When saving for your child’s education, have you ever found yourself lost on how to go about it? You’re not alone. This is the problem many of the parents and guardians of this country face: where to start, how much to save, and how not to let loose all their hard-earned money. Out of these challenges, the Registered Education Savings Plan (RESP) comes as a helping hand. Once an RESP starts, the next question that comes is, “How do I go about checking my RESP in Canada?”

In today’s blog, we’ll walk through the exact ways you can check your RESP, confirm your contributions and grants, and track your progress with confidence. That is presented in the form of narratives and personal challenges that resonate with a wide audience, and their resolutions may inspire you to reconsider your strategy regarding education savings. This blog intends to help and motivate you to continue your educational savings journey, regardless of your level of experience. Let’s go step-by-step into the process of checking, managing, and improving your RESP tracking.

Whether you’re wondering how to check RESP balance or need clarity on how to access my RESP, we’ll cover it all. We’ll walk you through how to check RESP contributions, understand RESP status, and even show you how to check RESP contribution room without confusion. If you’re unsure how to check RESP updates with your provider or how to find out how much RESP contribution room is left, this guide is for you. By the end, you’ll know exactly how to manage your RESP account with confidence and accuracy.

Understanding Your RESP

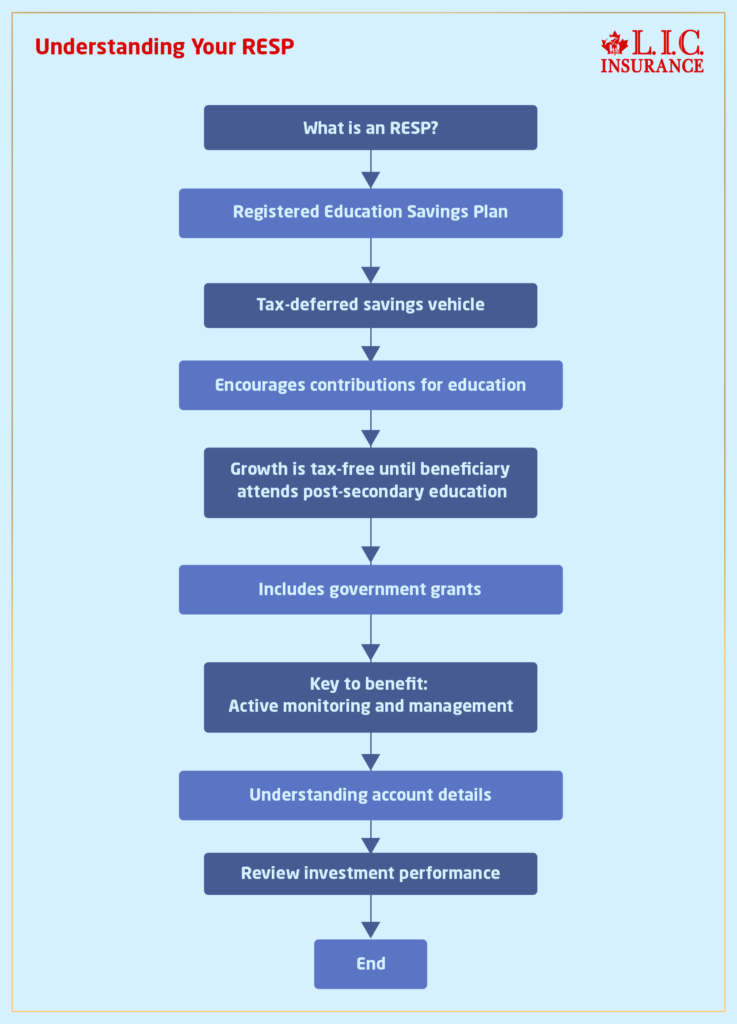

But before we go on to the how-tos, here is a little reminder for you to revise on: What exactly is an RESP? The full form of it is a Registered Education Savings Plan, which, in a nutshell, is a tax-deferred savings vehicle designed by the Canadian government to encourage parents, guardians, and well-wishers to contribute toward a child’s post-secondary education. But the beauty of RESP is that it grows tax-deferred (not tax-free) until the beneficiary is ready for college, university, or any other qualifying educational program besides the top-up grants from the government. Sounds like a plan?

However, like all investments, the key to harnessing the ultimate benefit is very active monitoring and management. This is where most of us get stuck: we don’t understand exactly how to get those account details and review how our investment performed.

Find Out: The Importance of RESP

Checking Your RESP

The world of Registered Education Savings Plans (RESPS) might be intimidating, but staying aware will go a long way toward making certain your Canada education savings are maximized. Here’s how to monitor your RESP account closely so that it continues to contribute to your child’s education.

Contacting Your RESP Provider

Each journey starts with a step, and this is definitely the beginning of the journey to learn and understand the Canadian Education Savings Plan: get in touch with your RESP provider—be it a bank, credit union, or a specialized financial firm that offers only the best Registered Education Savings Plans. This may be in the form of online banking, telephone contact, and face-to-face through some of the established institutions available. This equally calls for the fact that explicit guidance has to be obtained on how to view the account details with respect to the balance, contributions made, and government grants availed to be able to monitor your progress of savings.

Utilizing Online Platforms and Apps

Many RESP providers are now offering online and mobile app account access, responsive to the times of the digital era. Not only are these e-tools meant for inquiring about their balances, but they also provide a detailed view of the contributions made, acquired government grants, and how the investment grows.

Make sure you verify if your provider allows you to access your Canadian Education Savings Plan online if you haven’t already. That’s quite an easy and effective way you can monitor the performance of your RESP at your own convenience.

Understanding Your Statements

Statements come from your RESP provider from time to time, either via email or regular mail, in a bid to provide a snapshot of your account. It includes the amount you have contributed, any withdrawals that have been made, and the value of the investment as a whole. It is quite important that one gets to understand these statements in order to track how he or she is progressing in regard to the education savings plan Canada. They are a very important tool in the sense that with them, one can be guaranteed that they are on the right track to hit the set targets for their child’s education.

A Hidden Strategy to Track RESP Effectively: The “Contribution Room Log” Method

One of the most overlooked—but highly effective—ways to manage your RESP account beyond just looking at your online statement is to maintain what we call a “Contribution Room Log.” Most RESP users wonder how to check RESP balance, how to check RESP contribution room, or even how to access my RESP, but very few actually keep an organized log to track it all manually. Here’s why it matters.

The Canada Revenue Agency (CRA) does not currently provide real-time RESP contribution room updates like it does for RRSPs or TFSAs. That means if you’re wondering how to find out how much RESP contribution room is left, you must rely on your own tracking unless your provider offers real-time integration. That’s where a Contribution Room Log comes in.

Keep a simple spreadsheet (or use a budgeting app) where you manually note every contribution and compare it with your annual and lifetime limits. This lets you answer key questions like how to check RESP contributions over the years and stay well within the $50,000 limit to avoid over-contribution penalties.

Using this proactive log, you’ll also easily monitor RESP status changes during transfers, plan switches, or new beneficiary setups—something even online tools don’t always reflect instantly. It gives you control and clarity without waiting for mailed statements or provider call-backs.

This practical method isn’t offered by RESP providers—but it can help any Canadian looking for a hands-on way to optimize their education savings. So, the next time you’re unsure how to check RESP details or need a deeper understanding of your plan’s progress, your Contribution Room Log could be your most reliable ally.

The Value of Professional Advice

If at any time one is not too sure of the performance of their RESP or how to improve on their contributions, they should seek financial advice. The team of professionals covers all aspects of Canadian education savings plans, so they are the ideal people to provide you with highly personalized consultations based on your financial situation. A financial advisor will be in a position to explain to you any kind of complications in the RESP, which will enable you to make the best decision possible that would suit the goal you have in relation to education savings.

You should communicate with your RESP provider actively, manage accounts with digital tools, learn to read statements, and, finally, seek advice from financial professionals on the proper running and management of your Education Savings Plan for Canada. This is the most effective way to ensure one gets the maximum out of the RESP and, at the same time, everything is going right for a good educational future for your child.

How To Access RESP Funds, Government Matching, And Catch-Up Contributions

Many parents in RESP Canada planning feel confident after setting up their RESP account, but get stuck when they want to understand RESP Canada matching, RESP government contributions, and how withdrawals actually work. The good news is: once you understand the rules, tracking and managing the plan becomes much easier.

When people talk about RESP government match or RESP Canada matching, they usually mean the Canada Education Savings Grant (CESG). This grant is the most common form of RESP government contributions, and it matches 20% of your contributions up to a limit. This is also where the resp matching limit matters most, because the standard CESG match is capped at $500 per year, with a lifetime maximum of $7,200 per child.

RESP Contribution Per Year: What It Means In Real Life

Many parents search for resp contribution per year, but RESP rules can confuse people because there is no strict annual contribution limit. However, what does matter is the grant structure and contribution planning. Even though you can contribute more in a single year, the CESG match is capped annually, so the strategy becomes about optimizing the match rather than only focusing on deposits.

RESP Catch-Up Calculator: Why Parents Search For This

Another keyword that comes up often is resp catch up calculator. Parents look for a catch-up calculator because if you miss contributions in earlier years, you may still be able to earn unused CESG grant room later. In most cases, you can catch up by contributing more than $2,500 in a year to claim additional CESG, but the yearly grant catch-up limit still applies.

If you want to stay organized, you can add a small “catch-up” tab inside your contribution log and treat it like your personal resp catch-up calculator—tracking:

- How much you contributed each year

- How much CESG you received

- How much unused grant room may still be available

How To Access RESP Funds When Your Child Starts School

A very common question is how to access RESP funds when the child is ready for post-secondary education. In Canada, RESP withdrawals generally happen in two ways:

- Refund Of Contributions (ROC): your own deposits

- Educational Assistance Payments (EAP): grants + investment growth

Your provider will usually ask for proof of enrollment, and then guide you through the withdrawal process based on your RESP plan type and your RESP beneficiary details.

How To Report RESP On Tax Return

Parents also search for how to report RESP on tax return, and here’s the key point:

✅ Contributions are not reported as a tax deduction.

✅ Withdrawals from EAP (grants + growth) are usually reported on a tax slip and taxed in the student’s hands, not the subscriber’s.

If you want to avoid confusion later, it helps to download RESP statements yearly so you can track what was contributed, what grants were received, and what was withdrawn.

RESP Quebec Note (For Families Living In Quebec)

If you are searching for RESP Quebec, keep in mind that Quebec families may have additional provincial education incentives depending on eligibility and program availability. It’s best to confirm directly with your RESP provider, because not every institution supports every incentive automatically.

Tips for Optimizing Your RESP

Regular contributions: Develop a habit of saving. With compound interest and government contributions, small chunks will grow into substantial amounts over time.

Maximize Government Grants: Find out the government grants you are qualified to receive, such as the Canada Education Savings Grant (CESG), and decide on the contribution level that will allow you to receive the full grant annually.

Invest wisely: The most appropriate RESP is that which is highly diversified and can accommodate different time horizons and risk tolerances. It is recommended that one invest in line with the set goals through a financial advisor.

Life changes, and so might your financial situation. Review the contributions or investment choices made to your RESP and, as part of the regular review of your plan, make changes in order to continue to stay on track.

Wrapping It All Up

Looking after your RESP is one way of ensuring that your child does get the best education. Monitoring your educational savings plan means far more than simply tucking money away; it is an investment in your child’s dreams and aspirations. This isn’t a race but a marathon to save for the educational journey. By being patient, determined, and proactive, you will be able to win over all the challenges that will come your way in regard to RESPs and you will be able to secure a bright future for your loved ones. So what are you still waiting for? Start reviewing your RESP and make contributions today. If one has not started yet, this is the right time to do so. Your future self and child will surely appreciate the actions you will take right now. Together, let’s make education savings a priority and turn the dream of a college or university degree into a reality.

More on RESP

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

FAQs

Starting an education savings plan in Canada is easier than you think. In order to start one, you have to obtain a Social Insurance Number (SIN) for yourself and your child. Followed by choosing a financial institution or provider, one should choose the best- Registered Education Savings Plan suitable for their needs. They would help in the application, understanding the options available for investment, and finally show how you make good use of the grants given out by the government.

The best Registered Education Savings Plans are flexible, have low fees, and offer many choices in terms of investment. Ensure that the plan you consider subscribing to allows you to change the investment strategies if your goals or the market conditions change in due course. Additionally, since this is a great approach to managing your RESP, a contribution information plan for your investments is beneficial. The best plan for you is that which would be in sync with your financial position and goals for the education of your child.

Of course! Most financial institutions and RESP providers have an online platform where holders can log in and check their education savings plan balance. Such platforms normally have explicit information on your contribution, grants that may be earned from the government, and growth investments. If you’re not sure how to access your account online, contact your RESP provider for guidance.

Government grants, such as the Canada Education Savings Grant (CESG), are among the major benefits of RESPS. For every contribution that is made, the government tops up to a certain percentage and to a maximum amount in a year and the lifetime of a child. Your RESP will automatically be applying for these grants, so do make sure that you have such a setup done. Your RESP provider might help you with that, and you wouldn’t have to miss out on the contribution the government makes toward your child’s education savings.

You can transfer it to another child if the original beneficiary decides not to have a post-secondary education. However, there are some rules: a new beneficiary should also be eligible to receive the funds from the plan. Transfers, however, may affect the grants received, so it would be wise to discuss this with your RESP provider in order to understand clearly the implications.

Suppose, at any point, your child decides not to pursue post-secondary education. In that case, you will have several alternatives: keep the RESP open for any time in the future when the child decides to return to school (up to a maximum period), transfer the money to another eligible child, or close the plan if it no longer fits your situation (but the outcome depends on what type of money you withdraw).

Your original contributions are usually refundable to you tax-free, but government grants like CESG/CLB normally must be repaid if not used for education. Investment growth may be taxable if withdrawn as an AIP (Accumulated Income Payment), unless you qualify to roll it into your RRSP under CRA rules.

You can open an RESP and contribute on behalf of anybody’s child: a grandchild, niece, or nephew, for example. You would need his SIN to ensure the proper setup for receiving government grants on his behalf. This is a perfect way to help secure a child’s future education, showing how the education savings plans offered in Canada are flexible to help family members.

The lifetime limit for contributions under the RESP is $50,000 per child. While there is no annual limit on contributions, government grant contributions are subject to an annual limit. For example, the Canada Education Savings Grant is usually given on a 20% contribution matching of up to $500 in a year and has a lifetime limit per child of $7,200. A 5% additional grant can be added to those who are at a lower income level to help them build up the funds for their child’s education.

Yes, there is a penalty for over-contribution to an RESP. Contributions in excess of the lifetime $50,000 limit will attract a penalty tax of 1% per month until the excess amount is withdrawn. You should track the amounts contributed and, in case of doubt, clarify with your RESP provider to avoid these penalties.

Finding the best RESP provider, in fact, would call for proper consideration and analysis of the kind of institutions. Look out for a reputable provider who has low charges and offers flexibility to invest, yet at the same time, gets its job done brilliantly. You should also be able to deal with a provider who clearly explains how to handle and manage your investments. Please do not shy away from asking for some good recommendations from friends or family who may have had a good experience with their RESP.

Choose the right RESP depending on the needs of your family, considering the amounts that you can afford to contribute, the types of investment, and the flexibility of the plan in terms of changing beneficiaries. Speak to a financial advisor who knows the Registered Education Savings Plan scene very well in Canada. They will advise you according to your financial position and the objectives you hold. The best plan is that which saves according to your saving habits and the future desires of your children’s education.

It is possible to transfer your RESP provider, but you should take into account the fees or penalties that are taken to transfer an account. One needs to compare the benefits and costs of transferring an education savings plan within Canada. If such change is to be considered, do bring it to the notice of current and potential new providers, appraising fully the impact on both aspects.

But if the child takes some other way, then there are plenty of options. After that, you can change the beneficiary to another child, or, under certain conditions, you are allowed to roll your funds into your RRSP. When none of these three options suit you, you can always opt for an RESP closure. One should keep in mind that government grants have to be repaid, and in addition to that, there would be tax implications with respect to the investment income generated within the plan. That makes RESP a flexible education savings plan in Canada.

At a minimum, ensure that you contribute an annual amount of $2,500 towards your child’s RESP in order to get the full Canada Education Savings Grant (CESG) of $500 per year. If you catch up on your contributions, you may contribute more to make up for the unused grant room. Also, check if your child is eligible to receive more grants like the Canada Learning Bond or any provincial incentive that can top up your Canadian Education Savings Plan.

It is possible to open an RESP even when your child is a teenager. It is good to start even earlier so that there is more time to benefit from compound interest and to accumulate the maximum government grants, but an RESP can be established at any time and timed to accrue some of the educational support. Remember that an RESP can be contributed to and receive CESG until the end of the calendar year when the child is 17 years of age. So, take the chance to support your child’s post-secondary education dreams now.

Indeed, an RESP opened by a grandparent for his or her grandchild is also one of the nicest gifts that you can give to a student for his or her education. If you offer the gift of education, it is also an investment in your grandchild’s future. Further to that, you get to enjoy the tax benefits and government grants associated with education savings plans. Ensure you coordinate with the child’s parents to avoid exceeding the lifetime contribution limit.

Online, you may also check the balance and the performance of your RESP by logging into your account through the financial institution or RESP provider website. Most RESP providers allow online access so that account details about the contribution, government grant, and investment growth can be checked. If it is unclear how to access such information, please feel free to contact your provider directly. Staying up-to-date helps you understand the progress your education savings plan in Canada is making towards your goal.

If you’re facing financial challenges, remember that RESPS are flexible. You do not get penalized even if you miss a contribution, say, during a financially hard season. However, there is always the option of catching up, and this can be implemented by increasing one’s contributions to exceed the maximum lifetime contribution limits. This RESP, being a flexible education savings plan, means that temporary challenges of life do not have to impact a child’s educational future.

These FAQS were meant to clarify and help any family that wants answers about education savings in Canada. Of course, one should always seek the advice of a financial advisor and make the most sensible decision for their child’s RESP. Your proactive steps today pave the way for a brighter educational future tomorrow.

Sources and Further Reading

For those interested in deepening their understanding of Registered Education Savings Plans (RESPS) and how to effectively manage them, here is a curated list of resources and further reading. These sources provide valuable insights into making the most of your education savings plan in Canada, including details on government grants, investment strategies, and the nuances of RESP management.

Government of Canada – RESP Information:

- Official website providing comprehensive details on RESP accounts, including how to open an RESP, types of RESPs, and information on government grants like the Canada Education Savings Grant (CESG) and the Canada Learning Bond (CLB).

- Canada.ca - Education Savings

Canadian Scholarship Trust Foundation:

- A foundation that offers resources on planning and saving for post-secondary education, with a focus on RESP. It provides insights into choosing the best Registered Education Savings Plan tailored to your needs.

- CST.org - RESP Guide

Investment Industry Regulatory Organization of Canada (IIROC):

- Offers guides and tools for understanding investment products, including RESPs. Their resources can help you make informed decisions about your investment choices within your RESP.

- IIROC.ca - Understanding RESPs

Financial Consumer Agency of Canada (FCAC):

- Provides educational materials on managing finances and saving for education, including a guide on how to choose an RESP provider and understanding the fees associated.

- Canada.ca - Financial Consumer Agency

MoneySense:

- An online magazine offering practical advice on personal finance and savings, including articles on RESPs, tips for maximizing your education savings, and reviews of RESP providers in Canada.

- MoneySense.ca - RESP Guide

Canadian Securities Administrators (CSA):

- Provides investor education and resources, including information on saving for education through RESPs. Their tools and guides can help you understand the regulatory aspects of RESPs.

- Securities-Administrators.ca - Investors

- Understanding the legal aspects of insurance in Canada, including rights and responsibilities under different plans. This can involve reading through resources from legal advisory services or government health departments.

- Understanding the legal aspects of insurance in Canada, including rights and responsibilities under different plans. This can involve reading through resources from legal advisory services or government health departments.

These sources will equip you with the knowledge needed to navigate the RESP landscape confidently. From government resources to financial education platforms, the information available can help you make informed decisions, ensuring that you are utilizing the best strategies to save for your child’s education. Whether you’re new to RESPs or looking to optimize your current plan, these resources are a great starting point for anyone looking to invest in a child’s future education.

Key Takeaways

- Reach out to your RESP provider for account access and guidance.

- Use online platforms and mobile apps for convenient account management.

- Review your RESP statements regularly to track your savings progress.

- Consult with a financial advisor for tailored advice on your RESP.

- Maximize government grants like the CESG and CLB by understanding their criteria.

- RESPs offer flexibility for contributions and changing beneficiaries.

- Explore options for your RESP if the beneficiary does not pursue post-secondary education.

- Stay informed about RESPs and saving for education in Canada through reputable resources.

Your Feedback Is Very Important To Us

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com