- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

How The Canada Learning Bond Boosts Your Child’s RESP

By Harpreet Puri

CEO & Founder

- 12 min read

- June 1st, 2026

SUMMARY

Canada Learning Bond helps eligible families start a child’s RESP without contributions by providing free government funds. Covers eligibility, RESP grants Canada, Canada Education Savings Grant, and how combining these benefits can grow long-term education savings for post-secondary education while maximizing available government support.

Introduction

One of the most significant financial decisions a parent has to make for their child involves saving money to pay for the cost of their education. Statistics Canada states that “the average cost of post-secondary education is rising steadily, and tuition, housing, and other expenses add up to create a significant financial burden.” The Government of Canada states that thousands of eligible families are not benefiting from the available programs.

This is where the Canada Learning Bond really is a game-changer.

The Canada Learning Bond is a program that assists poor families in saving for their children’s education without them having to put up any of their own money. By opening up a Registered Education Savings Plan, they can start saving for their child’s education and create a stable financial base for them.

According to Canadian LIC, one of the least used but most powerful tools available to families is saving for your child’s education.

What Is The Canada Learning Bond CLB And How It Works In Canada

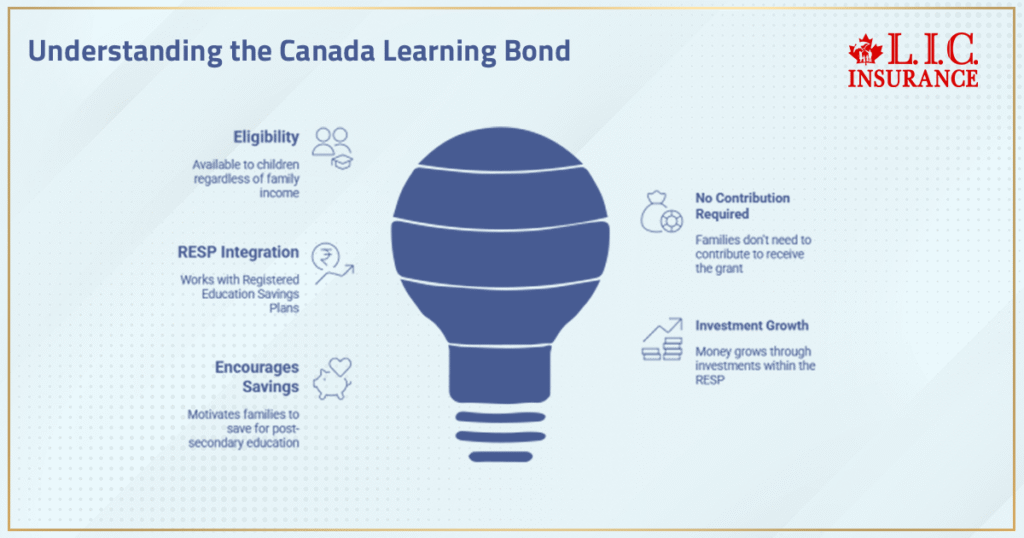

The Canada Learning Bond CLB is a government grant offered by the Government of Canada through Social Development Canada. Its aim is simple: to make sure that all children, regardless of their families’ incomes, have access to education savings.

Unlike the Canada Education Savings Grant, the Canada Learning Bond does not require any contributions from the families. This means that families can open an RESP account and start receiving the Canada Learning Bond without having to make any contributions themselves.

This program is part of a system of RESP grants that Canada offers, all of which are designed to encourage families to save for their children’s future and make post-secondary education accessible to them.

The learning bond gives children a financial kick start. Once money has been deposited into the child’s RESP account, it starts to grow by being invested in investment products offered by the RESP provider.

This gives children a long-term advantage, especially when other government grant programs are taken into consideration.

Canada Learning Bond Eligibility: Who Qualifies And Why It Matters

Understanding Canada Learning Bond eligibility is essential for maximizing benefits.

To qualify, eligible children must meet the following eligibility criteria:

- The child must have a valid social insurance number sin.

- The child’s primary caregiver must receive the Canada Child Benefit.

- The family income must fall within the income requirements.

- The primary caregiver must have filed income tax returns.

These requirements ensure that the program supports eligible families who need it most.

In many cases, families assume they are not eligible when, in fact, their child qualifies. This leads to unclaimed Canada Learning Bond money that could otherwise support a child’s education after high school.

For families receiving children’s special allowance or living in unique household structures, additional rules may apply, but eligibility is often broader than expected.

How Much Canada Learning Bond Money Your Child Can Receive

The Canada Learning Bond offers structured financial support over time.

Here’s how it works:

- Initial payment of $500 when the child is eligible

- An additional $100 per year for each year of eligibility

- Lifetime maximum of $2,000

This lifetime maximum is deposited directly into the child’s RESP.

One of the most powerful benefits is retroactive eligibility. If a child was eligible for a grant for previous years but didn’t apply, they can receive a grant for those years as soon as they start an RESP.

This means that families can receive a large amount of money at one time, accelerating their savings.

How To Open An RESP And Access Canada Learning Bond CLB Easily

To receive the Canada Learning Bond, families must open an RESP.

The process is straightforward:

- Obtain a social insurance number for the child.

- Choose a resp provider such as a financial institution or credit union.

- Open a resp account.

- Apply for all available government grant programs.

One of the greatest advantages is that no personal contributions are necessary to start an RESP plan.

It becomes easier for low-income families to start an RESP plan without any financial burden.

A knowledgeable RESP provider can ensure that all RESP and related benefits are utilized in an efficient manner.

Canada Education Savings Grant And Other RESP Grants Canada Families Should Know

While the Canada Learning Bond is powerful on its own, it becomes even more valuable when combined with other programs.

The Canada Education Savings Grant (education savings grant cesg) is one of the most widely used RESP grants Canada offers. It matches a portion of personal contributions, helping education savings grow faster.

Additional programs include:

- Additional CESG for eligible families

- British Columbia training incentives

- Other benefits, depending on the province

These education savings grant programs work in concert to ensure that a maximum amount of money is available to a child’s RESP.

These government grant sources can be combined to increase the amount of money that can be used to fund a child’s post-secondary education.

How The Canada Learning Bond Boosts Long-Term Education Savings Growth

The role of the Canada Learning Bond in the context of long-term education savings cannot be overstated.

Even without contributions, the initial investment will benefit from compounding over time. As the RESP grows, families can then make contributions and access matching funds from the Canada Education Savings Grant.

This layered strategy is highly effective:

- Start with Canada Learning Bond money.

- Add personal contributions when possible.

- Receive additional government grant support.

Over time, this creates a strong education savings account capable of covering a large portion of education costs.

From a planning perspective, starting early provides the greatest advantage.

Using RESP Funds For Your Child’s Education After High School

RESP funds are designed to support education after high school across a wide range of programs.

Eligible options include:

- Universities and colleges

- Apprenticeship programs

- Trade schools

- Other post-secondary studies

Funds can be used for various eligible expenses, including:

- Tuition

- Books and supplies

- Housing and transportation

- Tools required for training programs

When the child starts going to post-secondary institutions, the withdrawals are made in the form of Educational Assistance Payments.

The tax liability of these payments is in the name of the child, and in most cases, the tax liability is very low due to low levels of income.

This makes RESP one of the most tax-efficient savings plans for funding education.

Why Eligible Families Should Start An RESP Without Delay

The main reason why most eligible families are reluctant to start an RESP is that they think they need money to start.

However, the Canada Learning Bond completely removes this barrier.

When families open an RESP, they can receive money without having to make contributions. This gives them an immediate advantage and allows their child’s education savings to start immediately.

When families wait to start an RESP, they lose valuable time and may not qualify for certain benefits based on the year of eligibility.

When families start early, they allow their child’s RESP to reach its full potential.

The Role Of Financial Institutions And RESP Providers

Choosing the right RESP provider is a critical step in maximizing benefits.

Financial institutions such as banks and credit unions offer various RESP options, each with different investment products and fee structures.

A knowledgeable provider helps:

- Apply for all RESP grants in Canada programs.

- Manage contributions and withdrawals.

- Optimize long-term education savings.

From a Canadian LIC standpoint, working with a trusted advisor ensures that families receive the full value of available government programs.

Understanding RESP Contribution Limits And Strategy

Although there are no contributions required for the Canada Learning Bond, the importance of RESP contribution limits cannot be overlooked in terms of future planning strategies.

The lifetime contribution limit per beneficiary is set at $50,000.

Families can make contributions at their own pace, including how much they can contribute and when.

Making contributions can go a long way in maximizing the CESG and efficiently building the RESP.

Common Mistakes Families Should Avoid

Despite the benefits, many families make avoidable mistakes:

- Not opening an RESP early.

- Assuming they are not eligible

- Missing out on the retroactive Canada Learning Bond money

- Not combining multiple government grant programs.

Avoiding these mistakes can significantly improve the effectiveness of an education savings plan.

Final Thoughts: Secure Your Child’s RESP And Maximize Government Benefits

The Canada Learning Bond is one of the most effective vehicles to begin saving for your child’s education in Canada.

It provides immediate access to government funding, supports eligible families, and creates a solid financial foundation to fund your child’s education beyond high school.

From a Canadian LIC perspective, it’s clear:

Start early, use all government RESP grants available in Canada, and create a structured education savings plan that can support your child’s future.

Is your child eligible? Take action today:

Create a RESP, secure your Canada Learning Bond, and start securing your child’s financial future through education savings.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Yes, this is true, as it is possible for the Canada Learning Bond to be used in conjunction with other methods of education savings beyond a basic Registered Education Savings Plan. It is possible for this to be done in such a way that it is aligned with long-term financial planning tools provided by a financial institution, allowing for a more flexible approach for eligible children to receive money from multiple sources.

If the child decides not to attend post-secondary education at an early stage, the Canada Learning Bond funds can remain invested within the RESP plan. This allows the funds saved for education to grow through investment opportunities available for the child in the future. This option allows the child to benefit from the funds as long as they qualify for post-secondary education at a later stage.

The Canada Learning Bond amount is combined with other savings in the RESP account of the child, including the education savings grant amount and the individual’s contribution. Although there are set rules for withdrawals, the funds are utilized together once the child starts his or her education after high school. This concept enables all the savings to work together towards financing the child’s education. It simplifies the management of different government grants.

The role of the Canada Learning Bond is significant as it contributes to the expansion of educational savings for low-income families, who may not have participated otherwise. This is due to the removal of the need to make contributions, hence encouraging more families to open an RESP and become part of financial planning. This leads to more participation throughout Canada, hence more children preparing for future educational possibilities.

Sources and Further Reading

- Canada Learning Bond – Government Of Canada

Official overview of Canada Learning Bond, eligibility, and how money is deposited into a child’s RESP. - RESP And Related Benefits – Government Of Canada

Detailed breakdown of RESP grants Canada, including Canada Education Savings Grant and Canada Learning Bond amounts and rules. - Registered Education Savings Plans (RESP) Overview

Explains how to open an RESP, access government grant programs, and maximize education savings. - Canada Education Savings Grant (CESG) Details

Official information on education savings grant structure, contribution matching, and lifetime limits. - Canada Learning Bond Explained – Fidelity Canada

Insight into how Canada Learning Bond supports education savings and long-term RESP growth. - RESP Grants And Bonds – RBC

Practical overview of RESP contribution limits, grants, and eligibility for eligible families. - Canada Learning Bond – Toronto Metropolitan University

An academic resource explaining how CLB supports post-secondary education and eligible expenses. - RESP Contributions And Grants Overview – Wealthsimple

Covers RESP contribution limits, investment growth, and how grants like CLB and CESG interact. - Canada Learning Bond Community Resources – Government Of Canada

Resources explaining how Canada’s learning programs improve access to education savings across Canada. - Canada Learning Bond Overview – Toronto.ca

Explains how Canada Learning Bond money helps cover a child’s education after high school expenses.

Key Takeaways

- Canada Learning Bond provides up to $2,000 in government grant support for a child’s RESP, even without personal contributions.

- Eligible families can open an RESP and receive money deposited directly, helping start education savings early.

- Canada Learning Bond works alongside Canada Education Savings Grant and other RESP grants, Canada programs to boost overall education savings.

- Meeting Canada Learning Bond eligibility requirements, including a valid social insurance number and income tax returns, is essential to access benefits.

- Starting early allows education savings to grow through compounding and investment products within a Registered Education Savings Plan.

- RESP funds can be used for post-secondary education, including apprenticeship programs and other eligible expenses after high school.

- Combining government grant programs with personal contributions strengthens long-term financial support for a child’s education.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- How The Canada Learning Bond Boosts Your Child’s RESP

- What Is The Canada Learning Bond CLB And How It Works In Canada

- Canada Learning Bond Eligibility: Who Qualifies And Why It Matters

- How Much Canada Learning Bond Money Your Child Can Receive

- How To Open An RESP And Access Canada Learning Bond CLB Easily

- Canada Education Savings Grant And Other RESP Grants Canada Families Should Know

- How The Canada Learning Bond Boosts Long-Term Education Savings Growth

- Using RESP Funds For Your Child’s Education After High School

- Why Eligible Families Should Start An RESP Without Delay

- The Role Of Financial Institutions And RESP Providers

- Understanding RESP Contribution Limits And Strategy

- Common Mistakes Families Should Avoid

- Final Thoughts: Secure Your Child’s RESP And Maximize Government Benefits

Sign-in to CanadianLIC

Verify OTP