- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Loan Protection Insurance in Canada: Costs & Benefits

By Harpreet Puri

CEO & Founder

- 10 min read

- June 19, 2026

SUMMARY

Loan Protection Insurance Canada helps cover loan payments during disability, job loss, or critical illness. It offers short-term financial protection but comes with costs and limitations. Understanding insurance premiums, coverage structure, and alternatives like Life Insurance for loans in Canada is essential to decide if Loan Protection Insurance is worth it in Canada.

Introduction

Financial pressure builds quietly—until one missed payment puts everything at risk. Across Canada, rising household debt has made even stable incomes vulnerable. According to the Canadian Life and Health Insurance Association and Statistics Canada, Canadian households continue to have significant debt levels in comparison to income. This highlights the need for insurance protection solutions like Loan Protection Insurance Canada.

In the face of unexpected events like disability, unemployment, or critical illness, making ends meet to meet loan repayments becomes the priority at hand. This is where Loan Protection Insurance comes in to provide a safety net to ensure financial security.

Loan Protection Insurance In Canada: Costs, Benefits, And Is It Worth It?

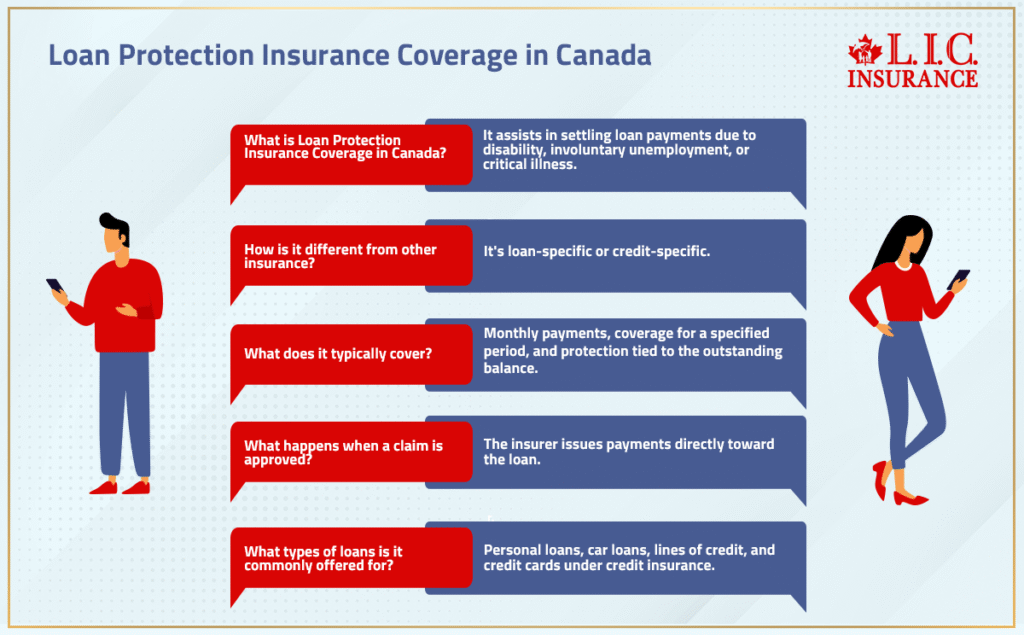

Understanding Loan Protection Insurance Coverage In Canada

Loan Protection Insurance Canada is meant to assist in the settlement of loan payments in the event that the borrower is unable to meet the loan obligations due to some risk, such as disability, involuntary unemployment, or critical illness. This insurance is different from other forms of insurance in the sense that it is loan-specific or credit-specific.

A typical Loan Protection Insurance Coverage includes:

- Monthly payments toward your loan balance

- Coverage for a specified period (often 12–24 months)

- Protection tied to the outstanding balance or the outstanding loan balance

When a claim is approved, the insurer issues payments directly toward the loan, helping maintain good standing and avoiding missed payments.

This type of protection insurance is commonly offered for:

- Personal loan

- Car loan or auto loan

- Line of credit

- Credit cards under Credit Insurance

How Loan Protection Insurance Works With Personal Loan, Car Loan, And Line Of Credit

The Loan Protection Plan in Canada is said to work in a different way.

In the case of a personal loan, it is said that a specific amount is paid towards loan repayment until the limits are met.

For a car loan or auto loan, the insurance may cover:

- Monthly installments

- Remaining balance in extreme cases (death benefit)

For a line of credit, benefits are often calculated using:

- Average daily balance

- Percentage of outstanding balance

Because each loan or line structure differs, the insurance certificate clearly outlines how payments are calculated.

Disability Insurance And Involuntary Unemployment Coverage Explained

A major component of Loan Protection Insurance is Disability Insurance and involuntary unemployment coverage.

If disability prevents you from performing regular duties, disability benefits can:

- Cover loan payments after a waiting period (typically 30–90 days)

- Continue until recovery or maximum benefit duration

In cases of involuntary unemployment or job loss:

- Coverage may activate if you involuntarily lose employment

- Payments continue for a defined period (often up to 12 months)

However, not all employment types qualify. For example:

- Seasonal employee roles may have limitations

- Self-employed individuals may face stricter eligibility

This makes understanding insurance application requirements critical.

Critical Illness And Life Coverage Under Loan Protection Insurance

Many policies include Critical Illness Insurance and Life Coverage components.

If diagnosed with a covered critical illness, such as:

- Heart attack

- Cancer

- Stroke

The policy may:

- Pay a lump sum toward the loan balance

- Or cover ongoing payments

In the event of death, Life Insurance pays the outstanding balance, ensuring the co-borrower or family is not burdened.

This form of Life Coverage differs from Traditional Life Insurance Policies because:

- It is tied to a specific insured loan

- It reduces as the loan balance decreases

Credit Insurance Vs Loan Protection Insurance: Key Differences

Loan Protection Insurance is often confused with Credit Insurance or Credit Life Insurance.

Key differences include:

| Coverage Type | Loan-specific | Credit-based |

| Payment Method | Monthly payments | Balance coverage |

| Flexibility | Higher | Limited |

| Cost Structure | Based on the loan | Based on the credit limit |

Credit Insurance often calculates benefits based on average daily balance, while Loan Protection Insurance focuses on structured loan payments.

Cost Of Loan Protection Insurance In Canada

The cost of Loan Protection Insurance Canada varies based on:

- Loan amount

- Age

- Employment status

- Health questionnaire or medical exam

Typical Personal Loan Protection Insurance cost ranges:

- $1.50–$3.50 per $100 of loan balance monthly

For example:

- $20,000 loan → $30–$70/month in insurance premiums

However, when bundled through lenders, premiums may be added to the loan, increasing total payments significantly.

Insurance Premiums Breakdown Based On Loan Type

Different loan types affect insurance premiums:

Personal Loan

- Fixed premiums

- Predictable payments

Line Of Credit

- Premiums based on outstanding balance

- Fluctuating payments

Auto Loan

- Lower premiums

- Limited duration

Premium structures also depend on:

- Coverage type (Life, Disability, Critical Illness)

- Policy duration

- Risk factors

Benefits Of Loan Insurance Canada: When It Actually Makes Sense

The benefits of Loan Insurance in Canada become clear in specific situations:

- Provides a safety net during unexpected events

- Protects credit score by maintaining payments

- Reduces financial stress during serious illness or job loss

- Ensures loan payments continue without disruption

It is especially useful for:

- Individuals with limited emergency savings

- High debt obligations

- Dependence on a single income

Is Loan Protection Insurance Worth It In Canada?

The answer depends on your financial situation.

Worth It If:

- You have high loan exposure

- Limited savings

- No existing Disability Insurance or Critical Illness Coverage

Not Always Worth It If:

- You already have strong Life Insurance and Disability Coverage

- Your employer offers benefits

- You can self-insure through savings

While Loan Protection Insurance offers convenience, it is often less flexible than standalone insurance policy options.

Loan Protection Insurance Vs Life Insurance For Loans Canada

Comparing Loan Protection Insurance vs Life Insurance for loans in Canada:

| Flexibility | Low | High |

|---|---|---|

| Coverage Use | Loan only | Any purpose |

| Cost | Higher long-term | More efficient |

| Payout | Goes to the lender | Goes to the beneficiary |

Many advisors recommend combining Life Insurance with financial planning rather than relying solely on loan protection.

Loan Protection Insurance Claims: Process And Limitations

Filing a Loan Protection Insurance claim requires:

- Claim forms submission

- Proof of disability, job loss, or covered illness

- Supporting documents

Important factors:

- Waiting period applies

- Pre-existing conditions may be excluded

- Claims may be denied if conditions are not met

Understanding full details before applying is essential.

Legal Disclaimers And Hidden Terms You Must Know

Every insurance policy includes legal disclaimers that impact coverage:

- Exclusions for pre-existing conditions

- Limited coverage for certain employment types

- Defined waiting periods

- Conditions to cancel coverage

Always review the insurance certificate carefully before signing.

Final Decision Framework: Should You Buy Loan Protection Insurance In Canada?

Loan Protection Insurance Canada provides targeted insurance protection—but it is not always the most cost-effective solution.

Before buying, evaluate:

- Existing insurance coverage

- Financial goals

- Risk tolerance

- Alternative options like Life Insurance

For many Canadians, the decision comes down to balancing convenience vs long-term value.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Loan Protection Insurance in Canada is usually specific to the loan in question or the line of credit. Therefore, it cannot be ported to another loan. In cases where refinancing occurs, it is usually required to make a new application for the insurance. This could affect the premium as well as the qualification for the insurance if the individual’s health status has deteriorated. Care should be taken when reviewing the insurance certificate.

The Loan Protection Insurance Coverage in Canada might only cover a portion of the loan payments rather than the full amount. The amount received might be based on the outstanding balance, the average daily balance, or the coverage amount. In this case, the individual making the loan might still have to make contributions towards the payments during the claim period. Therefore, it is essential to read the coverage agreement to avoid surprises in unexpected situations.

In cases where there are co-borrowers, the Loan Protection Insurance may provide cover for both parties through a Group Policy. However, the claims are made based on the individual experiencing disability, critical illness, or involuntary unemployment. The outstanding loan balance may be apportioned to both parties, making it important to understand how the benefits are applied to each party to ensure the insurance covers them adequately.

The majority of Loan Protection Insurance Plans in Canada provide a refund of your premium if you cancel your policy after a certain time. However, if you are past this time limit, your refund will be prorated depending on your remaining policy and premium paid. It is important to be mindful of your insurance protection in case of job loss or disability.

Your credit limit is not raised by Loan Protection Insurance. In addition, your chances of being approved for credit are not improved. Nevertheless, making regular payments through insurance coverage will assist in maintaining your credit profile. The lender provides credit insurance in addition to your loan. The insurance is not part of your credit.

The insurance premiums may be fixed or varied based on the type of loan. In the case of a personal loan, the insurance may be fixed, while in the case of a line of credit, the insurance may vary with the balance. This may indirectly impact the insurance premiums paid.

In case insurance premiums are not paid, it is possible that the Loan Protection Insurance Coverage may lapse, and the loan may no longer be protected. Some insurance policies may offer a grace period, but after a lapse in insurance, it is possible that a new insurance policy may be required. Failure to pay insurance premiums may remove the safety net against disability, critical illness, or involuntary unemployment.

This is true because the majority of the policies have a waiting period before the benefits can be activated. In the meantime, the borrowers are expected to make their own payments. This period is necessary so that the claims made are genuine and in accordance with the terms and conditions of the insurance policy certificate and disclaimers.

The best Loan Protection Insurance Plans that Canada offers vary depending on your loan type and your risk profile. While some plans offer Disability Insurance, Critical Illness Insurance, and Life Insurance under one package, others only cover loan repayment. Independent providers also offer more flexible protection insurance plans than credit insurance providers. Comparing Loan Protection Insurance quotes is also helpful.

For mortgages, Loan Protection Insurance is similar in nature but is also known as mortgage insurance or creditor protection. It can cover loan repayment or reduce the loan balance in the event of disability, critical illness, or death. This is usually related to the loan amount and can be reduced over time. It is important to analyze the cost of insurance and structure.

In the case of a car loan or auto loan, the Loan Protection Insurance may be valuable if the loss of income would prevent the ability to make payments on the loan. However, since auto loans are short-term loans, the cost of the insurance premiums must be considered against the amount still owed on the car, unless the person already has disability or Life Insurance Coverage.

Loan Protection Insurance Canada is available for purchase from financial institutions, insurance brokers, and insurance companies that offer online insurance quote and application services. You may be able to compare Loan Protection Insurance quotes and features on independent websites. Buying insurance separately from a loan may give you more control over insurance protection.

Lender-Provided Loan Insurance is convenient and simple to sign up for. However, it may also come with additional insurance premiums. Third-party protection insurance plans offer customized insurance plans and transparent insurance premiums. Nevertheless, it may also require undergoing a medical exam or answering an extensive health questionnaire in the insurance application process.

Yes, many Loan Protection Insurance policies provide involuntary unemployment or job loss protection as part of their protection insurance. In this regard, the policies provide protection for the loan payments for a specific period in the event of involuntary job loss. However, the policies’ eligibility could be based on the type of employment, and seasonal employee positions could be restricted.

The majority of the Loan Protection Insurance Coverage provides protection in the event of disability, critical illness, or death, while some may also provide protection in the event of involuntary unemployment. The coverage may include the loan payments or the reduction of the outstanding amount of the loan.

To file Loan Protection Insurance claims, the following documents are usually needed: completed claim forms, evidence of disability or illness covered under the insurance policy, employment records in cases of job loss, and medical documents. However, the process may require more verification depending on the claims filed. Keeping documents updated is always a good idea in case of any unexpected event.

The process of applying entails filling out an insurance application, which may include a health questionnaire and, in some cases a medical examination. Approval is based on factors such as employment and financial conditions. After approval, an insurance certificate indicates the conditions associated with your loan or credit.

Yes, the Loan Protection Insurance provides for the payment of loans in the event of involuntary unemployment, subject to the conditions set by the policy. The benefits are usually payable after the end of the waiting period for a specified period. This is one form of insurance protection for loans.

Some of the Loan Protection Insurance Canada plans will include Disability Insurance as a standard feature. In this case, if a policyholder is not able to carry out their regular duties, they will be able to access a disability benefit. However, this will depend on the terms and conditions of the policy, and some plans will be able to provide this benefit for a shorter or longer duration.

Sources and Further Reading

Government/consumer guidance

- Financial Consumer Agency of Canada – Credit or Loan Insurance — overview of what credit or Loan Insurance covers, including job loss, critical illness, accident, and death.

- Financial Consumer Agency of Canada – Loan Insurance: know your rights — explains that Loan Insurance is optional and requires express consent.

Loan/line of credit protection pages

- RBC Royal Bank – LoanProtector Insurance — directly about protection for a personal loan or line of credit, with life, disability, and critical illness options.

- RBC Royal Bank – LoanProtector Quote — direct quote page for loan and line of credit protection insurance.

- Scotiabank – Scotia Loan Protection Insurance — specifically about car loan protection and coverage for involuntary job loss, illness, injury, or death.

- Scotiabank – Scotia Creditor Insurance — broader creditor insurance page covering outstanding loan or credit balances and payment protection after critical illness, disability, or death.

- Scotiabank – Loan Balance Protection Quick Estimate — quote/estimate page for loan balance protection insurance.

- Desjardins – Loan Insurance: Life and Disability Coverage — directly relevant to mortgage, personal loan, auto loan, and line of credit protection.

Policy/certificate documents

- RBC – LoanProtector Certificate of Insurance (PDF) — detailed certificate showing group creditor life, critical illness, and Disability Insurance, underwritten by The Canada Life Assurance Company.

- Desjardins – Loan Insurance Versatile Line of Credit Documents (PDF) — direct product documentation for line of credit and linked-loan coverage.

- TD – Protection for Your Line of Credit (PDF) — certificate-style document describing life and critical illness coverage for a line of credit.

Key Takeaways

- Loan Protection Insurance Is Loan-Specific Coverage

Loan Protection Insurance Canada is designed to cover loan payments or reduce the outstanding balance during events like disability, critical illness, or involuntary unemployment. It is directly tied to a loan or line of credit, not general financial use. - Coverage Focuses On Income Disruptions, Not Wealth Building

Protection insurance mainly supports loan payments when income stops due to unexpected events. It acts as a short-term safety net rather than a long-term financial planning tool like Life Insurance. - Costs Can Vary Based On Loan Type And Risk Profile

The cost of Loan Protection Insurance Canada depends on factors such as loan balance, age, employment status, and coverage type. Insurance premiums may be fixed for personal loan products or fluctuate for a line of credit. - Disability, Critical Illness, And Job Loss Are Core Features

Most Loan Protection Insurance Coverage includes Disability Insurance, Critical Illlness Insurance, and involuntary unemployment benefits. These features help maintain payments and protect financial stability during difficult periods. - Benefits Are Limited By Terms, Waiting Periods, And Conditions

Loan Protection Insurance claims are subject to waiting periods, policy limits, and exclusions such as pre-existing conditions. Understanding the insurance certificate and legal disclaimers is essential before purchasing. - Lender-Offered Plans Offer Convenience But Less Flexibility

Many banks offer bundled credit insurance, but these plans may come with higher premiums and less customization. Independent insurance coverage options can provide more flexibility and better control. - Not Always The Most Cost-Effective Option

While Loan Protection Insurance offers convenience, it may be less efficient compared to standalone Life Insurance or Disability Insurance, especially for long-term financial protection. - Best Suited For High-Risk Or Low-Savings Situations

Loan Protection Insurance makes more sense for individuals with high loan exposure, limited emergency savings, or no existing insurance protection. - Understanding Policy Details Prevents Claim Issues

Reviewing coverage limits, claim forms, eligibility rules, and employment requirements ensures smoother claims and avoids unexpected denials. - Decision Should Align With Financial Goals And Existing Coverage

Whether Loan Protection Insurance is worth it in Canada depends on your financial situation, existing insurance coverage, and ability to manage loan payments independently.

Your Feedback Is Very Important To Us

Thank you for taking a moment to share your feedback. Your responses will help us better understand your financial goals and provide tailored guidance on Guaranteed Universal Life Insurance solutions.

Privacy Note

Your information will be kept confidential and used solely to provide personalized guidance and insurance solutions. Canadian LIC respects your privacy and adheres to Canadian data protection and anti-spam regulations.

IN THIS ARTICLE

- Loan Protection Insurance in Canada: Costs & Benefits

- Loan Protection Insurance In Canada: Costs, Benefits, And Is It Worth It?

- How Loan Protection Insurance Works With Personal Loan, Car Loan, And Line Of Credit

- Disability Insurance And Involuntary Unemployment Coverage Explained

- Critical Illness And Life Coverage Under Loan Protection Insurance

- Credit Insurance Vs Loan Protection Insurance: Key Differences

- Cost Of Loan Protection Insurance In Canada

- Insurance Premiums Breakdown Based On Loan Type

- Benefits Of Loan Insurance Canada: When It Actually Makes Sense

- Is Loan Protection Insurance Worth It In Canada?

- Loan Protection Insurance Vs Life Insurance For Loans Canada

- Loan Protection Insurance Claims: Process And Limitations

- Legal Disclaimers And Hidden Terms You Must Know

- Final Decision Framework: Should You Buy Loan Protection Insurance In Canada?

Sign-in to CanadianLIC

Verify OTP