John, a 40-year-old father of two, wakes up one day and realizes the uncertainty of life. Every morning, he kisses his kids goodbye, not knowing what the day may hold. The thought of leaving his family without financial support haunts him. So, he begins his quest for security through a Term Life Insurance Policy, hoping to protect his loved ones in case the worst happens. But like many Canadians, John is bogged down by questions and confusion: Does Term Life Insurance really cover death? What if there are exceptions? Many face these concerns when considering Term Life Insurance in Canada.

In this blog, we’ll walk through the ins and outs of how Term Life Insurance covers death in Canada, ensuring you’re equipped with the knowledge to make the best decisions for your family. We’ll share real-life struggles and triumphs, providing clarity through relatable stories. By the end, you’ll understand why securing a Term Life Insurance Policy is not just a choice but a necessity.

Does term insurance cover death?

By Harpreet Puri, June 04, 2024, 6 Minutes

John, a 40-year-old father of two, wakes up one day and realizes the uncertainty of life. Every morning, he kisses his kids goodbye, not knowing what the day may hold. The thought of leaving his family without financial support haunts him. So, he begins his quest for security through a Term Life Insurance Policy, hoping to protect his loved ones in case the worst happens. But like many Canadians, John is bogged down by questions and confusion: Does Term Life Insurance really cover death? What if there are exceptions? Many face these concerns when considering Term Life Insurance in Canada.

In this blog, we’ll walk through the ins and outs of how Term Life Insurance covers death in Canada, ensuring you’re equipped with the knowledge to make the best decisions for your family. We’ll share real-life struggles and triumphs, providing clarity through relatable stories. By the end, you’ll understand why securing a Term Life Insurance Policy is not just a choice but a necessity.

The Basics- Knowing Term Life Insurance

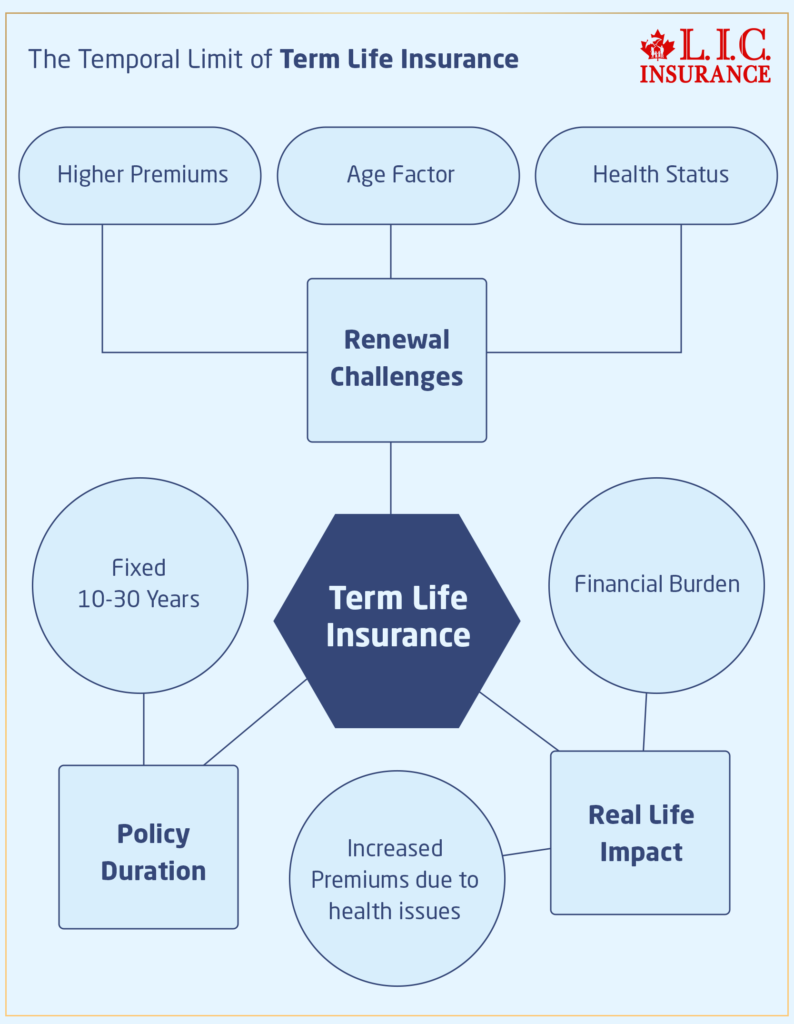

A Term Life Insurance (Term assurance or term plan) is life insurance that provides coverage at a fixed rate of payments for a limited period (as the name suggests, for a certain period), and the applicable term may be one year. At the end of the term period, the policyholder either renews the policy, converts the policy to a Permanent Life Policy, or allows the policy to terminate. This combination of price and simplicity explains why Term Life Insurance is the most common (and most affordable) type of life insurance while buying life insurance in Canada.

Sarah is a 30-something-year-old professional. She chose a Term Life Insurance Policy because it was the cheapest way to make sure her student loans did not become her parents’ responsibility if she died. She was able to pull a few Term Life Insurance Quotes and make the best decision for her based on her financial standing.

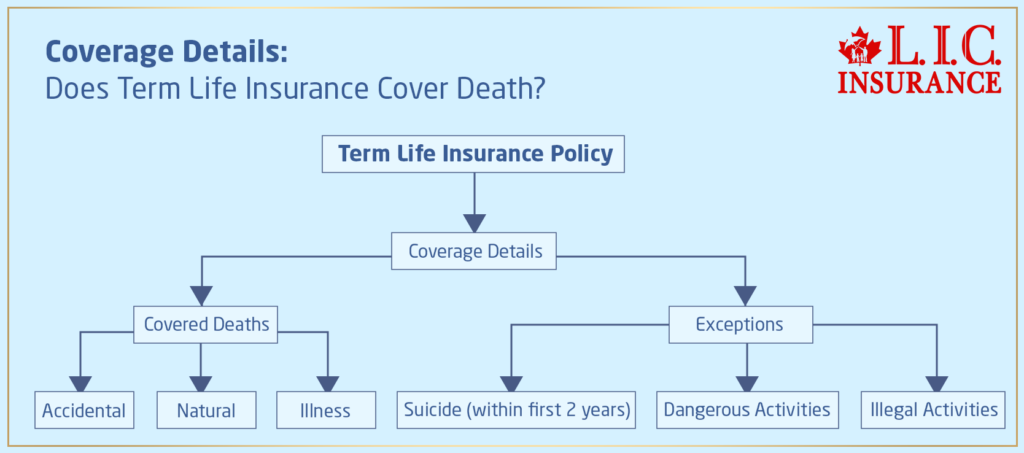

Coverage Details: Does Term Life Insurance Cover Death?

When described in the simplest terms, a Term Life Insurance Policy is designed to give your beneficiaries some sense of security when you pass away. But let’s go a bit deeper. What Happens When A Policyholder Or Insured Person Dies During The Term Of Their Policy? The policy passes to the beneficiaries tax-free as a death benefit. They know that however hard things are, they are protected financially. However, there are some variations from reality. Not all scenarios are covered, and this is important.

Which Deaths Do Term Life Insurance Policies Cover? A Canadian Term Life Insurance Policy is built to be as generic as possible, covering all or almost all causes of death — types such as accidental, natural, or illness. Relieving to know regardless of what was to happen, a sudden accident or a long-term illness, the policy sits as an anchor of financial replenishment for your family.

However, let us not forget about the exceptions, which are typically when the policyholder has their guard down. Most of the time, if you die by suicide within the first two years of when your policy was in effect, your death is not going to be covered. This is a provision almost all Canadian Term Life Insurance Policies carry, but one you should be mindful of from the get-go. Death from dangerous or illegal activities may not be covered either. Every Term Life Insurance is different in its specifics, so it is important to know the fine print!

High Risk and Insurance Life Coverage

So now, let me introduce a real-life example. Consider Michael, a licensed pilot and experienced skydiver. Michael had a unique challenge when it came to getting Term Life Insurance. He used to skydive — a high-risk hobby that would mean he would have to shop around to find the very best Term Life Insurance Quotes. Such pursuits are not allowed by all policies except for under known clauses or extra premiums.

What did Michael do? He shopped around for term life quotes, not just cost, but also differences in how they often covered high-risk activities. Therefore, he is diligent with his work to make sure that his family would be well-off financially if he cannot provide for them due to a bad event that happens to him.

Insurance Involvement

Put yourself in Michael’s shoes. Perhaps you are a fan of mountain climbing, scuba diving, or even a professional athlete. But how do you make sure your Term Life Insurance Policy really takes care of your family? Your best bet is first to try having open and transparent conversations with your insurance company. Be entirely open about all aspects of your life. This openness can help your agent to design an adaptable Term Life Insurance Policy according to your needs.

Why Does This Matters?

Because when you understand your Term Life Insurance Policy inside-out, you are actually protecting your family rather than just writing on paper. You make sure that when you die, your family is truly given the help you meant to give.

When was the last time you read your policy? If you know someone who could use a better understanding of how their Term Life Insurance works, Tell them to contact their provider or compare term life to start with any opportunities. A brief reminder: Knowledge is not just power but also security.

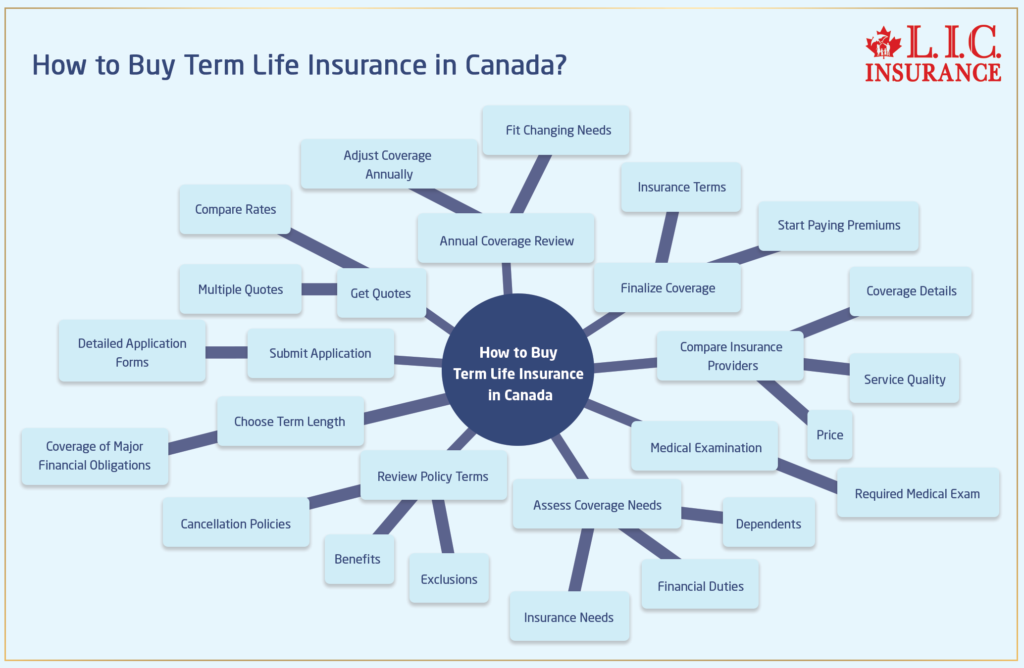

Comparing Canadian Term Life Insurance

While Term Life Insurance premiums are a major concern when shopping for the best Term Life Insurance in Canada, they are just one piece of the puzzle. To help you understand the highly complex decisions ahead, we broke down a series of actionable steps.

Step 1: Know Your Coverage Needs

The first thing to do is estimate the coverage you need so you can later select the best possible plan. This includes the amount of debts that you owe, your income, and the financial needs of your dependents. Using an online coverage calculator is the best way to determine the ideal amount of coverage that would safeguard the future of your family.

Meet Tom. With the responsibility of being the primary breadwinner in his household, he went to an online calculator to multiply Sibley’s income by the number of years he would need to sustain his spouse and children, pay for his mortgage, and offer his children a college fund and get the amount of coverage based on those figures. By taking proactive measures, Tom makes sure his family will have affordable Term Life Insurance that fits in with their long-term financial goals.

Step 2: Compare Term Life Insurance Quotes

The next step, once you know how much coverage you need, is to get quotes. Many websites across Canada allow you to compare Canadian Term Life Insurance Quotes from a wide range of insurers. Compare premiums and terms and conditions.

Shobhita explored various online platforms to gather quotes. She noted differences in premiums, terms, and the extent of coverage. This diligent comparison allowed her to understand the market and pinpoint a policy that offers the best value for her circumstances.

Step 3: Policy Flexibility and Exclusions

There are terms and conditions associated with every Term Life Insurance Policy and it should be customized to your personal needs. Specific causes might be left out when you apply for death benefits, or the policy can have built-in options for increasing or decreasing your coverage.

Raju found a Term Life Insurance Policy that initially seemed perfect with low premiums. But when he looked through the policy in more detail, he found that this did not include death from adventurous pursuits, which was a no-go zone for a keen mountain biker. A good reminder that an essential thing to do is read the fine print.

Step 4: Look at the Insurer’s Reputation/Customer Service

It is always a good idea to have an insurer whose claims experience and customer service link well with the experience your family would have to go through when they moved to claim the policy. Check reviews and ratings to see how insurance companies handle policyholders in their time of need.

Linda chose one of the lower-cost insurers but also one with a reputation for great customer service. The emotional support its representative lent to her family when they needed to make a claim lessened the trauma involved and further proved to Linda that she had made the right decision.

Step 5: Take into account the terms and conditions of renewal

Last but not least, think about the expiration of the term. Can you renew your policy? Will you need a medical exam to do so? How do these factors affect your long-term insurance strategy?

Kevin probably wouldn’t have been able to walk away from that huge chunk of money unless he could have gotten a second term life policy that would allow him to renew without a medical exam, in order to guard against losing the coverage as he aged and his health deteriorated. Kevin is grateful to have had this insight, as it ensures he will remain insurable and have peace of mind.

While the confusion in Canadian Term Life Insurance can be overwhelming, you are not alone. Each step you take brings you closer to securing a financially stable future for your loved ones. Have you tried to compare Term Life Insurance Policies? What struggles did you have to face? Tell us your stories, or we’d be happy to discuss your unique situation. We shall also help you in your journey to thus protect your future to the best of your ability.

Chen Family's Story

Despite the general perception that Canadians are well-educated on the intricacies of insurance claims and policy terms, this is a pervasive problem. This can be confusing because it can be difficult to know the ins and outs and this may cause a surprise when making a claim. Except, maybe we should just look at the Chen family, who spent two years trying to get the death benefit when their father dies unexpectedly. Their case showcases the need to fully comprehend your policy and make sure that all the proper paperwork is done.

Wrapping It All Up

As we’ve explored throughout this blog, Term Life Insurance is a critical safety net designed to ensure that your loved ones are taken care of financially if the worst were to happen. Whether you are a single professional, a high-risk hobbyist or a new parent, it is evident that a Term Life Insurance Policy can save you a pretty penny.

Now, it’s your turn to take action. Canadian LIC stands by you to provide expert advice and assistance throughout the journey. Wait not for uncertainty to knock on your door; buy your Term Life Insurance today and safeguard your family. Peace of mind is not an option; it is a necessity. Contact Canadian LIC today to get Term Life Insurance,

In this blog, we’ve uncovered the facts, shared stories, and simplified the complexities of Term Life Insurance. With the right knowledge and a proactive approach, securing your family’s financial future is within reach. Don’t let another day pass without ensuring your loved ones are protected. Connect with Canadian LIC today and start your journey towards a secure future.

Find Out: The age to stop buying term life insurance

Find Out: The advantages of Short Term Life Insurance

Find Out: Term Life Insurance Main Disadvantage

Find Out: Do the rates of Term Life Insurance go up?

Find Out: How to choose Term Insurance?

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Frequently Asked Questions(FAQs) About Canadian Term Life Insurance

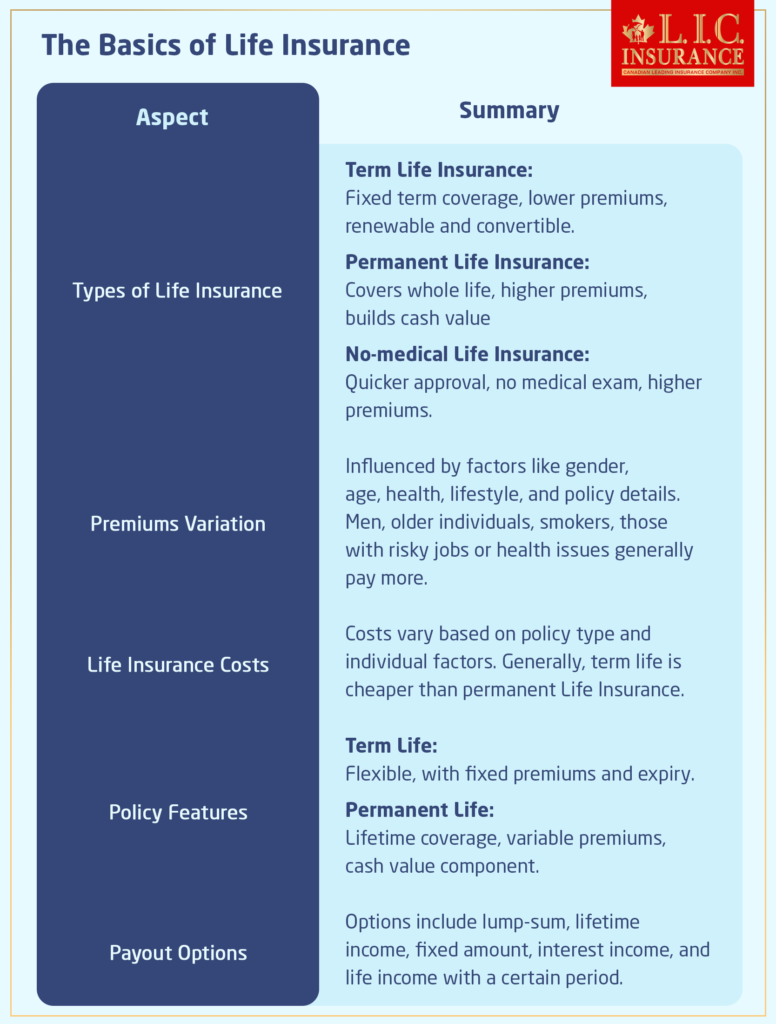

Term Life Insurance provides coverage for a specific period, typically 10-50 years. In Canada, there are two main types of policies: level term, where the death benefit and premiums remain constant throughout the term, and decreasing term, where the death benefit decreases over time, often used to cover decreasing debts like mortgages.

Samantha chose a level-term policy because she wanted the face amount of her policy to remain constant so that her family would have what they needed to continue living if she were to pass and her income were to vanish.

Typically, you can renew your policy at the end of the term without having to pass a medical exam, though premiums may increase due to your age at renewal.

Robert renewed his Term Life Insurance Policy, which had lapsed, even when his health had deteriorated. The no-exam renewal aspect played a significant role in his decision, to begin with, and the convenience proved its worth many years later.

Consider your current age, financial responsibilities, and when these financial responsibilities will lighten. For example, you may wish to have a term that lasts until your children are no longer dependent on you or until your mortgage is paid off.

Neil chose a 30-year term that aligned with his mortgage repayment schedule. This strategy ensured that his family would not have to worry about house payments if something happened to him.

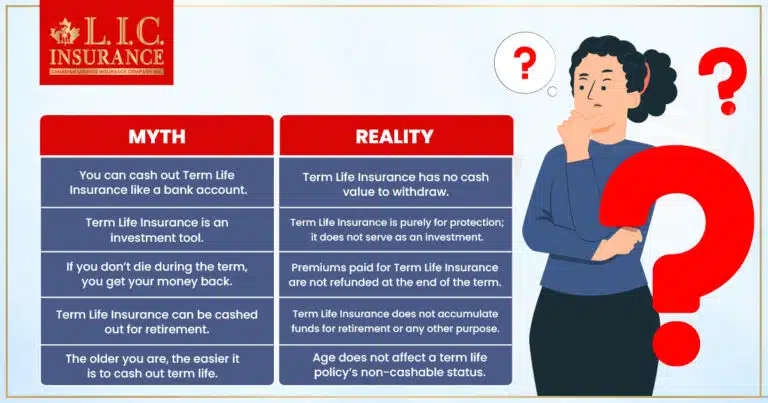

Exclusions in a Term Life Insurance Policy are events or activities that are not covered. Common exclusions include suicide within the first two years, skydiving, or illegal activities. Understanding these can prevent unexpected surprises during the claim process.

Dave, a part-time amateur racer, ensured he was eligible for a Term Life Insurance Policy that did not exclude all racing activities. This meant that his family would be protected even if he was competing in his favourite pastime.

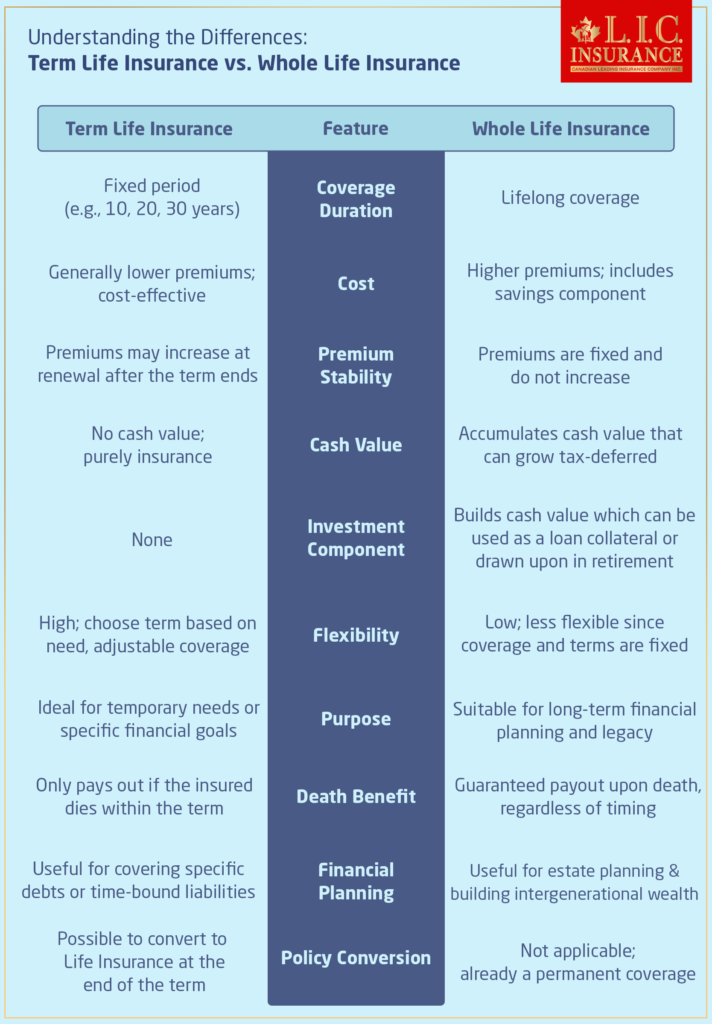

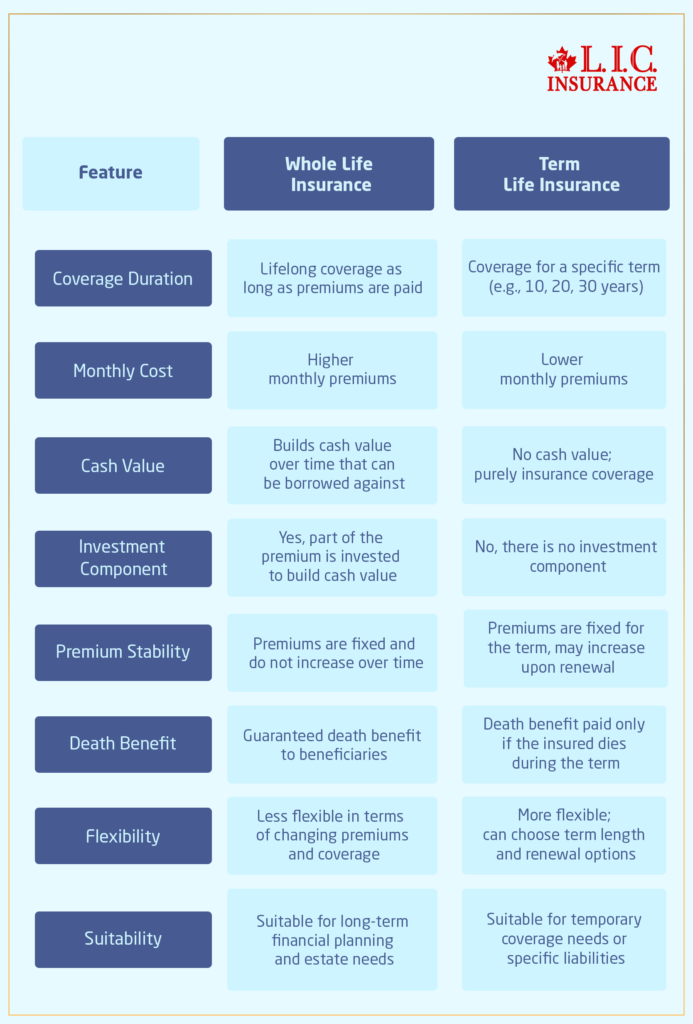

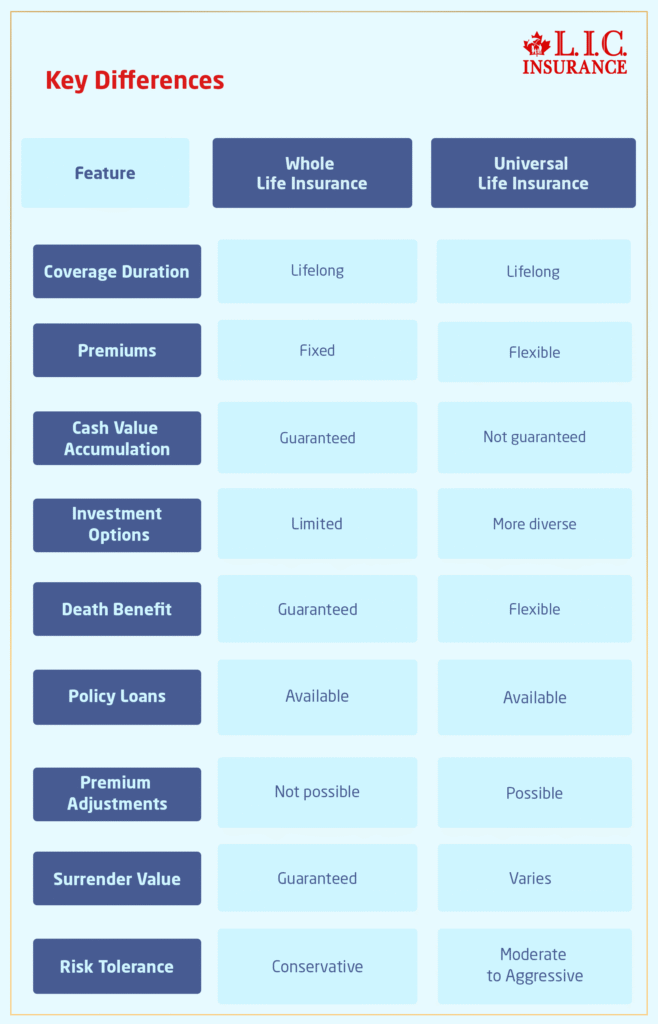

Term Life Insurance provides coverage for a specific period, while Whole Life Insurance, a type of Permanent Life Insurance, offers coverage that lasts your entire life and typically includes a cash value component. Term policies are generally less expensive and simpler, focusing solely on death benefits.Know the difference between Term Life and Whole Life Insurance in detail here.

Anita compared Term Life Insurance Quotes with Whole Life Insurance policies. She chose a term policy because it was more affordable and suited her need for temporary, straightforward coverage while her children were young.

Yes, you can change the beneficiary of your Term Life Insurance Policy at any time, as long as the policy designates the beneficiary as revocable. This flexibility allows you to adjust your policy to match changes in your personal circumstances.

After his divorce, Michael updated his Term Life Insurance Policy to list his children as beneficiaries. This ensured that the benefits would go directly to them without any hassle.

Consider factors like your current income, debts, future obligations (such as college for kids), and the financial needs of your dependents. The coverage should be large enough to provide for your family financially in the event of your death.

Lisa, a single mother and caregiver, chose a coverage amount high enough to replace her income and cover her children’s future college costs, ensuring they would be financially secure in her absence.

You should review your term policy every several years or after a major life event—like marriage, the birth of a child, or a significant change in your financial status. This ensures that you continue to have the right insurance protections.

Jacob reviews his life insurance policy every few years to ensure it aligns with his expanding family. When he had his second child, he increased the coverage to ensure both children could attend university without financial strain.

To lower the cost of your Term Life Insurance, buy a policy at a younger age, opt for a longer term to lock in lower rates, and lead a healthy lifestyle to qualify for better premium rates. Comparing Term Life Insurance Quotes from various providers can also help you find the most affordable option that meets your needs.

At 28, Carla decided to buy a Term Life Insurance Policy after learning that rates were lower for younger, healthier individuals. By securing a 30-year term, she locked in a low rate that would remain constant as she ages, ensuring her premiums are affordable throughout the policy’s duration.

Filing a claim on a Term Life Insurance Policy requires that beneficiaries submit a claim form, a certified copy of the death certificate, and any other documentation that the insurance company requests. You need to call the insurance company as soon as possible to get the claims process started.

When Mark died suddenly, his wife Lina was uncertain what to do with this claim. Fortunately, Mark had everything in one of his neat folders and had told her about the procedure. This preparation helped Lina ensure filings and claims ran smoothly and efficiently during a difficult time.

In the vast majority of situations, the death benefit paid out to beneficiaries as a result of a Canadian Term Life Insurance Policy is tax-free. For a single payment of an annual premium, Term Life Insurance provides financial assistance to close family members as soon as you pass away.

When her husband died, Susan collected the death benefit from his Term Life Insurance Policy. She was relieved to find the amount was tax-free, allowing her to pay off debt, fund college, and cover other financial obligations without additional burdens.

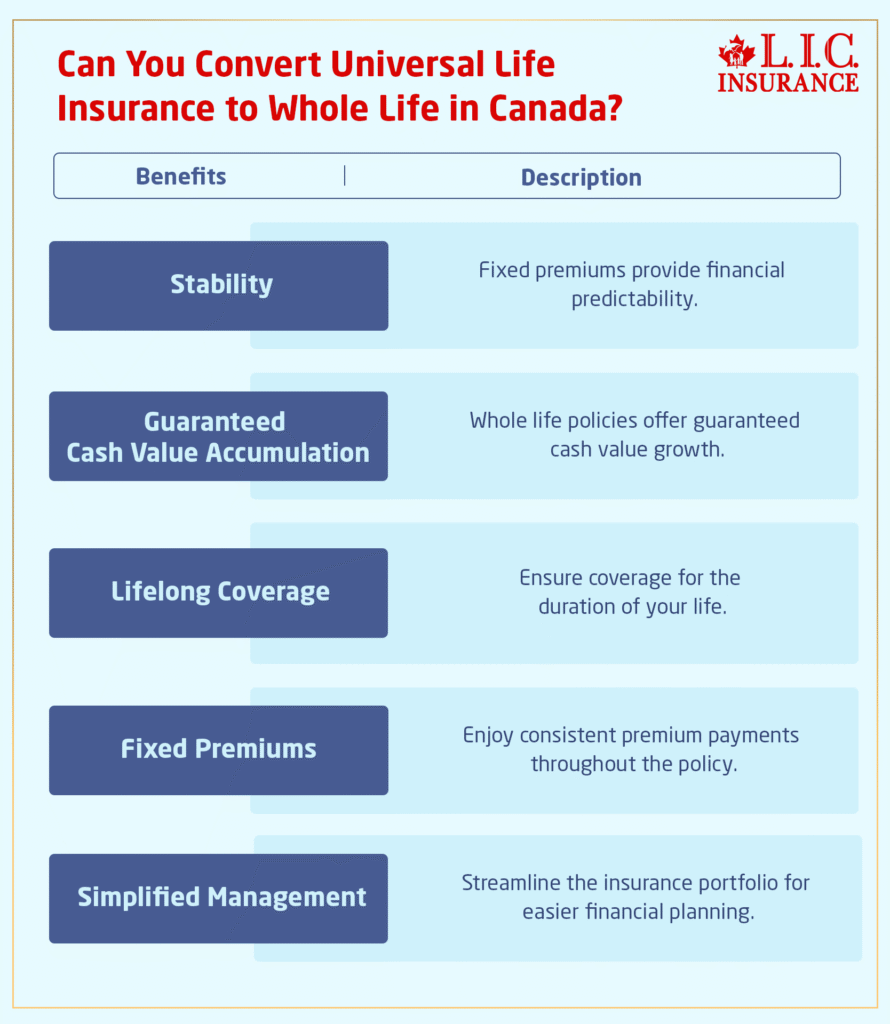

Indeed, many Term Life Insurance Policies in Canada allow you to convert the policy to a Permanent Life or Whole Life Insurance Policy without needing to undergo further medical examinations. This feature is useful if your health has declined, making new insurance expensive or impossible.

Before being diagnosed with cancer near the end of his term, Jim had taken out a term policy because it was cheaper. He converted his life insurance to a permanent policy without a health review, ensuring continued coverage

Indeed, many Term Life Insurance Policies in Canada allow you to convert the policy to a Permanent Life or Whole Life Insurance Policy without needing to undergo further medical examinations. This feature is useful if your health has declined, making new insurance expensive or impossible.

Before being diagnosed with cancer near the end of his term, Jim had taken out a term policy because it was cheaper. He converted his life insurance to a permanent policy without a health review, ensuring continued coverage

If you miss a premium payment, most policies provide a grace period (often 30 days) within which you can pay the premium and the policy will not lapse. It is crucial to make payments within this period to avoid cancellation of your coverage.

Rita, a single mom who is always on the go, once missed the timely payment of her Term Life Insurance premium. She took advantage of the grace period and made the payment without losing her policy’s coverage. Since then, Rita has set up automatic payments to avoid missing future deadlines.

Have these answers helped clarify some of your questions about Term Life Insurance in Canada? You’re not alone if you are still trying to understand Term Life Insurance. Share your thoughts and experiences in the comments, or reach out for a more detailed discussion. Together, let’s ensure you feel confident and informed about protecting your family’s future.

Sources and Further Reading

Sources and Further Reading

To ensure readers have access to reliable information that can expand their understanding of Term Life Insurance in Canada, here are some recommended sources and further reading materials:

Insurance Bureau of Canada (IBC) – Provides comprehensive guides and articles on different types of insurance available in Canada, including Term Life Insurance.

Website: www.ibc.ca

Canadian Life and Health Insurance Association (CLHIA) – Offers detailed information about life insurance policies and consumer protection regulations in Canada. Website: www.clhia.ca

Financial Consumer Agency of Canada (FCAC) – Features useful tips and advice on choosing the right insurance products to meet your needs and how to understand insurance contracts.

Website: www.canada.ca/en/financial-consumer-agency

Investopedia – Term Life Insurance – Provides a deep dive into what Term Life Insurance is, how it works, and the factors you should consider before purchasing a policy.

Link: Term Life Insurance Explained

NerdWallet – How to Choose Between Term and Whole Life Insurance – Offers a comparative analysis of term and Whole Life Insurance, helping readers decide which type of policy might be best suited to their needs.

Key Takeaways

- Term Life Insurance primarily pays out a death benefit if the insured dies within the policy term, with some exclusions.

- Comparing Term Life Insurance Quotes and policies is crucial to finding the right fit for financial needs and lifestyle.

- Knowing policy exclusions is essential to avoid surprises during the claims process.

- Most Term Life Insurance Policies offer options to renew or convert at the end of the term without a medical exam.

- Term Life Insurance is a vital financial planning tool that ensures financial security for families.

- Regular policy reviews are recommended to ensure coverage continues to meet changing life circumstances.

Your Feedback Is Very Important To Us

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com