- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Return of Premium In Critical Illness Insurance Plans In Canada

By Pushpinder Puri

CEO & Founder

- 10 min read

- July 15, 2026

SUMMARY

Critical Illness Insurance with Return of Premium combines protection with potential premium refunds if no claim occurs. It explains what is Return of Premium Insurance Canada, compares costs, coverage, and critical illness benefits in Canada, and shows how a Return of Premium rider impacts premium payments. Real examples highlight when Return Premium Life Insurance works best and when standard Critical Illness Insurance Coverage may be more cost-effective.

Introduction

A diagnosis will not only have consequences on your health, but also on your finances, career choices, and future family planning. As suggested by Sun Life, the annual average financial loss in Canada associated with a major illness will amount to at least six figures due to medical treatment, the loss of working days, and income reduction. Canadian Life and Health Insurance Association repeatedly underlines that, despite the claims being regularly fulfilled, people often experience problems associated with other types of losses, which are usually not covered by basic medical insurance.

This type of insurance thus becomes a question of personal strategy. And among the options provided within such strategies, one option stands out specifically in our consultations—Return of Premium. In other words, the discussion around Critical Illness Insurance changes direction when we start talking about getting your money back. This topic opens up new questions, including those that no one would like to admit aloud—what happens if my premium is returned without any claims?

The answer lies in the specifics of how such programs operate and function, in their behaviour throughout the contract period, and the practicality of this type of refund.

What Is Return of Premium Insurance Canada, And Why Does It Exist

At the initial stage, when clients hear “what is Return of Premium Insurance Canada,” the expectations become obvious. Clients think that if no claims ever occurred during a policy period and individuals were in good health, then their entire premium money would be returned. This may sound right in some way, but there are certain specifics, as well as an important intention of having such a feature included.

To begin with, one can define the purpose of insurance as transferring risks from individuals to other organizations. When you pay your premium to cover risks associated with a certain event, you get coverage for those. But if the event never took place, it would still seem natural that you have paid your money just to cover your back. Thus, a kind of forced saving emerges.

In order to provide the return of your premium, the insurers include it in their Critical Illness Policies as an add-on or ROP Rider. Some of these insurance companies in Canada are Canada Life Insurance Company and Sun Life Financial.

From a practical perspective, this enables customers who have no Critical Illness Insurance claims throughout the policy period to get back premiums paid. There may also be a partial premium refund if the policy is terminated at a particular point in time, or in case of death without having any critical illness claim.

The reason behind such a provision is that many clients find comfort in knowing that their monetary investment will not go to waste in case they stay healthy throughout the policy period.

How Critical Illness Insurance Coverage Works In Real Life

It is important to comprehend how the critical illness coverage functions in order to fully comprehend the significance of the Return of Premium. Critical Illness Insurance offers a lump sum payment once the insured individual gets a disease covered by the insurance, including cancer, heart attack, and stroke. It should be noted that these are not merely medical emergencies. These are significant diseases that cause disruption in income, necessitate long-term recuperation, and bring costs that exceed those covered by basic health insurance.

The difference from Disability Insurance lies in the fact that, while the latter makes periodic payments that replace lost income, Critical Illness Insurance offers a single cash payment. The reason why this distinction is important is that the goal of the payment is versatility. That is, the insured person is able to use the money for whatever purposes he or she wants.

In most cases, Canadian Critical Illness Insurance covers anywhere from 20 to 30 medical conditions, based on the insurance company and the selected level of coverage. This payment is usually tax-free, thus becoming an important aid for urgent money problems.

Indeed, when one becomes ill, the financial effect goes beyond hospitalization expenses. There is lost income, extra expenditures for care, and frequently the need to adjust one’s lifestyle. In this regard, the real value of the benefit does not lie in surviving; it lies in maintaining one’s dignity.

How The Return of Premium Rider Actually Works Over Time

Return of Premium Insurance’s attraction is evident once one looks at how it works within an extended period insurance scheme. The system does not have any instant rewards. Rather, it is structured to encourage persistence and loyalty.

Most insurance companies have a waiting period during which no refund can be claimed. This period depends on the insurance company, but it lasts between a few years and even up to a decade. Once this waiting period elapses, the accumulated value of the refund can be claimed by the policyholder.

In some instances, there may be even more triggers. Should the insured opt out within a specific timeframe, then he/she could get some sort of partial refund. In case of an early death without any claim being made, there is some coverage by way of a death benefit equal to the premium amount paid.

At Sun Life, for instance, the chances of getting refunds can increase each year. At Canada Life, the same happens when it comes to Critical Illness Policies.

What you need to know about these policies is that they are not free of cost. They cost you more than regular insurance. The excess premium that you pay goes towards that future refund.

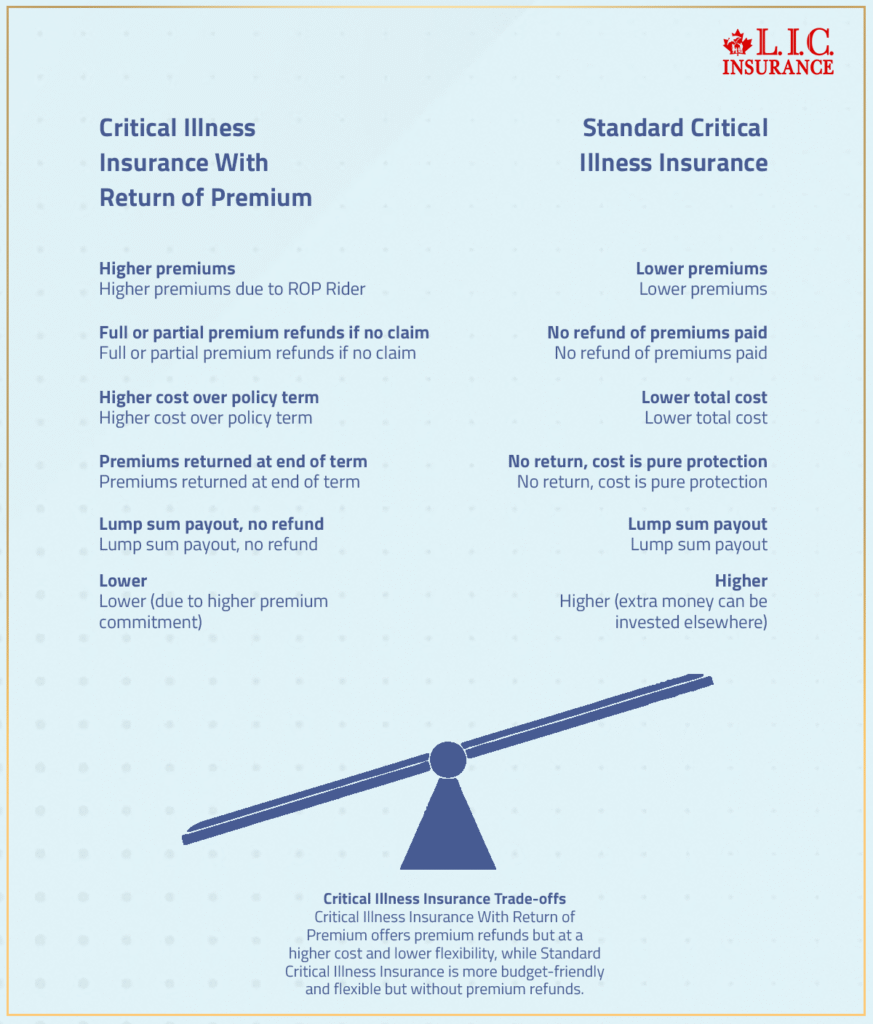

The Real Cost Difference: What You Pay And What You Get Back

On the face of it, the opportunity of reclaiming one’s money appears to be an obvious edge. Yet, upon further consideration, it becomes evident that the assessment of the additional expense factor is important.

According to the estimates based on quotes provided and published rate ranges of large Canadian insurance companies, such as Sun Life and Canada Life (trends for 2025-2026), the average monthly cost of purchasing regular Critical Illness Insurance for a 35-year-old individual can range between $40-$55.

The addition of a Return of Premium option increases the monthly cost to around $70-$95, taking into account the amount of coverage, underwriting, and policy period selection.

The above-mentioned numbers are merely illustrative and do not represent quotes.

| Plan Type | Monthly Premium | Total Premium Paid (20 Years) | Premium Refund |

|---|---|---|---|

| Standard Critical Illness Insurance | $40–$55 | $9,600 – $13,200 | $0 |

| Critical Illness Insurance With Return of Premium | $70–$95 | $16,800 – $22,800 | Full or partial premium refunds |

This comparison highlights how higher premiums in a Return of Premium Plan increase upfront cost, but may result in premium refunds if no critical illness claim occurs during the policy term.

Comparing ROP, Non-ROP, And Disability Insurance

There must be a comparison in order to make a sensible choice. To properly analyze the Critical Illness Insurance that has ROP, one needs to know its differences from the usual Critical Illness Insurance and Disability Insurance.

A policy with an ROP will have higher premiums, but it gives you your premiums back in the absence of a claim. Meanwhile, a non-ROP plan only aims at providing you with security, and the premiums will be less expensive, but without any refund. Disability Insurance covers the income and provides monthly benefits, while Critical Illness Insurance provides cash benefits.

The difference plays a vital role when considering the various risks that you may encounter. Although you cannot work due to your illness, you can still earn money, unlike disabilities that will directly affect your income source. Most clients have both plans to provide themselves with sufficient protection.

Return of Premium Vs Standard Critical Illness Insurance

A more precise understanding of Critical Illness Insurance benefits with premium repayment can be achieved by contrasting the two products with each other. Both plans have many similarities, but their structure, pricing, and future gains differ greatly.

Partial Benefits And The Reality Of Claims

Many people wrongly assume that modern Critical Illness Insurance Plans only pay out on a case-by-case basis. This is not always the case. In addition to paying full amounts for specified conditions, some insurance companies also offer partial payment benefits. Under this provision, there will be lower payouts for fewer medical cases.

Take the example of Sun Life Insurance Company. The insurance provider offers partial payouts in cases where the patient undergoes treatment at an early stage. As such, you can receive a portion of your total plan coverage without losing out on other benefits.

When The Policy Pays And When It Refunds

The value of an insurance product can be appreciated only through some practical examples. Take two possibilities.

In the first possibility, the insured person finishes the period of insurance coverage without having had a critical illness. In the end, the entire amount of premiums will be returned to him/her. Here, the policy turned out to be unnecessary; however, there was no loss.

In the second situation, the insured person is found to have a covered illness, such as a myocardial infarction. For this reason, $100,000 is paid out. There is no refund of premiums since the insurance payment has already been made. In terms of finances, the outcome is definitely positive.

It is obvious now that the insurance product can bring benefits to the policyholder regardless of its actual application.

How Return of Premium Worked In Practice

A 42-year-old businessman came to our office seeking insurance cover for critical illnesses, which would cover him from losses incurred on account of his business in case such an illness happens. He had no previous history of any illness and was well insured in terms of health care insurance. The main problem he was facing was the high cost of medical expenses if such an illness happened, and the risk of disruption of his business.

After analyzing the available options, he chose an insurance policy for a period of 15 years with a Return of Premium rider for coverage of $100,000.

For those 15 years, he paid premiums totaling $21,600 without experiencing any illness covered by the insurance policy. At the end of the policy period, he received the entire amount he had paid as premiums, hence making the policy profitable for him despite being costly as compared to other similar policies.

This is one of the cases where Return of Premium works perfectly for someone who prefers certainty rather than risking their money through investments.

When Return of Premium Was Not Recommended

A client, a salaried individual aged 38 years, came to us seeking a Critical Illness Insurance Policy. On looking at the available options, it appeared that the right option would be to get an ROP Rider. After analyzing the client’s finances of the client, however, we decided to advise him otherwise and suggest that he go for an ordinary critical illness policy without the ROP Rider.

The main reason was affordability issues. With the ROP Rider included, he would increase the monthly payments to more than twice what he was paying for without the rider. Instead, he settled on getting more coverage in terms of insurance but kept the extra money in a savings account.

In this way, it became easier for him to make use of the funds, unlike with the refund, which would only come after several years.

The case above shows that though ROP Rider is good, it might not be the best option depending on other circumstances.

When Return of Premium Makes Strategic Sense

Return of Premium can be attractive to clients because of its predictability. It is especially suitable for those who are disciplined, careful about risks, and think long-term.

Clients who are healthy, have a steady income, and wish to safeguard their family may find benefit in this product. The concept fits into the philosophy of insurance, which focuses on protecting oneself while also recovering the investment.

Another category of clients that may prefer this insurance policy would be those who are more inclined toward a structured payment plan rather than self-managing investments.

When It May Not Be The Right Choice

Even with its positive points, the Return of Premium approach is not necessarily the best way to go about it. Clients who value flexibility will find themselves paying for something that is not really beneficial to them. People who prefer to invest on their own might find it more useful to purchase cheaper insurance plans and invest the rest of the money elsewhere.

When there is adequate coverage available and no need to upgrade at all, adding the ROP option may just add more layers of complications. Likewise, people with stricter budget constraints can gain more out of maximizing their coverage.

Tax Considerations And Financial Implications

The benefits of Critical Illness Insurance in Canada are the favourable tax implications for payments that may come into play. Specifically, the benefit amount received will be generally free of taxes. Thus, it will be easier to cope with financial difficulties caused by health problems.

At the same time, some insurers may offer various plans for premium returns, which may imply different taxation rules for refunds. In any case, you should consult a tax expert for more information.

Canadian LIC is a licensed insurance brokerage company operating in Canada, offering services from several top insurers, such as Sun Life and Canada Life. We help Canadians in comparing insurance plans, including Critical Illness Insurance, Life Insurance, and other types of coverage.

We have no connection with any of our carriers, so we can offer unbiased suggestions.

Closing Thought

The choice between a basic Critical Illness Insurance Plan and a Critical Illness Insurance Plan with a Return of Premium rider isn’t a matter of what’s correct or incorrect. It’s about being in sync. If you’re compatible with the plan structure, then you see its benefits immediately.

Those comparing Critical Illness Insurance refund Canada options will likely see how their own goals affect which one makes sense for them.

About The Author

Harpreet Puri is a licensed insurance advisor with over 14 years of experience helping individuals and families structure Critical Illness Insurance, Life Insurance, and long-term financial protection strategies. As a senior advisor at Canadian LIC, he has guided hundreds of clients through complex decisions involving critical illness coverage, premium riders, and risk management planning across Canada.

FAQs

A ROP Rider will not be able to switch from one insurer to another. It would mean that you have to open up a new Critical Illness Insurance Policy and begin paying premiums all over again.

Yes, even though the refunded premiums represent the same amount paid initially, they do not factor in inflation, whose effects will be seen over the period of a lengthy insurance contract, thus making them less valuable over time.

Insurers permit the combination of premium riders, such as waiver of premium or disability riders, with ROP Riders. But with more riders being included, the cost of premiums rises.

The person is no longer eligible for any refundable premium payments in case there is lapsed insurance due to cessation of premium payments. Some companies do provide policies for reinstatement; however, this varies according to the type of critical illness policy.

Insurance companies such as Sun Life and Canada Life offer Critical Illness Insurance with a Return of Premiums as an added benefit. Premium riders are offered by insurance companies with varying time frames for the returns based on the policy period and premium payments.

Yes, most Critical Illness Insurance Policies with a ROPe provision provide insurance protection against more than one serious illness, normally 20 to 30 diseases like cancer, strokes, and heart attacks. Other insurers go even further by adding limited coverage for preliminary stages of the disease, thereby extending Critical Illness Insurance Coverage.

There are many insurance companies that have incorporated software systems to help determine the Critical Illness Insurance cost and provide quotes through the Internet. For example, insurance companies such as Sun Life have incorporated an easy-application feature for some types of coverage policies.

The introduction of a ROP Rider ensures that one receives the maximum refunds in case there is no claim. It also ensures that people are assured of receiving their money in case there is nothing to claim. However, it means that one will incur higher premiums and hence increased costs.

In the case of a 40-year-old in good health, typical premiums for Critical Illness Insurance tend to vary from $40 to $100 per month. The inclusion of the return-of-premium clause tends to drive up premiums considerably, with increases ranging from 40% to 70%.

The application process requires the selection of an existing critical illness plan first. Next, the insured is required to opt for a ROP Rider, which would be attached to their Critical Illness Insurance cover at the time of application. Thereafter, medical disclosures may be necessary along with possible medical examinations.

Short-term Disability Insurance Coverage is typically provided by insurers such as Sun Life Financial, Manulife, and Canada Life. This insurance is typically covered under an employee group plan or within the overall structure of the insurance plan.

A Disability Insurance claim usually requires submission of medical evidence, proof of loss of income, and information about the nature of your work. The insurer will then determine if your situation qualifies for the total disability as defined in the policy contract.

When requesting a customized Disability Insurance quote, you would normally need to give your age, income per year, occupation, and medical condition. Thereafter, you may be able to have various Disability Insurance quotes reviewed by an online comparison tool or an insurance broker, who will then suggest income-protection policies for you.

Disclaimer

This content is provided for general informational purposes only and does not constitute financial, insurance, or tax advice. Individual needs vary, and readers should consult a licensed insurance advisor or financial professional before making decisions regarding Critical Illness Insurance, Return of Premium, or any related coverage. Policy features, availability, and terms may differ by insurance provider.

Sources and Further Reading

- Critical Illness Insurance Overview – Explains how Critical Illness Insurance works in Canada, including return-of-premium options and payout structure.

- Sun Life Critical Illness Insurance Details – Provides a detailed breakdown of Return of Premium structures, refund percentages, and eligibility timelines.

- Sun Life Critical Illness Insurance Overview – Overview of available plans, coverage options, and policy features for Critical Illness Insurance in Canada.

- Canada Life Critical Illness Insurance Guide – Covers tax-free lump sum benefits, policy structure, and financial planning considerations.

- Canada Life Critical Illness Insurance Product Page – Includes return-of-premium options and how policies can be structured based on client needs.

- Sun Life Partial Benefit Coverage Details – Explains partial benefits for early-stage illnesses and how payouts work within policies.

- Investment Executive – Canada Life Product Updates – Discusses newer features such as premium payback and refund options in Canadian policies.

Key Takeaways

- Critical Illness Insurance with Return of Premium blends protection with potential premium refunds, offering value even if no claim occurs.

- A ROP Rider increases premium payments, but may return all or part of the premiums paid at the end of the policy term.

- The core benefit remains a tax-free lump sum, providing immediate financial support for medical costs, recovery, and lost income when a critical illness is diagnosed.

- Higher premiums vs flexibility is the key trade-off—choosing between guaranteed refunds or lower cost with independent investing options.

- Not all Critical Illness Policies treat partial benefits and refunds the same; understanding payouts tied to claims is essential.

- Leading insurers like Sun Life and Canada Life offer structured Return of Premium options with different timelines and conditions.

- A comparison approach is critical—ROP plans suit long-term planners, while standard plans may better fit budget-focused individuals.

- Real-life scenarios show that Return of Premium works best when aligned with financial discipline, not just the expectation of getting money back.

- Evaluating opportunity cost is important—extra premiums could alternatively be invested outside the policy.

- The right Critical Illness Insurance Coverage depends on personal goals, risk tolerance, and overall financial strategy—not just product features.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- Return of Premium In Critical Illness Insurance Plans In Canada

- What Is Return of Premium Insurance Canada, And Why Does It Exist

- How Critical Illness Insurance Coverage Works In Real Life

- How The Return of Premium Rider Actually Works Over Time

- The Real Cost Difference: What You Pay And What You Get Back

- Comparing ROP, Non-ROP, And Disability Insurance

- Return of Premium Vs Standard Critical Illness Insurance

- Partial Benefits And The Reality Of Claims

- When The Policy Pays And When It Refunds

- How Return of Premium Worked In Practice

- When Return of Premium Was Not Recommended

- When Return of Premium Makes Strategic Sense

- When It May Not Be The Right Choice

- Tax Considerations And Financial Implications

- Closing Thought

Sign-in to CanadianLIC

Verify OTP