- Connect with our licensed Canadian insurance advisors

- Schedule a Call

Basics

Basics

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Disability Insurance Isn’t Optional In 2026—Here’s Why

By Pushpinder Puri

CEO & Founder

- 12 min read

- May 12th, 2026

SUMMARY

Disability Insurance Plans in Canada have become essential in 2026 as auto insurance and accident benefits offer limited income protection. The discussion explains Disability Insurance coverage gaps, rising Disability Insurance costs, Ontario system changes, and why relying on optional benefits or group benefits can leave people underinsured. It highlights income risk, long-term support needs, and when requesting a Disability Insurance quote online, it becomes critical.

Introduction

Introduction: A Fundamental Shift In How Canadians Are Protected

The risk of disability is not something far in the future anymore, in the year 2026, but a financial fact that many Canadians are undervaluing. The Ontario Government and FSRA data released show that the number of claims made because of injuries is constantly growing, and the benefit limit has stayed relatively the same. Concurrently, medical and rehabilitation costs are working towards being stretched by inflation like never before.

Consumers are finding out too late across Ontario that their insurance does not entirely cover their income. In Canada, Disability Insurance Plans have been perceived as supplemental. Nowadays, they are established. Disability Insurance coverage has become the distinction between financial salvation and economic instability. The true cost of having no Disability Insurance would increase with the increase in its cost. That is the reason why an increasing number of Canadians are asking to have their Disability Insurance quote over the internet before an accident compels the matter.

This is not a message based on fear. It is a reaction to the system that is experiencing a fundamental change, one that makes people more responsible.

Why Accident Benefits Still Matter More Than Most People Realize

The protection system in Ontario after an accident is based on accident benefits. The statutory accident benefits schedule has some benefits that will be mandatory irrespective of fault. These are medical and rehabilitation costs and low-income replacement.

Nevertheless, statutory accident benefits never aimed at the complete restoration of financial stability. Although benefits will still be in place in the prevailing system, the level of coverage is, in most cases, too low to recover in real life. In Ontario, drivers often assume that they are covered entirely, only to find out that they have limits when the claim process commences.

Accident benefits are useful, but do not reduce risk. They do not provide complete protection, but only minimal support.

The Hidden Gaps Inside Optional Benefits Most Drivers Skip

It is in optional benefits that real protection is found, and it is to optional benefits that the majority of drivers are choosing to forego. The optional benefits can be declined, which will lower the premiums, but this will also leave less coverage when it is required the most.

Such optional coverage as higher income replacement, extra benefits, and enriching care options are not well understood or may be overlooked. In the long run, this opting behaviour will result in long-term gaps for underinsured accident victims. Add-ons are worthwhile diversions, but most consumers do not know the real value of optional add-ons until they have had a serious collision.

Not taking much coverage is not a savings plan. It is a gamble.

When A Personal Injury Lawyer Becomes Part Of The Equation

A personal injury attorney can enter into the fray in severe accidents, particularly when tort damages are committed against a negligent driver. Such cases are characterized by grave injury, grave outcomes of collision, or impairment in the long term.

Though litigation can provide compensation, it is hardly quick. The claims are costly, the results are unpredictable, and victims of accidents are left vulnerable financially in the whole process. The use of litigation and, in lieu of adequately planning insurance, is dangerous, unpredictable, and emotionally exhausting.

Insurance must not substitute legal action; it must decrease it.

Auto Insurance Isn’t Disability Insurance—And Never Was

Auto insurance has been misconstrued. Auto Insurance offered by Ontario is not aimed at substituting long-term income, but a response to a car accident. Although the insurance company can play the role of the first payer following an accident, the amounts and the time frame of the benefits of the auto insurance are small.

Automobile policy insures against liability and immediate expenses of accidents. It is not a substitute for a full-fledged Disability Insurance Plan. The insurance firms design coverage to reflect this, and income protection is not much a part of the auto framework.

This differentiation is more than ever.

How Insurance Companies Are Reshaping The Current System

Increased claims, increased medical expenses, and regulations are all forcing insurance companies to adapt. What would be the outcome is a new model that does not aim at expansion but goes towards sustainability? This has brought a paradigm change in the delivery of benefits.

New regulations restrict the exposure, premiums are priced higher, and containment of costs has been a priority. The system remains, albeit it has taken the form that the consumers are expected to play a more active role in risk management.

Less coverage is not a coincidence- it is a design.

Learn more about Why Do Professionals Need Disability Insurance?

Why You Must Act As Your Own Risk Manager In 2026

In the modern world, every person should become his or her own risk manager. It is no longer realistic to wait until the insurers or government programs fill the gaps.

Being one’s own risk manager implies checking policies periodically, knowing the exposure, and acquiring more control over the income protection. Concentrating on reactive claims needs to be changed to proactive planning.

Risk management is no longer a choice; it is a personal duty.

Ontario’s Auto Insurance Rules And What They Mean For Accident Victims

The system of auto insurance in Ontario is still being modified under government control. Although statutory accident benefits are still active, there are differences between coverage provisions that apply to accident victims.

The non-earners, caregivers, and dependents are supported by limited non-earner benefits, caregiver benefits, and funeral benefits when tragedy strikes. The supports are there, though they are rarely indicative of the reality of financial demands.

Ontario government policy gives shape, but not assurance.

Why Non-Earners Face Even Greater Financial Risk

The non-earners usually perceive that they are not vulnerable to the loss of income. That assumption is flawed. The replacement benefits are limited in the income, and the lost income is not just restricted to wages.

Household contribution, care giving, and long-term dependency are all financial. In case these roles are disrupted through injury, benefits are not sufficient. It is not only earners that are not spared by income disruption.

Disability Insurance should be looked at through the prism of the family.

Medical Rehabilitation And Attendant Care Costs Add Up Fast

Attendant care and medical rehabilitation costs are rapidly increasing in the case of severe injury. Rehabilitation and attendant care services tend to go beyond the normal limits in months.

Attendant care benefits will support, but not necessarily adequately. Health care demands, recovery schedules, and long-term assistance put financial and family burdens.

The care expenditure in the future is among the least estimated risks after an accident.

Group Benefits Are Not A Complete Safety Net

Group benefits are beneficial, but are predetermined to be short-term. Exposure is caused by coverage limits, employment dependency, and restraining definitions.

The use of group benefits only makes individuals susceptible in case of a career change or prolonged recuperation.

The protection is not replaced by group plans.

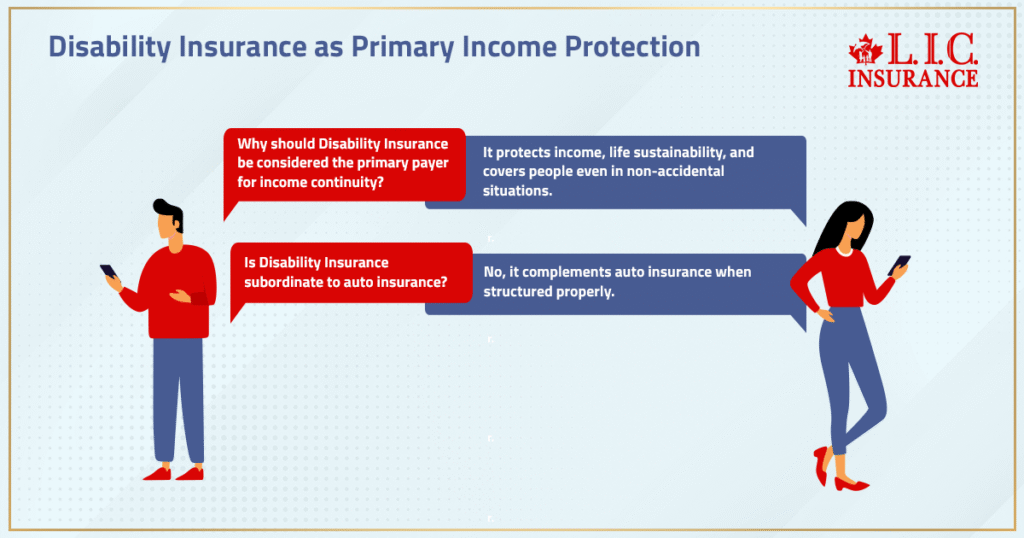

Disability Insurance As The True First Payer For Income Protection

Disability Insurance ought to be considered as the primary payer in terms of income continuity. It shields revenues, life sustainability, and people are still covered even in instances that are not accidental.

Disability Insurance is not subordinate to auto insurance, but rather it is complementary to it when structured properly.

What Ontario Drivers Need To Do Before The Next Claim Happens

Weaknesses to be found should not be determined after a claim is made. Having an experienced broker enables the client to know the limitations of insurers, the areas of gaps, and to match the coverage with the actual risk.

Insurance review has ceased to be a choice. It is essential.

Final Perspective: Disability Insurance Isn’t Optional Anymore

Disability Insurance Plans in Canada have shifted their position from optional planning devices to a level of financial protection. Disability Insurance deals with the facts that are not covered under auto insurance. The cost of Disability Insurance is based on risk- but the cost of being uncovered is even greater.

Canadians are advised to find a Disability Insurance quote online before the next accident compels them to make a choice and take control over their protection plan.

Waiting until 2026 is the most costly of all the options.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Auto insurance does not react to a long-term income disruption. The Canadian Disability Insurance Plans are concerned with the income coverage, which cannot be maintained under an auto policy. The coverage of Disability Insurance helps to maintain the financial position when the benefits of the accidents are exhausted. The difference is paramount with the changing system in Ontario.

The cost of being underinsured is unpredictable; the cost of Disability Insurance is predictable. Injured individuals tend to experience gaps in income, health care, and future care expenditure beyond the basic benefits. Managed risk is represented by premiums, and exposure by the uncovered loss. Such a difference is significant even after a claim is made.

Yes, the Disability Insurance does not substitute; it complements optional benefits. Whereas optional coverage involves coverage of accident-specific expenses, Disability Insurance compensates for income replacement despite the mode of how the injury is sustained. This is a stratified system that provides consumer control. It also makes the use of claims less dependent.

Non earners still contribute economic value through caregiving and household support. When injury interrupts that role, limited benefits may apply. Disability Insurance helps protect families from indirect income loss. A broker’s role is to identify those overlooked risks.

Most claims do not require a personal injury lawyer. Legal involvement typically arises when tort claims, serious injury, or fault disputes exist. Proper insurance planning reduces dependence on litigation. Coverage should stabilize finances, not escalate conflict.

It is necessary to review policies every few years, particularly with the emerging new rules. Coverage needs are influenced by changes in income, family structure, or work. The Ontario drivers enjoy the proactive readjustment as opposed to the reactive claims. To begin with, the process of being an own risk manager is through regular reviews.

Group benefits do not provide assurance; they just provide convenience. It can be terminated with employment or cut benefits prematurely. Disability Insurance is continuous even in the case of a change of occupation. Such consistency is important in a fluid insurance system.

Prior to an accident, there is a compelling urgency. By getting a Disability Insurance quote online, one will have time to study the coverage, costs, and terms of the insurers at ease. Timely planning enhances results. Waiting limits options.

Sources and Further Reading

Official Government & Regulatory Sources

- Government of Canada – Disability Insurance Overview

A detailed explanation of what Disability Insurance is, how it replaces income, and key considerations when buying coverage. Canada - Ontario Regulation 34/10 – Statutory Accident Benefits

Official regulation outlining minimum statutory accident benefits all Ontario drivers must carry under auto policies. Ontario

Industry & Insurance Association Publications

- CLHIA & Industry Briefs on Disability Income Insurance Plans

Research on disability income insurance plans in Canada and how they interact with public programs. House of Commons of Canada

Accident Benefits & Auto Insurance Information

- Accident Benefits in Ontario – Coverage and Limits

Breakdown of accident benefits coverage, including income replacement and other benefits provided under Ontario auto policies. ThinkInsure - How to Apply for Accident Benefits in Ontario

Practical guidance on claiming provincial accident benefits after a motor vehicle accident. Howie Sacks & Henry LLP

Statistical & Social Context

- Statistics Canada – Disability in Canada (CSD Data)

National disability prevalence statistics show how many Canadians are affected by disability. Wikipedia

Additional Relevant Supports

Key Takeaways

- Disability Insurance Plans in Canada are no longer optional in 2026. Changes across Ontario’s system mean individuals must protect income beyond what auto insurance and accident benefits provide.

- Disability Insurance coverage fills critical gaps left by auto insurance. Statutory accident benefits remain mandatory, but they were never designed to replace long-term income or support extended recovery.

- Disability Insurance costs are predictable; uncovered risk is not. Premiums are manageable compared to the financial impact of lost income, medical rehabilitation, and future care costs after serious injury.

- Optional benefits help, but they don’t solve the full problem. Declining optional coverage often leads to being underinsured, especially when income replacement limits are reached.

- Auto insurance is not income protection. Ontario’s auto insurance system focuses on accident response, not sustained financial stability, making Disability Insurance the true first payer for income.

- Non-earners and families face unique exposure. Caregiver roles, household contribution, and indirect income loss are rarely addressed adequately without disability coverage.

- Relying on litigation is risky and slow. Proper planning reduces dependence on tort claims and personal injury lawyer involvement after serious accidents.

- Requesting a Disability Insurance quote online before an accident matters. Early planning gives consumers more control, better coverage alignment, and long-term financial security.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- Disability Insurance Isn’t Optional In 2026—Here’s Why

- Why Accident Benefits Still Matter More Than Most People Realize

- The Hidden Gaps Inside Optional Benefits Most Drivers Skip

- When A Personal Injury Lawyer Becomes Part Of The Equation

- Auto Insurance Isn’t Disability Insurance—And Never Was

- How Insurance Companies Are Reshaping The Current System

- Why You Must Act As Your Own Risk Manager In 2026

- Ontario’s Auto Insurance Rules And What They Mean For Accident Victims

- Why Non-Earners Face Even Greater Financial Risk

- Medical Rehabilitation And Attendant Care Costs Add Up Fast

- Group Benefits Are Not A Complete Safety Net

- Disability Insurance As The True First Payer For Income Protection

- What Ontario Drivers Need To Do Before The Next Claim Happens

- Final Perspective: Disability Insurance Isn’t Optional Anymore

Sign-in to CanadianLIC

Verify OTP