- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- Is there a penalty for cancelling Term Life Insurance?

- Why Do People Cancel Their Term Life Insurance?

- Does Cancelling a Term Life Insurance Policy Involve a Penalty?

- What Happens to Your Beneficiaries if You Cancel Your Term Life Insurance?

- Alternatives to Cancelling Your Term Life Insurance

- When Should You Cancel Your Term Life Insurance?

- How to Cancel Your Term Life Insurance Policy

- More on Term Life Insurance

Who Is Eligible For RRSP In Canada?

By Pushpinder Puri

CEO & Founder

- 11 min read

- March 14th, 2025

SUMMARY

This blog explains who is eligible for an RRSP in Canada, detailing age requirements, income sources, contribution limits, and special cases like spousal RRSPs. It also highlights strategies for maximizing RRSP contributions and the tax benefits of using an RRSP for retirement savings. Additionally, the blog discusses how RRSPs work alongside Term Life Insurance and provides practical tips on getting the best Term Life Insurance quotes online to complement your financial planning.

Introduction

Are you hoping to make your future more financially secure? RRSPs are a registered retirement savings tool in Canada used by millions of people for retirement while getting tax benefits. However, one of the most frequently asked questions Canadians ask is: Who can contribute to RRSP?

When you first hear about RRSPs, it just sounds like some complex financial product, like trying to understand a Term Life Insurance policy. Both have valuable long-term benefits, but determining how they play into the overall picture of your finances can be confusing. In this blog, we’ll cover who is eligible for RRSP contributions, some budgeting tips, and how you can take advantage of this tool to have a more secure financial future.

At the end of this post, you will learn not only who is eligible for an RRSP but also how to effectively use your RRSP to maximize the amount of retirement income you have and the amount of money you save on taxes!

What is an RRSP, and Why Should You Consider It?

Before we get into RRSP eligibility criteria, let’s start with what exactly an RRSP is and what it does for you.

An RRSP is a retirement savings account for Canadians. RRSP contributions are tax-deductible — you can offset your taxable income in the same year you contribute. This allows you to save tax immediately. The cash in your RRSP compounds tax-free until you take it out, normally in retirement when your income may be in a lower tax bracket.

The tax-deferred growth of an RRSP can be a powerful tool for anyone saving for retirement. But in order to take full advantage of an RRSP to save for the future, you need to know the eligibility rules so that you can contribute.

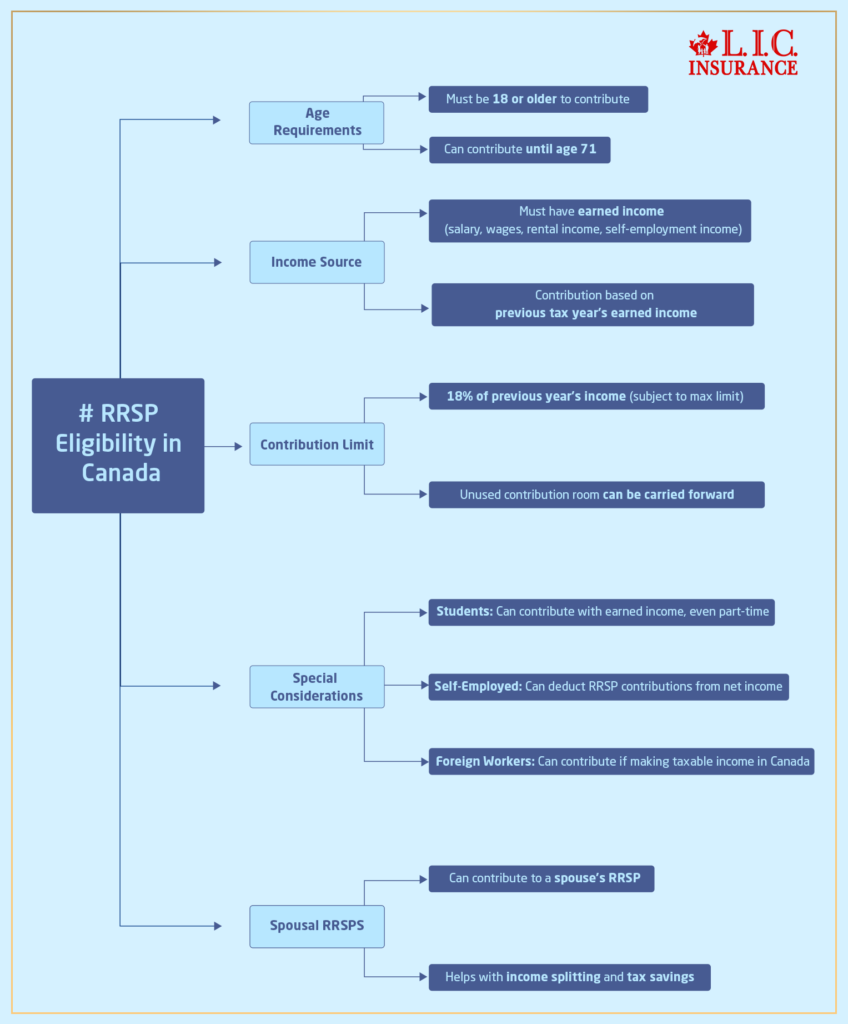

Who is Eligible for RRSP in Canada?

Understanding who can contribute to an Registered Retirement Savings Plan is crucial to making the most of this savings tool. The eligibility requirements are relatively straightforward but include some important exceptions and conditions.

1. Age Requirements:

- Age: You must be 18 or older to open and contribute to an RRSP. This is the full withdrawal age, allowing you to benefit from RRSP contributions.

- Under 71: You can make contributions to an RRSP until you turn 71. After that, contributions have to cease, but the money sitting in your RRSP can sit there and compound tax-deferred.

2. Income Source:

- Anyone with earned income can make RRSP contributions. This includes salary, wages, rental income and all other taxable income from employment or contracting. You can contribute to an RRSP if you have earned income.

- But in order to add to an RRSP, you need to have earned income in the previous tax year. Your maximum contribution to an RRSP is tied to your earned income from the previous year.

3. Contribution Limit:

- The contribution room for an RRSP is usually 18% of your income from the previous tax year, subject to a government-declared maximum amount. For example, for the 2025 tax year, the maximum contribution is $32,490.

- If you don’t max out the allowable contribution in a particular year, you may carry over the unused contribution room to future years. This offers you additional flexibility in future years where you may want to contribute more.

4. Special Considerations for Certain Groups:

- Students: You may also deduct contributions to an RRSP even if you’re a student and have limited income, as long as you earned income. This is an excellent way to begin to build your retirement savings early, even if only doing part-time jobs. While most students wouldn’t consider Term Life Insurance in their early years, it is possible to add up baby steps such as monthly RRSP contributions with Term Life Insurance quotes to preserve financial security well into the future.

- Self-Employed: Self-employed Canadian residents can deduct RRSP contributions from net income from self-employment. It works the same as with employees, but you’ll declare your self-employment income when you file your taxes and that will determine your RRSP contribution room.

- About RRSPs and foreign workers in Canada: A non-resident can also contribute to an RRSP but must also meet the same requirements as a Canadian resident. To qualify, you’ll have to make taxable income in Canada.

5. Spousal RRSPs:

- You can also put money into your spouse’s RRSP if you are married or in a common-law relationship. This is called a spousal RRSP and can be beneficial to making income splitting between you and your spouse work so that you can pay less overall tax if one of you is in a higher tax bracket than the other. This is a great way for couples to maximize their retirement savings and lower their overall tax burdens.

Special Cases and Eligibility for RRSPs

While the general eligibility for an RRSP is clear, there are some unique situations that might affect your ability to contribute or the amount you can contribute.

1. Students and Early Career Professionals:

If you’re a student or in the early stages of your career, you might not have a lot of earned income. However, you can still take advantage of RRSP contributions by saving small amounts. The tax-deferral benefits of an RRSP are especially useful when starting early in your career.

2. Retirees:

If you’re over 71 but still working or receiving earned income, you can continue contributing to your RRSP. However, once you turn 71, you must either convert your RRSP to a Registered Retirement Income Fund (RRIF) or use other retirement savings options.

How to Maximize Your RRSP Contributions

To truly benefit from an RRSP, it’s not just about contributing; it’s about maximizing your contributions. Here are a few strategies you can use to get the most out of your RRSP:

1. Contribute Early and Regularly:

The earlier you start contributing to your RRSP, the more you benefit from tax-deferred growth. Contributing regularly—whether monthly or annually—ensures that you’re consistently building wealth for retirement.

2. Catch Up with Unused Contribution Room:

If you haven’t contributed the full limit in past years, you can carry over unused contribution room to future years. This allows you to contribute more in years when you can afford to.

3. Use Spousal RRSPs to Split Income:

If one spouse is in a higher tax bracket, using a spousal RRSP can help reduce the overall tax burden. The lower-income spouse contributes to the spousal RRSP, and the funds will be taxed at their lower rate when withdrawn.

4. Avoid Over-Contribution:

While RRSPs offer a lot of flexibility, it’s important to avoid over-contributing. The Canada Revenue Agency (CRA) allows a small buffer (up to $2,000) over your limit without penalty, but any contributions above that can lead to a penalty tax of 1% per month on the excess amount.

RRSP Withdrawals and Tax Implications

Although the basic eligibility for an RRSP is straightforward, there are some special circumstances that can limit your ability to contribute or the amount of contribution you can make.

- Students & Early Career Professionals: If you’re still a student or are just starting your career, you may not have much in terms of earned income. Still, you don’t need to invest large sums to benefit from RRSP contributions and extend your savings. The RRSP tax-deferral advantages are particularly advantageous when begun early in your career.

- Retirees: If you turned 71 last December or earlier but are still working or continuing to earn income, you can still contribute to your RRSP. Once you reach age 71, however, you have to either convert your RRSP to a Registered Retirement Income Fund (RRIF) or to other retirement savings options.

- Maximize your RRSP contributions: It’s not just about making contributions; it’s about maximizing them. There are several things you can do to maximize your RRSP:

- Participate in the early stages and on an ongoing basis: If you wait until you are older to contribute to your RRSP, you lose out on tax-deferred growth; the longer you contribute early on, the better. By contributing regularly, whether monthly or annually, you make sure that you are consistently building wealth for retirement.

- Make Up Unused Contribution Room: An unused contribution room can carry forward to future years if you did not contribute the full limit in prior years. It enables you to pay more when you can afford to do so.

- Split Income Using Spousal RRSPs: Another efficient use is to utilize spousal RRSPs to ensure that you are making use of both spouse’s tax exemptions if there is a disparity between the tax bracket of a husband and a wife. The lower-earning partner invests the spousal RRSP and pays tax at a lower bracket rate when the money comes out.

Avoid Over-Contribution: While RRSPs are fairly flexible, it’s important to know how to avoid over-contributing. The Canada Revenue Agency (CRA) does allow you some manoeuvrability (up to $2,000 over your limit). However, any dollars contributed above this limit are punished with a penalty tax of 1% each month on the excess dollars contributed over your limit.

Combining RRSPs with Life Insurance

While RRSPs are an excellent way to save for your retirement, many Canadians are unaware that it is imperative to include life insurance as a part of the overall financial plan. For instance, Term Life Insurance can cover specific financial needs at critical times in your life, like when you are building your career or raising children.

For further information on RRSP contributions and Term Life Insurance, please visit our website. Lastly, speaking with a Term Life Insurance agent can help you understand how life insurance can work with your RRSP strategy.

Final Thoughts

When it comes to RRSPs, identifying who can participate is key to establishing a successful plan for retirement. Contributing early, maximizing unused RRSP contribution room, and using tactics such as spousal RRSPs can greatly increase your retirement savings. Putting these initiatives together with a Term Life Insurance policy enables you not only to save for retirement but also to shield your loved ones over the long term.

If you’re ready to get started, review your contribution room and consider working with a financial advisor to discuss how to structure your RRSP contributions best to meet your goals.

Next Steps:

- Check your RRSP contribution room.

- Consult a financial advisor for tailored retirement planning.

- Start contributing today to benefit from tax-deferred growth.

More on Term Life Insurance

- How Long Does It Take To Get Approved For Term Life Insurance?

- Does Term Life Insurance Expire At Age 65?

- Can You Be Denied Term Life Insurance?

- How Long Does Group Term Life Insurance Last?

- Does Term Life Insurance Expire At Age 65?

- How Expensive Is Term Life Insurance?

- What Is The Rule Of Term Life Insurance?

- What Is The Waiting Period For Term Insurance?

- Is Natural Death Covered In Term Insurance?

- Should I get a 20 or 30-year Term?

- How Do I Claim Term Insurance?

- Can I Use MyTerm Life Insurance To Pay Off Debt?

- Who Is The Largest Provider Of Term Life Insurance?

- What Happens After 15-Year Term Life Insurance?

- What is a 5-Year Term Life Insurance Policy?

- What Is The Expiry Date OnTerm Life Insurance?

- What Is The Short Term Policy Rate?

- Can I Change My Nominee In Term Insurance?

- The Evolution OfTerm Life Insurance: Past, Present, And FutureFrom Confusion To Clarity: How Harpreet Puri Guided A Client Through Complex Term Life Insurance Decisions

- Do Rich People Have Term Life Insurance?

- What Are The Common Term Life Insurance Clauses?

- What Are The Disadvantages Of Joint Term Insurance?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 844-542-4678 to speak to our advisors.

Get Quote Now

Frequently Asked Questions (FAQs) about RRSP Eligibility in Canada

Anyone age 18 or older with earned income, either from employment or self-employment, can contribute to an RRSP. Your contribution limit depends on your income, up to a maximum amount set by the Canadian government. You can also make contributions to an RRSP if you have income from an eligible source, as long as you’re not 71 or older.

Case in point: We see many clients approach us on whether they can contribute to an RRSP while self-employed. The answer is yes! RRSP contributions lower your taxable income, so as long as you have income, this can be of benefit to you.

Putting money into an RRSP reduces your taxable income, which means you’ll pay less tax during the year in which you contribute. The money you put into your RRSP grows tax-free until you withdraw it — at a time typically in retirement when your tax bracket is lower.

True story: One of our clients, Alex, did well at work last year. By making a contribution to an RRSP, Alex was able to drop his taxable income a lot and save hundreds in taxes. This tax saving allowed Alex to save more for the future.

No, to contribute to an RRSP, you need to have taxable income from employment or self-employment. If you don’t have income, you won’t have contribution room for the current year, but you may be able to use carry-forward contribution room from previous years if applicable.

Each year, you can contribute a maximum of 18% of the earned income from the previous year or whatever amount is capped by the Canadian government. The limit for 2025 is $32,490. Unused contribution rooms from previous years can be carried forward, too.

Tip: One of the most common questions clients ask us is: “How much can I put in my RRSP?” The simplest way to find out is to look at your Notice of Assessment from the Canada Revenue Agency (CRA), which details your contribution room.

If you’re marrying or living in a common-law partnership, you can contribute to a spousal RRSP. If one partner is in a higher tax bracket than the other, it is an excellent mechanism to copay income and decrease the tax burden.

For example, last year, a couple approached us for information on spousal RRSPs. They also saved on taxes by contributing to a spousal RRSP, ensuring that both members of the couple were contributing to savings for retirement.

Yes, on excess contributions over your limit of more than $2,000, you’ll pay a penalty of 1% per month on the excess amount. Tracking your contributions will save you from this penalty.

For example, one of our clients accidentally over-contributed to their RRSP last year and was hit with a penalty. We assisted them in rectifying the error and avoided incurring additional penalties — a timely reminder of the necessity of adhering to contribution limits.

Yes, but withdrawing money from your RRSP before retirement means you will be taxed on whatever you withdraw. The money can be withdrawn from the plan for specific reasons without tax implications, such as for the Home Buyers’ Plan (HBP) or Lifelong Learning Plan (LLP), which also allows you to take tax-free money if you have to pay either to purchase your first home or education.

For example, we recently helped a client withdraw some money from their RRSP under the Home Buyer’s Plan, which they used for their first home down payment. At the same time, this particular program made them tax-free on their withdrawal and guaranteed them a better future than other investments.

An RRSP gives you tax-deferred growth, while a Tax-Free Savings Account (TFSA) allows tax-free growth. RRSP contributions are tax-deductible, but withdrawals are taxed. In contrast, TFSA contributions aren’t tax-deductible, but withdrawals aren’t taxed.

Tip: Many of our clients ask us whether to choose an RRSP or a TFSA. It depends on your goals—if you’re looking for immediate tax savings, an RRSP may be the better option. If you want more flexible withdrawals without paying taxes later, a TFSA could be more suitable.

Yes, you can contribute to both. Each account has its own set of contribution limits. This strategy allows you to save for retirement in an RRSP while keeping some savings in a TFSA for more flexible access.

In your financial plan, an RRSP and Term Life Insurance can work complementarily. As your RRSP helps you accumulate savings for retirement, Term Life Insurance protects you for specific periods — while you’re raising a family or paying off a mortgage, for example.

For example, Mark is a client who had a strong RRSP, but he also needed insurance coverage for his family. We found him a low-cost Term Life Insurance policy to complement his RRSP and ensure his family was covered in the event something happened to him.

RRSPs are for retirement savings, but you can spend your RRSP fund on life insurance premiums if you want to. By definition, life insurance itself is not an asset held inside the RRSP; it is merely a separate policy.

Note: Many of our clients ask us about getting term life insurance quotes online combined with their RRSP. Though they are distinct, ensuring they are developed at the same time makes your overall financial well-being more robust.

Example: One of our clients, Lisa, was seeking Term Life Insurance but was uncertain what plan to go for. It was a good example of this. We were able to get her several quotes for Term Life Insurance online at an affordable price that fit her needs.

Contributing to an RRSP should begin as soon as you earn income. The earlier you start, the more you can benefit from tax-deferred growth and compound interest.

Clients who begin contributing to their RRSP in their early twenties typically have significant savings by the time they retire. Early preparation makes a world of difference, and all this, combined with Term Life Insurance, guarantees a solid financial future.

To get a Registered Retirement Savings Plan Quote Online, you can visit the websites of various financial institutions and Registered Retirement Savings Plan Providers in Canada. Many of these providers offer easy-to-use tools that allow you to calculate your potential contributions, tax savings, and retirement growth. This is a quick way to compare different plans and find the best options for your retirement goals.

There are several reputable Registered Retirement Savings Plan Providers in Canada. Some of the top names include major banks, credit unions, and independent financial institutions. It’s important to compare Registered Retirement Savings Plan Quotes Online from these providers to understand their fees, contribution limits, and investment options. Popular providers include RBC, TD Canada Trust, Scotiabank, and Manulife, among others.

We hope that these FAQs have clarified who can have an RRSP in Canada and how it relates to other financial tools like Term Life Insurance. And if you have further questions or want personalized advice, reach out. And we’re here to help craft an effective financial plan today and for the future.

Sources and Further Reading

- Canada Revenue Agency (CRA) – RRSPs and Taxes

The official CRA page offers a wealth of information on RRSP eligibility, contribution limits, and tax rules. It’s essential for anyone looking to contribute to an RRSP.- Website: Canada Revenue Agency – RRSPs

- Financial Consumer Agency of Canada (FCAC) – RRSP Overview

The FCAC provides a clear, straightforward guide on RRSPs, including eligibility and benefits.- Website: FCAC – RRSP Guide

- Investopedia – Understanding RRSPs

This article on Investopedia provides an in-depth breakdown of RRSPs, including how they work, the tax benefits, and strategies for using them effectively.- Website: Investopedia – RRSP

- Sun Life – RRSP Contribution Limits and Eligibility

A well-known Canadian insurance provider, Sun Life, explains the RRSP contribution limits, carry-forward rules, and how to maximize your contributions.- Website: Sun Life – RRSP Guide

- The Globe and Mail – RRSP Strategies for Retirement

This article provides useful strategies for Canadians looking to maximize their RRSP contributions and retirement savings.

Website: The Globe and Mail – RRSP Strategies

Key Takeaways

- RRSP Eligibility: To contribute to an RRSP, you must be at least 18 years old and have earned income. Contributions are limited to 18% of your income up to a specified maximum each year.

- Tax Benefits: RRSPs offer significant tax deferral benefits. Contributions reduce your taxable income, while the funds grow tax-free until you withdraw them, typically in retirement.

- Contribution Limits: The annual contribution limit is 18% of your earned income from the previous year, up to a maximum limit ($30,780 for 2023). Unused contribution room can be carried forward to future years.

- Spousal RRSPs: You can contribute to your spouse’s RRSP, which can help split income and reduce overall taxes if one spouse is in a higher tax bracket.

- RRSP vs. TFSA: While both are valuable savings tools, RRSPs are ideal for tax deferral on retirement savings, whereas TFSAs offer tax-free growth with more flexible withdrawals.

- Withdrawing from RRSPs: Withdrawals from RRSPs are taxed, but specific programs like the Home Buyers’ Plan (HBP) and Lifelong Learning Plan (LLP) allow tax-free withdrawals for specific purposes.

- Integration with Term Life Insurance: An RRSP and Term Life Insurance can complement each other in a financial plan. While RRSPs help build retirement savings, Term Life Insurance provides coverage for specific life events.

- Start Early for Maximum Growth: The earlier you begin contributing to your RRSP, the more you benefit from tax-deferred growth and compounded returns. Even small, regular contributions can add up significantly over time.

- Avoid Over-Contribution: Be mindful of your contribution limit to avoid penalties for over-contributing. The CRA allows a $2,000 buffer, but excess contributions beyond that are taxed.

Plan for the Future: Incorporate both RRSP and Term Life Insurance strategies to ensure long-term financial security. Speak with a financial advisor to align these tools with your retirement and family planning goals.

Your Feedback Is Very Important To Us

We would love to hear about your experience and any struggles you’ve faced in understanding RRSP eligibility in Canada. Your feedback helps us improve our content and better address your needs.

Thank you for taking the time to fill out this questionnaire!

Your feedback is invaluable in helping us improve our content and assist you better in understanding RRSPs.

IN THIS ARTICLE

Sign-in to CanadianLIC

Verify OTP