- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Whole Life Insurance Cost In Canada 2026

By Pushpinder Puri

CEO & Founder

- 12 min read

- May 27th, 2026

SUMMARY

Whole Life Insurance cost in Canada 2026 varies based on age, health status, coverage amount, and smoking status. Whole Life Insurance offers permanent Life Insurance Coverage, stable Life Insurance premiums, and growing cash value. Understanding Life Insurance rates, Whole Life Insurance quotes, and Life Insurance products helps compare Term Life Insurance, Universal Life Insurance, and whole life policies to choose the right Life Insurance Policy for financial security and income replacement.

Introduction

Understand The Whole Life Insurance Rates, Cash Value, And Monthly Premiums

One of the most important tools in the overall process of financial planning in Canada is Life Insurance. It has been found that over 22 million Canadians own some type of Life Insurance Policy, with over $5 trillion in total insurance protection, as stated by the Canadian Life and Health Insurance Association (CLHIA). This shows how important Life Insurance is in providing overall security and income replacement for families in Canada.

Among the numerous insurance plans that are offered, the Whole Life Insurance Policy stands out as it provides permanent protection, guaranteed cash value growth, and fixed premiums. But one of the most asked questions by Canadians is:

“How much does Whole Life Insurance cost in Canada in 2026?”

In this guide, we will discuss the cost of Whole Life Insurance in Canada 2026, the cost of Whole Life Insurance, what affects the cost of Life Insurance, and how to compare Whole Life Insurance to find the best policy to meet individual needs.

Whole Life Insurance Cost In Canada 2026

To comprehend the cost of Whole Life Insurance in Canada 2026, one must first understand that the cost of Whole Life Insurance in Canada can differ significantly depending on the individual’s age, health, policy amount, and terms.

Generally speaking, the cost of Whole Life Insurance in Canada can range from $42 to $462 per month for a $100,000 policy. Younger applicants with good health will likely pay lower insurance premiums, while older applicants with health concerns may have to pay higher insurance premiums.

Typical monthly Life Insurance premiums in Canada:

These Whole Life Insurance rates assume:

- $100,000 coverage amount

- Non-smoker

- Good health

- Life pay structure

The cost of Life Insurance for Canadians who are in their 20s and 30s might be around $42 to $75 on average every month, and this makes early enrollment the best way to ensure affordable Life Insurance.

While it is true that the cost of Whole Life Insurance Policies will be more than what Term Life Insurance costs, there are many other benefits that Canadians might want to take into consideration.

What Is Whole Life Insurance

This Whole Life Insurance Policy can be described as follows: A Whole Life Insurance Policy can be described as a Life Insurance Policy that will cover your life for your entire life, provided that you make your premium payments on time.

A Whole Life Insurance Policy can be differentiated from other forms of Life Insurance, like Term Life Insurance, on the basis that, unlike Whole Life Insurance, Term Life Insurance can cover your life for only 10 years, 20 years, 30 years, 50 years, etc., but not your entire life.

Key features include:

- Guaranteed death benefit

- Stable Life Insurance premiums

- Growing cash value account

- Potential dividends for Participating Policies

Most Canadians prefer to have Whole Life Insurance Coverage as it not only provides financial security to their loved ones, but it also has an additional feature of savings, which is tax-advantaged.

As the insurance premiums are paid, they are used to build up a cash value, which increases over time. This cash value is guaranteed and can be accessed by the policyholder in the form of a loan, which can be used by the policyholder in times of need.

Therefore, Whole Life Insurance products are used as they have so many benefits.

Average Life Insurance Cost Per Month In Canada

When discussing Life Insurance cost, it is important to remember that different Life Insurance Plans have different pricing structures.

Typical ranges for Canadians include:

| Policy Type | Average Monthly Cost |

|---|---|

| Term Life Insurance | $20 – $60 |

| Whole Life Insurance | $45 – $100 |

| Universal Life Insurance | $60 – $150 |

Although Term Life Insurance Policy options provide cheaper premium rates, they do not offer cash value or renewal after a certain period.

On the other hand, permanent Life Insurance provides the following benefits:

* lifelong protection

* tax advantages

* guaranteed death benefit

These benefits have made some Canadians opt for Whole Life Insurance, even at higher premium rates.

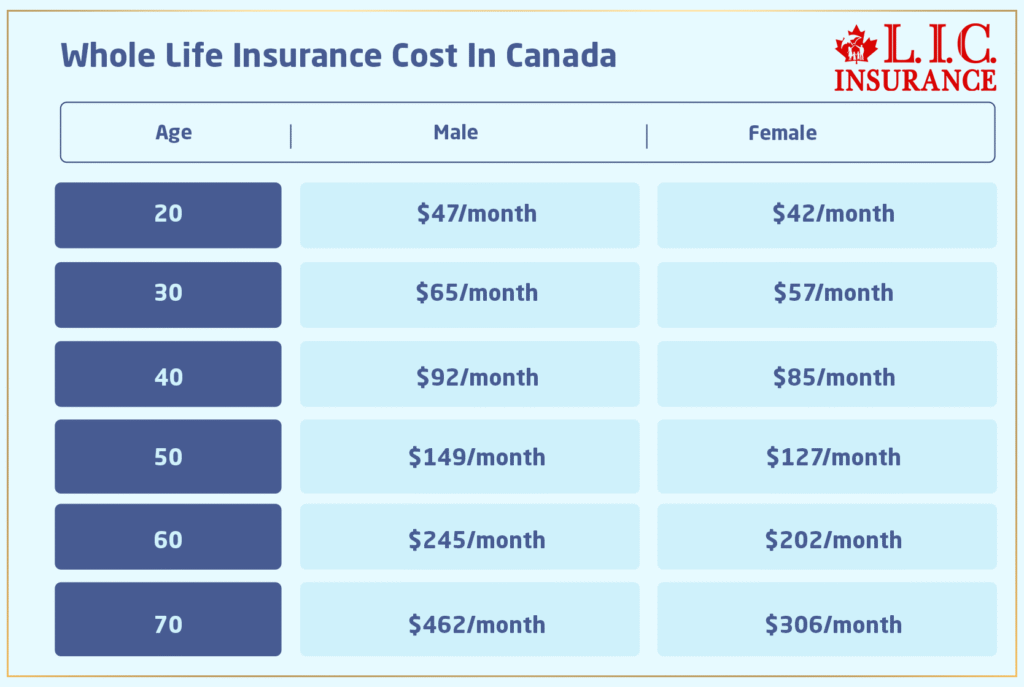

Whole Life Insurance Quotes In Canada

Below is a simplified example of Whole Life Insurance quotes for $100,000 coverage.

| Age | Male (Non-Participating) | Female (Non-Participating) |

|---|---|---|

| 20 | $47 | $42 |

| 30 | $65 | $57 |

| 40 | $92 | $85 |

| 50 | $149 | $127 |

| 60 | $245 | $202 |

These Whole Life Insurance prices may vary depending on:

- smoking status

- medical history

- coverage details

- insurance provider

However, the underwriting standards may differ from one insurance company to another. This is why it is essential to compare Life Insurance quotes.

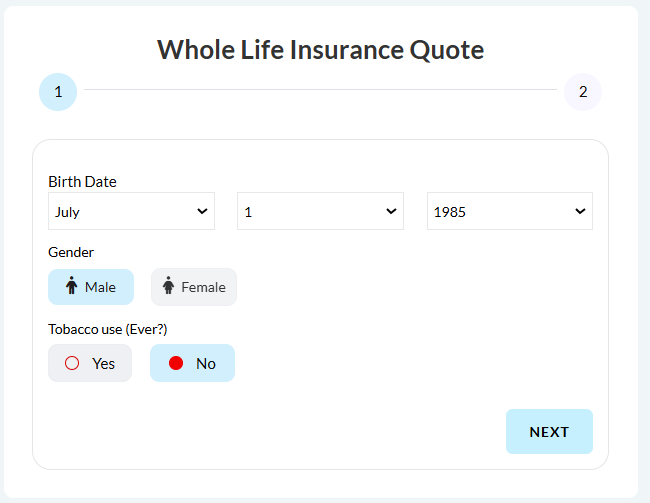

Most Canadians rely on a Whole Life Insurance calculator to determine the amount of Life Insurance they require and the premium they will have to pay every month.

Life Insurance Rates By Age Chart Canada

The most significant factor affecting Life Insurance premiums is our age.

As we age, our life expectancy decreases. This means there are more chances that the insurance company will pay out the death benefit. This explains why the Life Insurance rate by age chart Canada displays increasing costs over time.

Example progression:

| Age | Estimated Monthly Premium |

|---|---|

| 25 | $50 |

| 35 | $70 |

| 45 | $120 |

| 55 | $210 |

| 65 | $350 |

Buying earlier often results in lower premiums for life. Waiting until later years may lead to significantly higher premiums due to health risks or pre-existing conditions.

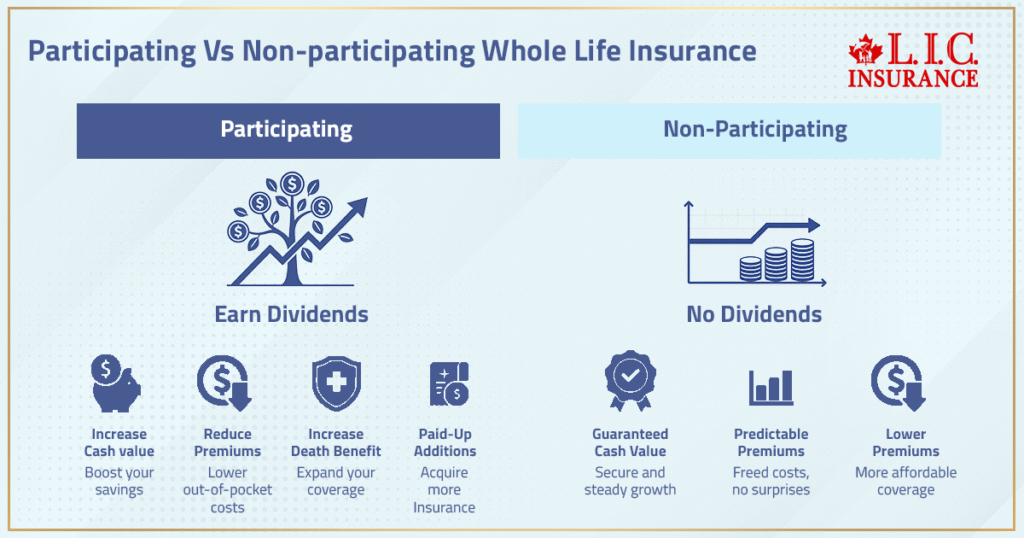

Participating Vs Non Participating Whole Life Insurance Policy

There are two major types of Whole Life Insurance Policy designs.

Participating Whole Life

A Participating Life Policy allows policyholders to receive annual dividends from the Life Insurance company’s investment performance.

These dividends may be used to:

- purchase paid-up additions

- increase cash value

- reduce premiums

- increase the death benefit

Major Canadian insurers offering participating Whole Life Insurance include Sun Life, Canada Life, Industrial Alliance, Equitable, Foresters, Cooperators, etc., among others.

Non-Participating Whole Life

A Non-Participating Whole Life Policy does not pay dividends. Instead, it offers predictable, guaranteed cash value and stable insurance premiums.

Because it lacks dividend potential, it generally has lower premiums compared to participating policies.

Life Pay Vs Limited Pay Whole Life

Another factor affecting Whole Life Insurance premiums is the payment structure.

Life Pay

With life pay, monthly payments continue for the entire lifetime. This option spreads the Life Insurance premium across many years and often results in more affordable monthly payments.

Limited Pay

Limited pay policies allow clients to pay higher premiums for a limited number of years, such as:

- 10 pay

- 20 pay

- pay to age 65

Once the policy becomes paid up, coverage continues for life without additional payments.

Many Canadians prefer limited pay plans because they eliminate insurance premiums during retirement.

Whole Life Insurance Cash Value Explained

One of the most attractive benefits of having a Whole Life Insurance Policy is probably the cash value feature.

Every time money is added to this policy, it grows in cash value, and the money that is built up in this policy has the special advantage of being untaxed.

It can be used as an asset.

Policyholders may access funds through:

- policy loans

- partial withdrawals

- surrendering the policy

The Whole Life Insurance cash value may also support retirement planning, emergency funds, or business financing.

Because the growth is guaranteed in many policies, this creates a stable financial safety net.

Factors Affecting Life Insurance Cost In Canada

There are some key factors that affect the cost of Life Insurance in Canada.

Age

The older you are, the higher the Life Insurance rates. Conversely, the younger you are, the lower the Life Insurance rates.

Health Status

The insurance company will take into account the applicant’s medical history, health, and potential health hazards.

Some Life Insurance Policies require medical tests, while others do not.

Smoking Status

The Life Insurance rates are greatly affected by whether or not you smoke. Smokers pay double the rates of nonsmokers due to mortality risk.

Coverage Amount

The Life Insurance rates will also be affected by the amount of coverage you choose. Therefore, the higher the death benefit, the higher the Life Insurance rates.

Lifestyle And Occupation

Other factors that can affect Life Insurance rates include high-risk jobs, hobbies, and travel habits.

Insurance Provider

Different insurance companies have different guidelines for Life Insurance. This is why it is essential to compare Life Insurance quotes.

Whole Life Vs Term Life Insurance Costs

Many Canadians compare Whole Life Insurance with Term Life Insurance.

Term Life Insurance

A Term Life Insurance Policy provides coverage for a fixed period, typically:

- 10 years

- 20 years

- 30 years

- Up to 50 years (max up to age 85)

Because the policy expires, Term Life Insurance costs are much lower.

Whole Life Insurance

With a Whole Life Policy, there will be permanent coverage, stable premium payments, and growth in cash value.

The Life Insurance premium may be higher, but it will provide security.

For Canadians, when deciding between the options, a Life Insurance options comparison is key.

Life Insurance Policy Comparison: Whole Life Vs Term Vs Universal Life

Canadians seeking an easier way to compare the cost of the most popular Life Insurance Policies have many options. The following table shows some of the major differences between whole life, term life, and Universal Life Insurance, including policy length, cash value accumulation, and premiums.

| Policy Type | Coverage Length | Cash Value | Premium Cost |

|---|---|---|---|

| Term Life Insurance | Fixed term (10–50 years) | No cash value | Lower premiums |

| Whole Life Insurance | Lifetime coverage | Guaranteed cash value growth | Higher premiums |

| Universal Life Insurance | Lifetime coverage | Flexible cash value component | Moderate to higher premiums |

How Much Coverage Do You Need

Determining how much coverage you need depends on several financial factors.

Typical recommendations include coverage equal to 10 to 15 times annual income.

A proper calculation should consider:

- mortgage balance

- education costs

- debt repayment

- income replacement

- long-term family support

Using a Life Insurance calculator can help estimate the right coverage amount for your situation.

Whole Life Insurance For Long-Term Financial Security

Many Canadians purchase Whole Life Insurance Policies not only for protection but also as part of a long-term financial strategy.

Benefits include:

- lifelong coverage

- guaranteed death benefit

- stable premiums

- growing cash value

- tax advantages

Due to the growth in cash value, it can also act as a financial safety net.

The financial security and savings features of Whole Life Insurance products make them highly attractive to families.

Book A Consultation With Canadian LIC

In order to make the right decision in choosing a Life Insurance Policy, one has to plan. Every individual has unique financial objectives, health issues, and insurance requirements.

One can also use the services of a licensed insurance agent in order to compare Life Insurance Plans and make the right decision in choosing the best Life Insurance Plan.

If you are planning to buy Whole Life Insurance in Canada, you can schedule an appointment to:

- Compare Whole Life Insurance quotes

- Analyze your coverage amount

- Explore Term Life Insurance Coverage alternatives

- Design a personalized financial protection strategy

These resources can help you better understand the differences between Term Life Insurance, Universal Life Insurance, and Whole Life Insurance Coverage.

Final Thoughts

The cost of Whole Life Insurance in Canada in 2026 varies greatly depending on the individual’s health, as well as the face value of the insurance policy. Although the cost of Whole Life Insurance is greater than that of Term Insurance, it provides the benefits of Life Insurance as well as the cash value.

Whole Life Insurance can be an important financial tool for you as an individual living in Canada. It provides the individual with the death benefit, fixed premiums, and tax benefits.

Seeking information on the cost of Life Insurance, getting a quote for Life Insurance, and acquiring professional advice will help you make the best decision for the financial well-being of your family.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

The Participating Whole Life Insurance Policy may also provide annual dividends based on the Life Insurance company’s performance. This can result in increasing the cash value of the policy or adding to the policy to provide additional Life Insurance. This can result in increasing the entire value of the Whole Life Insurance Policy without increasing the base Life Insurance premium.

A Whole Life Insurance Policy is often used by Canadians as an integral component of an

overall estate plan, as the proceeds can be used to pay taxes or other final expenses. The proceeds received from a Life Insurance Policy are tax-free, and this can be used to provide for the heirs.

In most Life Insurance Policies, there is a feature that allows policyholders to convert their policies from Term Life Insurance to Permanent Life Insurance. This is done without undergoing any medical tests if done during the eligibility period. It is advisable to convert Life Insurance Policies at an early age in order to ensure lifelong coverage.

Optional riders offer policyholders the ability to add additional benefits to their Life Insurance Policy. These riders include critical illness insurance, disability waiver of premiums, or accidental death benefits. These additional benefits increase insurance premiums but offer greater financial benefits.

Whole Life Insurance pricing in Canada depends on age, health status, smoking status, gender, coverage amount, policy type, and the insurance company’s underwriting rules.

The monthly premium for Permanent Life Coverage is mainly affected by your age at application, medical history, lifestyle risks, coverage amount, and whether the policy includes cash value or optional riders.

Participating Whole Life Policies usually have higher upfront premiums, but dividends may help increase cash value, buy paid-up additions, or offset long-term policy costs.

Sources and Further Reading

Canadian Life Insurance Statistics

Insurance Business Magazine – Record Insurance Benefits Paid To Canadians

https://www.insurancebusinessmag.com/ca/news/breaking-news/life-and-health-insurers-paid-out-record-143-3b-to-canadians-in-2024–report-550700.aspx

What Is Whole Life Insurance

Government of Canada – Life Insurance Guide (Financial Consumer Agency of Canada)

https://www.canada.ca/en/financial-consumer-agency/services/insurance/life.html

Sun Life Canada – Whole Life Insurance Overview

https://www.sunlife.ca/en/insurance/life/permanent-life-insurance/whole/

BMO Insurance – Whole Life Insurance Guide

https://www.bmo.com/en-ca/insurance/life-insurance/permanent/whole-life/

Cash Value Life Insurance

Canada Life – Participating Whole Life Insurance

https://www.canadalife.com/insurance/life-insurance/permanent-life-insurance/participating-whole-life-insurance.html

Foresters Financial – Whole Life Insurance

https://www.foresters.com/en-ca/life-insurance/whole-life

Whole Life Vs Universal Life Insurance

RBC Insurance – Whole Life Vs Universal Life Insurance

https://www.rbcinsurance.com/en-ca/advice-learning/life-insurance/whole-life-vs-universal-life-insurance/

Canada Life – Types Of Life Insurance Policies

https://www.canadalife.com/insurance/life-insurance.html

Determining Life Insurance Coverage Needs

One Day Insurance – How Much Life Insurance Do You Need

https://onedayinsurance.ca/life-insurance/alberta/

Alberta Blue Cross – Personal Life Insurance Coverage

https://www.ab.bluecross.ca/plans/personal/life-insurance/personal-life-insurance.php

Additional Educational Resources

Edward Jones Canada – Whole Life Insurance Guide

https://www.edwardjones.ca/ca-en/investment-services/insurance/whole-life-insurance

SecurePlan – Whole Life Insurance In Canada

https://secureplan.ca/the-rise-of-whole-life-insurance-in-canada/

Wikipedia – Whole Life Insurance Overview

https://en.wikipedia.org/wiki/Whole_life_insurance

Key Takeaways

- Whole Life Insurance Cost In Canada 2026 typically ranges from $42 to $462 per month for a $100,000 Whole Life Insurance Policy, depending on age, health status, smoking status, and coverage amount.

- Whole Life Insurance premiums are generally higher than Term Life Insurance costs because the policy provides Permanent Life Insurance Coverage, a guaranteed death benefit, and a growing cash value account.

- Younger applicants in good health often qualify for lower premiums, while older applicants or those with health risks or pre-existing conditions may face higher Life Insurance rates.

- A Whole Life Insurance Policy builds guaranteed cash value over time, allowing policyholders to access funds or borrow money through a policy loan if needed.

- Canadians can choose between participating Whole Life Insurance with dividends or non-participating whole life coverage with guaranteed cash value and stable insurance premiums.

- Payment structures such as life pay or limited pay policies affect monthly premiums and long-Term Life Insurance costs.

- Comparing Life Insurance quotes, using a Life Insurance calculator, and reviewing different Life Insurance products help determine how much coverage is needed.

- Whole Life Insurance offers lifelong coverage, financial protection, and a financial safety net, making it a long-term option for income replacement and family financial security.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- Understand The Whole Life Insurance Rates, Cash Value, And Monthly Premiums

- Whole Life Insurance Cost In Canada 2026

- What Is Whole Life Insurance

- Average Life Insurance Cost Per Month In Canada

- Life Insurance Rates By Age Chart Canada

- Participating Vs Non Participating Whole Life Insurance Policy

- Life Pay Vs Limited Pay Whole Life

- Whole Life Insurance Cash Value Explained

- Factors Affecting Life Insurance Cost In Canada

- Whole Life Vs Term Life Insurance Costs

- Life Insurance Policy Comparison: Whole Life Vs Term Vs Universal Life

- How Much Coverage Do You Need

- Whole Life Insurance For Long-Term Financial Security

- Book A Consultation With Canadian LIC

- Final Thoughts

Sign-in to CanadianLIC

Verify OTP