- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

RRSP Withdrawals Rule in Canada: Key Insights

By Harpreet Puri

CEO & Founder

- 12 min read

- June 16, 2026

SUMMARY

RRSP Withdrawals Rule In Canada: Key Insights explains how a Registered Retirement Savings Plan in Canada works, when you can withdraw from your RRSP, and how tax on RRSP withdrawal and RRSP withholding tax affect taxable income. It covers RRSP contribution room, spousal RRSP rules, RRSP to a RRIF conversion, lump sum withdrawal risks, and structured retirement savings strategies to manage tax and protect retirement income.

Introduction

Retirement savings become useful if you understand how to access them properly.

According to the Canada Revenue Agency (CRA), millions of Canadian residents invest in a Registered Retirement Savings Plan Canada to minimize their income tax liabilities and create a well-structured retirement savings plan. Statistics Canada data show that the assets held in a Registered Retirement Savings Plan Canada are one of the largest forms of personal retirement savings in Canada. The Canadian Life and Health Insurance Association (CLHIA) always shows that a Registered Retirement Savings Plan Canada is one of the key components of retirement income security for Canadian families.

We often come across individuals who have been making their Registered Retirement Savings Plan Canada contributions for many years but are confused about the rules for making RRSP withdrawals, tax on RRSP withdrawals, and how RRSP withdrawals affect their income tax liabilities.

Understanding the RRSP Withdrawals Rule in Canada is critical if you want to avoid a hefty tax bill and protect your retirement income.

What Is A Registered Retirement Savings Plan, And How Does An RRSP Work

Before we get to discuss the strategies of withdrawal, it is imperative to address a question that is frequently asked: What is a Registered Retirement Savings Plan?

A Registered Retirement Savings Plan is a government-approved plan for saving money for retirement. It allows an individual to reduce their income for income tax purposes for the year in which they contribute to a Registered Retirement Savings Plan.

When an individual makes a contribution to a Registered Retirement Savings Plan in Canada, they earn:

- Contribution room based on prior income

- RRSP deduction limit

- Tax-deferred growth on RRSP investment

Many clients ask: How does an RRSP work?

Here is the simplified structure:

- You contribute to the savings plan.

- The contribution reduces your taxable income.

- Investments grow tax sheltered.

- When you withdraw money, it becomes taxable income.

The key distinction is that RRSP is not tax-free. It is tax-deferred. That means you will eventually pay tax when you withdraw funds.

RRSP Contribution Room And Deduction Limit

Your RRSP contribution room builds up over the years, depending on the income you have earned. The CRA calculates your RRSP deduction limit and notifies you through your Notice of Assessment.

Unused RRSP contribution room is carried forward if you do not use it. However, once you start making withdrawals from your RRSP account, the corresponding contribution room is lost forever.

Unlike a Tax-Free Savings Account, where the contribution room is regained after making withdrawals, the RRSP contribution room cannot be regained. This is an important factor to consider before making an early withdrawal.

It is always advisable to consider the contribution room before making a withdrawal from the RRSP account.

RRSP Withdrawals Rule In Canada

A question that many Canadians ask us directly: Can I withdraw from an RRSP anytime?

The answer: Yes, as long as the RRSP funds are not in a locked-in RRSP or other locked-in retirement accounts that were transferred from a registered pension plan.

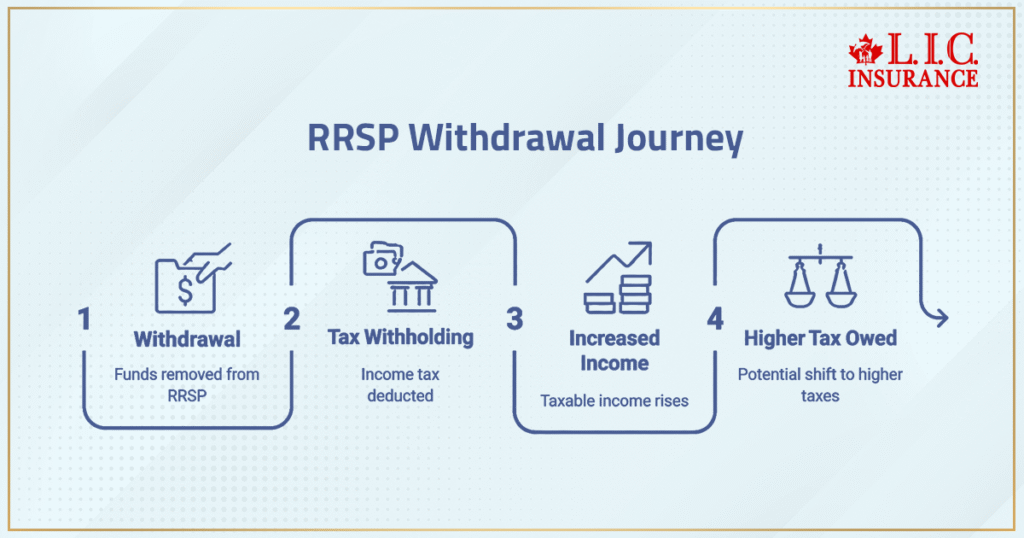

Every RRSP withdrawal results in:

- Immediate withholding tax

- Increase in taxable income

- Possible shift into a higher tax bracket

- Permanent reduction in retirement savings

RRSP withdrawals can happen at any age, but the tax consequences differ depending on timing, amount, and income level.

The decision to withdraw funds should never be made casually.

Retirement Savings And The Impact On Taxable Income

However, the entire amount you withdraw from your RRSP will be included in your gross income and total income for the year.

This means:

- You will have to pay income tax.

- Your marginal income tax rate may rise.

- Your provincial income tax may rise.

- Your total tax may expand considerably.

If you are having a high-income year and you withdraw money from your RRSP account, you may have to pay a lot more income tax than you would have paid if you had withdrawn the money from a lower income year.

This is the reason for strategic planning for retirement savings.

RRSP Withholding Tax Explained In Detail

The aspect of RRSP withdrawal, which is often misunderstood, is withholding tax.

When you ask for an RRSP withdrawal, the financial institution will deduct RRSP withholding tax before sending you the funds.

The federal withholding tax rates, outside of Quebec, are applied as follows:

- In small withdrawals, a low percentage of withholding tax is applied

- In medium withdrawals, a high percentage of withholding tax is applied

- In large withdrawals, the maximum withholding tax is applied

However, this withholding tax is not your final tax obligation. It is simply tax withheld in advance.

If your marginal tax rate exceeds the withholding tax rate, you may owe more tax at tax time.

Many clients mistakenly assume that once withholding tax is deducted, no further tax applies. That assumption can lead to surprise tax consequences.

If you make multiple withdrawals in one year, your total taxable income increases, potentially moving you into a higher tax bracket and increasing your total tax.

Understanding RRSP withholding tax versus final income tax liability is essential.

Early Withdrawals And Long-Term Impact

Early withdrawals from your Registered Retirement Savings Plan can create lasting consequences.

When you withdraw money:

- You reduce funds available for future retirement income.

- You permanently lose contribution room.

- You interrupt tax-deferred compounding.

- You increase taxable income immediately.

Even small early withdrawals can reduce the long-term market value growth of RRSP funds.

We encourage clients to evaluate alternatives before withdrawing from their RRSP prematurely.

Lump Sum Withdrawal And Tax Consequences

A lump sum withdrawal may appear simple, but the tax implications can be substantial.

If you withdraw all the funds in one calendar year:

- The entire lump sum becomes taxable income.

- You may enter a higher tax bracket.

- Provincial tax increases total liability.

- You may face additional tax beyond the withholding tax.

- Your tax bill may escalate sharply.

The fair market value of your RRSP investment at the time of withdrawal is what will be used to calculate the amount of tax that is owed.

Lump sum withdrawals can mean a substantial tax liability for the investor.

Seeking advice from a tax expert is highly recommended prior to a lump sum decision.

RRSP Withdrawal Rules At Age 71

Your RRSP must mature by December 31 of the year you turn 71.

At this stage, you must choose one of the following options:

- Convert RRSP to a RRIF

- Purchase an annuity

- Take a lump sum withdrawal

Most Canadians change their RRSP to a Registered Retirement Income Fund.

A retirement income fund RRIF forces you to withdraw a certain amount each year. This minimum amount is part of your income for taxation purposes.

There is no mandatory withholding tax for the minimum amount at the time of withdrawal. However, the income over the minimum amount may attract a withholding tax.

With proper RR SP to RRIF planning, you can enjoy a secure retirement income while controlling the tax risk.

Registered Retirement Income Fund And Guaranteed Income Options

Converting RRSP to a RRIF allows structured retirement income withdrawals based on CRA guidelines.

Alternatively, some clients choose to purchase an annuity, creating guaranteed income for life or for a specified period.

In both cases:

- Income received is taxable.

- Planning affects the marginal tax rate.

- Strategic withdrawals reduce tax pressure.

Understanding how registered retirement income fund withdrawals interact with taxable income is essential for preserving retirement savings longevity.

Lifelong Learning Plan And Education Withdrawals

The Lifelong Learning Plan allows you to withdraw money from your RRSP for full-time education or training for yourself, your spouse or your common-law partner.

LLP withdrawals are tax-free at the time of withdrawal, provided the eligibility criteria are met.

However:

- There is a defined repayment period.

- If repayments are missed, the unpaid amount becomes taxable income.

- LLP withdrawals must follow CRA rules strictly.

The lifelong learning plan LLP offers flexibility, but discipline is required to avoid unintended tax consequences.

Home Buyers Plan HBP And Down Payment Strategy

The money can be withdrawn tax-free under the Home Buyers Plan HBP for a qualifying down payment.

The money has to be paid back within the stipulated time frame. Failure to do so will cause the money to be added to income.

The Home Buyers Plan is one of the few ways to withdraw money from your RRSP without a right away tax impact.

Spousal RRSP And Attribution Rules

A spousal RRSP helps equalize retirement income between spouses.

However, spousal RRSP withdrawals follow attribution rules:

- If contributions were made recently, the contributing spouse may have to pay income tax.

- The spouse or common law partner cannot bypass tax obligations through short-term shifting.

Proper planning with a financial advisor prevents unintended tax consequences.

Locked-In RRSP And Pension Transfers

If you received your RRSP from a registered pension plan, it is called a locked-in RRSP.

Locked-in accounts are those that restrict access until retirement unless certain hardship provisions are met.

It is always best to verify with both your RRSP provider and financial institution regarding accessibility.

Best Way To Withdraw Money From RRSP Online

The best way to withdraw money from an RRSP online involves:

- Contacting your RRSP issuer.

- Confirming withholding tax details.

- Understanding tax implications.

- Arranging direct deposit to your bank account.

- Consulting a tax professional if needed.

Planning withdrawals near tax time may help manage total income and minimize tax surprises.

Managing Tax Brackets And Avoiding A Hefty Tax Bill

Strategic withdrawal planning focuses on:

- Keeping taxable income within lower tax brackets.

- Spreading withdrawals across multiple years.

- Coordinating RRSP withdrawals with retirement income sources.

- Using tax-free savings account funds strategically.

- Minimizing more tax exposure.

A poorly timed withdrawal can generate more tax than anticipated.

Final Thoughts On RRSP Withdrawal Rules In Canada

Understanding the RRSP Withdrawals Rule in Canada enables you to protect your retirement savings.

You can make a withdrawal at any time, but every withdrawal has tax consequences.

We assist clients in making a well-planned approach to ensure:

Reduced income tax spikes

Marginal tax rate

Preservation of the contribution room

Long-term retirement income protection

Avoiding tax consequences

Proper planning enables your registered retirement savings to work for you instead of against you.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Yes, however, you must consider the impact on your taxable income and income for the year due to the RRSP withdrawal. This could affect income benefits, for example, the Guaranteed Income Supplement or provincial tax credits, as a higher income can decrease these benefits. Tax planning goes beyond merely paying taxes, so you should plan carefully in order to avoid a large tax liability. Careful planning can help you maintain long-term stability in your retirement income sources.

The RRSP withholding tax is simply an advance payment of taxes, which is applied when you withdraw the funds from your financial institution. The actual amount of taxes owed is based on your marginal tax rate and overall income, which is calculated when you file your income tax return. If the amount withheld is less than you actually owe, you will need to pay additional taxes at tax time. Strategic planning can help you avoid paying more taxes than you need to.

When you withdraw money from your RRSP, the contribution room used to make that deposit does not return, even if you had unused RRSP contributions available. This can permanently reduce future retirement savings capacity. Early withdrawals may also affect your long-term savings plan growth. Reviewing contribution room status before accessing RRSP funds is essential.

The decision between RRSP conversion to a RRIF and a lump sum depends on the strategy for income during retirement and the tax situation. A retirement income fund RRIF can provide a structured income strategy for dealing with income taxes. A lump sum can place the individual in a higher tax bracket and may cause other tax issues. A financial advisor can provide guidance to meet the needs of the savings plan.

A spousal RRSP can help balance income between a spouse or common-law partner, which may result in a lower marginal tax rate for the two. However, the rules of attribution will apply if the money is withdrawn too soon from the account. Proper timing can prevent unfavourable tax effects. Spousal RRSP income can be managed for maximum tax efficiency by coordinating the timing of withdrawals from the account.

Some programs, like the lifelong learning plan and the home buyers plan, allow for temporary tax-free use of money from your RRSP if eligibility requirements and repayment period rules are satisfied. However, if repayment is not made, these become taxable income. It is very important to be aware of these structured exceptions to avoid future complications. It is always wise to check with the Canada Revenue Agency guidelines.

The Home Buyers Plan HBP allows eligible residents of Canada to withdraw funds from their RRSP on a tax-free basis for a qualified home down payment. The funds are required to be repaid to your Registered Retirement Savings Plan within a specific period, or they will be added to your income tax. Therefore, it is always advisable to verify the rules provided by the Canada Revenue Agency before proceeding.

While there is no formal ‘RRSP penalty’ levied by the government, financial service providers may impose administrative charges based on the type of RRSP provider or investment held. In addition, making early withdrawals may also result in market value adjustments or deferred sales charges for some types of RRSP investment products, such as mutual funds. Regardless of the provider, withholding tax and income tax laws are still administered by the Canada Revenue Agency. Knowing the provider fees can help minimize unnecessary costs beyond taxes.

The best RRSP for withdrawals depends on flexibility, fee structures, and access to structured income solutions for retirement. Banks, credit unions, and independent financial institutions have different RRSP withdrawal processes and RRSP to RRIF conversion processes. Some financial institutions may offer easier transfer funds services for RRSP withdrawals. It is best to compare services with a financial advisor for proper alignment with your retirement savings strategy.

Yes, many financial organizations permit scheduled withdrawals after your Registered Retirement Savings Plan is converted to a registered retirement income fund. Such automatic payments may help manage your income taxes more evenly throughout the year. Before age 71, however, you may withdraw funds from your RRSP on a requested basis rather than on a scheduled basis. Be sure to check on the rules for a minimum amount before setting up any scheduled payments.

The basic rules for withdrawing money from the RRSP are governed federally; therefore, the withholding tax rules and taxable income rules are the same for all providers. However, the administrative rules for timelines, fees for transactions, and the methods for processing may differ for each RRSP provider. Some may require additional documentation before withdrawing the money from the RRSP account, especially if it is a locked-in RRSP account.

Sources and Further Reading

Government & Regulatory Sources

- Canada Revenue Agency (CRA)

- Registered Retirement Savings Plan (RRSP) overview

- RRSP withdrawal rules

- RRSP withholding tax rates

- Home Buyers’ Plan (HBP) details

- Lifelong Learning Plan (LLP) rules

Website: https://www.canada.ca/en/revenue-agency.html

- Statistics Canada

- Household retirement savings data

- Registered Retirement Savings Plan participation statistics

Website: https://www.statcan.gc.ca

Industry & Financial Education Authorities

- Financial Consumer Agency Of Canada (FCAC)

- RRSP basics and retirement income planning

- Tax implications of RRSP withdrawals

Website: https://www.canada.ca/en/financial-consumer-agency.html

Professional Planning Resources

- Chartered Professional Accountants Of Canada (CPA Canada)

- Income tax guidance

- Marginal tax rate impact on withdrawals

Website: https://www.cpacanada.ca

- Government Of Canada – Retirement Income Planning Tools

- RRSP and RRIF minimum payment tables

- Tax filing guidance

Website: https://www.canada.ca

Key Takeaways

- RRSP Withdrawals Are Taxable: Any RRSP withdrawal increases your taxable income and may move you into a higher marginal tax rate, affecting your overall tax bill.

- Withholding Tax Is Not Final Tax: RRSP withholding tax is only an advance payment. You may still owe more income tax at tax time, depending on your total income.

- Contribution Room Is Permanently Lost: When you withdraw money from your Registered Retirement Savings Plan in Canada, the contribution room used does not reset.

- Age 71 Conversion Is Mandatory: You must convert RRSP to a RRIF, purchase an annuity, or take a lump sum withdrawal by the end of the year you turn 71.

- Structured Programs Allow Tax-Free Access: The Home Buyers Plan HBP and Lifelong Learning Plan LLP allow temporary tax-free withdrawals if repayment rules are followed.

- Spousal RRSP Rules Require Timing: Spousal RRSP withdrawals may trigger attribution rules if contributions were made recently.

- Strategic Planning Reduces Tax Exposure: Coordinating RRSP withdrawals with retirement income, tax-free savings account funds, and other retirement savings sources helps manage taxable income efficiently.

- Professional Guidance Matters: Working with a financial advisor and tax professional ensures you minimize tax implications and protect long-term retirement savings.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- RRSP Withdrawals Rule in Canada: Key Insights

- What Is A Registered Retirement Savings Plan, And How Does An RRSP Work

- RRSP Contribution Room And Deduction Limit

- RRSP Withdrawals Rule In Canada

- Retirement Savings And The Impact On Taxable Income

- RRSP Withholding Tax Explained In Detail

- Early Withdrawals And Long-Term Impact

- Lump Sum Withdrawal And Tax Consequences

- RRSP Withdrawal Rules At Age 71

- Registered Retirement Income Fund And Guaranteed Income Options

- Lifelong Learning Plan And Education Withdrawals

- Home Buyers Plan HBP And Down Payment Strategy

- Spousal RRSP And Attribution Rules

- Locked-In RRSP And Pension Transfers

- Best Way To Withdraw Money From RRSP Online

- Managing Tax Brackets And Avoiding A Hefty Tax Bill

- Final Thoughts On RRSP Withdrawal Rules In Canada

Sign-in to CanadianLIC

Verify OTP