- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

How Money Back Life Insurance Works And Benefits

By Pushpinder Puri

CEO & Founder

- 10 min read

- June 22, 2026

SUMMARY

Money Back Life Insurance Canada combines life coverage with periodic payouts. It explains how Money Back Life Insurance works, including death benefit, survival benefits, and Cash Value Life Insurance Policy features. It compares Term Life Insurance with money back and evaluates if a Money Back Policy is worth it in Canada based on costs, benefits, and financial goals.

Introduction

Why More Canadians Are Rethinking Life Insurance

Life Insurance in Canada is no longer just about the safety net. According to the Canadian Life and Health Insurance Association, Life Insurance is now part of the financial planning strategy for many Canadian households. This is because people are looking for more from Life Insurance than just the basic safety net. There is a greater need for people to see Life Insurance as an investment that can provide value to them while they are still alive. This is the reason why people are looking for Money Back Life Insurance in Canada.

We often come across people who are not sure about paying insurance premiums for many years without seeing any returns on investment, unless something untoward happens. This is the reason why people are looking for Money Back Life Insurance in Canada. This type of Life Insurance not only provides financial security but also the liquidity that people often seek when they are juggling multiple financial objectives at the same time.

A Life Insurance Policy with money back is not simply about coverage. It is about timing, access to funds, and aligning insurance with real-life needs such as a child’s education, retirement planning, or managing financial requirements during uncertain economic conditions.

What Is Money Back Life Insurance And Benefits (Life Insurance Policy Explained)

A Money Back Policy is a form of Life Insurance Policy in which there is a benefit paid out at regular intervals during a given time period. This is different from a Term Life Insurance Policy, in which there is a payout when the insured passes away. Under a Money Back Policy, there is a payout when one is still alive.

To those asking what is Money Back Life Insurance and what the benefits associated with it are, one can say that a Money Back Policy is a hybrid form of Life Insurance in which one is able to save as well as protect themselves. There is a payout every time one is still alive, in addition to having a Life Insurance Policy.

This is different from a regular savings plan in which one invests in a portfolio in hopes of earning a return on investment. Under a Money Back Policy, one is able to make a financial commitment in which there is a payout based on what one has paid in terms of premiums. This is a more reliable way of saving in the long term, as one is not exposed to any form of risk.

How Money Back Life Insurance Works (Premium Life Insurance Work Explained)

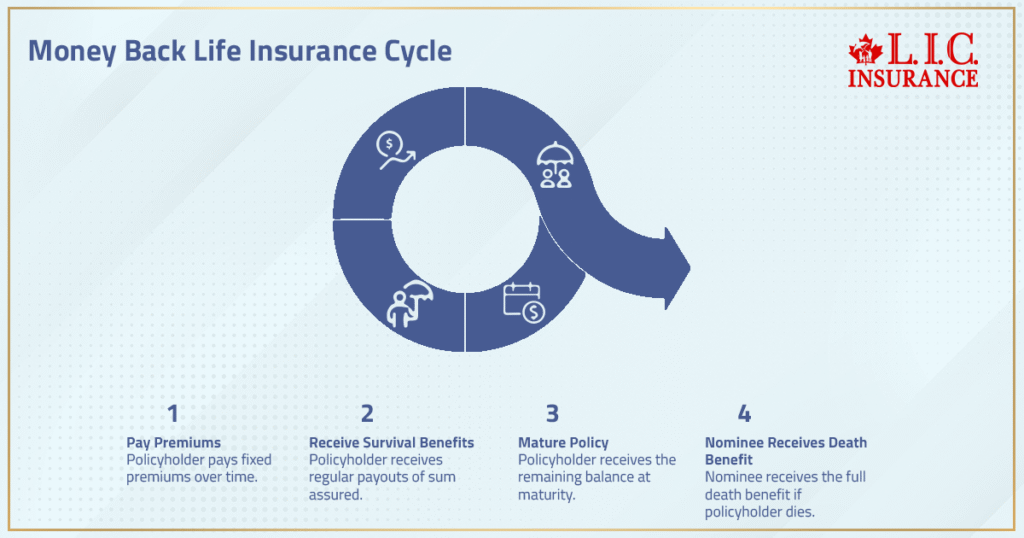

To comprehend the concept of Money Back Life Insurance, it is vital to comprehend how the flow of money is structured in this type of policy. The policyholder agrees to pay premiums over a particular policy duration. The policy premiums are fixed and are determined at the outset.

Over time, a certain percentage of the sum assured is paid back to the policyholder at regular intervals. This is a guaranteed payout and represents the survival benefits of this type of policy.

At maturity, the balance is paid to the policyholder. If death occurs, the nominee receives the entire death benefit payout, irrespective of any payouts received in the past.

This two-fold benefit helps to ensure that the premium Life Insurance work model is beneficial in both the short term and long term, providing liquidity in life and protection in case of death, which is a sad event in life but a reality nonetheless.

Cash Value Life Insurance And How Cash Value Builds Over Time

For many, Money Back Plans are often related to Cash Value Life Insurance. However, there is a slight variation in the structure. Generally, a Cash Value Life Insurance, which can be either universal life or whole Life Insurance, relies heavily on the long-term accumulation of a cash value account.

However, Money Back Plans place more emphasis on scheduled payments. Yet, there can be an option to have a cash value account, which can allow the individual to accumulate more cash over time. This Life Insurance can provide an individual with an added source of support.

The accumulation of the cash value account occurs over time according to the structure set up by the insurance company. While it does not accumulate quite as quickly as in universal Life Insurance, it can provide an individual with a sense of security, especially if he or she values stability over other investment opportunities.

Death Benefit And Life Coverage: What Your Family Actually Receives

One of the main advantages of this type of insurance policy is that there is no compromise on the level of protection. The sum assured in the policy is not compromised even in the event of multiple claims during the policy term.

In the event of a death, a lump sum is paid out to the nominee, which can then be utilized immediately as a source of support.

This structure ensures that a Life Insurance Policy is able to continue to serve its main objective of protecting the future of a family in a way that is reassuring and protective.

Can You Borrow Money From A Money Back Policy?

There are some policies that offer the facility of borrowing money from the overall policy value. This is a good option in case of emergencies where liquid funds are required.

The policyholder may use these funds for a down payment, for a business requirement, or for filling a gap in the financial needs of the policyholder. The loan is offered by the policy with a fixed interest payment. The loan is deducted from the final payment if not cleared by the policyholder.

However, it is important to use this facility after consulting a financial advisor or a financial professional so that the long-term financial plans are not hampered.

Tax Advantages And Life Insurance Taxable Rules In Canada

One of the most important advantages of a Life Insurance Policy is tax efficiency. According to the Canada Revenue Agency, “the receipt of a death benefit from a Life Insurance Policy is not included in taxable income.” This is one of the most important advantages of a Life Insurance Policy.

However, there are some elements of a Life Insurance Policy related to cash value that may be subject to tax implications. These may be included in taxable income as per the Income Tax Act. It is important to know when a Life Insurance Policy is subject to tax implications in order to avoid any tax liabilities.

It is always better to consult a tax advisor or tax expert in order to structure a Life Insurance Policy in a way that can benefit from tax advantages.

Money Back Life Insurance Vs Term Life And Whole Life Insurance

Comparing various Life Insurance Plans, in this case, Term Life, Money Back, Whole Life, and Universal Life, they are all unique in their respective ways. Term Life offers affordable protection with no returns, while Whole Life and Universal Life are centered on building long-term cash value, which is more expensive.

The Money Back Policy, on the other hand, offers periodic returns along with protection, which is ideal for those who want protection and returns at the same time. Although this policy attracts higher premiums than term life, it offers returns, which are not available in term life.

This policy is ideal for those who value returns over risk, as they are assured of their returns, unlike in other high-risk, high-return investments.

Is Money Back Policy Worth It In Canada? (Real Decision Framework)

To make a decision regarding whether is Money Back Policy worth it in Canada or not, one has to keep in mind one’s own requirements and priorities. For people who are low-risk takers and want fixed returns on their investment, this policy can prove highly advantageous.

It is always important to keep in mind the opportunity cost as well. If one were to invest in mutual funds, one might earn more compared to what is earned in this policy. The cost and cost-plus associated with this policy should also be taken into consideration.

The decision completely depends on how well you can match your requirements with your financial planning strategy.

Money Back Life Insurance Benefits You Should Not Ignore

The value of Money Back Life Insurance benefits lies in the predictability of the returns. The policyholder will enjoy regular payments, also known as survival benefits, while enjoying life cover every month.

The payments will come in handy for any plans that the policyholder may have. The policyholder will enjoy the returns even if he outlives the policy period. Therefore, Money Back Life Insurance outliving scenarios are very practical.

Money Back Life Insurance is a very predictable financial tool for any person who needs stability.

Common Risks: Policy Lapses, Costs, And Hidden Trade-Offs

Though it has its own advantages, the Money Back Policy also involves some level of risk. Failure to pay the premium might cause the policy to lapse, which might cause the insured to lose the benefits. Secondly, the premium is high compared to the standard Term Life Insurance premium, which might not be affordable.

In terms of the returns, it is low compared to the market-linked investments. It is important to evaluate if the policy is meeting your financial requirements.

Who Should Consider A Money Back Life Insurance Policy?

This type of insurance plan is most appropriate for individuals who appreciate a certain level of predictability and a structured approach to their financial planning processes. Families with long-term commitments, such as a child’s education, will appreciate this type of plan.

This type of plan is most appropriate for individuals who would like a certain level of returns on their investment, as opposed to market-linked investments. It is always advisable to seek professional advice from a financial planner to ensure this plan works well with your financial plan in general.

How To Choose The Right Insurance Company In Canada

Choosing a good insurance company is a vital step in achieving a high level of satisfaction with your insurance policy.

Some of these factors include the claim settlement ratio, stability, and transparency.

A seasoned insurance company will provide you with clear policy conditions and quality service.

We help clients compare a number of insurance companies to get the most appropriate policy according to their needs.

Final Thoughts: A Balanced Approach To Protection And Returns

The Money Back Life Insurance Policy provides an individual with a method to plan their finances. This policy offers protection, savings, and investment, which can be considered an important option for an individual.

This Life Insurance Policy can be considered an important option for an individual who wants to utilize their Life Insurance in an active manner. This policy offers an individual a balanced option to utilize their Life Insurance in an active manner. This policy can be considered an important option for an individual who wants to utilize their Life Insurance in an active manner.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Yes, the Money Back Life Insurance Canada Plan can help provide supplementary retirement income through planned payoffs during the later policy years. This helps minimize the use of the savings while still providing Life Insurance coverage. This is one way many clients seek to make the insurance coverage work towards meeting financial objectives while avoiding market risk.

One policy type is the Cash Value Life Insurance Policy, which focuses on building of the cash value. The other type is the Money Back Policy, which focuses on the guaranteed payback. The best policy for an individual who wants predictable returns instead of building the cash value is the Money Back Policy.

These portions can be considered taxable income, particularly if they exceed limits set in the Income Tax Act. Although the death benefits are tax-free, it is important to know the Life Insurance taxable rules to manage them effectively. This can be done with the help of a tax advisor.

Missing out on premium payments may lead to a lapse in the insurance policy. Some of these plans may offer some leeway, but repeated non-payment of premiums may have an adverse effect on the value of your insurance policy.

However, a Money Back Policy is not a direct replacement for a mutual fund investment because it does not focus on high returns but rather on guaranteed returns. This method is better for those who want to save in a disciplined manner and also want to have Life Insurance benefits.

Yes, there are several insurance companies that offer a premium rider option as part of the policy, which can increase coverage. These types of riders can offer more flexibility in a policy; however, there may be a cost involved in these types of riders. It is up to you to decide what you need in terms of financial planning.

People who are risk-averse, or who have a low risk tolerance, would most likely opt for a Money Back Life Insurance Policy, as they would want a regular payout and a regular rate of return, unlike other market-linked investment plans, which are dependent on market performance.

The selection of a policy duration that matches key financial events, such as a child’s education or retirement, is a key factor. This will help ensure that Life Insurance benefits are available to meet real-world needs. This will help maximize the value of your Life Insurance Policy.

In Canada, true money-back plans are not really offered as standalone products but can be included with Term Life Insurance with return of premium options. Leading insurance companies such as Manulife, Sun Life Financial, and Canada Life offer Money Back Life Insurance Policies, wherein the Life Insurance Policy can return the premium amounts paid.

When comparing a Money Back Life Insurance Canada Plan, you will not only compare premiums, but you will also compare the structure of the insurance policy, return conditions, and benefits of life coverage. It is also important to compare how different insurance companies handle their payments, premiums, and flexibility, and you should consider a professional’s advice.

It is possible to do so, yes. However, the availability of options might be limited depending on the insurer’s rules. There are some insurance companies that offer Simplified Issue Life Insurance Policies. Nevertheless, these policies might come with high premiums. It is important to work with an experienced insurance provider to find the right plan that suits your health profile.

Return of premium features make the policy more costly compared to standard Term Life Insurance products, as the cost includes the refund of the premium payments made during the policy term in the event that the policyholder survives the policy term. The cost is subject to the policyholder’s age, coverage amount, and policy duration; however, the policy is considered costly as it includes an extra benefit.

Sources and Further Reading

- Money Back Life Insurance Canada Explained

Detailed explanation of how Money Back Life Insurance works in Canada, including return of premium structures and policy comparisons. - Life Insurance Guide – Government Of Canada

Covers how Life Insurance works, including term life, cash value, and borrowing options from policies. - CLHIA Insurance Glossary And Definitions

Explains key terms such as cash value, death benefit, and how insurance companies structure policies. - Return Of Premium Life Insurance Explained

Provides insight into how return of premium features work and when payouts may apply. - Tax Treatment Of Life Insurance Premium Returns

Explains how returned premiums may be treated under Canadian tax rules and when they may become taxable income. - Cancelling Life Insurance And Cash Value Insights

Covers policy cancellation, refunds, and how cash value or policy loans can be used effectively.

Key Takeaways

- Money Back Life Insurance Canada combines protection with returns, offering periodic payouts along with a guaranteed death benefit, making it different from standard Term Life Insurance Policies.

- Understanding how Money Back Life Insurance works is essential, as structured premium payments provide both survival benefits and long-term financial protection.

- Unlike traditional Cash Value Life Insurance Policy options such as whole Life Insurance or universal Life Insurance, Money Back Plans focus more on predictable payouts than long-term cash accumulation.

- The policy’s death benefit remains intact, ensuring a lump sum payout for the family’s future even if periodic payouts have already been received.

- Certain plans allow you to borrow money through policy loans, but managing the outstanding loan and interest payments is important to avoid reducing final benefits.

- There are important tax benefits, as most death benefit payouts are tax-free in Canada, although some components may be considered taxable income under the Income Tax Act.

- A Money Back Policy sits between term life and permanent Life Insurance, offering moderate cash value, guaranteed returns, and continued life coverage, but often at a higher cost.

- Whether Money Back Policy is worth it Canada depends on your financial goals, risk tolerance, and preference for guaranteed returns over market-linked investment options like mutual funds.

Your Feedback Is Very Important To Us

Privacy Note

Your information will be kept confidential and used solely to provide personalized guidance and insurance solutions. Canadian LIC respects your privacy and adheres to Canadian data protection and anti-spam regulations.

IN THIS ARTICLE

- How Money Back Life Insurance Works And Benefits

- How Money Back Life Insurance Works And Benefits

- How Money Back Life Insurance Works (Premium Life Insurance Work Explained)

- Cash Value Life Insurance And How Cash Value Builds Over Time

- Death Benefit And Life Coverage: What Your Family Actually Receives

- Can You Borrow Money From A Money Back Policy?

- Tax Advantages And Life Insurance Taxable Rules In Canada

- Money Back Life Insurance Vs Term Life And Whole Life Insurance

- Is Money Back Policy Worth It In Canada? (Real Decision Framework)

- Money Back Life Insurance Benefits You Should Not Ignore

- Common Risks: Policy Lapses, Costs, And Hidden Trade-Offs

- Who Should Consider A Money Back Life Insurance Policy?

- How To Choose The Right Insurance Company In Canada

- Final Thoughts: A Balanced Approach To Protection And Returns

Sign-in to CanadianLIC

Verify OTP