- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Is Visitor Insurance to Canada Refundable? What You Should Know

By Pushpinder Puri

CEO & Founder

- 12 min read

- May 6th, 2026

SUMMARY

Visitor Insurance refund Canada rules explained for visitors to Canada, including when a full refund or partial refund applies, Canada Visitor Insurance cost factors, Super Visa Insurance cases, pre-existing medical conditions, and how Visitor Insurance brokers handle refund requests using Visitor Insurance quotes online, and the best Visitor Insurance Plans Canada.

Introduction

All these millions of visitors to Canada have one common issue every year: medical risk. The figures released by the Immigration, Refugees and Citizenship Canada show that Canada accepted over 22 million temporary immigrants and visitors in a single year, which comprises the tourists, parents, and super visa applicants. What they fail to realize until they find themselves in a critical situation is that one medical emergency is going to cost them between $5,000 and $15,000 a day, even if they are not a resident, as far as the Canadian Institute of Health Information reports.

That’s why visitor to Canada insurance is no longer optional. But once the policy is purchased, a second question always follows:

Is Visitor Insurance to Canada refundable?

We do refunds on a daily basis – visa refusals, travel arrangements, premature returns, and misconceptions in coverage. The short answer? Yes, Visitor Insurance may be refundable, but only in case of very certain conditions. The long answer is just what you are about to read.

Understanding Canada Insurance And Visitor Insurance Refund Basics

The insurance in Canada is not similar to that in most other countries. There is a canadian insurance company that provides Visitor Insurance, and its underwriting and regulatory policies are strict. As soon as the insurance policy is taken up, the risk is transferred to the insurer, even in the case of no medical treatment.

This is why refund rules depend on:

- The purchase date

- The policy’s effective date

- Whether a medical emergency occurred

- Whether an insurance claim was initiated

The majority of the insurance companies permit refunding under the condition that no claims or emergency medical costs were incurred in the course of the termination.

It is our mandate as Visitor Insurance brokers to clarify these rules before you buy insurance, not after you are denied a refund.

How A Visitor Insurance Policy Works In Canada

A standard Visitor Insurance or medical insurance plan is designed to protect visitors to Canada from high emergency medical costs. Coverage typically includes:

- Hospitalization

- Emergency medical treatment

- Diagnostic testing

- Prescription medications

- Ambulance services

The coverage period begins on the effective date listed in the actual policy documents. From that moment onward, the insurer assumes financial risk, which is why refund eligibility becomes limited.

Every insurance policy clearly outlines:

- Coverage limits

- Waiting period clauses

- Pre-existing medical condition rules

- Refund policies

Ignoring the policy wording is the fastest way to lose refund eligibility.

Canada Travel Insurance And Refund Eligibility Scenarios

Canada Travel Insurance refunds depend heavily on your travel plans. Common refundable situations include:

- Visa denial before travel

- Trip cancellation prior to the effective date

- Delayed or cancelled travel dates

When the policy is, however, active and you enter Canada, then there is a huge difference in eligibility for the refunds, even when no side trips are made, and the same coverage is not availed.

The Travel Insurance is charged on the basis of risk exposure rather than on usage.

When Visitor Insurance Refund Canada Is Allowed

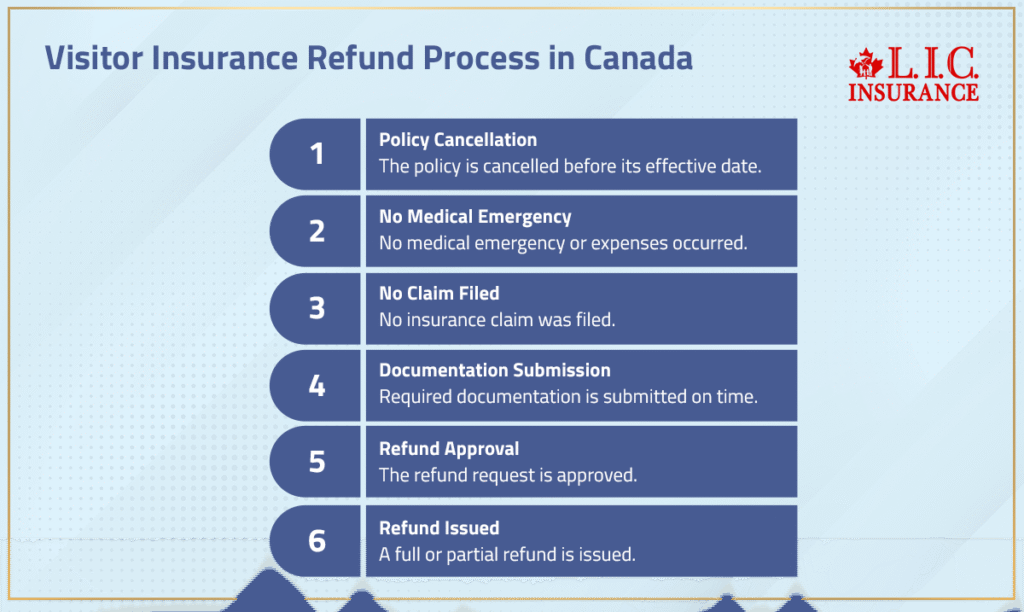

A Visitor Insurance refund Canada request is usually approved under these conditions:

- The policy is cancelled before the effective date

- No medical emergency or medical expenses occurred

- No insurance claim was filed

- Required documentation is submitted on time

You could get a full refund or a partial refund, less an administration fee or processing fees, depending upon the insurer.

There can also be some policies under which a refund of the premium may be given to the visitor, in case he leaves Canada earlier than indicated in the return date.

Refund Rules For Visa Denial And Visa Rejection Letter

Visa denial is one of the most common refund scenarios we handle. If Immigration Canada refuses a visa application, most insurance providers require:

- A formal visa rejection letter

- A refund request submitted before the policy’s effective date

In these cases, Visitor Insurance brokers can usually secure a full refund, minus a small administrative fee.

Does Visitor Insurance Cover Emergency Medical Expenses Before Refunds Apply?

This is where confusion often arises.

Once a policy begins to cover emergency medical expenses, refunds are almost always void. Even a single:

- Medical emergency visit

- Emergency medical consultation

- Diagnostic test

…counts as risk utilization.

Emergency medical coverage exists to protect against unexpected medical expenses, not to function as a refundable reservation.

Medical Expenses And Refund Limits After A Claim

If any medical expenses are incurred, refund eligibility drops to zero. This includes:

- Hospital admission

- Emergency medical treatment

- Prescription drugs

- Emergency medical costs are tied to severe symptoms

An insurance claim, even if later denied, typically disqualifies refunds entirely.

Medical Insurance Refunds And Pre-Existing Medical Conditions

Refunds become more complex when pre-existing medical conditions are involved. Many policies include:

- Medical questionnaires

- Waiting period clauses

- Stability requirements

In case a medical condition already existed before coverage and the symptoms manifest, the insurer not only might deny the claim, but also may deny a refund.

That is why the pre-existing condition insurance of tourists should be selected thoughtfully. Inaccurate disclosure or misconception concerning the presence of serious symptoms will cancel coverage and refunds.

Health Insurance Refunds For Visitors To Canada

Visitor health insurance often covers:

- Emergency medical

- Prescription medications

- Essential coverage during short stays

However, health insurance refunds follow the same rules:

- No claims

- No medical treatment

- Cancellation before the effective date

Once prescription medications are dispensed under the policy, refunds are typically disallowed.

Super Visa Insurance Refund Rules For Parents And Grandparents

Super Visa Insurance carries stricter rules. Since super visa applicants must show one full year of coverage upfront, refund eligibility usually applies only if:

- The super visa was refused

- The applicant never enters Canada

A Super Visa Insurance Policy cannot be refunded after initiation, even when the parent or grandparent visits for a few weeks.

That is why it is much more important to choose the most suitable Visitor Insurance for a parent rather than the price.

Emergency Medical Coverage Under Basic Plan Vs Enhanced Plan

A basic plan typically includes lower coverage limits and fewer refund options. An enhanced plan may offer:

- Higher emergency medical coverage

- More flexible early return refunds

- Better handling of emergency medical expenses

However, neither plan guarantees refunds after claims.

Early Return Refunds And Unused Portion Of Coverage

Some insurers allow early return refunds for the unused portion of coverage if:

- No claims occurred

- The visitor leaves Canada permanently

- Proof of departure is submitted

Refunds apply only to the unused portion, not the full premium.

Administration Fees And Processing Fees You Should Expect

Most refund policies include:

- An administration fee

- Processing fees are deducted from the refund

These fees cover underwriting, documentation review, and policy issuance costs.

What Visitor Insurance Brokers Look For Before Approving A Refund Request

As Visitor Insurance brokers, we review:

- Purchase date vs effective date

- Claims history

- Required documentation

- Policy wording compliance

Most insurance providers follow identical refund logic — but broker advocacy can make a real difference in edge cases.

Who Is Not Eligible For Visitor Insurance Refunds

Refunds are usually denied if:

- The visitor becomes a permanent resident

- The insured is a Canadian citizen

- A self-inflicted injury occurs

- Coverage was misused or misrepresented

Visitor Insurance is designed strictly for visitors to Canada, not permanent residence transitions.

Financial Or Legal Advice Disclaimer

This content does not constitute financial or legal advice. Always review actual policy documents before making decisions.

Why Choosing The Best Visitor Insurance Plans Canada Matters

Choosing the best Visitor Insurance Plans in Canada isn’t about chasing the lowest Canada Visitor Insurance cost. It’s about:

- Refund clarity

- Emergency medical coverage reliability

- Honest handling of pre-existing medical conditions

- Transparent policy wording

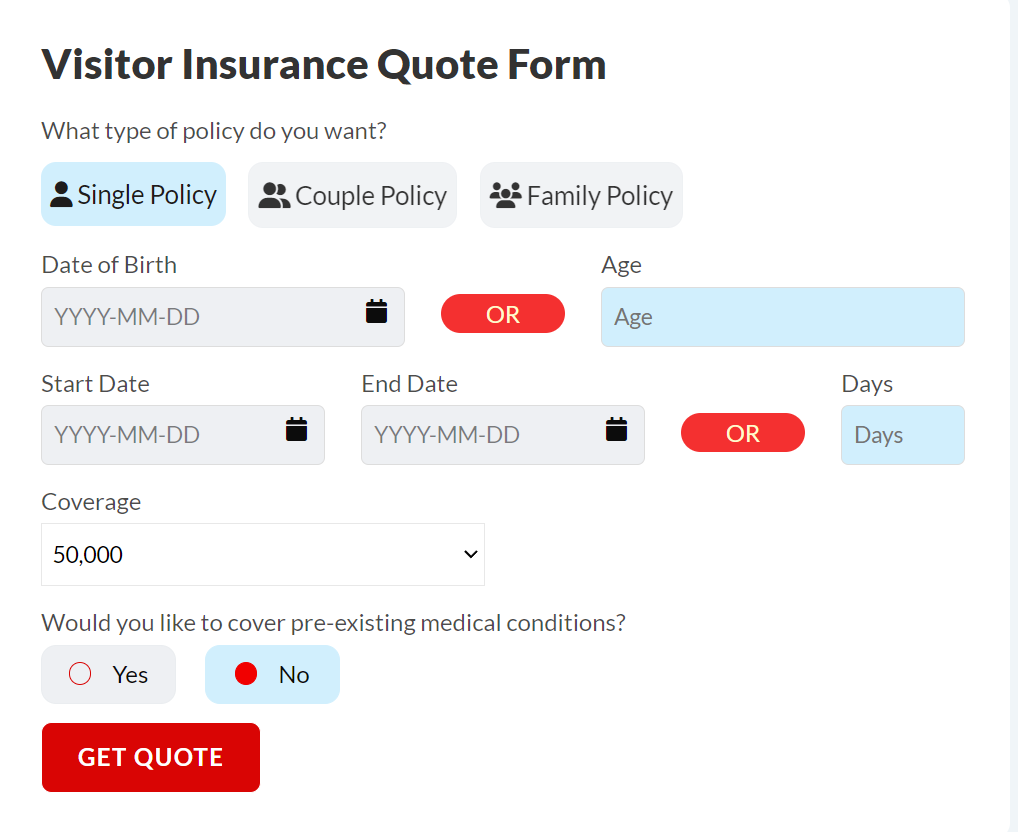

We guide visitors, families, and super visa applicants through Visitor Insurance quotes online with one priority: no surprises when it matters most.

Because when something goes wrong, clarity beats cheap every single time.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Yes, in limited cases. Most insurance companies can make full refunds after a refund request has been made, provided that the travel plans are changed before the start of the policy. Refunds to be received after coverage begins are ordinarily based on unused coverage and evidence of cancellation. Nevertheless, refund policies should always be checked in the insurance policy.

Not automatically. Refunds will also be available even in the absence of medical treatment or emergency medical costs, depending on whether the period of coverage commenced. Active coverage is considered a risk assumed by many insurance companies, whether used or not. Rules of Visitor Insurance refund Canada are based on time, rather than the results.

It can. In case a medical condition is revealed via the medical questionnaire and no symptoms are reported, the refund regulations remain general. Severe symptoms or emergency medical use involving pre-existing medical conditions normally cancel the eligibility for a refund, though. Wording of policies is more important than assumptions.

Yes. Super Visa Insurance policies have stricter rules of refund since the super visa applicants are obligated to insurance coverage. Refund is normally considered in case there is a rejection of a visa prior to the actual start of the policy. Refunds are hardly granted once the parents or grandparents enter Canada.

Absolutely. The Visitor Insurance brokers liaise directly with the insurance company to confirm the required documentation, purchase date, and cover status. Brokers do not have the authority to defy the policy rules; however, good management of them can be timely and save avoidable processing costs. This is where experience does count.

In most cases, yes. A small administrative fee or processing fees may be charged even in the case of a full refund. The fees included underwriting and issuing of policies billed by the canadian insurance company. This precise figure is enumerated in the actual policy documents.

Sometimes. In case the visitors to Canada depart earlier than the planned date of returning and they fail to claim the insurance, the insurance companies will reimburse the remaining amount. Evidence of departure and travel dates is needed. Early refund of the money will not occur after emergency medical coverage has been incurred.

Only in case of side trips which are under Canada coverage and acceptable terms of Travel Insurance. Even when the main visit was brief, medical emergency claims on side trips may affect the eligibility for the refund. It is a good idea to always ensure that you confirm side trip limits before you buy insurance, especially if you plan to stay longer.

Sources and Further Reading

Visitor Insurance, Refunds, And Coverage Rules

- Government of Canada – Travel Insurance Information

https://travel.gc.ca/travelling/documents/travel-insurance - Financial Consumer Agency of Canada – Insurance Basics & Consumer Rights

https://www.canada.ca/en/financial-consumer-agency/services/insurance.html - Canadian Life and Health Insurance Association – Travel & Health Insurance Explained

https://www.clhia.ca/consumers/travel-insurance

Medical Costs And Emergency Care For Visitors To Canada

- Canadian Institute for Health Information – Hospital Costs & Emergency Care Data

https://www.cihi.ca/en/health-system-costs - Ontario Ministry of Health – Health Coverage For Non-Residents

https://www.ontario.ca/page/ohip-coverage-while-outside-canada

Super Visa Insurance And Immigration Rules

- Immigration, Refugees and Citizenship Canada – Super Visa Requirements

https://www.canada.ca/en/immigration-refugees-citizenship/services/visit-canada/super-visa.html - IRCC – Temporary Resident Visa Refusals And Reapplications

https://www.canada.ca/en/immigration-refugees-citizenship/services/application/application-status.html

Consumer Protection And Insurance Policy Guidance

- Financial Consumer Agency of Canada – Understanding Insurance Policies

https://www.canada.ca/en/financial-consumer-agency/services/insurance/understanding.html - Government of Canada – Consumer Protection In Financial Services

https://www.canada.ca/en/financial-consumer-agency.html

Border Entry, Exit, And Travel Dates (Refund Validation)

- Canada Border Services Agency – Entry & Exit Information

https://www.cbsa-asfc.gc.ca/travel-voyage/menu-eng.html

Key Takeaways

- Visitor Insurance to Canada can be refundable, but refunds depend strictly on timing, policy status, and whether emergency medical coverage was used.

- A full refund is usually possible only before the policy’s effective date, often in cases like visa denial, supported by a visa rejection letter.

- Once the insurance policy starts and any medical emergency or medical expenses occur, refund eligibility is typically lost, even if costs are minimal.

- Partial refund options may apply for early return refunds, limited to the unused portion of coverage and subject to administration or processing fees.

- Visitor Insurance with pre-existing conditions requires extra caution, as undisclosed or unstable medical conditions can affect both claims and refunds.

- Super Visa Insurance follows stricter refund rules, with limited flexibility once parents or grandparents enter Canada.

- The Canada Visitor Insurance cost should never be the only decision factor; refund policies, coverage limits, and emergency medical expenses matter more long-term.

- Working with experienced Visitor Insurance brokers helps prevent refund issues, ensures correct documentation, and avoids misunderstandings hidden in policy wording.

- Always review the actual policy documents, including waiting periods, coverage periods, and refund policies, before you purchase insurance.

Your Feedback Is Very Important To Us

We value real experiences.

Your responses help improve clarity around Visitor Insurance refund rules for visitors to Canada.

This questionnaire does not provide financial or legal advice.

IN THIS ARTICLE

- Is Visitor Insurance to Canada Refundable? What You Should Know

- Understanding Canada Insurance And Visitor Insurance Refund Basics

- How A Visitor Insurance Policy Works In Canada

- Canada Travel Insurance And Refund Eligibility Scenarios

- When Visitor Insurance Refund Canada Is Allowed

- Refund Rules For Visa Denial And Visa Rejection Letter

- Does Visitor Insurance Cover Emergency Medical Expenses Before Refunds Apply?

- Medical Expenses And Refund Limits After A Claim

- Medical Insurance Refunds And Pre-Existing Medical Conditions

- Health Insurance Refunds For Visitors To Canada

- Super Visa Insurance Refund Rules For Parents And Grandparents

- Emergency Medical Coverage Under Basic Plan Vs Enhanced Plan

- Early Return Refunds And Unused Portion Of Coverage

- Administration Fees And Processing Fees You Should Expect

- What Visitor Insurance Brokers Look For Before Approving A Refund Request

- Who Is Not Eligible For Visitor Insurance Refunds

- Why Choosing The Best Visitor Insurance Plans Canada Matters

Sign-in to CanadianLIC

Verify OTP