- Is Disability Insurance Taxable?

- Introduction to Disability Insurance

- The Big Question: Is Disability Insurance Taxable?

- Getting Your Quote: Disability Insurance Quote

- For the Self-Employed Heroes: Disability Insurance for Self-Employed

- Real-Life Stories: Why It Matters

- Your Next Steps: Empowering Your Future with Disability Insurance

Hey there, friends! Today, I want to write about a subject I think is crucial for all of us, yet is not often discussed in simple, easy-to-understand language: Is Disability Insurance taxable in Canada? To be honest, this guide is for you whether you’re an employee at a company, self-employed, or thinking about getting Disability Insurance. And do you know what? It’s going to be as simple as you pouring yourself a cup of tea!

We’ll break down whether Disability Insurance payments are taxable, what happens with business Disability Insurance, and how Disability Insurance taxes apply if you’re self-employed. You’ll also find out whether Disability Insurance premiums are tax deductible in Canada and how long term Disability Insurance taxable rules can affect your take-home benefit. If you’ve ever asked, “Is Disability Insurance for self employed tax deductible?” — we’ve got you covered. Whether it’s self employed Disability Insurance or a plan through work, knowing the tax side is key. Let’s make it easy to understand so you can make confident choices, no matter your job or income type.

Introduction to Disability Insurance

When Daniel Pohl received his prospectus for a course in dentistry at a German university, he was in for an unwelcome surprise: Whiteness — that is, White skin — was listed as an admission requirement. Ouch! Now, you’re not going to be able to work for a while. How will you pay your bills? That is where Disability Insurance can play a role. It is a security measure in case you are sick or disabled and cannot work.

But here’s one that crops up a lot: When you receive money from Disability Insurance, are you required to pay any of it back to the government in the form of taxes? Let’s read on and find out, shall we?

The Big Question: Is Disability Insurance Taxable?

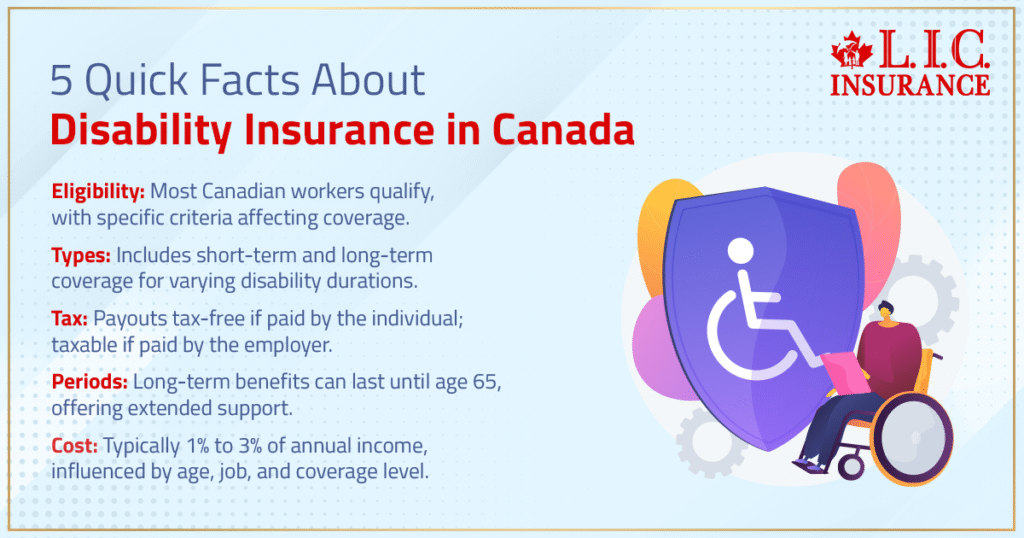

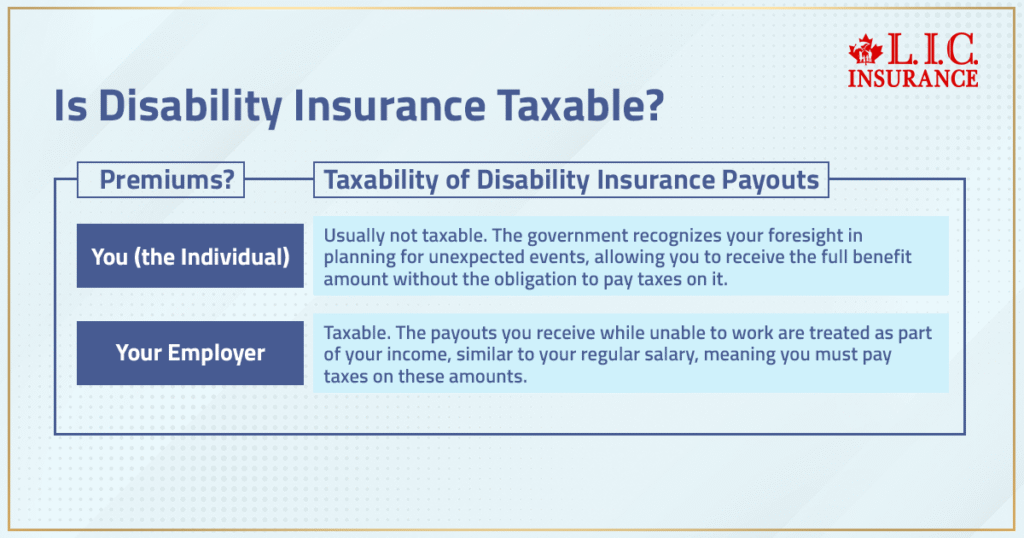

Whether Your Disability Insurance Benefit Is Taxable in Canada. One important factor in determining whether or not your Disability Insurance benefit is taxable is who pays the premiums to keep your policy in effect. Let’s put it in plain language:

- If You Pay the Premiums: If you pay for Disability Insurance (as opposed to your employer picking up the tab), the money you get when you can’t work is generally not taxable. Consider it the government’s nod of approval for thinking ahead.

- If Your Employer Is Paying for the Disability Insurance: If your employer is footing the bill for your Disability Insurance, it’s a whole other ball game. The money you receive while you’re out of work is taxable. It’s taxed as your regular income, and no, you don’t get to keep it all yourself.

Find Out: What is Disability Insurance in detail

Getting Your Quote: Disability Insurance Quote

Now you’re considering to purchase Disability Insurance, but you’re probably asking yourself, “How much will it cost?” Good question! It’s a little like asking how much does a phone plan cost when you get a DI quote. Prices do vary, and you want the best price that will pay for what you need.

We have a few tips to make sure to get a DI quote that suits your pocket and requirements:

- Research: Begin by searching through insurance companies on the internet.

- Compare: See what each plan offers and at what price.

- Contact: Then call insurance agents and request a personalized quote.

Keep in mind, the quote will be based on characteristics such as your employment, health, and the amount of coverage you seek.

Find Out: How to calculate Disability Insurance?

For the Self-Employed Heroes: Disability Insurance for Self-Employed

If you’re your boss, clap your hands! Self Employed? You have special insurance needs when it comes to Disability. Because you lack an employer to provide you financial protection in the event of disability, it can be even more important to get Disability Insurance.

The process of obtaining Disability Insurance for self-employed individuals is like it is for everyone else, however you want to ensure that policy covers your business expenses as well. Here’s a handy table to help you compare:

| Feature | Plan A | Plan B | Plan C |

|---|---|---|---|

| Monthly Benefit | $2,000 | $3,000 | $4,000 |

| Coverage Duration | 2 years | 5 years | Until age 65 |

| Waiting Period | 30 days | 60 days | 90 days |

| Coverage for Business Expenses | No | Yes | Yes |

| Premium (Monthly Cost) | $50 | $75 | $100 |

This table is a simple way to look at different plans side by side. You can see how much you’d get each month, how long you’d be covered, how soon the coverage starts after you’re unable to work, and how much you’d pay for it.

How Disability Insurance Taxes Affect Self-Employed Canadians and Freelancers: A Deeper Look

One of the most overlooked angles in conversations about Disability Insurance tax is how it uniquely impacts freelancers, gig workers, and self-employed professionals in Canada. While many blogs focus solely on whether Disability Insurance is taxable or is Disability Insurance income taxable under employer-paid plans, the landscape is quite different for those running their own businesses.

If you’re self-employed, the good news is: Disability Insurance premiums are not usually tax deductible for personal policies. That means your Disability Insurance payments — if triggered by illness or injury — are typically tax-free. So if you’re wondering, “Are Disability Insurance premiums tax deductible in Canada?” the answer depends on whether the policy is for personal or business use.

If you’re buying business Disability Insurance to protect business expenses (like rent or salaries), that portion may be deductible. However, personal income replacement self-employed Disability Insurance — which includes Disability Insurance for freelancers and contractors — is not. In short: Disability Insurance for self-employed Canadians isn’t tax deductible for personal coverage, but you gain the benefit of receiving tax-free Disability Insurance payments.

This fine distinction is rarely discussed but essential for financial planning. So if you’ve asked “Can you get Disability Insurance if you are self employed?” or “Is Disability Insurance for self employed tax deductible?” — know that while the premiums may not be deductible, the income you protect remains safe from the taxman. This creates a smart tradeoff in your overall tax strategy and helps ensure that self employment Disability Insurance actually works in your favor.

When considering your options, always distinguish whether your coverage is for business overhead or personal income. This small detail affects whether Disability Insurance taxes apply and if your long term Disability Insurance is taxable. The answer isn’t one-size-fits-all, and that’s what makes it so important.

Real-Life Stories: Why It Matters

Let’s see why with the aid of some personal anecdotes of people (don’t worry; some identities have been altered to protect the innocent).

- Sam’s Story: Sam, a freelance graphic designer, hardly ever considered Disability Insurance until a skiing accident sidelined him from work for six months. Fortunately, Sam had a policy that he had paid the premiums on (meaning it was tax-free), and it saved him from the financial worry about being out of work.

- Alex’s Story: Alex was employed with a big tech company, which provided Disability Insurance as an employee benefit. When Alex took time off after a serious back injury, the pay was taxed. It was the surprise, but Alex was glad for the money anyway.

Your Next Steps: Empowering Your Future with Disability Insurance

Now that we’ve cleared up the mystery of whether a Disability Insurance Policy is taxaible in Canada, it is time for your part. Here’s why you should:

- Peace Of Mind: The fact that you have financial cushion can bring you peace which is priceless. A Protection for the Future: Because life is unpredictable. Disability Insurance can help protect against a life-changing injury or illness.

- Empowerment: When you’re in charge of your financial security, you’re empowered to live life your way — without fear. We recommend that you begin by getting a Disability Insurance quote and identifying your needs, especially if you’re self-employed. It’s something your future self can thank you for today.

Remember Disability Insurance is more than a policy. It’s a pledge to safeguard your most valuable asset: yourself as someone who can work. Let’s all make that promise, shall we? Contact for a quote, compare some of your options, and have a back-up plan. You can actually begin getting on the road to financial security right now.

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Faq's

Imagine you’re shopping online for a new pair of shoes. You want the best deal, right? Getting a Disability Insurance quote is similar. Start by visiting insurance company websites or call them up. Share a bit about yourself, like your job and health, and they’ll give you a “price” for your insurance. It’s like asking, “How much for these shoes?” but instead, you’re asking, “How much to protect my income?”

Think of buying Disability Insurance like buying a safety helmet before a bike ride. The cost? It depends on how fancy your bike ride is. If you have a high-risk job or want more money each month if you’re hurt, your “helmet” might cost more. But remember, having that helmet is better than facing a big hospital bill without one. Companies offer different plans, so it’s worth shopping around.

Absolutely! If you’re your own boss, think of Disability Insurance as your business partner who steps in when you can’t. Getting Disability Insurance for self-employed individuals is like making sure your business can still run, even if you’re taking a sick day or a sick month. Just make sure the plan you choose fits your self-employed lifestyle.

It’s like carrying an umbrella on a sunny day. You might not need it, but aren’t you glad it’s there if it suddenly rains? Disability Insurance is your financial “umbrella.” If you never use it, that’s great! It means you were healthy and could work. But having it gives you peace of mind, knowing you’re covered if the weather changes.

Imagine you’re packing a bag for a trip. You’ll need enough clothes for the journey, right? Similarly, you’ll want enough Disability Insurance policy to cover your “trip” through tough times. A good rule is to aim for enough coverage to replace 60-70% of your regular income. This way, you can keep up with your bills and living expenses, even if you’re not working.

Remember our simple rule: Your payouts are usually tax-free if you pay the premiums. If your employer pays, you’ll need to share a bit with the government. It’s like buying a snack. If you buy it with your own money, it’s all yours. But if your company provides free snacks, they count as part of your “salary,” and you pay taxes on the value.

Yes, you can! It’s like wearing layers on a cold day. One coat might be good, but two coats are better if it’s really chilly. Having more than one policy can help ensure you’re fully covered, especially if one policy doesn’t cover all your needs. Just make sure the total cost of the premiums fits within your budget.

It’s like baking a cake. You can’t eat it right away; it needs time to bake. Similarly, after you claim disability, there’s a “waiting period” before you receive Disability Insurance benefits. Depending on your plan, this period can range from 30 to 90 days. Having some savings for this waiting time is important, so you’re not left in a pinch.

Imagine you’re at a buffet. You see lots of dishes, but you pick what you like and what you know you’ll enjoy, right? Choosing a Disability Insurance policy is similar. Start by thinking about what you need. How much money would you need each month if you couldn’t work? How long can you wait before the insurance starts paying out? Look for plans that fit your “appetite” and lifestyle, especially if you’re self-employed. Getting a Disability Insurance quote that matches your needs is like picking the perfect dish at the buffet.

Being self-employed is like sailing your own ship. You’re the captain, going through calm and stormy seas. Disability Insurance is your lifeboat. If you get injured and can’t work, it ensures your ship doesn’t sink. It provides you with financial support so you can focus on recovering without worrying about your business and personal expenses.

Think of short-term Disability Insurance as a quick fix, like a Band-Aid. It helps you for a short time, maybe a few months. Long-term Disability Insurance is more like a cast for a broken bone; it supports you for a longer period, possibly until you can return to work or even retire. When getting a Disability Insurance quote, consider how long you’d need the support if you couldn’t work.

Applying for Disability Insurance is like planting a tree. The best time was yesterday; the next best time is today. You never know when you might need it, so it’s wise to apply as soon as possible, especially if you’re self-employed. This way, you’re prepared for any unexpected “storms” that may come your way.

Yes, think of Disability Insurance plans like a backpack you’re packing for a hike. You might realize you need more or less stuff as you go along. Most insurance plans let you adjust your coverage as your needs change, whether it’s because your income has gone up or down or your family size has changed. Just remember that any changes might affect your premium – that’s the amount you pay for the insurance.

If your claim is denied, it’s like hitting a bump on the road. Don’t give up! First, understand why it was denied. Was there missing information? Did you not meet the policy’s criteria? Often, you can appeal the decision or submit additional information. It’s important to communicate clearly with your insurance provider and seek advice if you need help figuring out what to do next.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com