- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Personal Line Of Credit Loan Protection Plan In Canada: Why You Should Consider It In 2026

By Harpreet Puri

CEO & Founder

- 15 min read

- March 31st, 2026

SUMMARY

Understand how a Loan Protection Insurance Policy in Canada safeguards personal loans and lines of credit against disability, job loss, and critical illness. It covers Loan Protection Insurance benefits, coverage options, premiums, and claims, highlighting how credit insurance and Line of Credit Insurance strengthen financial planning and protect your family’s financial future in 2026.

Introduction

When situations in life don’t go the way you plan, the last thing that should be on your mind is all of your financial responsibilities. According to Statistics Canada and the Bank of Canada, total household credit market debt in Canada exceeds $3 trillion, with personal loans and lines of credit forming a significant share of non-mortgage borrowing. Yet sometimes, few consider just how vulnerable they are if a disability, job loss or critical illness blocks them from making the payments on that debt.

That’s when a Loan Protection Insurance Policy is not only something to consider but a financial safety net.

Understanding Loan Insurance And Its Growing Importance

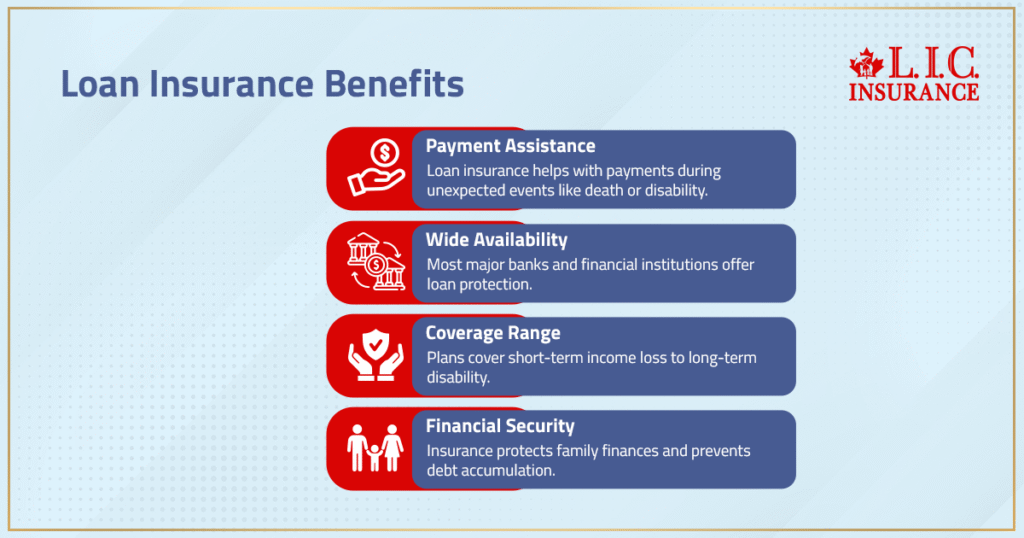

Loan Insurance can benefit the borrower by making their loan payments if something unexpected occurs — like death, disability or a covered critical illness. The vast majority of major banks and financial institutions have protection that extends to a personal loan, mortgage loan or line of credit.

A Personal Loan Protection Insurance Plan, for example, would typically pay the remaining balance or make payments through a certain period if you can’t. In Canada, these plans are created by many banks and insurers to provide coverage for anywhere from loss of short-term income to a disability that is more long-term disability.

Such insurance cover ensures that a family’s financial well-being is not compromised, halting the growth of debt when things turn tough.

What Is A Line Of Credit Protection Plan?

A line of credit offers flexible access to borrowed money, but with that flexibility comes the responsibility of making payments. If you die or become disabled, your loan balance doesn’t vanish — it may still be owed by your estate or co-borrower.

Line of Credit Insurance addresses this risk. It’s a form of credit insurance that covers all or part of your lines of credit if certain events happen — death, disability or a critical illness covered.

Depending on the coverage options, you can choose a plan that:

- Pays the full loan balance in case of death.

- Provides monthly benefit payments if you experience disability.

- Offers Critical Illness Coverage for events such as heart attack, cancer, or stroke.

These plans make sure your family’s future and financial resources are protected when you need them most.

The Role Of Disability Insurance In Loan Protection

Any Loan Protection Plan is incomplete without disability insurance. It’s there to help you out if illness or injury keeps you from working and paying off your loan.

According to Canadian insurance industry disability experience studies, more than one in three working Canadians will experience a disability lasting longer than 90 days before age 65. That is not a modest threat — it’s a distinct possibility.

With disability benefits included in your loan insurance, you will benefit from a steady income during recovery. It makes a lump-sum payment toward your balance or monthly payments in the amount of your usual loan payment.

At a time when income stops but bills do not, this is a practical financial safety net.

Credit Insurance And Critical Illness Protection

Credit insurance is commonly mistaken for loan insurance, yet there’s a slight difference. And while loan insurance covers individual debts, credit insurance can cover multiple open lines of credit — from a personal loan to a new card balance.

The vast majority of lenders offer critical illness insurance as part of their credit insurance products. So if you are diagnosed with a covered critical illness (think cancer or heart attack, for example), your insurer may pay off the loan balance in full or make payments based on your benefit amounts.

For a lot of those clients whom we have assisted, this coverage has made it possible for them not to have to deplete retirement assets or liquidate assets to be able to survive. It’s one of the least known and most powerful forms of insurance available today.

Why Canadians Need Loan Protection Insurance Coverage In 2026

Even as borrowing costs and inflation fluctuate, many Canadians are taking on credit merely to keep their lives going. According to Statistics Canada, the average household debt-to-disposable-income ratio remains near 180%, meaning Canadians owe roughly $1.80 for every dollar of disposable income. This means that the average Canadian owes $1.80 in debt for every dollar of disposable income.

In this context, Loan Protection Insurance Coverage in 2026 isn’t just a Plan B — it’s an element of responsible family financial planning.

Through a Loan Protection Insurance Policy, your personal loans, lines of credit or mortgage obligations are looked after in case you can’t make payments due to death, disability or critical illness.

It preserves your budget and protects your family and net worth.

Key Loan Protection Insurance Benefits

- Debt Relief During Crisis – The policy can pay off or reduce your outstanding balance if tragedy strikes.

- Protection Against Disability – Some loan protection policies include disability coverage, while job-loss benefits are limited, conditional, and available only through select lenders.

- Flexible Coverage Options – Choose what events you want covered: death, disability, or critical illness.

- Simplified Approval – Many loan protection plans use simplified underwriting with limited health questions, rather than full medical examinations.

- Cost-Effective Premiums – Insurance premiums often scale with your average daily balance, keeping costs manageable.

- Peace For Co-Borrowers And Family Members – Ensures your family’s future isn’t burdened with unpaid loan balances.

These Loan Protection Insurance benefits provide tangible value, especially when paired with broader Life Insurance or Critical Illness Insurance Coverage.

How Loan Protection Insurance Works In Canada

When you get a personal loan or line of credit, your lender may present the option to take out loan protection insurance. The insurance premiums, if approved, are added to your loan payments or line of credit statement.

Coverage begins once the insurance application is accepted, and all of that information can be found in the group policy, which provides you with all the specifics — such as maximum age, benefit amounts and coverage options.

Should a covered event happen, you or your loved ones will file a claim for Loan Protection Insurance. The lender is then paid directly by the insurer and can reduce or pay off (if the amount is extinguished) the outstanding balance.

This maintains the integrity of your credit and spares your financial life from even more pressure.

Combining Loan Insurance With Life Insurance

Loan Protection Policies cover certain debts, whereas life assurance covers general financial risks. Many of our customers end up with both.

A Term Life Insurance or Whole Life Policy can be used to replace income, pay taxes and fund future goals — while loan insurance is there to cover down debt.

Together, they make a powerful financial safety net — hitting every side of risk management. It’s part of what we refer to as a full financial plan — protecting both your possessions and the ability to pay for them.

Comparing Line of Credit Insurance To Other Insurance Products

| Type of Coverage | Purpose | Typical Events Covered | Payout Type |

|---|---|---|---|

| Line of Credit Insurance | Protects variable borrowing | Death, Disability, Critical Illness | Pays lender directly |

| Credit Insurance | Covers multiple credit accounts | Death, Disability, Job Loss | Partial or full balance |

| Loan Insurance | Tied to one loan | Death, Disability | Lump sum or monthly benefit |

| Life Insurance | Covers family and dependents | Death | Lump sum to beneficiaries |

| Critical Illness Insurance | Helps after a major diagnosis | Heart Attack, Cancer, Stroke | Lump sum to insured |

Understanding how these insurance products work together helps you design better protection around your financial resources and commitments.

How Insurance Premiums Are Calculated

Insurance premiums for loan protection vary depending on several factors:

- Age and health at the time of application.

- The loan amount or credit limit.

- Type of coverage options (life, disability, or critical illness).

- Whether coverage applies to an insured line or insured lines jointly with a spouse.

Premiums can be calculated as a percentage of your average daily balance or the total loan amount.

Our advisors often recommend reviewing quotes from multiple insurers, as Loan Protection Insurance quotes can vary depending on product design and lender partnerships.

Eligibility And Medical Requirements

Most Loan Insurance or Line of Credit Insurance plans have straightforward eligibility criteria:

- Applicants must be Canadian residents.

- Minimum age: 18 years; Maximum age: 65 to 70 years, depending on the insurer.

- No major health questions for smaller loans; larger loan balances may require a medical examination.

Some lenders offer automatically approved coverage upon loan approval, making it seamless for new borrowers.

Handling Loan Protection Insurance Claims

When you experience a covered event — such as a disability or a critical illness diagnosis — you or your representative files a Loan Protection Insurance claim with the insurer.

Most financial institutions have a standardized claims process:

- Complete a claim form with relevant health and loan details.

- Provide documentation (doctor’s note, proof of loan).

- The insurer verifies eligibility under the insurance policy.

- Once approved, the lender receives payment directly.

Claim processing timelines vary by insurer and complexity, typically ranging from several weeks to longer if additional documentation is required.

Reviewing Coverage Options Before You Commit

Before signing up, review the coverage options carefully. Check:

- Whether the plan covers only death, or includes disability and critical illness.

- What benefit amounts apply?

- Whether there are exclusions for pre-existing health conditions.

- The maximum age for eligibility.

- Any waiting periods before coverage begins.

Understanding the full details of your Loan Protection Insurance Policy ensures you aren’t surprised when it matters most.

Integrating Loan Protection Into Your Financial Plan

We’ve see countless clients have a lot of success in combining loan insurance, life insurance and critical illness all into one financial plan.

When it is designed right, it’s not just coverage — it’s part of your financial planning approach to shield assets and income.

With interest rates, credit conditions and more importantly, personal obligations evolving in 2026, that kind of layered protection is a must-have for all responsible borrowers.

Why Choose Canadian LIC For Loan Protection Insurance In Canada

Canadian LIC has over 10 years of experience working with top banks and insurers and can quickly secure competitive loan protection for you.

We don’t just sell insurance products — we create a protection plan to match your financial goals, insuring your loans and building up security in your net worth.

No matter if it’s a personal loan, home mortgage loan or line of credit, our specialists will compare options for coverage and calculate the best insurance premium rates before you sign on the dotted line.

You want to safeguard your family, your financial future, and the access you have to a line of credit — with professional guidance from our team.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

By taking out a Loan Protection Insurance Policy through the high-risk facility, we will be able to make loan repayments on your behalf if you meet an accident that leads to death, disability or critical illness. It protects your line of credit and personal loan from unpaid balances. This coverage will help to keep your lender and family protected during unfortunate circumstances.

Loan insurance helps clear your outstanding balance, whereas Life Insurance ensures that you leave behind the same amount of money for your family. Both of these combined form a full financial cushion for your future.

Yes, disability payments are one of the benefits built into many Personal Loan Protection Insurance Policies. These cover your monthly loan payments if you can’t work because of an illness or injury. It’s a simple way to safeguard income and financial stability.

Many major banks offer loan protection insurance with simplified eligibility questions, particularly for smaller balances, though coverage is not fully guaranteed. With larger balances, health questions may need to be answered (just a few), depending on the insurer and age.

Absolutely. Line of Credit Insurance is a specialized type of credit insurance available for revolving lines of credit. It will pay off your outstanding loan balance or monthly benefit amounts if you pass away, become totally disabled or are diagnosed as having a critical illness.

Premiums are based on loan amount, age, health and coverage elections. A few insurers (the premiums are based on the average daily balance to help make the policy affordable and predictable.

If a covered event happens, your insurer will pay the lender on your behalf, which shrinks or zeros out what you owe. Claims for death, disability and critical illness are settled as soon as possible once eligibility can be verified.

There are valuable insurance products, like credit insurance for personal loans and credit card balances. It will prevent you from accumulating debt when times are tough by preserving the strength and integrity of your overall financial plan.

A temporary cover for job loss is available with some loan protection insurance policies. They help keep regular loan payments active while you look for new income. This type of benefit is often seen as a form of financial backup should something bad happen in life.

Indeed, many banks and other financial institutions allow borrowers to add a Line of Credit Insurance policy to credit accounts they already have. It can serve to protect the insured line in case of unforeseen circumstances such as disability or critical illness. Plumping up coverage will provide additional support to your existing financial protection plan.

Coverage typically lasts until the loan or line of credit is paid off in full. Certain group policies automatically renew each year. For full-length durations, always check benefits and legal disclaimers.

Exemptions may be pre-existing medical conditions, self-inflicted injury, or age limits. Be sure to read your insurance application thoroughly before you sign up. Knowing exclusions are, makes certain coverage decisions meet your needs.

Yes, the majority of lenders allow cancellation at any time with written notice. Premiums could cease immediately, or there may be a partial refund owed. Look at the document outlining your insurer’s policy before you make a change.

Loan Protection Insurance makes sense when directly associated with a personal loan or line of credit. It prevents sudden debt accumulation and supplements life or critical illness insurance. What the perfect pairing is will depend on your financial situation and tolerance for risk.

Nope, loan protection does not impact your score or the process of getting approved for a loan. It’s a voluntary insurance product that pays your lender and you in the event of covered events that interrupt your payments.

According to most insurance, the oldest you can be is usually between 65-70. Younger applicants can also receive lower insurance premiums. Check policy criteria always before you go ahead and take out Loan Protection Insurance.

Yes, when applying for insurance against losses on a joint line of credit loan with insurable lines coverage. Both borrowers are covered for life, disability and critical illness of either party on pro rata basis. It provides equal coverage for both joint financial responsibilities.

Loan protection is such a great addition to your long-term financial plans. Life insurance and critical illness then protect your estate and keep any liabilities of the financial institutions secure. Together, both provide stability for your financial future.

Sources and Further Reading

- Credit or Loan Insurance – Financial Consumer Agency of Canada (FCAC) – overview of credit/loan insurance in Canada. Canada

- Loan Insurance: Know Your Rights – FCAC – consumer rights regarding loan insurance. Canada

- Line-of-Credit Protection – Scotiabank “Line of Credit Protection Insurance” – specific bank product covering line-of-credit. Scotiabank

- Creditor Insurance – Canada Life Assurance Company (Creditor Insurance page) – lender-offered insurance covering personal loan, line of credit, critical illness. Canada Life

- Loan and Line of Credit Insurance – National Bank of Canada (NBC) – coverage details for loans & lines of credit, including death/disability/critical illness. National Bank

- Loan and Line of Credit Protection Insurance – Bank of Montreal (BMO) – information on protecting personal loans/lines of credit with optional coverage. bmo.com

Key Takeaways

- Loan Protection Insurance Policy helps repay your loan balance or line of credit if you experience death, disability, or critical illness.

- Coverage ensures financial safety for your family and prevents debt from burdening co-borrowers during unexpected events.

- Disability insurance and critical illness insurance features offer monthly benefits or lump-sum payments based on coverage options.

- Most lenders and financial institutions provide Line of Credit Insurance with flexible coverage options and cost-effective premiums.

- Credit insurance can include additional protection for credit card balances and personal loans under a single policy.

- No medical examination is required for most smaller loan amounts; coverage can be automatically approved during the loan process.

- Insurance premiums are usually tied to the average daily balance or loan amount, keeping the policy affordable.

- Combining loan protection, life insurance, and critical illness coverage builds a solid foundation for your long-term financial plan.

- Reviewing eligibility, legal disclaimers, and benefit amounts before applying ensures complete understanding of your protection.

- Partnering with Canadian LIC provides access to multi-carrier comparisons and expert guidance on choosing the right loan protection coverage for 2026.

Feedback Questionnaire:

We’d love to hear your thoughts!

Your feedback helps us understand the financial challenges Canadians face and how Canadian LIC can better guide you toward the right protection plan.

Thank you for sharing your thoughts!

Your answers help Canadian LIC continue improving its support, tools, and guidance for Canadians seeking the best Loan Protection Insurance Plans in 2026.

IN THIS ARTICLE

- Personal Line Of Credit Loan Protection Plan In Canada: Why You Should Consider It In 2026

- Understanding Loan Insurance And Its Growing Importance

- What Is A Line Of Credit Protection Plan?

- The Role Of Disability Insurance In Loan Protection

- Credit Insurance And Critical Illness Protection

- Why Canadians Need Loan Protection Insurance Coverage In 2026

- Key Loan Protection Insurance Benefits

- How Loan Protection Insurance Works In Canada

- Combining Loan Insurance With Life Insurance

- Comparing Line of Credit Insurance To Other Insurance Products

- How Insurance Premiums Are Calculated

- Eligibility And Medical Requirements

- Handling Loan Protection Insurance Claims

- Reviewing Coverage Options Before You Commit

- Integrating Loan Protection Into Your Financial Plan

- Why Choose Canadian LIC For Loan Protection Insurance In Canada

Sign-in to CanadianLIC

Verify OTP