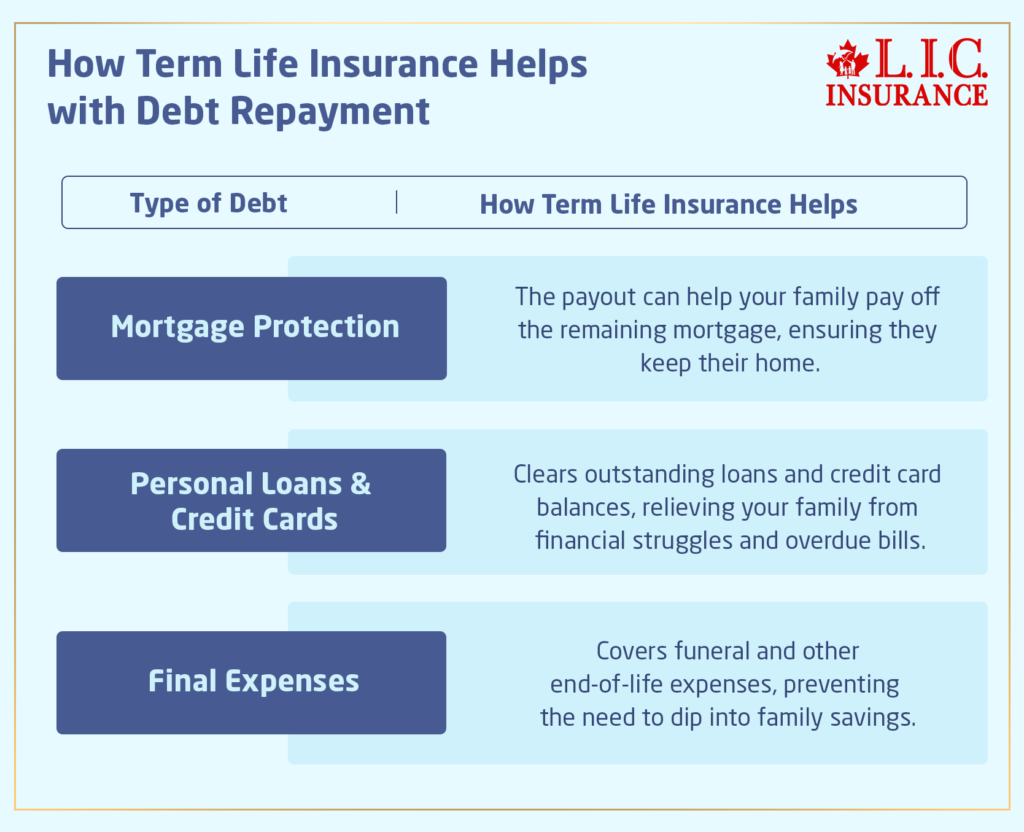

- Can I Use My Term Life Insurance To Pay Off Debt?

- Who Is The Largest Provider Of Term Life Insurance?

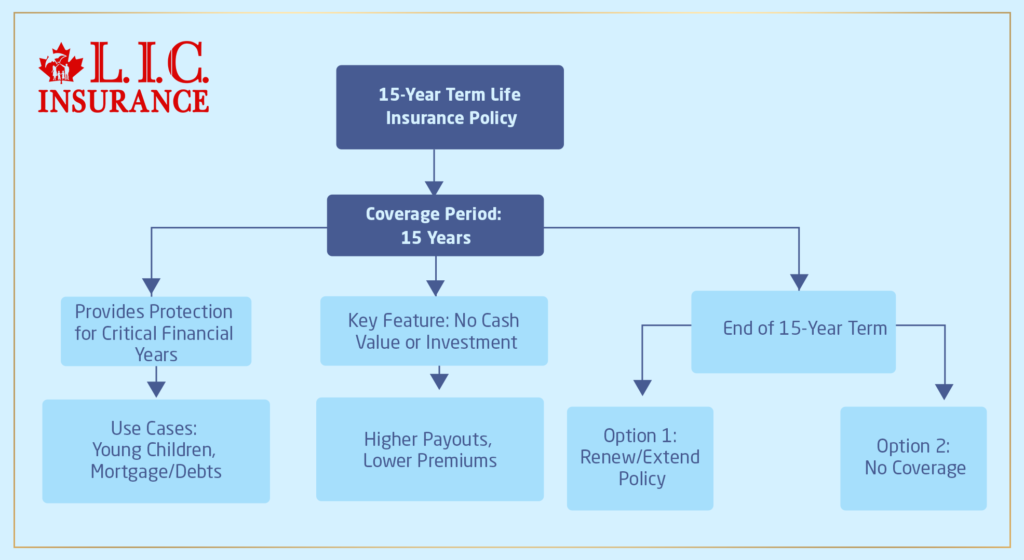

- What Happens After 15-Year Term Life Insurance?

- What is a 5-Year Term Life Insurance Policy?

- What Is The Expiry Date On Term Life Insurance?

- What Is The Short Term Policy Rate?

- Can I Change My Nominee In Term Insurance?

- The Evolution Of Term Life Insurance: Past, Present, And Future

- From Confusion To Clarity: How Harpreet Puri Guided A Client Through Complex Term Life Insurance Decisions

- Do Rich People Have Term Life Insurance?

- What Are The Common Term Life Insurance Clauses?

- What Are The Disadvantages Of Joint Term Insurance?

- What Is The Oldest Age At Which You Can Get Term Life Insurance?

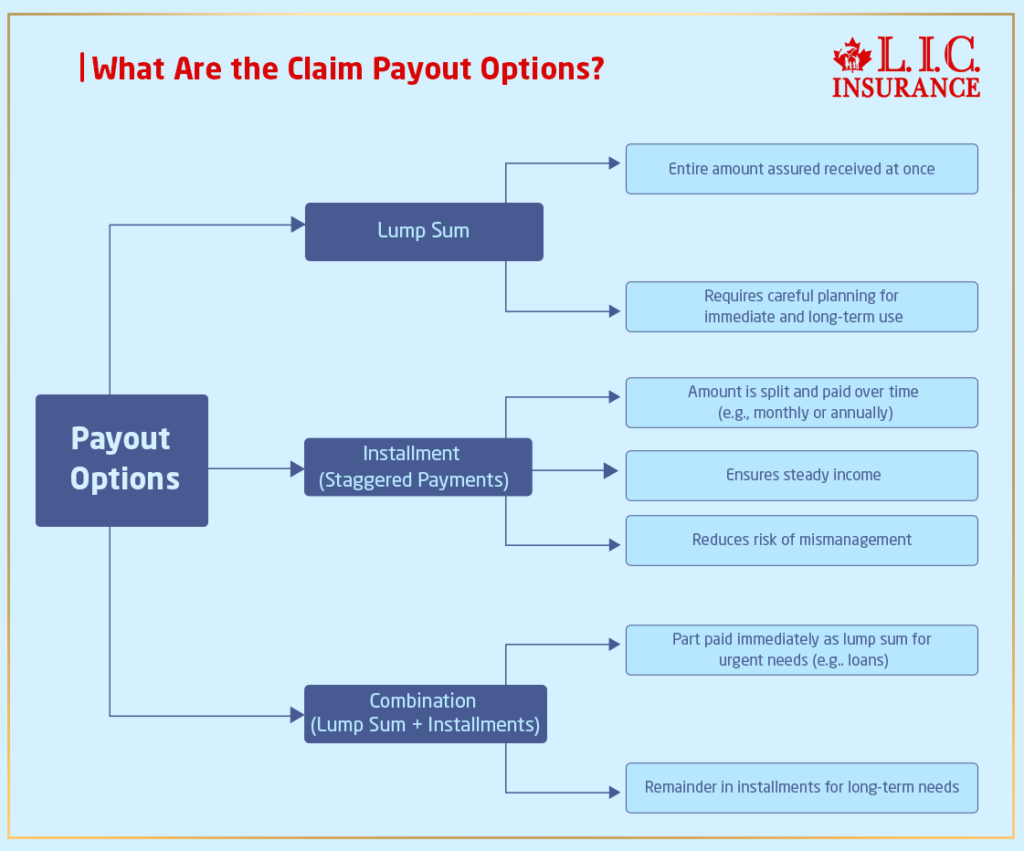

- How Do You Choose The Right Claim Payout Option For Your Term Insurance?

- Is There a Medical Exam for Term Life Insurance?

- Limited Pay vs Regular Pay Term Insurance

- When To Cancel Term Life Insurance?

- Best Term Life Insurance Plans For Couples

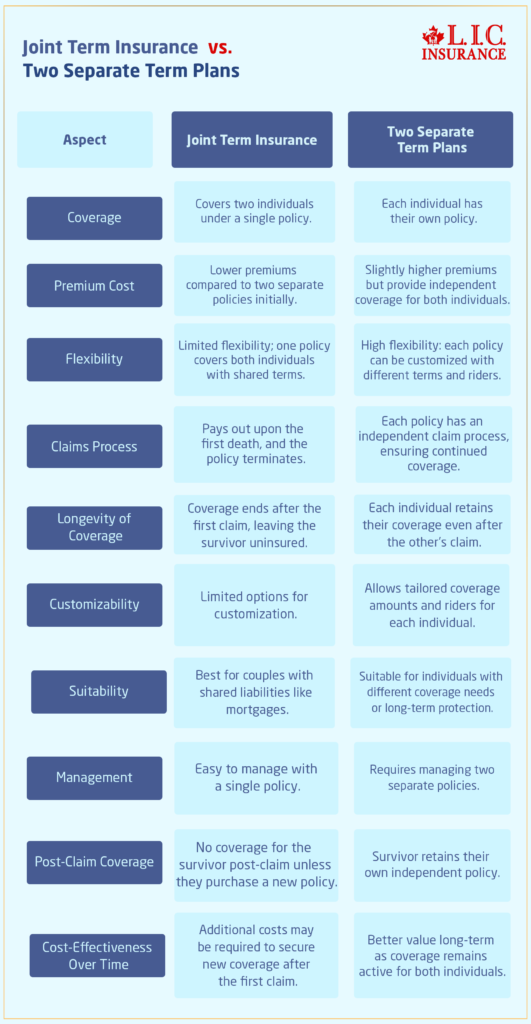

- Joint Term Insurance VS. Two Separate Term Plans

- Which Is Better – Term Insurance Or Health Insurance?

- Importance Of Accidental Total And Permanent Disability Rider With Term Insurance

- Why Are Term Life Insurance Claims Rejected

- What Type Of Risk Is Covered By Short Term Insurance?

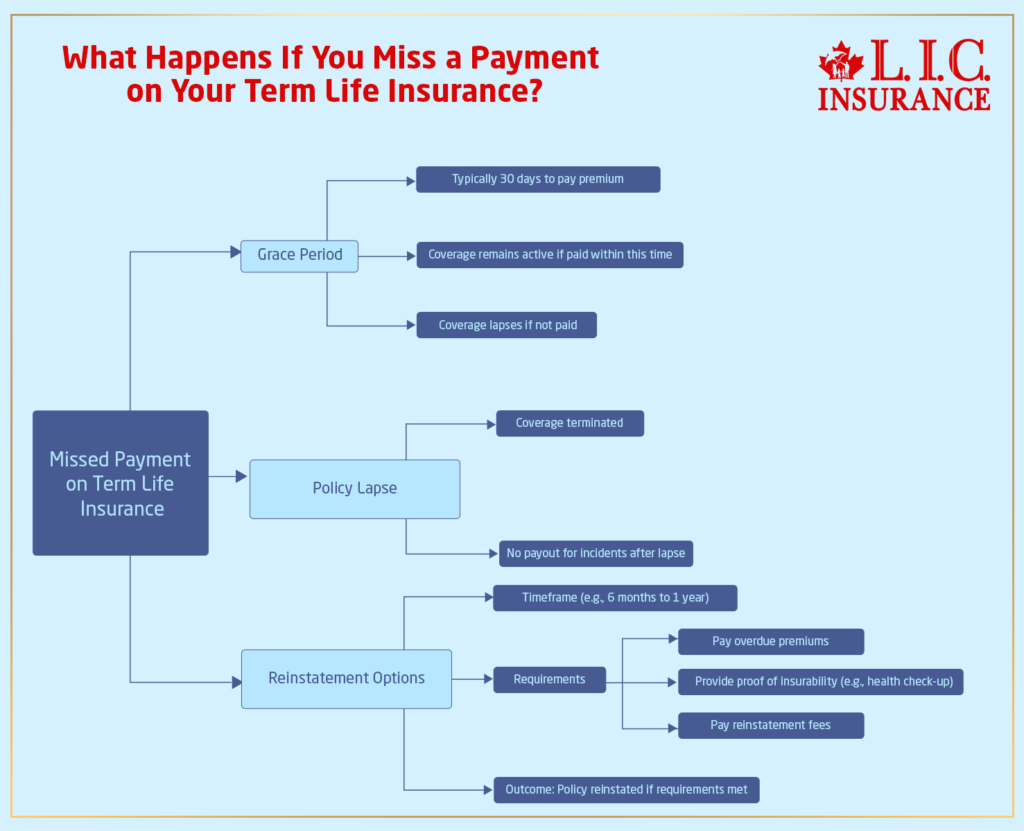

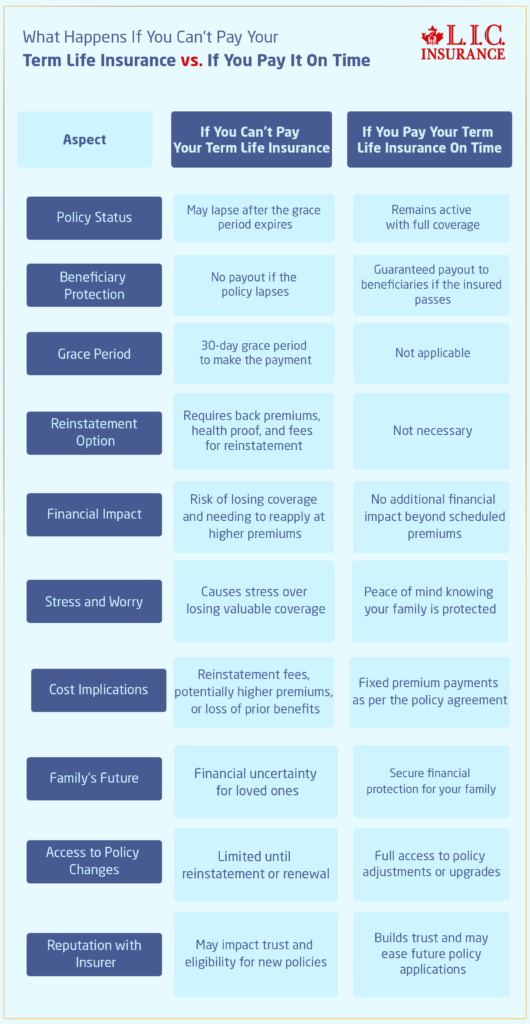

- What Happens If You Can’t Pay Your Term Life Insurance?

- What Will Disqualify You From Term Life Insurance?

- Can Riders Be Added To Term Life Insurance?

- Why Buy Term Life Insurance From An Insurance Broker?

- Why Not Buy Term Life Insurance From Banks?

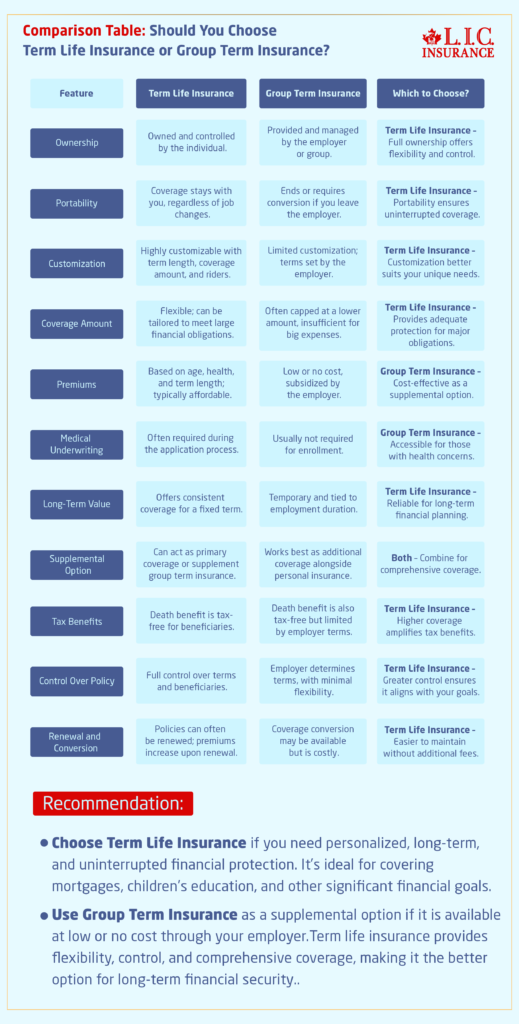

- What Is The Difference Between Term Insurance And Group Term Insurance?

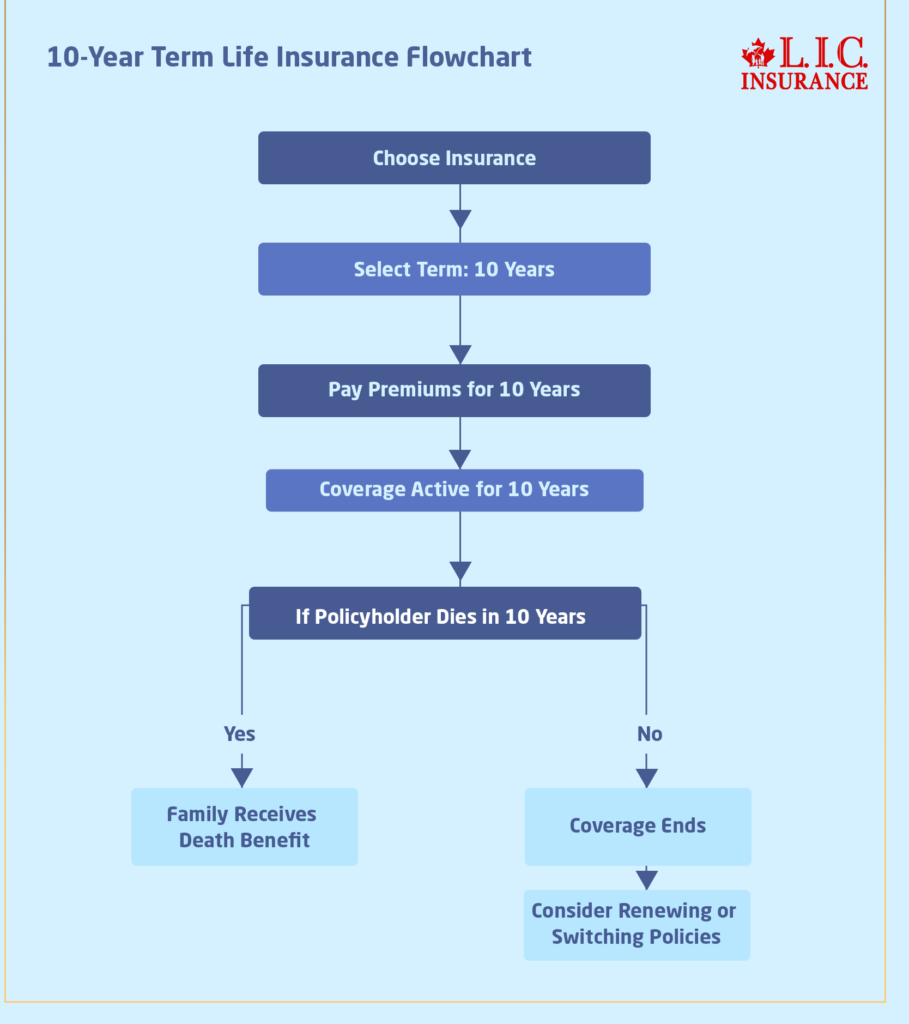

- Is There 10-Year Term Life Insurance?

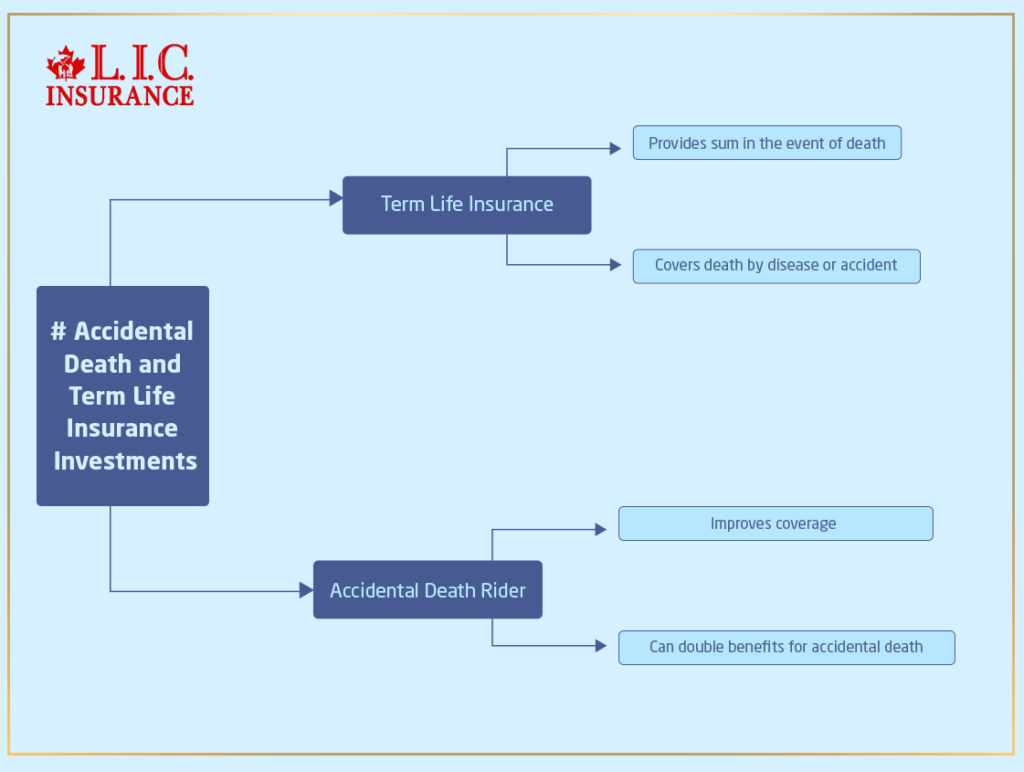

- Does the Term Life Cover Accidental Death?

- Is Buying a Term Plan Online Safe?

- When Does Term Life Insurance Payout?

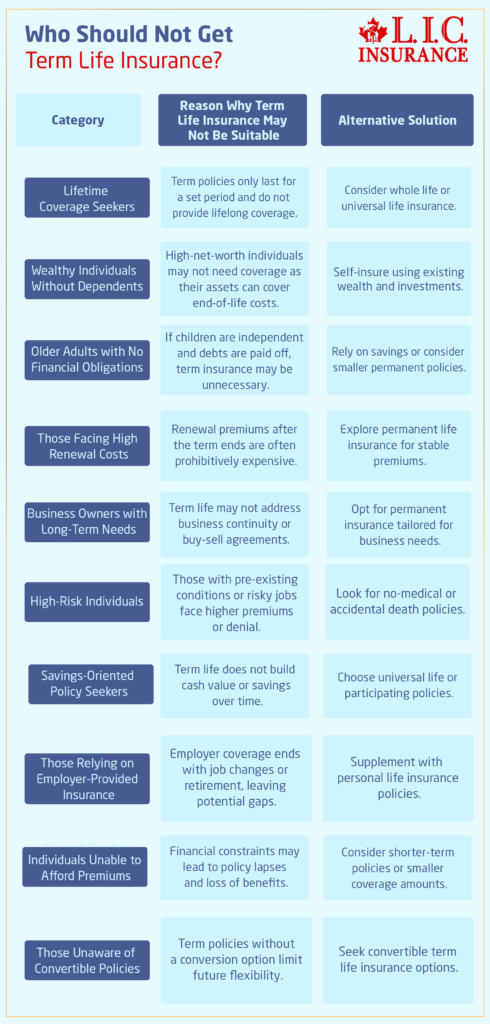

- Who Should Not Get Term Life Insurance?

- What Is the Maximum Limit in Term Insurance?

- What Are the 4 Types of Term Life Insurance?

- Can a Child Be the Owner of a Term Life Insurance Policy?

- Which Is Better, Term Insurance or SIP?

- What types of death are not covered in Term Insurance?

- Can I Pay Term Insurance Monthly?

- Pros and Cons of Buying Term Life Insurance Plans

- Can Term Life Insurance Be a Business Expense?

- What Happens When Term Life Insurance Expires?

- What Happens After 20 Years of Term Life Insurance?

- Can Term Life Insurance Be an Investment?

- Term Life Insurance Plan for All Age Groups

- What Does It Mean to Buy Term & Invest the Difference?

- How Do You Calculate Term Insurance Value?

- Why Is Term Life Insurance with a Return of Premium Option Not the Best Risk Coverage for You?

- Group Term Life Insurance & Individual Term Insurance: Know the Details

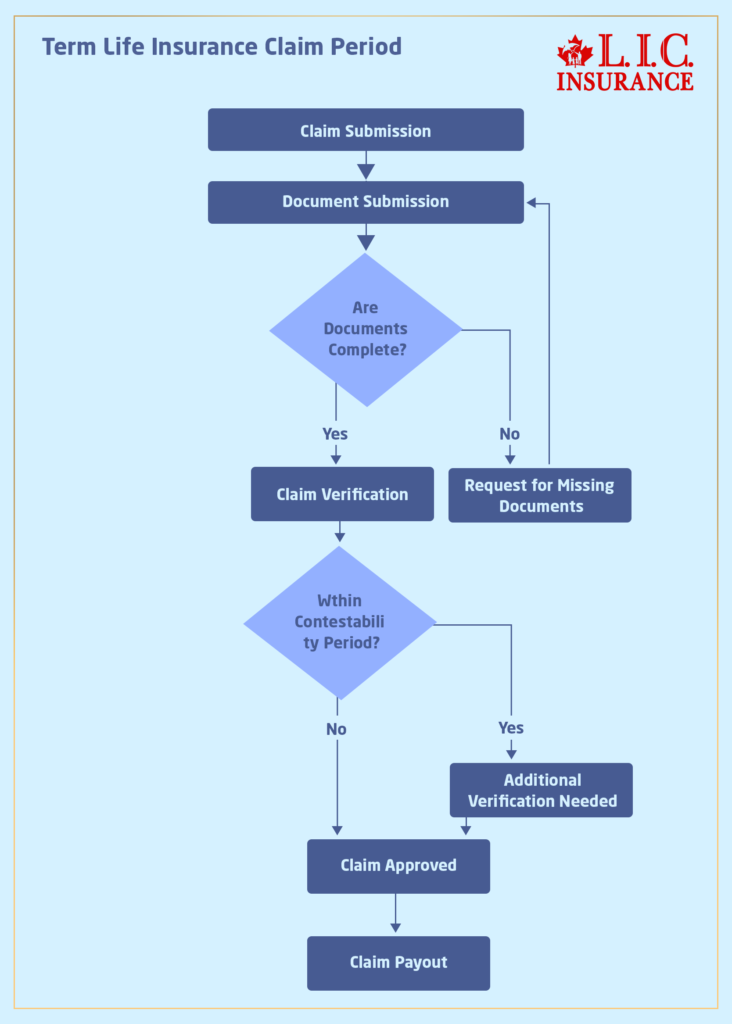

- What Is the Claim Period for Term Life Insurance?

- Can I Convert My Term Policy to Whole Life?

- Can You Use Term Life Insurance to Pay Off a Mortgage?

- Do Term Life Insurance Plans Offer Cash Value?

- What Happens to Term Insurance If the Nominee Dies?

- What Is the Shortest-Term Life Insurance Policy?

- What Is the Cheapest Term Life Insurance for Seniors Over 70?

- Who Benefits from Term Life Insurance?

- Can Term Insurance Be Rejected After Five Years?

- What Is the Longest Term Life Insurance?

- Does Term Insurance Automatically Renew?

- Can you extend a 20-Year Term Life Policy?

- Do I Get Money Back from Term Life Insurance?

- Can You Cash Out a Term Insurance Policy?

Frequently Asked Questions

Yes, a canadian Term Life Insurance Plan for smokers is available. Most insurers will work with smokers, but the cost could be higher. Even one client we spoke with said he was relieved to have a broker find him a plan more suitable for his financial needs.

Smokers will pay a higher fee for Canadian Term Life Insurance Policy than non-smokers. That is because smoking is associated with increased risks to health. Others told me that searching for quotes on the internet really opened their eyes to the price difference.

The process is explained by Term Life Insurance Brokers in Ontario, Canada, for smokers. They describe the underwriting process and assist in compiling health documents. One client said his broker demystified the application process by explaining each step.

Smokers typically pay higher premiums and go through more stringent medical checks. Clients are sometimes overwhelmed by the additional questions about their smoking habits. Brokers sort these issues and recommend ways to improve rates.

Survivorship Life Insurance, also known as a second-to-die policy, covers two lives and pays a death benefit after both people have died. For smokers, it means financial help for their loved ones if the worst comes to pass. Knowing that his family was protected assuaged one policyholder’s concerns.

Yes, you can pay less over time for smoking less. Some insurers let you “update” your health information if you demonstrate improvement. We have had clients get better quotes after quitting smoking.

Collect all your health records and be forthright about your smoking history. Check out September Term Life Insurance quotes in Canada and speak to experienced brokers. One client said his meticulous preparation allowed him to get the right coverage.

Sources and Further Reading

- Government of Canada – Life Insurance Regulations

https://www.canada.ca - Canadian Life and Health Insurance Association (CLHIA)

https://www.clhia.ca - Financial Consumer Agency of Canada – Understanding Life Insurance

https://www.canada.ca - Insurance Bureau of Canada – Term Life Insurance Explained

https://www.ibc.ca - Ontario Securities Commission – Choosing an Insurance Plan

https://www.getsmarteraboutmoney.ca - Life Insurance Canada – Smoker vs. Non-Smoker Insurance Rates

https://www.lifeinsurancecanada.com

Key Takeaways

- Smokers Can Get Term Life Insurance – Smoking does not disqualify applicants from getting a Canadian Term Life Insurance Plan, but it affects premiums.

- Smoker Classification Affects Costs – Insurers consider anyone who has used tobacco or nicotine in the last 12 months as a smoker, leading to higher Term Life Insurance Coverage costs.

- Premiums Are Higher for Smokers – Smokers typically pay two to four times more than non-smokers for the same Term Life Insurance Policy quotes Canada.

- Ways to Lower Insurance Costs – Comparing multiple insurers, improving overall health, opting for a medical exam, and quitting smoking can help reduce rates over time.

- Preferred Smoker Rates Exist – Some Term Life Insurance Brokers in Ontario Canada can help occasional smokers find preferred rates that are lower than standard smoker premiums.

- Switching to Non-Smoker Rates – Smokers who quit for 12 months can request reclassification and significantly lower their Term Life Insurance Plans costs.

- No Medical Exam Plans Are an Option – Smokers with health concerns can opt for no-medical-exam Term Life Insurance, but these policies come with higher premiums.

- Financial Protection is Essential – Despite higher premiums, securing Term Life Insurance Coverage ensures financial security for loved ones in case of unexpected events.

- Working With an Insurance Broker Helps – Experienced Term Life Insurance Brokers in Ontario, Canada, can guide smokers in finding affordable coverage and future savings.

- Starting Early is Beneficial – The younger a smoker applies for a Term Life Insurance Plan, the lower the premiums, making it essential to act sooner rather than later.

Your Feedback Is Very Important To Us

Thank you for taking a moment to share your thoughts. We value your input and want to learn about your challenges in choosing the best Term Insurance amount. Your feedback helps us serve you better.

Thank you for your feedback! Your responses will help us improve how we assist smokers in finding the best Life Insurance Coverage in Canada. We will reach out to you soon with tailored solutions.

IN THIS ARTICLE

- Can A Smoker Get Term Life Insurance?

- Understanding Term Life Insurance

- How Smoking Affects Term Life Insurance

- The Medical Underwriting Process

- Higher Life Insurance Premiums: What to Expect

- Securing a Canadian Term Life Insurance Plan as a Smoker

- Real-Life Struggle Stories from the Field

- Benefits of Term Life Insurance for Smokers

- Navigating the Application Process

- Challenges and Considerations for Smokers

- Success Stories and Lessons Learned