BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Missed The RRSP Deadline? Here’s Exactly What To Do Next

By Pushpinder Puri

CEO & Founder

- 10 min read

- April 29th, 2026

SUMMARY

Missing the RRSP deadline doesn’t end your tax planning options. The discussion covers the RRSP contribution deadline, how RRSP contributions and contribution room work, ways to maximize RRSP contributions, manage RRSP tax benefits, and plan a Canadian Registered Retirement Savings Plan using carry forward strategies, CRA data, and smart timing based on income and tax year decisions.

Introduction

Realizing you missed the RRSP deadline after tax season can be frustrating. It happens to a lot of Canadians. Canadians have millions of RRSP contribution rooms sitting unused on a yearly basis that are not yet allocated to millions of Canadians, as data published by the Canada Revenue Agency indicates that billions of dollars are sitting unclaimed within the Canadian Registered Retirement Savings Plan regime. That makes us understand one thing: it is not uncommon to miss the deadline of RRSP contribution – and it is not the end of your tax strategy.

We observe this in our daily practice during the spring. This was the case of smart, industrious Canadians with good income, good intentions, and busy schedules who just lacked time. The good news? The fact that you have missed the deadline for submitting your RRSP does not imply that you have missed the chance to accumulate tax savings, a retirement fund, or the ability to live comfortably in the long run. It simply indicates strategy changes.

We will go step by step, then, on what to do next, calmly, clearly, and correctly.

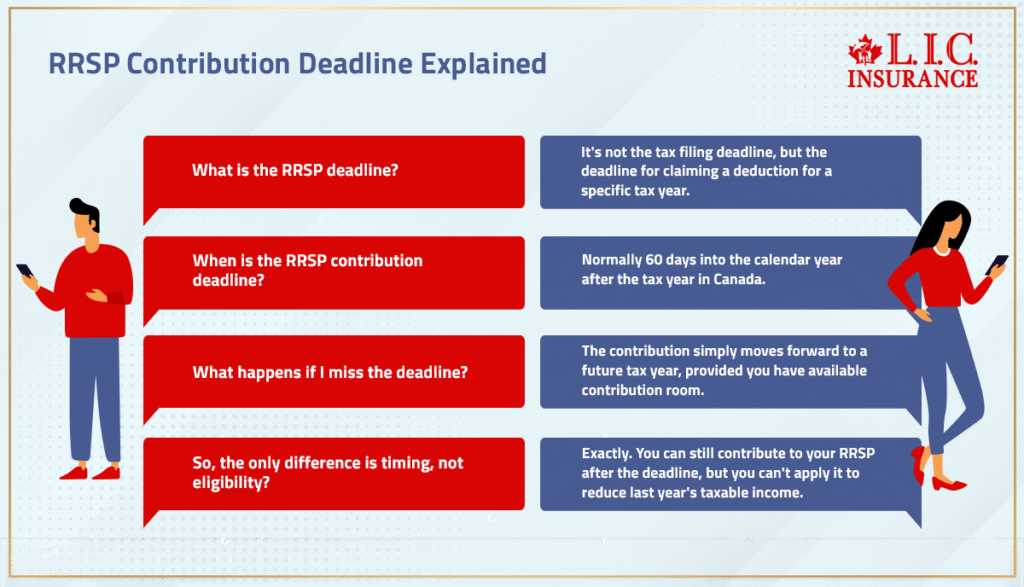

What The RRSP Deadline Actually Means For Your Taxes

The deadline for RRSPs is also misconstrued. It is not the deadline for tax filing. It is a deadline for claiming a deduction for a particular tax year.

The deadline for contributions to the RRSP is normally 60 days into the calendar year after the tax year in Canada. The contributions prior to this date can be deducted from the former year’s income on income tax. Miss that window, and the contribution merely moves forward.

Here’s the key point:

The only difference is timing — not eligibility.

You can still contribute to your RRSP after the deadline. You just can’t apply that contribution to reduce last year’s taxable income. It will apply to a future tax year instead, provided you have available contribution room.

Missed The RRSP Deadline: What You Can Still Do Immediately

mistake we see is rushing into last-minute contributions without understanding the numbers.

Here’s what still makes sense right away:

- Confirm your available contribution room

- Review your tax bill before deciding how much to contribute

- Avoid panic deposits that create an excess amount

- Shift focus to the current and upcoming tax year

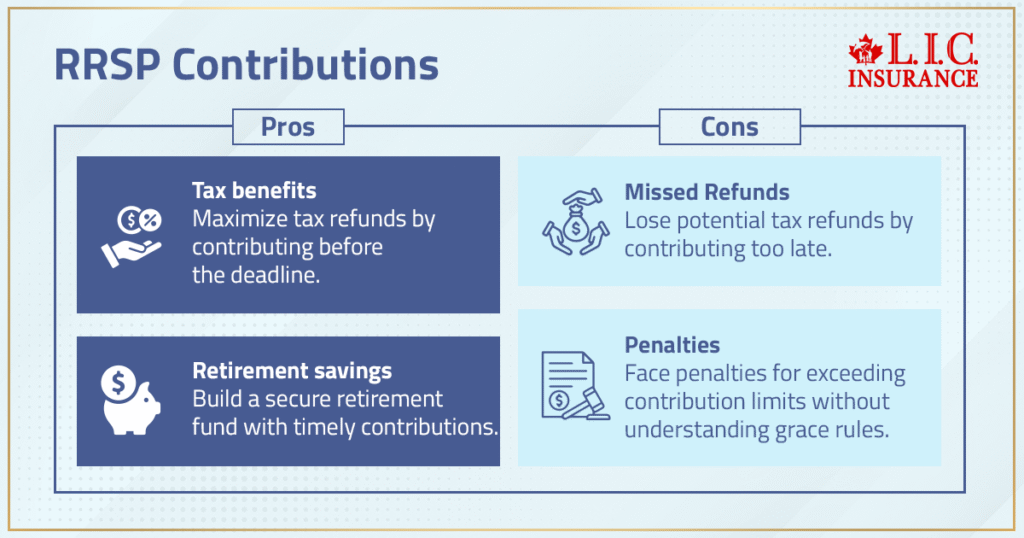

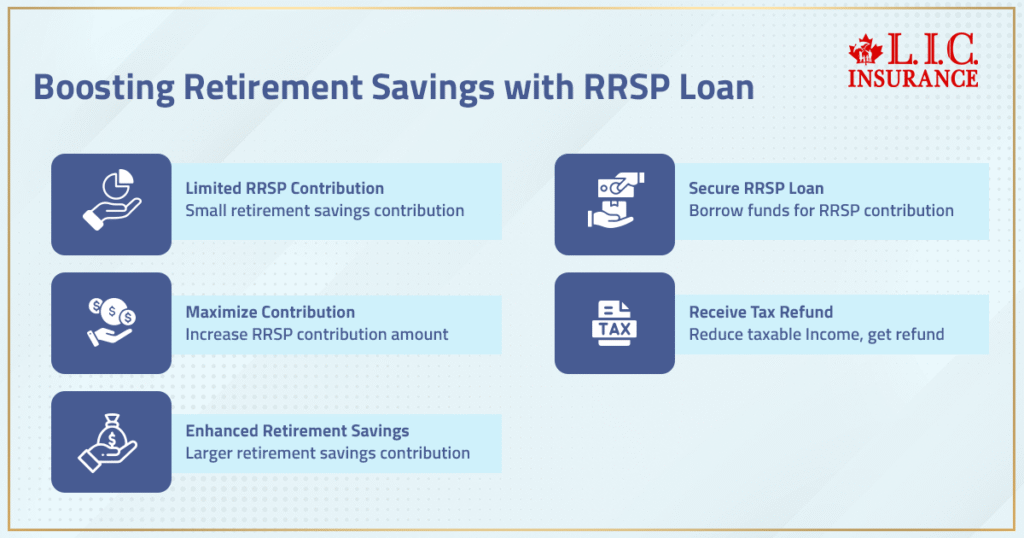

Yes, you may have to pay tax for the prior year without the RRSP deduction. But contributing strategically now can still reduce future taxes and strengthen long-term retirement savings.

Missing the RRSP isn’t a failure — it’s a planning reset.

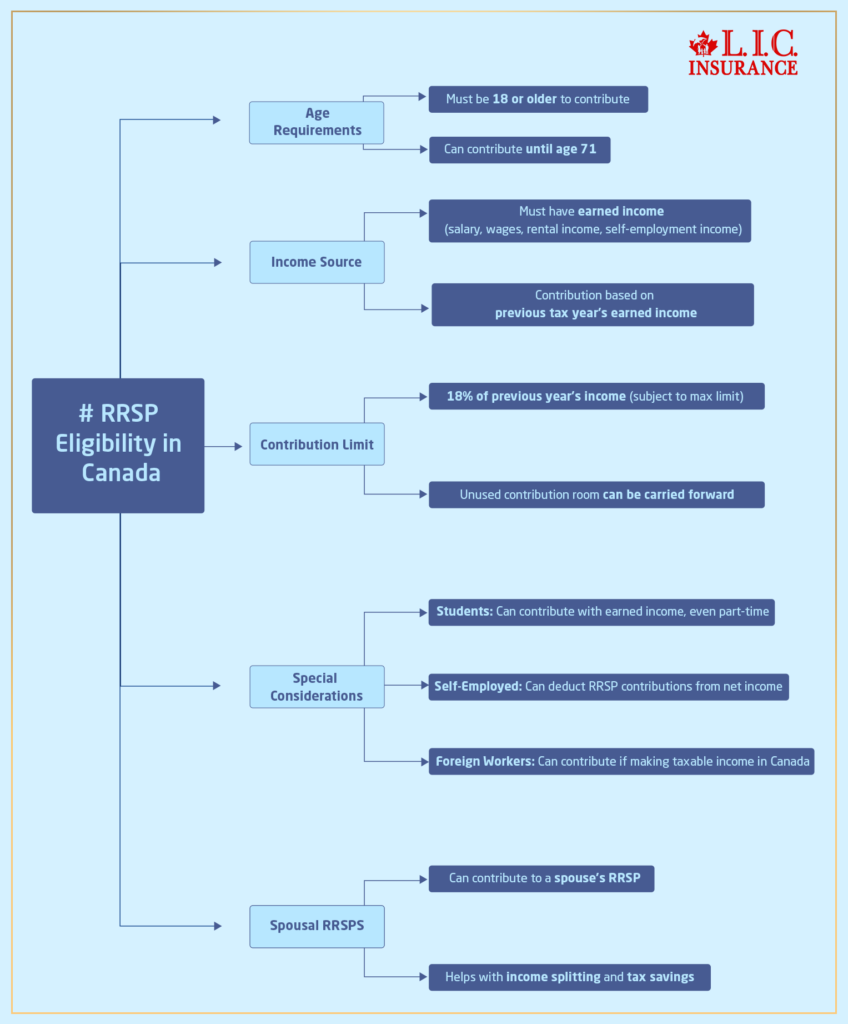

RRSP Contributions And How Contribution Room Really Works

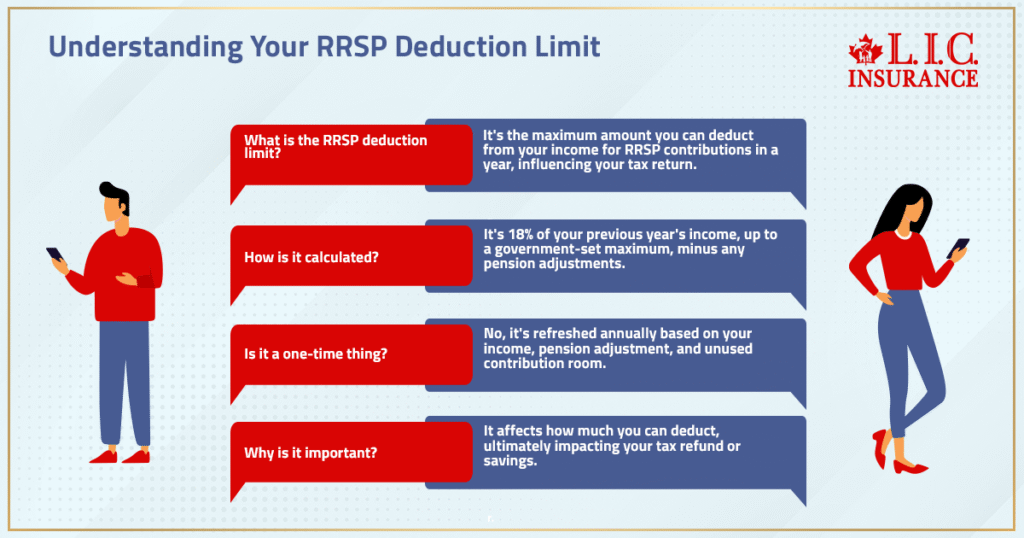

Contribution room, not emotions, regulates the RRSP contributions. The amount of your RRSP contribution room is calculated according to the amount of earnings you earned in the previous year, but is limited to the amount stipulated by the federal government annually.

The contribution room builds up. When you do not use it, it does not fade away. It is a continuation that cannot end.

This forms what is referred to as the unused RRSP contribution room, or the unused contribution room – one of the least used planning instruments in Canada.

We have been discussing Notices of Assessment on which clients have five, ten, or even fifteen years of unused room awaiting to be put into strategic deployment.

Understanding The RRSP Contribution Limit And Deduction Rules

The RRSP contribution limit changes annually and is tied to earned income. The annual contribution limit is capped, even if your income is high.

Important distinction:

- You can contribute up to your contribution limit

- You can deduct only up to your RRSP deduction limit

Exceeding the limit results in an excess amount, which triggers a penalty tax of 1% per month on the excess amount.

This has occurred when individuals have guessed rather than checked their numbers. RRSPs that are over-contributed to gradually drain cash until they are fixed.

This is the reason why the decision on contribution must always be related to CRA data, rather than estimates.

How The Canada Revenue Agency Tracks Your RRSP Room

The Canada Revenue Agency is the final authority on your Registered Retirement Savings Plan limits — not your bank, not your investment platform, and not memory.

Your Notice of Assessment outlines:

- RRSP contribution room

- RRSP deduction limit

- Unused room carried forward

- Any excess amount warnings

The Canada Revenue Agency CRA updates these figures every year after your tax return is processed. That’s why relying on last year’s numbers without checking your latest assessment can create errors.

Contribution Room Strategies After You Missed The RRSP

Once the deadline passes, planning becomes more flexible — not less.

You can still:

- Make a lump sum contribution when cash flow allows

- Set up monthly contributions to build discipline

- Use regular contributions to smooth market risk

- Align deposits with evolving financial goals

This approach often works better than rushed, deadline-driven decisions. The contribution room didn’t vanish — it simply waits for smarter timing.

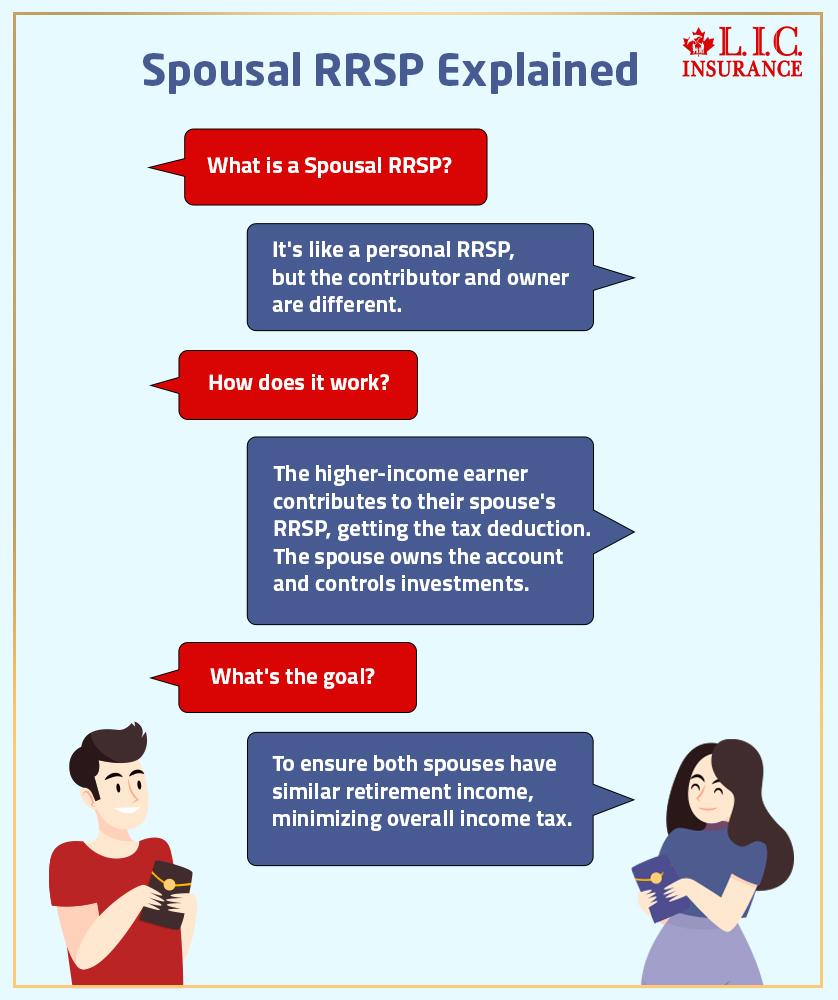

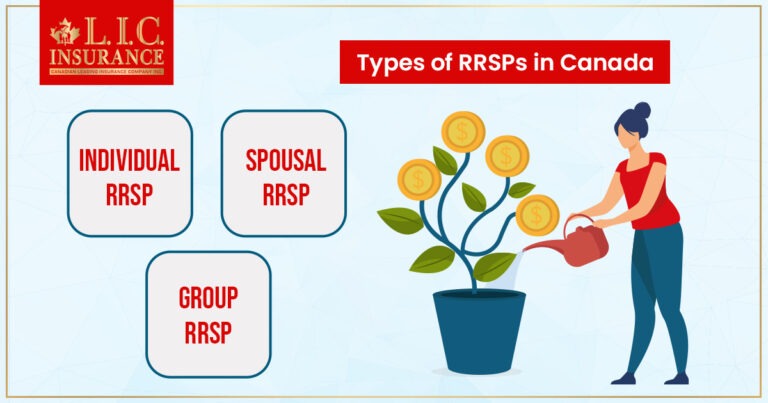

Spousal RRSPs And Common Law Partner Planning After A Missed Deadline

Spousal RRSP is one of the most effective income-sharing tools for partners (married or common-law).

Although not generally binding, a contribution to the RRSP of a common-law partner can equalize future retirement income, particularly where one of the partners is in a higher tax bracket.

Partners retain their own RRSP, yet it is possible to make contributions strategically so as to minimize tax payouts in the long run.

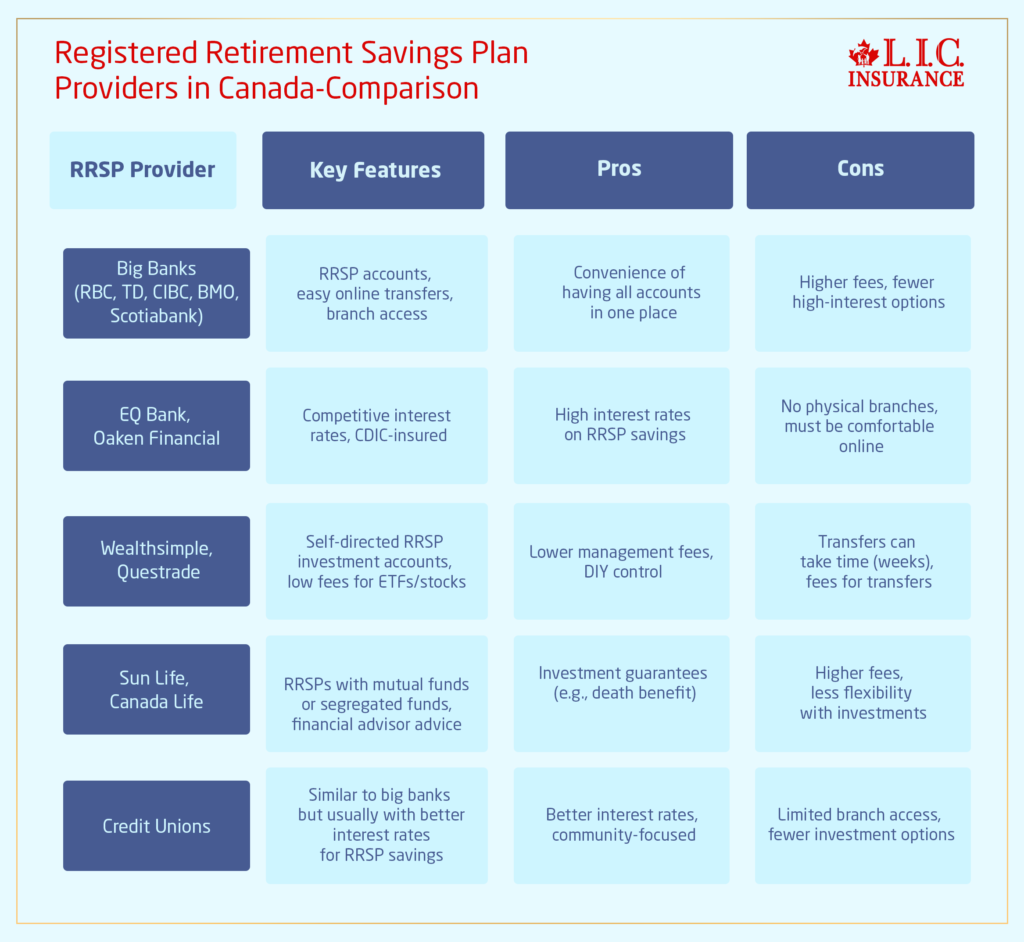

RRSP Investment Choices That Still Matter After The Deadline

Missing the deadline doesn’t reduce the importance of what you invest in.

RRSPs can hold a wide range of qualified investments, including:

- Mutual funds

- Guaranteed investment certificates

- Diversified portfolios built for tax-deferred growth

Your RRSP portfolio should reflect time horizon, risk tolerance, and income stability — not calendar pressure.

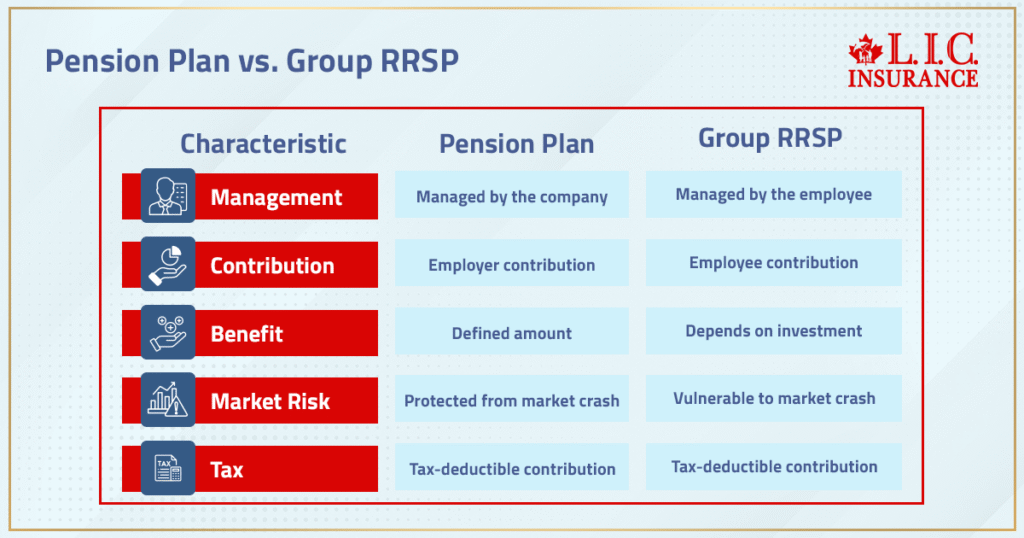

Employer-Sponsored Plans And Pension Plan Coordination

A good number of Canadians make contributions through employer-sponsored programs or contribute to a workplace-sponsored pension. These take away some RRSP space rather than the planning opportunities.

RRSPs continue to have a role to play in addition to pensions, particularly when one is moving into a registered retirement income fund in their later life.

Coordination is important – particularly to middle-career workers.

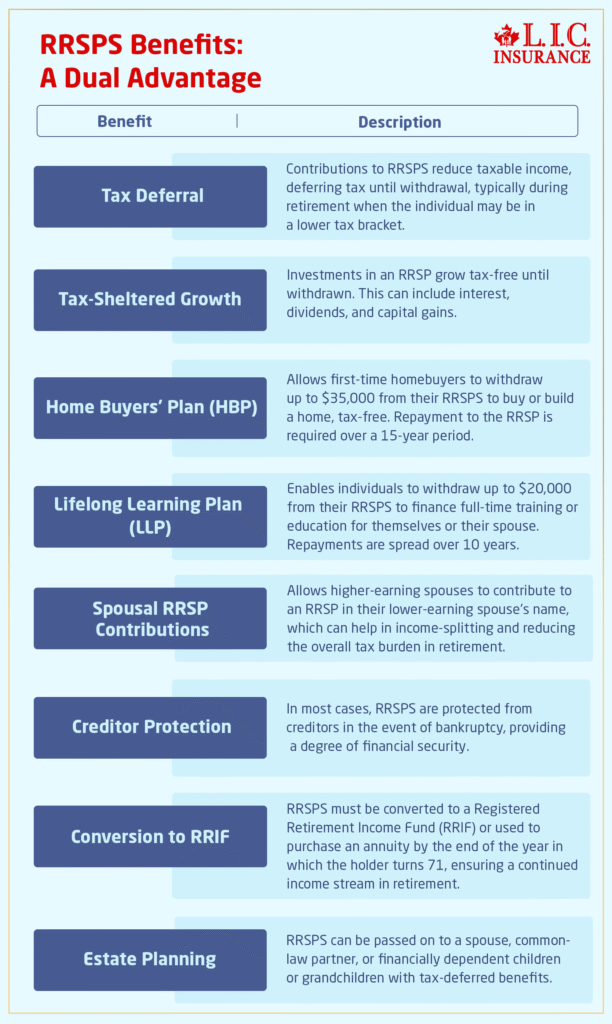

How RRSP Tax Benefits Actually Reduce Your Tax Bill

The real power of RRSPs lies in the RRSP tax benefits.

RRSP contributions create a tax deduction, reducing taxable income. This leads to tax savings, particularly for Canadians facing higher marginal tax rates.

In simple terms:

- Higher income year = more benefit

- Lower income year = less benefit

Used properly, RRSPs mean less tax, not just deferred tax.

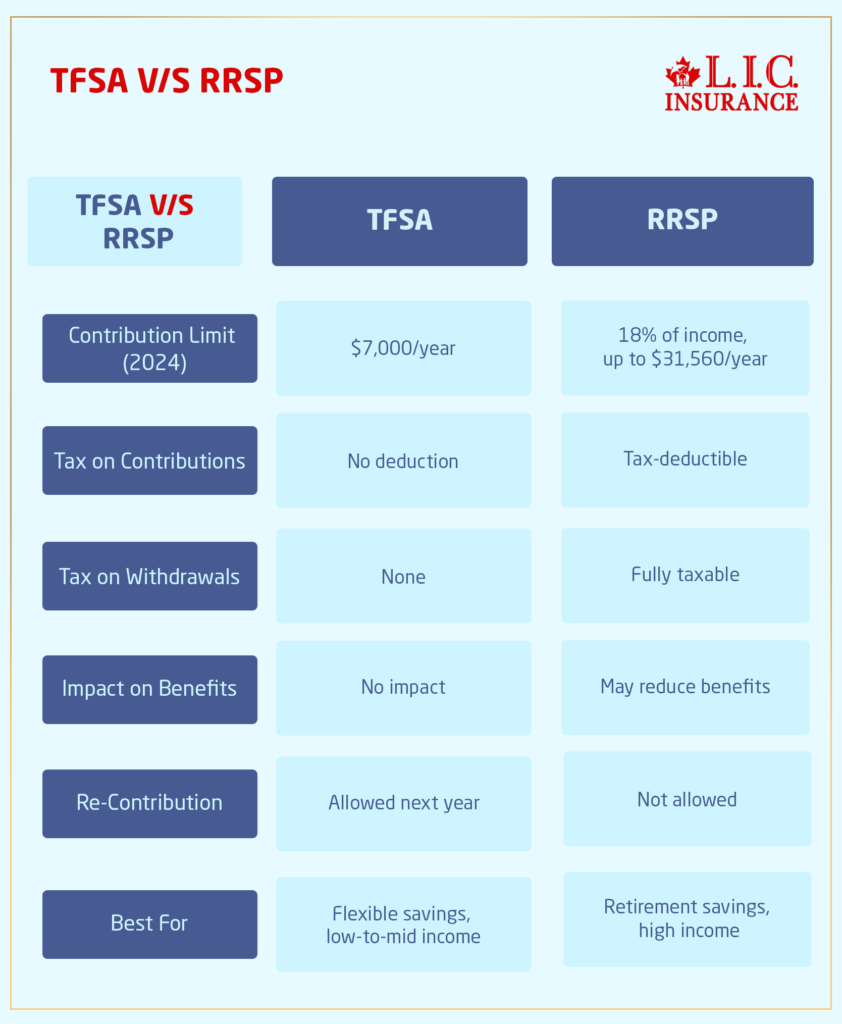

TFSA Vs RRSP When The Deadline Is Missed

A tax-free savings account can prove to be a better short-term action when the RRSP deadline is not met.

TFSAs are not tax-deductible, but withdrawals are tax-free. This is temporarily effective compared to RRSPs among some Canadians, particularly those whose income is not very stable.

Otherwise, the gap is closed by a non-registered account.

The option is a matter of timing, income, and a long-term retirement savings plan.

Home Buyers Plan And Lifelong Learning Plan Considerations

RRSPs interrelate with such programs as the Home Buyers’ Plan and Lifelong Learning Plan.

Both will enable you to access funds in RRSPs without immediate taxation, but there are repayment policies. Defaulted repayments are turned into RRSP withdrawals and raise the taxable income.

Such programs ought to be laid down in a well-thought-out manner and not superimposed on missed deadlines without reexamination.

Common RRSP Mistakes After Missing The Deadline

From our experience, the most costly mistakes include:

- Guessing the contribution room

- Ignoring CRA warnings

- Creating an excess amount

- Triggering unnecessary penalty tax

- Making emotional contributions to offset a tax bill

RRSP planning works best when it’s deliberate — not reactive.

How Canadian LIC Helps Clients Maximize RRSP Contributions Going Forward

We do not make RRSPs a one-year decision. Our clients get to maximize the RRSP using year-round planning to optimize income to make the best use of taxes and long-term objectives.

It can be checking contribution room, working with a tax consultant, or assisting clients in asking an RRSP quote online, and the attention remains on strategy and not stress.

Moving Forward With Confidence

Failure to meet the deadline of the RRSP does not cancel your future. You are still a Canadian resident and have at your disposal one of the most powerful retirement systems in the world.

RRSPs will keep the long-term retirement income, even smarter tax results, and sustainable wealth even where the calendar fails.

It is not what transpired last month that is of the highest priority. It’s what you do next.

FAQs

Yes, but the timing changes. The contributions to RRSP after the RRSP deadline will not lower the taxable income of the previous year. They can still receive the RRSP tax benefits in a subsequent tax year, and this will assist in lowering their tax bill in a time when the income or marginal tax rate is higher.

No. Even when you have missed the RRSP contribution deadline, your contribution room in the RRSP will not be lost. All of the unused contribution room in RRSPs will be brought forward and can be utilized in subsequent years without penalty, provided you remain within the limit on contributions.

Yes. You are allowed to make a contribution to your RRSP and have the tax deduction claimed in a future tax year. The plan is effective when you think you will earn more income or when you expect to receive more tax benefits in the future.

The unused RRSP contribution room and your RRSP deduction limit are indicated on your Notice of Assessment provided by the Canada Revenue Agency CRA. Always use CRA records, rather than estimates, to prevent an over-contributed situation and penalty tax treatment.

It relies on the cash flow and financial objectives. A lump sum may be helpful following a bonus or windfall, whereas monthly deposits assist in stabilizing an annual retirement savings and lessen the danger of timing the market in your RRSP portfolio.

Yes. The spousal RRSP or the RRSP of a common-law partner may be a contribution made after the deadline. This strategy is used to plan the long-term retirement income and minimize income tax in cases where one of the partners earns a high income consistently.

In some cases, yes. A tax-free savings account can work in case of low income in the short term or when there is a need to be flexible. RRSPs are still superior in terms of tax deferral growth in cases where the income, contribution room, and tax brackets are properly matched.

Any amount over the contribution limit imposed would attract a penalty tax. Canada Revenue Agency permits some grace, but the ones that persistently exceed can silently increase your tax bill to the point of rectification.

Yes. Participation in pension plans and employer-sponsored plans has diminished RRSP contribution space. This is why it is important to review your Notice of Assessment every tax year to make RRSP contributions or carry forward plan beforehand.

When there is a variation in income, deductions are postponed, or past years exhibited significant unused contribution space, a discussion with a tax advisor provides a way to synchronize contributions to RRSP with the result of income tax and long-term retirement savings.

Sources and Further Reading

- Canada Revenue Agency (CRA)

RRSP contribution limits, deduction rules, over-contribution penalties, Notices of Assessment

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans.html - Canada Revenue Agency – RRSP Guide T4040

Official CRA guide covering RRSP contributions, carry forward rules, spousal RRSPs, and withdrawals

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4040.html - Statistics Canada

Data on retirement savings behaviour, income trends, and unused RRSP contribution room

https://www.statcan.gc.ca - Department of Finance Canada

Federal rules on annual RRSP contribution limits and registered retirement savings policy

https://www.canada.ca/en/department-finance - Office of the Superintendent of Financial Institutions (OSFI)

Oversight and regulation of federally registered financial institutions offering RRSP products

https://www.osfi-bsif.gc.ca - Government of Canada – Lifelong Learning Plan (LLP)

RRSP withdrawal rules for education funding

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/lifelong-learning-plan.html

Key Takeaways

- Missing the RRSP deadline does not eliminate your ability to build tax savings. RRSP contributions can still support long-term retirement planning when contribution room and timing are managed correctly.

- The RRSP contribution deadline only affects when a tax deduction can be claimed, not whether you can contribute to a Canadian Registered Retirement Savings Plan in the current tax year.

- Unused RRSP contribution room continues to carry forward, allowing future RRSP contributions without losing eligibility or triggering penalty tax when limits are respected.

- Reviewing your Notice of Assessment from the Canada Revenue Agency helps prevent over contributed amounts and ensures RRSP planning aligns with verified contribution limits.

- RRSP tax benefits are most effective when contributions match income levels, marginal tax rates, and long-term retirement income goals rather than last-minute tax pressure.

- Strategic options such as spousal RRSPs, lump sum deposits, and regular contributions help maximize RRSP contributions even after a missed contribution deadline.

- Aligning RRSP planning with employer-sponsored plans, pension participation, and TFSA use creates stronger overall retirement savings outcomes.

Your Feedback Is Very Important To Us

Your responses help us create clearer guidance for Canadians dealing with RRSP timing, taxes, and retirement planning.

Closing Note

Your feedback helps improve future guidance on RRSP deadlines, contribution planning, and long-term retirement savings for Canadians.

IN THIS ARTICLE

- Missed The RRSP Deadline? Here’s Exactly What To Do Next

- What The RRSP Deadline Actually Means For Your Taxes

- Missed The RRSP Deadline: What You Can Still Do Immediately

- RRSP Contributions And How Contribution Room Really Works

- Understanding The RRSP Contribution Limit And Deduction Rules

- How The Canada Revenue Agency Tracks Your RRSP Room

- Contribution Room Strategies After You Missed The RRSP

- Spousal RRSPs And Common Law Partner Planning After A Missed Deadline

- RRSP Investment Choices That Still Matter After The Deadline

- Employer-Sponsored Plans And Pension Plan Coordination

- How RRSP Tax Benefits Actually Reduce Your Tax Bill

- TFSA Vs RRSP When The Deadline Is Missed

- Home Buyers Plan And Lifelong Learning Plan Considerations

- Common RRSP Mistakes After Missing The Deadline

- How Canadian LIC Helps Clients Maximize RRSP Contributions Going Forward

- Moving Forward With Confidence