- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Key Benefits Of Mortgage Insurance Coverage In Canada

By Harpreet Puri

CEO & Founder

- 10 min read

- June 23, 2026

SUMMARY

Mortgage Insurance Canada plays a key role in enabling home ownership with lower down payment requirements while reducing lender risk. The benefits of Mortgage Insurance include improved loan approval, competitive rates, and structured Mortgage Insurance costs. It also compares Mortgage Protection Insurance with Life Insurance, explains how Mortgage Insurance works in Canada, and highlights smarter coverage options for long-term financial stability.

Introduction

Why Mortgage Insurance Canada Matters More Than Ever

Owning a home in Canada has evolved from a financial aspiration to a well-timed decision based on market conditions, savings, and access to the right financial instruments. Home prices in Canada have been rising steadily over the last decade, and the situation has been compounded by the fact that buyers have been having trouble meeting the requirements for a mortgage. According to the Canada Mortgage and Housing Corporation, a significant percentage of Canadian homebuyers use insured mortgages, and the majority of them are new entrants to the market.

We encounter many people who initially think in terms of Mortgage Insurance as a cost, not a benefit. However, the situation changes when the concept and the benefits are fully understood. Mortgage Insurance is more than just a form of protecting the interests of the lender. It’s about creating opportunities and defining the path forward with confidence in a competitive marketplace.

The benefits of Mortgage Insurance extend far beyond the surface. When the concept and benefits are fully understood, it’s clear to see how this financial structure is a big part of assisting the process of moving forward from renting to owning, and from waiting to planning.

Understanding The Real Role Of Mortgage Insurance

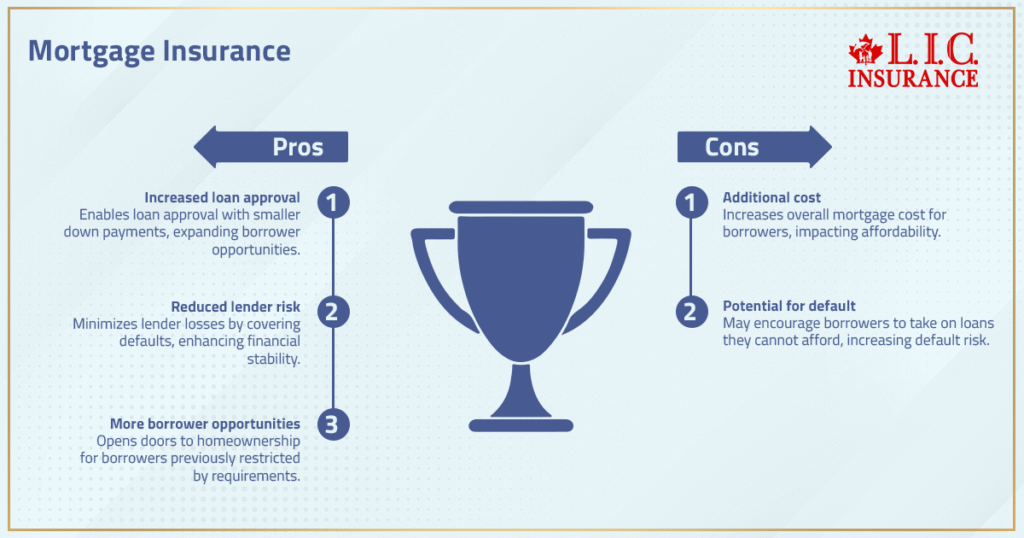

The reason why Mortgage Insurance was created in the first place is to address the risks associated with the approval of a loan. When a borrower seeks to apply for a mortgage and has a smaller down payment, the lender will be exposed to a certain level of uncertainty. If the borrower defaults on the payment, the lender will be exposed to a high level of loss. However, with the presence of Mortgage Insurance, exposure to such risks will be reduced.

This, therefore, creates a situation in which the borrower benefits. While the structure has been created to benefit the lender, the borrower will be the one to benefit in the end. This is because, without the Mortgage Insurance, the application will not be approved. However, with the Mortgage Insurance, the lender will be able to have the confidence to provide the necessary financing.

From a borrower’s perspective, this changes everything. Without mortgage insurance, many applicants would struggle to qualify, especially those who are early in their financial journey. With it, the pathway to securing a mortgage becomes more accessible, structured, and predictable.

Enables Home Ownership Without Long Delays

One of the most significant advantages of having Mortgage Insurance is the fact that it helps to alleviate the biggest obstacle in purchasing a home. For many people in Canadian markets, saving up the full 20 percent to put towards a home can take years. During those years, the price of the home will only continue to go up, making the goal even more out of reach.

With the assistance of Mortgage Insurance Canada, buyers will be able to enter the market with a much smaller down payment. This means that instead of delaying the decision to purchase a home, the individual will be able to enter the market much sooner. This, in turn, will allow the individual to start building equity in the home much sooner.

This leads to a good financial situation over time. This is something that might have been achieved over several years by saving up. For first-time buyers, Mortgage Insurance is likely to be the single factor that makes owning a home possible right now, rather than something to be achieved over several years.

Improves Mortgage Approval Opportunities

Another major advantage of Mortgage Insurance is its ability to improve the outcome of approvals. Lenders consider various factors when evaluating an application for a mortgage. These factors include income, credit history, and any financial responsibilities. However, for some, it can be difficult to meet all these requirements, especially if they are young and/or immigrants.

Mortgage Insurance helps to minimize risk for lenders, thus providing more flexibility for approvals. While it does not eliminate financial responsibility, it helps to create a more balanced approach. Those who were previously denied due to various reasons find that with the inclusion of Mortgage Insurance, their applications are approved.

This is an advantage for individuals who do not necessarily meet the common criteria for obtaining a mortgage. It offers an alternative for those who wish to purchase homes but do not necessarily meet financial expectations. It ensures that an individual’s right to own a home is not denied based on financial history.

Supports Access To More Competitive Interest Rates

The general assumption for many borrowers is that Mortgage Insurance merely adds another cost to borrowing. Although there is indeed a premium, there are circumstances that can make interest rates fall. This is because there is less risk for the lender, so there are competitive rates for insured mortgages as opposed to those which are not.

The effects of a reduced interest rate are felt for the entire length of time for which one has a mortgage. This means that even a small reduction can make a big difference in terms of overall interest payments.

If one looks at Mortgage Insurance as a whole in this way, then one can see that Mortgage Insurance is not just a cost factor but can actually be a part of a financial structure which can increase overall efficiency.

Where Traditional Bank Mortgage Insurance Falls Short

At this point, most homeowners think that all types of Mortgage Insurance are the same. This is where a key difference must be explained. Bank Mortgage Insurance is generally only intended to cover the lender.

Most types of bank Mortgage Insurance have their coverage reduced as the loan amount decreases. This means that although the homeowner is paying the insurance premium, they are getting less and less insurance over time. In addition, the money paid out on a claim goes directly to the bank, not the family. The homeowner has no control over the use of the money, nor is the money dependent on anything other than the loan amount.

This creates a disconnect between what the homeowner believes they are getting and what they really receive. They think they are getting insurance for their family, but what they are really getting is insurance for the bank.

A Smarter Approach: Flexible Mortgage Protection Solutions

A more strategic approach to mortgage protection focuses on flexibility and control. Instead of tying the coverage strictly to the loan, modern solutions combine elements of Term Life Insurance and Critical Illness Protection.

In this structure, the benefit is paid directly to the beneficiary rather than the lender. This allows the family to decide how the funds are used. They may choose to pay off the mortgage, but they can also allocate money toward living expenses, education, or other financial needs.

Another key difference is that the coverage amount remains fixed. Even as the mortgage balance decreases, the insurance benefit does not reduce. This ensures that the value of the protection remains consistent throughout the policy term.

Portability is also a significant advantage. Unlike bank-linked insurance that is tied to a specific lender, these policies can move with the homeowner. If the borrower refinances or switches lenders, the coverage remains intact without the need for requalification.

This level of flexibility transforms mortgage insurance from a basic requirement into a comprehensive financial protection strategy.

Accelerates Equity Growth And Long-Term Financial Progress

One of the most powerful tools in creating financial security is the ownership of real estate. Mortgage Insurance enables the borrower to commence this process at an early stage. This has significant implications for the long-term financial situation. With the regular payment of the mortgage, the outstanding mortgage balance decreases, and the borrower improves his position.

However, the asset may increase in value over the course of the mortgage term. This has the cumulative effect of creating financial security. The advantage of commencing this process early in life cannot be overstated. Rather than waiting until the borrower has sufficient funds for the deposit, the borrower can commence the process immediately. This has significant implications for the long-term financial situation.

Adds Stability In Times Of Financial Uncertainty

The fact remains that life is full of uncertainties, and financial conditions can change in a moment. Mortgage Insurance also plays a crucial role in creating a more predictable borrowing situation by allowing loans to be arranged within safe parameters. While the main aim of Mortgage Insurance is to protect the lender, it also has a positive effect on the borrower.

However, when coupled with flexible protection schemes, the effect is much more powerful. Instead of just providing cover for the mortgage itself, the cover also extends to the entire family. This creates a much more stable situation, even in the face of unexpected challenges.

Final Perspective

Mortgage Insurance is usually made a requirement before an individual is approved for a mortgage. However, the value of Mortgage Insurance is not necessarily found in this, but in what it enables. It enables an individual to make progress with their purchase, access finance effectively, and arrange their mortgage accordingly to create a long-term foundation.

At Canadian LIC, the emphasis is always on enabling the client to think beyond the surface. This means that an appropriate mortgage protection solution is not just about meeting a mortgage lender’s requirements but about providing control, flexibility, and security. This is especially important because it is possible to arrange a mortgage solution that will ensure the home you build now will support you through the future, regardless of how life changes.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

In the case of refinancing your mortgage in Canada, it is not necessarily the case that the current Mortgage Insurance will be included in the refinanced mortgage. It is actually dependent upon the lender as well as the property value. It is therefore important that the Mortgage Insurance cost is considered prior to refinancing.

Additionally, in some instances, it is possible for the Mortgage Insurance to be cancelled when the mortgage amount decreases, and the equity is sufficiently accumulated. This will, however, depend on the type of Mortgage Insurance. For instance, for those with insured mortgages under CMHC Mortgage Insurance, the cancellation requirements are more rigorous. It is crucial to evaluate the loan term before considering the cancellation.

The Mortgage Insurance does not cover the failure to pay the mortgage by the borrower. Instead, it covers the lender in case the borrower defaults on the loan. If the borrower wants to be protected in case of failure to pay the mortgage, then the borrower has to consider the Mortgage Protection Insurance.

The requirement for Mortgage Insurance is not for all home loans, but it becomes a necessity when the amount of down payment is less than a certain amount. This is because the lender requires Mortgage Insurance in order to minimize risk. It is not always a necessity, but some people opt for it in order to enjoy better terms for the loan.

In the case of Canada, the main institutions offering Mortgage Insurance services include the Canada Mortgage and Housing Corporation. Additionally, private Mortgage Insurance providers that meet the federal housing regulations can be considered. The main factor in selecting the provider may not be the name but the suitability of the Mortgage Insurance services in meeting the objectives.

The Mortgage Default Insurance is there to protect the lender in case the borrower fails to make payments on the mortgage. This reduces the overall risk for those wanting to lend money. It also allows for home ownership, as those who want to buy a home can do so with a lower down payment and a set premium on their insurance.

The first kind of insurance is the Mortgage Insurance, which protects the lender from default in the payment of the mortgage. Then there is the Home Insurance, which safeguards the homeowner’s property from damage. It is apparent from the above statements that both types of insurance have different uses and purposes.

High ratio Mortgage Insurance is usually necessary when the down payment made on the house is less than 20% of the total cost of the house. This means the borrower will have to take out Mortgage Insurance to cover the risk. While it increases the cost of the Mortgage Insurance, it also enables the borrower to proceed with the purchase.

In most instances, Canadian lenders will require at least a minimum down payment before approving a mortgage with insurance. Although Mortgage Insurance is required, it does not replace the need for money out-of-pocket. The amount borrowed, as well as the individual and lender requirements, will determine the amount of money required as a down payment.

The calculation of Mortgage Insurance premiums depends on various factors, such as the amount of the loan, down payment, and risk profile. The cost of the insurance premium can be included in the loan balance or paid through monthly installments. The cost of the premium varies according to the structure of the loan.

Sources and Further Reading

- Mortgage Loan Insurance Overview – CMHC

Comprehensive explanation of mortgage loan insurance, eligibility, costs, and how Mortgage Insurance Canada works for homebuyers. - Mortgage Insurance Guidance – OSFI

Regulatory framework explaining how Mortgage Insurance protects lenders and supports financial system stability in Canada. - Mortgage Default Insurance Explained – WOWA

Detailed breakdown of Mortgage Insurance cost, providers, down payment rules, and how premiums are calculated in Canada. - Mortgage Insurance Underwriting Practices – OSFI

Guidelines on how mortgage insurers assess risk, lenders, and borrower eligibility within Canadian Mortgage Insurance systems. - Residential Mortgage Industry Report – CMHC

Insights into mortgage trends, policy changes, and the role of Mortgage Insurance in Canada’s housing market. - Mortgage Default Insurance vs Mortgage Life Insurance

Comparison of Mortgage Protection Insurance and Life Insurance strategies to better understand coverage differences. - Mortgage Default Insurance Overview (Disclosure Document)

Explains how Mortgage Insurance enables lower down payment home purchases and protects financial institutions.

Key Takeaways

- Mortgage Insurance Canada plays a critical role in helping buyers enter the housing market sooner by reducing the need for a large down payment while still meeting lender requirements. It improves approval chances by lowering lender risk and often provides access to better mortgage rates, which can reduce long-term borrowing costs.

- The benefits of Mortgage Insurance extend beyond approval, as it supports early equity growth, structured financial planning, and stability during uncertain situations. Mortgage Insurance cost is predictable and can be managed through flexible premium options aligned with the loan structure.

- There is a clear difference between traditional bank Mortgage Insurance and Mortgage Protection Insurance, especially in terms of control, coverage flexibility, and who receives the payout. Evaluating both Mortgage Insurance vs Life Insurance in Canada is essential for building a complete financial protection strategy.

- Overall, understanding how Mortgage Insurance works in Canada allows borrowers to make informed decisions, optimize their home loan structure, and secure long-term financial stability.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- Key Benefits Of Mortgage Insurance Coverage In Canada

- Understanding The Real Role Of Mortgage Insurance

- Enables Home Ownership Without Long Delays

- Improves Mortgage Approval Opportunities

- Supports Access To More Competitive Interest Rates

- Where Traditional Bank Mortgage Insurance Falls Short

- A Smarter Approach: Flexible Mortgage Protection Solutions

- Accelerates Equity Growth And Long-Term Financial Progress

- Adds Stability In Times Of Financial Uncertainty

- Final Perspective

Sign-in to CanadianLIC

Verify OTP