- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Can A Person With Dementia Get Life Insurance?

By Harpreet Puri

CEO & Founder

- 09 min read

- July 06, 2026

SUMMARY

Covers whether a person with dementia can get Life Insurance, including Alzheimer’s disease, Life Insurance options, guaranteed acceptance policies, coverage limits, premiums, and death benefit payouts. Explains how dementia affects eligibility, existing Life Insurance Policy benefits, life expectancy impact, and alternative solutions like Long-Term Care Insurance for better financial planning.

Introduction

Dementia, Alzheimer’s Disease, And Life Insurance Reality

What was once considered a medical issue is now becoming a financial and planning issue in Canada as well. The Alzheimer Society of Canada indicates that in 2020, the number of people living with dementia in Canada surpassed 600,000, and this number is likely to rise to 1 million people by 2030.

This has thus led to the following issues in relation to financial protection:

Can a person with dementia get Life Insurance?

The short answer is yes, but only under certain circumstances and conditions.

We know from our real-world experience working with our clients that the majority of the public thinks that, after they have received a diagnosis, it is impossible to acquire Life Insurance. Well, let us set the record straight. It simply is not true. It may be difficult, but it is certainly possible to acquire other types of Life Insurance that are just as good as traditional Life Insurance.

This guide will help you understand what is possible, what is impossible, and what is in your best interest.

What Is Dementia, and Why Does It Matter for Life Insurance

Dementia is not regarded as a disease, but rather a classification of a group of signs and symptoms that affect memory, thinking, and social behaviour.

Common forms of dementia include:

- Alzheimer’s disease. It is regarded as the most severe and common form of dementia.

- Lewy Body Dementia.

- Vascular Dementia.

- Frontotemporal Dementia.

All forms of dementia have cognitive signs and symptoms and can be regarded as a progressive disease. Progressive means that the signs and symptoms of the disease become more severe over time.

Why Insurers Treat Dementia As High Risk

Life Insurance companies base decisions on two core factors:

- Life expectancy

- Predictability of health outcomes

Dementia affects both.

Clinical data indicate that a person diagnosed with Alzheimer’s lives an average of 8–10 years, although some may live considerably longer with optimal care.

From the insurance company’s point of view, this translates to:

- Increased risk of claims

- Increased uncertainty

- Increased need for long-term care

As a consequence, dementia is included in a group of serious medical conditions that may prevent a person from obtaining Life Insurance.

Can A Person With Dementia Get Life Insurance After Diagnosis?

Yes. A person with dementia can still get Life Insurance, but approval depends on timing and severity.

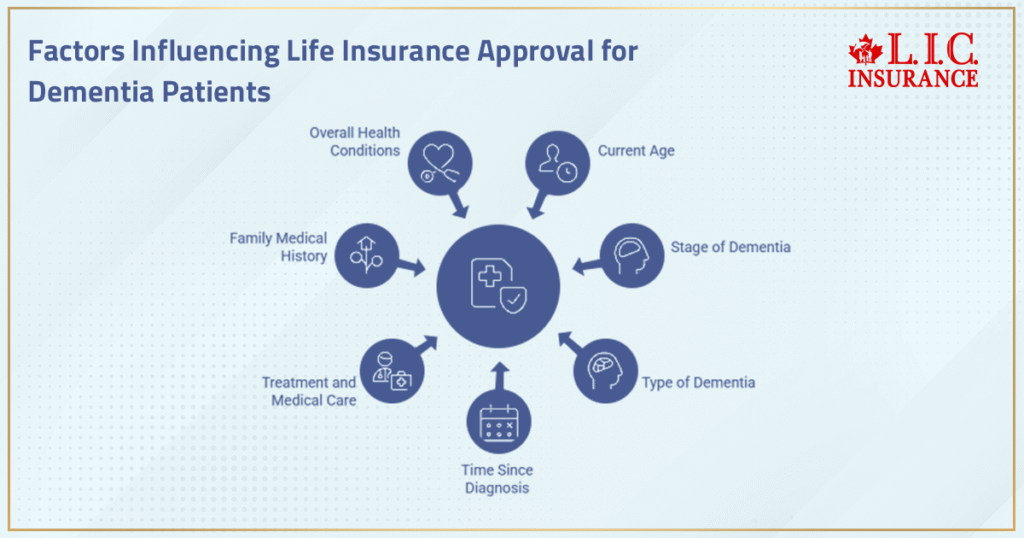

What Insurance Companies Look At

When evaluating an application, insurers assess:

- Current age

- Stage of dementia (early, moderate, advanced)

- Type (Alzheimer’s disease, vascular, etc.)

- Time since diagnosis

- Treatment and medical care

- Family medical history

- Overall health conditions

Real-World Insight (From Advisory Experience)

In practice:

- Clients who are diagnosed very early may still have limited options other than guaranteed plans.

- Clients diagnosed mid-to-late stage are almost always sold guaranteed acceptance policies.

The earlier the client applies, the more options and cost savings they will have

Life Insurance Options For Seniors With Dementia

Understanding available policy types is critical. Not all insurance is equal, and each option serves a different purpose.

Traditional Life Insurance (Why It Rarely Works)

Traditional Life Insurance includes:

- Term Life Insurance

- Permanent Life Insurance

These policies require:

- A full medical exam

- Detailed medical questions

- Access to medical records

For someone with dementia, approval is extremely unlikely.

Even in rare early-stage approvals:

- Premiums are significantly higher.

- Coverage may be restricted.

From an underwriting standpoint, most Life Insurance companies decline these applications outright.

Simplified Issue Life Insurance (Limited Opportunity Window)

Simplified policies remove the medical exam but still include health questions.

They are often marketed as no medical exam Life Insurance, but they still assess risk.

For dementia applicants:

- Early-stage cases may sometimes qualify.

- Moderate or advanced cases are typically declined.

Even when approved:

- Coverage is lower

- Premiums are higher

This option exists in a very narrow eligibility window.

Guaranteed Issue Life Insurance (Most Practical Option)

For most individuals with dementia, this becomes the primary solution.

How It Works

- No medical exam

- No health questions

- Guaranteed acceptance

What You Need To Know

- Higher Premiums

The cost of the insurance is higher as the risk is not underwritten.

- Lower Coverage

The amount of coverage is between $5,000 and $50,000.

- Waiting Period (Graded Benefit)

If the insured dies within the first 2 years:

- Premiums are returned

- Death benefit may not be fully paid.

- Limited Flexibility

No extra Life Insurance riders

Mainly Permanent Coverage

Despite limitations, this policy ensures that benefits are paid and financial protection exists, even in complex health situations.

How Much Life Insurance Coverage Is Realistic With Dementia?

Unlike traditional policies, coverage here is designed for specific financial needs, not large income replacement.

Typical Coverage Range

- $5,000 to $50,000

- Occasionally higher through multiple policies

Common Uses

- Funeral costs

- Final medical expenses

- Small debts

- Immediate family support

Professional Guidance

A practical approach is to:

- Prioritize essential expenses

- Avoid overpaying for limited benefit increases.

This ensures premiums remain manageable while still delivering value.

What Happens To Existing Life Insurance After Diagnosis?

This is one of the most misunderstood areas.

If you have an existing Life Insurance Policy:

- The coverage stays the same

- The premium does not increase.

- The policy cannot be cancelled because of the diagnosis. Most importantly, the full death benefit still applies. This illustrates one of the key principles of Life Insurance.

The best time to buy Life Insurance is before any major health issues arise.

Does Life Insurance Cover Dementia And Alzheimer’s Disease?

Yes. Death resulting from dementia is considered to fall under natural cause of death.

This means that:

- The policy pays as it should

- There are no exclusions (except those that were chosen during purchase)

- The full benefit is paid to the beneficiaries.

Life Expectancy And Its Impact On Insurance Decisions

Life expectancy plays a central role in underwriting.

Clinical Data

- Average survival: 8–10 years after diagnosis

- Extended cases: up to 15–20 years

Insurance Impact

Since dementia is not necessarily considered a terminal illness, the following may not apply:

- Terminal illness riders may not be triggered.

- Accelerated death benefits may not be available.

This distinction must be made when comparing policies.

Alternatives To Life Insurance For Dementia Patients

In many cases, combining strategies provides better protection.

Long-Term Care Insurance

- Covers assisted living and care costs.

- Supports Alzheimer’s care planning

Critical Illness Insurance

- Provides a lump-sum payment

- More effective if purchased before diagnosis

Government Support

Programs may include:

- Supplemental Security Income

- Provincial healthcare assistance

These can reduce financial burden significantly.

Key Considerations Before Buying Life Insurance With Dementia

1. Cost vs Value

- Higher premiums must justify the benefit.

- Avoid over-insuring with limited policies.

2. Waiting Period Awareness

- Understand the 2-year clause.

- Plan for immediate financial needs separately

3. Coverage Purpose

Focus on:

- Funeral costs

- Family support

- Debt clearance

4. Work With A Licensed Advisor

An experienced insurance agent helps:

- Compare Life Insurance companies.

- Identify suitable coverage

- Avoid costly mistakes

Final Thoughts – What Families Need To Understand

A dementia diagnosis changes the insurance landscape—but it does not eliminate options.

From a professional advisory perspective, the most effective strategy is:

- Act early whenever possible.

- Understand realistic coverage limits.

- Focus on essential financial protection.

Even limited coverage can offer valuable support, including payment of final expenses, which can help alleviate the financial burden on loved ones.

Even limited Life Insurance Coverage represents a powerful financial tool, particularly when utilized optimally based on the restrictions of dementia-related eligibility.

FAQs

It is possible for a person suffering from dementia to obtain Life Insurance, and this will depend on the level of dementia as well as health conditions. Most insurance companies do not cover individuals suffering from dementia, as this reduces their lifespan due to cognitive impairment. The guaranteed acceptance policy, however, assists the individual in obtaining coverage without undergoing medical tests to determine whether they are eligible for the coverage or not. The process of obtaining the coverage is easy, although there is a reduction in the benefits as well as higher premiums paid.

For most people, only no medical exam options for Life Insurance are available. These types of insurance plans, especially for guaranteed issue Life Insurance, do not require any medical exam or extensive questions regarding the insured’s health. This is good news for people suffering from serious conditions such as Alzheimer’s disease, as they are able to acquire Life Insurance. However, the premium for this insurance is normally high because no medical exam is required.

In most cases, for patients suffering from Alzheimer’s and other elderly patients suffering from dementia, guaranteed issue Life Insurance is considered to be the best and only option available. In a guaranteed issue Life Insurance Policy, a person is guaranteed to be accepted for a Life Insurance Policy, irrespective of their medical history or existing health problems. Although the sum insured is limited and premiums are higher, a death benefit is guaranteed. Other forms of Life Insurance are not available.

After an individual with dementia has been able to secure a guaranteed acceptance policy, it becomes hard to increase the coverage of the insurance policy. Most insurance companies will not allow you to increase your coverage because, with dementia, the health condition of the individual will continue to deteriorate. In other instances, the individual with dementia can choose to buy several insurance policies, which can be quite beneficial in increasing coverage. The best way to ensure that your family is well taken care of is to buy sufficient Life Insurance.

The life expectancy of a person suffering from dementia varies based on different factors, including the age of the person, the type of disease, and health conditions. On average, people suffering from Alzheimer’s disease survive for 8-10 years after being diagnosed with the disease. However, this period can be extended with proper medical care. As the disease is progressive, Life Insurance companies consider this carefully. We assist you in understanding the importance of life expectancy in relation to Life Insurance.

Yes, you can still apply for Life Insurance if you are in the early stages of dementia. There are Life Insurance companies that offer simplified Life Insurance Coverage, depending on your health records. In the case of early-stage dementia, you have more choices when it comes to Life Insurance. We work with several insurance companies to provide you with the best coverage.

There are some insurance companies in Canada that offer guaranteed acceptance Life Insurance Coverage to people living with dementia. The insurance coverage is given without the need to undertake a medical test or answer health questions, thus ensuring that the clients are accepted despite their condition. Although the coverage is low, it is a great way of ensuring that the clients receive their benefits. We compare the best insurance providers and help clients choose the most affordable coverage.

Generally, the best Life Insurance Plans for seniors with cognitive impairment involve guaranteed issue and simplified Life Insurance. The plans help seniors get Life Insurance despite their health conditions, such as dementia. The guaranteed acceptance plans may be the only choice for seniors with advanced cognitive impairment to ensure that their loved ones receive their life benefits. We help seniors determine the most suitable Life Insurance Plans according to their needs.

When applying for a Life Insurance Policy and having a diagnosis of dementia, it is highly recommended to seek the assistance of an insurance agent who is experienced in handling complicated health conditions. Additionally, it is necessary to provide medical records and answer health-related questions. However, for a guaranteed acceptance policy of Life Insurance, a medical exam is not required. We will be with you every step of the way to make the process a success.

You can locate an insurance broker who specializes in health issues faced by seniors through experienced companies such as Canadian LIC. They can help you understand how dementia influences Life Insurance and recommend the appropriate policies. We have access to numerous Life Insurance companies that can help us offer personalized solutions to our clients in Ontario.

An existing Life Insurance Policy will not be affected by a diagnosed case of dementia as long as payments are made on a timely basis. The insured will still be covered, and the full face value will be paid out in case of death. Life Insurance companies cannot terminate or change a policy due to a change in health. We often advise clients to do so in advance to reap long-term benefits.

There are no policies specifically designed for dementia patients, but some Life Insurance Plans are designed for high-risk individuals. The most relevant options are guaranteed acceptance Life Insurance and no medical exam Life Insurance. These types of insurance plans provide coverage without requiring detailed medical information. Canadian LIC helps clients make decisions regarding the most suitable insurance policy.

There are situations where you may be able to convert your existing policy, especially if it is a Life Insurance Policy that allows for conversion. This allows you to change from term insurance to permanent insurance without having to take a medical exam. However, this would depend on the policy and how soon you are diagnosed. We assess our clients’ existing policies to ensure we know how to best convert them.

A diagnosis of dementia has a significant impact on the premium costs of Life Insurance when a new policy is being considered. The premium costs are higher due to the risk and reduced life expectancy. The premium costs are the highest in the case of a guaranteed acceptance policy, as no medical tests are required.

We assist clients in making a comparison of the premium costs of various Life Insurance companies in order to find the most cost-effective option.

The documentation varies depending on the type of Life Insurance Policy applied for. For traditional and simplified insurance, medical records, doctor reports, and medical information may be required. For guaranteed acceptance, minimal documentation is required, which includes basic client information. We provide assistance in preparing the right documentation to facilitate quick processing.

In order to compare the Life Insurance Plans, it is necessary to consider the coverage, premium, waiting period, and benefits. It is also necessary to understand the difference between the guaranteed acceptance plan and the simplified plan. We compare the Life Insurance companies and provide the best Life Insurance options to the clients.

There are several Canadian Life Insurance companies that offer coverage to individuals suffering from dementia through guaranteed acceptance and simple policies. They specialize in offering insurance solutions to individuals with no medical requirements. Although this coverage is limited, it offers basic protection to individuals suffering from this condition. We work with top companies to ensure that clients receive the best coverage for their needs and budget.

Sources and Further Reading

Dementia Numbers In Canada

Detailed statistics on dementia prevalence, future projections, and impact across Canada.

Dementia In Canada – Key Findings (CIHI)

Insights into how dementia risk increases with age and its prevalence among seniors.

How Dementia Impacts Canadians

Data on new cases, national trends, and the growing burden on healthcare systems.

Alzheimer’s Awareness Month – Statistics Canada

Government-backed data on dementia-related deaths and national trends.

Public Health Agency Of Canada – Dementia Overview

Official overview of dementia, diagnosis rates, and population impact.

Alzheimer Society Of Canada – Landmark Study Reports

Research reports and projections on dementia trends and future outlook.

Dementia Risk Factors (Alzheimer Society)

Information on causes, risk factors, and progression of Alzheimer’s disease.

UBC Landmark Study On Dementia Growth

Academic research projects the rise of dementia cases in Canada.

Canadian Dementia Statistics (StatCan & Research Data)

Epidemiological data on prevalence, incidence, and demographics.

Global & Canadian Alzheimer’s Data (Alzheimer’s Association)

A broader perspective on dementia as a global and national health issue.

Key Takeaways

- A person with dementia can still get Life Insurance, but options are limited based on the stage of the illness and overall health conditions.

- Traditional Life Insurance is difficult to qualify for, while guaranteed acceptance Life Insurance is the most common and accessible option.

- Guaranteed acceptance policies offer coverage without a medical exam, but come with higher premiums and lower benefits.

- Early-stage applicants may still qualify for more flexible Life Insurance options compared to advanced dementia cases.

- An existing Life Insurance Policy remains fully valid, and the death benefit is paid even after a dementia diagnosis.

- Dementia, including Alzheimer’s disease, is treated as a natural cause of death, so coverage is not denied.

- Coverage amounts are typically lower and mainly used for funeral costs and final expenses.

- Life expectancy plays a major role in how Life Insurance companies assess eligibility and premiums.

- Alternatives like Long-Term Care Insurance and Critical Illness Insurance can help strengthen financial planning.

Your Feedback Is Very Important To Us

We value your input to better understand the challenges people face when exploring Life Insurance for dementia patients. Your responses will help improve guidance and solutions.

IN THIS ARTICLE

- Can A Person With Dementia Get Life Insurance?

- What Is Dementia, and Why Does It Matter for Life Insurance

- Can A Person With Dementia Get Life Insurance After Diagnosis?

- Life Insurance Options For Seniors With Dementia

- How Much Life Insurance Coverage Is Realistic With Dementia?

- What Happens To Existing Life Insurance After Diagnosis?

- Does Life Insurance Cover Dementia And Alzheimer’s Disease?

- Life Expectancy And Its Impact On Insurance Decisions

- Alternatives To Life Insurance For Dementia Patients

- Key Considerations Before Buying Life Insurance With Dementia

- Final Thoughts – What Families Need To Understand

Sign-in to CanadianLIC

Verify OTP