- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

How Much Is Disability Insurance In Canada?

By Harpreet Puri

CEO & Founder

- 10 min read

- July 09, 2026

SUMMARY

Disability Insurance in Canada explained with a clear breakdown of Disability Insurance cost, premiums, and monthly benefit estimates. Covers long-term Disability Insurance, Income Protection Plans in Canada, and how health status, occupation, and elimination period affect pricing. Also compares disability and Life Insurance, highlights providers, and shows how to get accurate Disability Insurance quotes.

Introduction

Why Disability Insurance Costs Matter More Than You Think

The promise of a stable paycheck seems safe until the pay stops coming. It happens more often than one would expect. According to statistics provided by the Canadian Life and Health Insurance Association, the majority of disability claims in Canada are caused by illnesses and not injuries. On the other hand, the figures from Statistics Canada reveal that there are millions of Canadians who have disabilities that may impact their productivity in life.

It’s clear from the experience at Canadian LIC that the actual danger goes beyond covering health costs. More importantly, the problem lies in the absence of income at a particular moment. If illness or injuries prevent you from doing your job, your liabilities remain the same. Whether it is your mortgage payments, rent, food, insurance bills, or anything else, you still owe money even without earning.

The Cost of Disability Insurance in Canada involves more than just the monthly premium amount. It requires knowledge of the level of coverage that you require to sustain your finances in times of income interruption. This way of thinking alters the way most individuals perceive Disability Insurance, where the costs seem insignificant relative to the potential risks involved.

What Is Disability Insurance And How Does It Work In Canada?

Disability Insurance serves the purpose of ensuring you receive payments in case of sickness or accident that leaves you unable to go to work. The money is given out on a monthly basis as a benefit and replaces a certain proportion of the income you were making. This will help ensure that you are able to cover all your costs, including housing, buying food, transport, and all other monetary obligations.

The definition of disability varies according to most Canadian policies, and it determines when you start receiving the benefits. Total disability refers to the situation where you are unable to perform the duties of your occupation, while residual disability happens when you can work but earn less as a result of the condition.

In addition, today’s policies come with “own occupation” provisions, and therefore, even if you can work but not in your own job, you get benefits. Professionals who have unique skills are protected by such clauses since changing occupations might result in lower income levels.

Income replacement is one of the most important aspects of Disability Insurance, and in almost all cases, about 60-70% of pre-disability income is replaced by the policy.

Types Of Disability Insurance Plans In Canada

There is no standard design for Disability Insurance, which influences both coverage and cost.

The most customized option available is individual Disability Insurance. In an individual Disability Insurance Plan, the insured can choose his or her own benefit amount, elimination period, and benefit period. This type of insurance is particularly useful for people seeking long-term Disability Insurance that is independent of their occupation.

Group Disability Insurance covers a group of employees in a particular organization. This type of insurance is convenient and easy to access. However, it comes with certain restrictions and limitations. The employer may pay for group Disability Insurance, but it is not always possible to keep the coverage upon changing jobs.

Disability Insurance assumes greater importance in the case of those who are self-employed. Self-employed people do not have an automatic system of income replacement provided by their employers. The insurance will ensure that the individual’s income is not affected by any ups and downs in the business.

The government and workers’ compensation schemes may help some in providing income protection, but this is not meant for everyone. In several cases, the compensation will be partial and may not meet all the requirements.

How Much Does Disability Insurance Cost In Canada?

The first and foremost query pertains to the cost of Disability Insurance in Canada. There are various parameters involved; however, there is always a standard rule of thumb for arriving at an estimated figure.

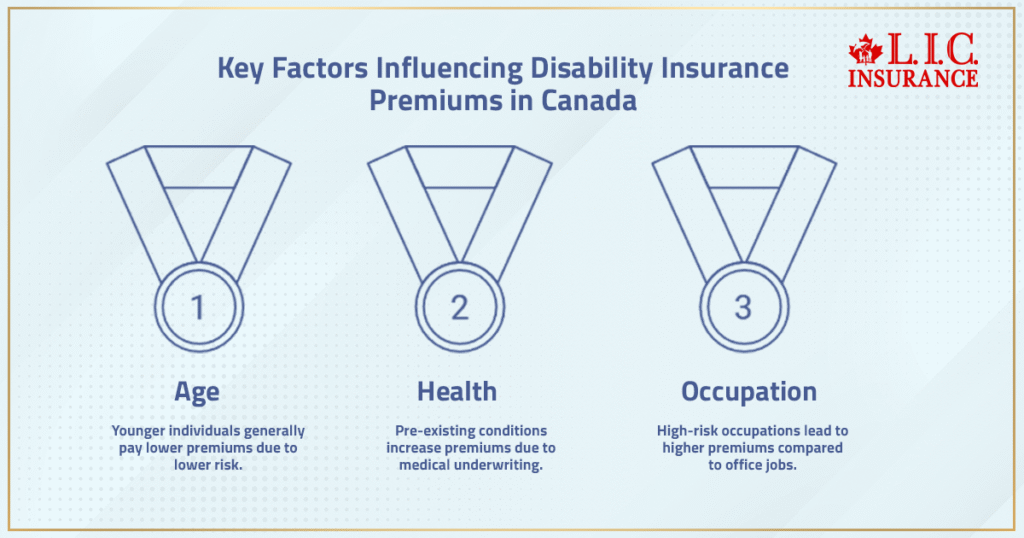

Usually, the insurance premium amount varies within the 1% and 3% bracket of your total income amount. An individual with a salary of $80,000 can expect premiums between $70 and $160 on a monthly basis. Other variables include age, health, occupation, and terms of the insurance policy.

Generally, young people have to pay fewer amounts for insurance coverage since they do not pose any danger to the insurance company. With increasing age, one’s chances of suffering from sickness and accidents increase, leading to increased premiums. The health condition of the applicant also matters greatly since people with pre-existing diseases have to pay more due to medical underwriting.

Occupation is yet another important determinant. An individual employed in an office setting pays lower premiums compared to one who works in a job that requires physical exertion, like construction work. The extent of risk involved with the kind of work determines the cost of purchasing Disability Insurance.

The size of the benefit will make a difference, too. Greater benefit amounts mean higher premiums; however, they give better coverage.

Disability Insurance Premium Comparison In Canada (2026)

A clearer picture emerges when looking at typical premium ranges across different age groups and income levels.

| Age | Annual Income | Monthly Benefit | Elimination Period | Estimated Monthly Premium |

|---|---|---|---|---|

| 25 | $60,000 | $3,000 | 90 Days | $40–$65 |

| 35 | $80,000 | $4,500 | 90 Days | $75–$120 |

| 45 | $100,000 | $5,500 | 90 Days | $140–$220 |

| 55 | $100,000 | $5,000 | 120 Days | $220–$350 |

These estimates reflect patterns seen across the Canadian market and multiple insurers. They highlight how monthly premiums increase with age and how benefit levels affect cost.

What Factors Affect Disability Insurance Premiums?

There are several components that make up the cost of Disability Insurance. While age is definitely one of the biggest ones, there are others that play their part as well.

First off, health can be a huge determining factor in insurance premiums. People who are generally healthy without any sort of chronic illness are likely to enjoy lower premiums based on medical underwriting.

The field of work will determine your premiums as well. If you are doing something that poses little danger, such as accounting, then your premiums will be relatively low. Otherwise, the more dangerous the work is, the higher the insurance premium will be.

As of late, insurance providers have been paying close attention to psychological problems that may affect their clients. In particular, claims made because of stress-related issues have been on the rise lately.

Smoking and other lifestyle choices can also raise your insurance premiums.

How the Elimination Period Impacts Disability Insurance Cost

The Elimination Period is sometimes called the Waiting Period. It represents the period from the onset of your disability until the start of benefit payments. The selection will have a direct influence on your monthly premium payment.

In case you want your benefit payments to be paid sooner, a smaller Elimination Period should be considered; however, it will increase the cost of insurance. Otherwise, the larger Elimination Period will lower the premium rate but will require some money reserve.

One can recommend 90 days as the Elimination Period for most people.

How Much Disability Insurance Coverage Do You Need?

The amount of coverage required would depend on your liabilities and needs. The general rule is to purchase an insurance policy that will replace your income by 60%-70% per year.

Such income replacement will cater to your basic needs, which include mortgage repayments, electricity bills, groceries, and other necessities. This would guarantee you financial freedom in case you have no income source.

The other thing to remember is that you will require more insurance in future. Some insurance companies have future income provisions in their policy, which will enable you to increase your insurance as you earn more without any further medical examination.

Long-Term Disability Insurance Vs Short-Term Plans

Short-Term Disability Insurance gives cover only for a short while, normally a few months. This type of insurance is meant to cover temporary income disruptions.

Long Term Disability Insurance covers one for a relatively long period, which may range from a few years to all the way through one’s working life until one retires. It therefore becomes important in financial planning.

Both combined can prove quite effective.

Learn more about Can I Have Both Short-Term and Long-Term Disability Insurance?

Disability Insurance Vs Life Insurance: Understanding The Difference

Life Insurance and Disability Insurance have different uses despite being equally important for financial safety.

Where Life Insurance guarantees financial security in the form of a lump sum after the policyholder passes away, Disability Insurance covers financial needs during the lifetime of the insured person. Both of these make for an effective financial plan.

It is frequently observed that those who give priority to Life Insurance neglect the possibility of income interruption while they are young and able-bodied.

Mental Health Conditions And Disability Benefits In Canada

In Canada, mental disorders have been among the top contributors to disability cases. Mental illnesses, such as depression, anxiety, and burnout, are considered valid grounds for obtaining disability benefits.

There is an increased trend toward the inclusion of mental health disorders in Disability Insurance Plans, despite some restrictions that may be imposed.

Real Example: How Disability Insurance Protects Income

A contractor earning $80,000 annually can be considered an example, which will allow understanding the principle of Disability Insurance. As a consequence of the accident, he will be unable to continue working for many months; therefore, there will be a decrease in his income.

Without any insurance policy, he will have to use all the funds until there are none. If he has a policy, then his monthly income would be roughly $4,000. Therefore, he will still be able to cover his expenses and live well.

Such cases are common. It is obvious that protecting your income is necessary for most people.

Top Disability Insurance Providers In Canada

The Canadian market has a few providers who offer insurance policies tailored for disabled persons. Examples of such companies include RBC Insurance, Sun Life Financial, and Manulife.

It is advisable to seek the assistance of an insurance broker, who will help you review the different policies from various providers.

How To Get The Best Disability Insurance Quotes In Canada

Comparing Disability Insurance premiums is not simply a matter of looking for cheaper rates. Comparisons have to be made regarding policy features, what disability is defined to mean, and the structure of benefits provided.

This is where the expertise of an insurance broker comes into play. The broker will be able to look at your situation from the perspective of several insurance providers.

Common Limitations To Understand Before Buying

Each policy will have some restrictions as well. They can consist of maximums, exclusion of certain ailments from coverage, and even a waiting period before benefits commence.

It is important to understand all these factors in order not to be caught off guard in case you need to collect your benefits. Moreover, there are policies that carry tax consequences, and sometimes the premium is tax-deductible.

Is Disability Insurance Worth The Cost In Canada?

In assessing the cost of Disability Insurance, one must consider how the premium relates to the financial effects of losing income.

For the average person, the premium would only account for a fraction of his or her monthly earnings. Yet, without Disability Insurance, the repercussions could be quite severe.

The financial security provided by Disability Insurance is unparalleled in savings. A substantial emergency fund might be insufficient during prolonged income loss.

Final Educational Takeaway: Understanding Disability Insurance Cost

The Cost of Disability Insurance in Canada depends on the degree of coverage you want. Well-selected insurance helps ensure the continuity of the flow of money, regardless of whether you can go to work or not.

The point is that you need to see Disability Insurance not as spending money, but as a guarantee of your financial well-being in the future. Regular payment each month gives you access to coverage that will allow you to feel comfortable financially.

FAQs

Yes, because there is a chance that you will be able to make changes to your policy after buying Disability Insurance. This includes lowering your coverage amount, altering your elimination period, or upgrading your policy’s options based on your financial standing.

While being paid disability benefits, insurance companies look at medical files, doctors’ statements, and your performance at work. Sometimes an independent assessment may be required to prove that you have either total or partial disability.

Some companies provide reduced premiums on their bundled packages with life and critical illness coverages. Individuals working in less risky professions can also be eligible for better premiums in Canada.

Disability Insurance may be used to pay for the routine expenses associated with running your business. Disability Insurance Policies are designed specifically in Canada to ensure financial security in case you get ill or injured, making it impossible for you to work.

Most individual Disability Insurance Plans remain valid across provinces. Coverage continues without interruption, although local healthcare systems and claim processes may slightly influence how benefits are administered.

Certainly. Both are designed to protect you in completely different ways. The Disability Insurance gives you a steady income, while the critical illness policy will give you one payment in full.

It is possible to find such insurance, although its premiums are higher, and the benefit amount is lower compared to underwritten insurance policies, which cover you longer and have lower premiums.

Generally speaking, buying coverage earlier results in lower premiums and better eligibility. Waiting until health conditions develop can increase costs or limit access to comprehensive Disability Insurance Plans.

There are several top Disability Insurance companies operating in Canada. Some of these companies include RBC Insurance, Sun Life Financial, and Manulife. The different insurance companies have various types of Disability Insurance Plans. Comparing Disability Insurance quotes enables one to choose an appropriate plan for them.

The purpose of disability income insurance is to provide coverage for some of your income in the event you become sick or injured to the extent that you are unable to work. This will guarantee you a consistent income flow without having to depend totally on your savings.

Short-term Disability Insurance Coverage is typically provided by insurers such as Sun Life Financial, Manulife, and Canada Life. This insurance is typically covered under an employee group plan or within the overall structure of the insurance plan.

A Disability Insurance claim usually requires submission of medical evidence, proof of loss of income, and information about the nature of your work. The insurer will then determine if your situation qualifies for the total disability as defined in the policy contract.

When requesting a customized Disability Insurance quote, you would normally need to give your age, income per year, occupation, and medical condition. Thereafter, you may be able to have various Disability Insurance quotes reviewed by an online comparison tool or an insurance broker, who will then suggest income-protection policies for you.

Sources and Further Reading

- Financial Consumer Agency of Canada

Disability Insurance Explained In Canada

Clear explanation of how Disability Insurance works, including income replacement ranges (typically 60%–85%) and benefit structures.

- Canadian Life and Health Insurance Association

CLHIA Consumer Guides On Disability Insurance

Industry-backed guidance on Disability Insurance Coverage, claims, and financial protection concepts.

- Canadian Life and Health Insurance Association

Guide To Disability Insurance (Income Protection Overview)

Explains how Disability Insurance protects against income loss when illness or injury stops earnings.

- Government of Canada

Canada Pension Plan Disability Benefits Overview

Details government disability benefits and how they complement private Disability Insurance Plans.

- Canadian Life and Health Insurance Association

Insurance Industry Overview And Disability Coverage Context

Provides broader insights into Disability Insurance within Canada’s life and health insurance sector.

Key Takeaways

- Disability Insurance in Canada plays a central role in protecting income when an illness or injury prevents you from working. The cost of Disability Insurance in Canada typically ranges between 1% and 3% of annual income, making it a manageable monthly premium compared to the financial impact of lost income.

- Disability Insurance premiums are influenced by age, health status, occupation, and the structure of the insurance plan, including the elimination period and benefit period. Choosing longer waiting periods can reduce monthly premiums, while higher coverage and shorter elimination periods increase costs.

- Long-term Disability Insurance provides extended income protection and is often more critical than short-term plans, especially for maintaining financial stability over time. While group Disability Insurance offers basic coverage, individual Disability Insurance Policies provide stronger and more flexible protection.

- Mental health conditions are now a significant factor in disability claims, and many modern policies include coverage for these conditions, subject to policy terms. Comparing Disability Insurance quotes from multiple providers ensures better alignment with income protection needs.

- Disability and Life Insurance serve different purposes but work together to create a complete financial protection strategy. A well-structured Disability Insurance Plan ensures continued income replacement, helping cover financial obligations, essential expenses, and long-term commitments without relying solely on savings.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- How Much Is Disability Insurance In Canada?

- What Is Disability Insurance And How Does It Work In Canada?

- Types Of Disability Insurance Plans In Canada

- How Much Does Disability Insurance Cost In Canada?

- Disability Insurance Premium Comparison In Canada

- What Factors Affect Disability Insurance Premiums?

- How the Elimination Period Impacts Disability Insurance Cost

- How Much Disability Insurance Coverage Do You Need?

- Long-Term Disability Insurance Vs Short-Term Plans

- Disability Insurance Vs Life Insurance: Understanding The Difference

- Mental Health Conditions And Disability Benefits In Canada

- Real Example: How Disability Insurance Protects Income

- Top Disability Insurance Providers In Canada

- How To Get The Best Disability Insurance Quotes In Canada

- Common Limitations To Understand Before Buying

- Is Disability Insurance Worth The Cost In Canada?

- Final Educational Takeaway: Understanding Disability Insurance Cost

Sign-in to CanadianLIC

Verify OTP