- Can I Have Two Critical Illness Policies?

- Lets First Know About Critical Illness Insurance

- Critical Illness Insurance Cost & Coverage

- Can You Have Two Critical Illness Policies?

- The Overlooked Advantage: Combining Individual and Group Critical Illness Insurance

- Selecting the Right Critical Illness Coverage

- Application Process: Steps to Take

- Dealing with Claims and Beyond

- Final Thoughts

What if you have two different routes in front of you? One is smooth, well-lit, and dependable, while the other is uneven, unclear, and hard to predict. This situation is a lot like real life, especially when it comes to our health. It was easy for John and Emily for years, just like it was for many other Canadians. They carefully saved money, made plans for the future, and put money into their health. When John was told he had a serious illness, though, everything took a surprising turn and became more difficult.

During this time of confusion, an important but often overlooked question came to light: is one Critical Illness Insurance policy enough to cover the financial issues that come up during a serious sickness? We will find the answer to this question as we look into the idea of Critical Illness Insurance, a way to save money that can help you in times of trouble.

Critical Illness Insurance policies help by giving a lump sum payment when certain illnesses are diagnosed. This money can help with many things, like medical care that isn’t covered by provincial health plans and daily living expenses during recovery. But John and Emily learned that one policy might not cover as much as one would hope, especially when thinking about how a critical illness will affect someone for a long time.

John and Emily’s story is not the only one like this. After getting a bad health report, a lot of Canadians reevaluate their financial situation and wonder if their coverage is enough. When you look at it this way, having more than one Critical Illness Insurance policy isn’t just an option; it might be necessary to make sure you have full protection.

We want to give you the information you need to make smart choices about your health and finances by going into more detail about Critical Illness Insurance. This includes the costs, the types of coverage, and the pros and cons of having more than one policy. Understanding Critical Illness Insurance policies might seem like a difficult process, but if you know what you’re doing and plan ahead, you can go through it with confidence, knowing that you and your family are safe no matter what.

The purpose of this blog is to explain the different types of Critical Illness Insurance and make it easier to choose the right policy. You will be able to answer the question, “Should I buy not one but two Critical Illness Insurance policies in Canada?” by the end.

Lets First Know About Critical Illness Insurance

If you get sick with a major illness that could change your life, Critical Illness Insurance will help pay for your medical bills and other costs. These kinds of insurance are made to cover a wide range of people in Canada. They offer a lump-sum payment that can help a lot with the financial stress that comes with critical illnesses.

What Constitutes a Critical Illness?

‘Critical Illness’ covers a predetermined list of conditions considered severe enough to impact your life significantly. Commonly covered conditions include, but are not limited to, heart attacks, strokes, certain types of cancer, and major organ transplants. Each insurance provider has its list of covered conditions, making it essential to look into these details when considering a policy.

Find Out: What is Critical Illness Insurance in detail

The Role of Provincial Healthcare

Although the Canadian healthcare system is praised for its extensive coverage, its main objective is to meet the requirements of people with basic medical conditions. When it comes to critical illnesses, there are gaps in coverage that can leave individuals facing hefty out-of-pocket expenses. For example, while a hospital stay might be covered, the costs associated with new or experimental treatments, at-home care, or modifications to your living space for accessibility purposes might not be. This is where Critical Illness Insurance steps in to fill those gaps, providing financial resources that can be used flexibly according to your needs.

The Mechanics of Critical Illness Insurance

When you invest in a critical illness plan, you’re purchasing a promise: if you are diagnosed with one of the covered conditions, you will receive a one-time, lump-sum payment. This amount is determined at the outset of your policy and can range significantly depending on the level of coverage you choose.

The process typically involves:

- Application and Assessment: You’ll describe your health, lifestyle, and medical history. Some insurers might require a medical exam or access to your medical records.

- Waiting Period: Many policies include a waiting period, usually about 90 days from the start of your policy, during which a critical illness diagnosis will not result in a payout.

- Claim Process: Should you be diagnosed with a covered illness, you'll submit a claim along with the necessary medical documentation. Once approved, the insurer issues your lump-sum payment.

- Use of Funds: Unlike health insurance, which pays directly for medical services, Critical Illness Insurance provides you with a sum of money to use as you see fit. This could be for medical treatments not covered by your provincial plan, daily expenses, or even a recuperative holiday.

Critical Illness Insurance Cost & Coverage

The cost of critical illness plans can vary widely based on several factors:

- Age and Health: Younger, healthier individuals typically face lower premiums, as they're less likely to make a claim. As you age or if you have pre-existing health issues, premiums increase.

- Coverage Amount: Higher coverage amounts lead to higher premiums. Deciding on the right amount involves balancing the potential financial impact of a critical illness with the insurance cost.

- Policy Type: Rates can also differ based on whether you opt for a term policy, which covers you for a specific period, or a permanent policy, which lasts a lifetime.

Selecting the right Critical Illness Insurance policy requires carefully examining your personal and financial situation, considering the potential costs associated with a critical illness and the existing coverage you may have through other insurance plans or your employment.

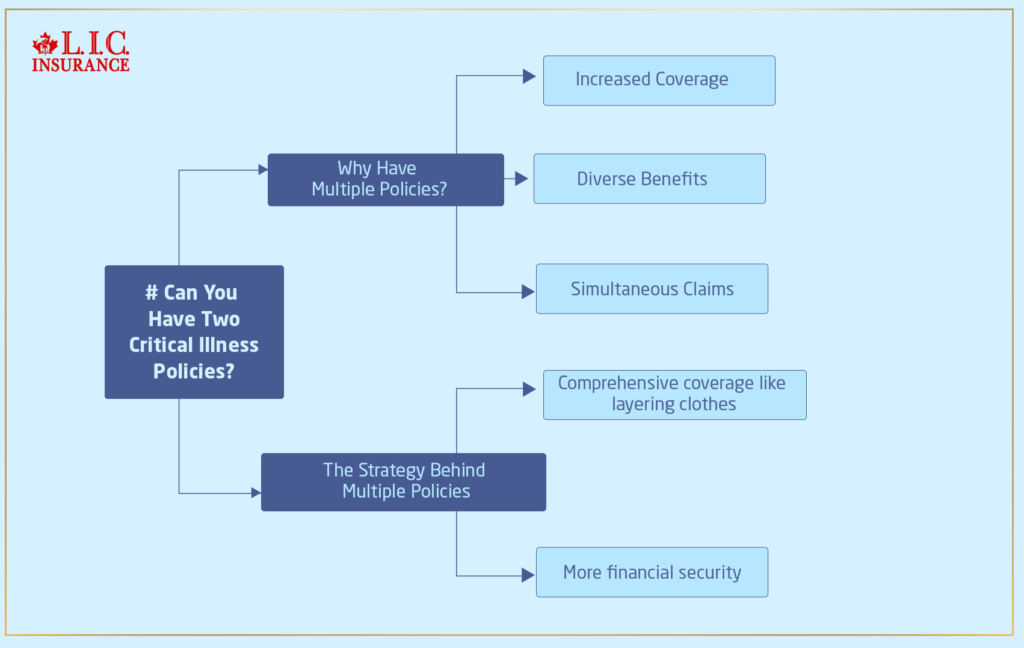

Can You Have Two Critical Illness Policies?

Sometimes, dealing with the unknowns in life can be as challenging as walking on a tightrope. This is especially true when it comes to preparing for the possibility of a critical illness, which is a problem that doesn’t always have a single answer for everyone. Having more than one Critical Illness Insurance policy is a way for many Canadians to improve their financial security. But what does this mean for you, and how will it help you?

The Strategy Behind Multiple Policies

The concept of holding more than one Critical Illness Insurance policy is rooted in a desire for comprehensive coverage. Just as one might layer clothing to prepare for variable weather, layering insurance coverage can provide solid financial health protection. Here’s why:

- Increased Coverage: With multiple policies, the total potential payout in the event of a critical illness increases, offering a larger financial cushion.

- Diverse Benefits: Different policies may have varied terms and cover different illnesses or provide unique benefits, such as the return of premium options.

- Simultaneous Claims: If you get sick and both policies cover your sickness, you can get money from both, which will help your finances even more.

The Practicality of Dual Coverage

Consider the case of Alex, a software developer with a family history of heart disease. Understanding his high risk, Alex opted for two critical illness policies from different insurers, each with distinct coverage benefits—one focused on heart-related conditions and another offering a broader range of illness coverage. When Alex suffered a heart attack, the combined payouts from both policies allowed him to cover his medical expenses and take the necessary time off work to recover without financial strain.

Weighing the Benefits Against the Drawbacks

While the advantages of multiple critical illness policies are clear, it’s important to understand this path with eyes wide open to potential challenges:

- Cost Considerations: Holding multiple policies means paying multiple premiums, which can significantly increase your overall insurance costs. Balancing the desire for comprehensive coverage with the reality of your budget is essential.

- Policy Management: More policies equate to more paperwork and potentially more complexity in managing your insurance portfolio. Staying organized and keeping detailed records become very important.

- Underwriting Hurdles: Applying for several policies means undergoing medical examinations or assessments for each, which can be time-consuming and stressful for some.

Things to Consider Before Doubling Up

- Overlap in Coverage: Carefully review the terms and covered conditions of each policy to minimize excessive overlap, ensuring you’re broadening your safety net without unnecessary redundancy.

- Affordability: Weigh the cost of additional premiums against the potential financial impact of a critical illness. It’s essential to strike a balance that doesn’t overextend your financial resources.

- Full Disclosure: When applying for multiple policies, transparency with each insurer about your existing coverage is necessary. Failure to disclose other policies could complicate the claims process.

The Overlooked Advantage: Combining Individual and Group Critical Illness Insurance

While many Canadians ask, “Can I have 2 critical illness policies?” or “Can you have more than one critical illness policy?”, few explore the strategic value of combining individual and group critical illness insurance plans. This combination is not only allowed—it’s often a smart move that can fill financial protection gaps most people don’t even realize exist.

Group critical illness insurance is typically offered through an employer or professional association. It’s affordable, easy to enroll in, and often doesn’t require medical underwriting. But it can also be limited in scope and coverage amount. That’s where an individual policy becomes essential. It allows you to customize coverage to match your personal risk profile, health history, and long-term financial goals.

When used together, multiple critical illness insurance policies—such as one group and one individual—can increase your total payout if you’re diagnosed with a covered condition. This layered approach gives you the flexibility to handle medical costs, lifestyle changes, or extended recovery without compromising your financial stability.

So, to answer the common question—“Can I have multiple critical illness policies?” or “Can you have 2 critical illness policies?”—yes, and in fact, integrating both types may be the key to building a more resilient safety net.

Selecting the Right Critical Illness Insurance Coverage

When you start looking for not just one but possibly several Critical Illness Insurance plans, you need to be very careful to choose the right coverage. This step is very important because the decisions you make now will greatly affect how well you can handle money when your health goes bad.

Assessing Your Needs and Risks

Begin by conducting a thorough assessment of your personal health risks and financial situation. Consider factors like family medical history, current health status, lifestyle, and your financial ability to cover medical and living expenses in the event of a critical illness. Understanding your unique risks and needs helps tailor your insurance coverage to provide the most effective protection.

Comparing Policies and Providers

No two Critical Illness Insurance Plans are identical, and the same goes for insurance providers. When evaluating options, pay close attention to:

- Covered Conditions: Ensure the policy covers a broad range of illnesses, including any you might be particularly at risk for.

- Exclusions and Limitations: Understand what’s not covered by the policy. Certain pre-existing conditions might be excluded, or there might be limitations on how the payout can be used.

- Premiums: Compare the cost of premiums between policies, but also consider the factors that might influence these costs, such as your age, health, and the policy term length.

- Policy Terms: Look at the fine print regarding policy renewability, term lengths, and whether premiums might increase over time.

Utilizing Tools and Resources

Many insurers and independent financial websites offer tools and resources, such as online calculators or comparison charts, that can help you visualize the differences between policies. These tools can help you understand the selection process and make the right choice.

Seeking Professional Advice

While personal research is invaluable, consulting with an insurance specialist can provide personalized insights. These professionals can assess your specific situation, suggest suitable coverage options, and help you go through the application process.

Application Process: Steps to Take

Once you’ve identified the Critical Illness Insurance policies that best meet your needs, the next step is the application process. This typically involves:

- Completing an Application: Provide accurate information about your health, lifestyle, and financial situation.

- Undergoing Medical Underwriting: Some policies require a medical exam or access to your medical records to assess your risk.

- Review and Approval: The insurer will review your application and, if approved, will offer you a policy with specific terms and premiums.

- Policy Issuance: Upon acceptance of the offer, your policy will be issued, and coverage will begin according to the policy’s effective date.

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Dealing with Claims and Beyond

Understanding how to deal with the claims process if you ever need to use your Critical Illness Insurance is just as important as selecting the right policy. Familiarize yourself with the required documentation and the steps involved in filing a claim to ensure a smooth process when you need support the most.

Final Thoughts

Before you buy Critical Illness Insurance, whether it’s one coverage or several, you should carefully consider your health risks, your financial goals, and the specifics of each insurance plan. You can build a solid financial protection system that gives you and your family peace of mind and security by carefully evaluating your needs, comparing policies, and getting professional help. Remember, being well-prepared is your most vital asset in the face of life’s uncertainties.

FAQs on Critical Illness Insurance in Canada

A Critical Illness Policy is a type of insurance policy that provides a lump-sum payment if you are diagnosed with one of the illnesses specified in the policy. This payment can help cover medical expenses, living costs, and other financial obligations during your recovery period.

Having more than one critical illness policy can increase your coverage amount and ensure broader protection against various illnesses. It also allows you to benefit from different policy features and potentially claim from multiple policies if you’re diagnosed with a covered condition.

Critical Illness Policy provides a one-time, lump-sum payment following the diagnosis of a covered illness, regardless of your actual medical expenses. In contrast, health insurance typically covers specific medical costs as they occur, up to the policy’s coverage limits.

Several factors can influence the cost of Critical Illness Insurance, including your age, health status, the amount of coverage you choose, and the specific illnesses covered by the policy

Yes, but it may affect your coverage options. Some insurers might exclude your pre-existing condition from coverage, increase your premium, or offer a policy with specific limitations related to your condition.

Consider your personal and financial situation, including any existing health risks, your financial obligations, and what you want the policy to cover. Comparing policies from different insurers and consulting with an insurance broker can help you find a policy that meets your needs.

Contact your insurance provider as soon as possible to start the claims process. You’ll likely need to provide medical documentation confirming your diagnosis and complete any required claim forms.

In Canada, the lump-sum payout from a critical illness policy is generally not taxable. This means you can use the full amount of the payout as you see fit without worrying about tax implications.

Yes, you can cancel your policy at any time. However, be aware that you may not receive a refund of your premiums, especially if you have a Term Policy. Review your policy’s terms or consult with your insurer for specific details regarding cancellation.

It’s a good idea to review your Critical Illness Insurance coverage annually or after significant life changes, such as getting married, having a child, or experiencing a change in your health status. This ensures your coverage continues to meet your needs over time.

Critical Illness Insurance offers financial protection if you’re diagnosed with a specified critical illness, such as cancer, heart attack, or stroke. It provides a one-time, lump-sum payment you can use at your discretion—whether for medical treatment, to cover living expenses, or even to take a recuperative vacation. Key points to understand include the range of illnesses covered, the importance of disclosing your medical history accurately during the application process, and the tax-free nature of the benefit payment.

The ideal time to apply for a Critical Illness Insurance plan is when you are relatively healthy and young, as premiums tend to increase with age and the onset of health issues. Applying early not only secures lower premiums but also ensures financial protection is in place before a potential diagnosis. Remember, certain conditions may have waiting periods, so securing coverage sooner rather than later is advisable.

Critical Illness Insurance Coverage can end for several reasons: reaching the policy’s age limit (often 65 or 70 years old), upon payment of a claim, if the policy is canceled, or if premiums are not paid and the policy lapses. Some plans offer the option to convert to a different type of coverage as you approach the policy’s age limit. Check your policy’s terms for specific details.

Before filing a Critical Illness claim, gather all necessary documentation, including your medical diagnosis, treatment records, and any other information required by your insurance provider. Review your policy to understand the specific conditions and the process for filing a claim. It’s also beneficial to contact your insurance provider or broker to discuss the next steps and ensure you have all the information needed for a smooth claims process.

Critical Illness Insurance provides a lump-sum payment if you’re diagnosed with one of the specified critical illnesses, regardless of your ability to work. In contrast, Long-term Disability Benefits offer a regular income replacement if a medical condition prevents you from working for an extended period. The key difference lies in the payment structure and the qualifying criteria; critical illness coverage is based on the diagnosis of specific conditions, while disability benefits depend on your ability to work.

A Critical Illness claim may be denied for several reasons, including the illness not being covered under your policy, a pre-existing condition exclusion, incomplete or inaccurate information provided during the application process, or failure to meet the policy’s definition of the critical illness. If your claim is denied, review the insurer’s reasons carefully, consult your policy’s terms, and consider seeking legal advice or contacting the insurance experts for further assistance.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com