- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Understanding Group Benefits Plans in Canada (2026): Coverage, Costs, and Employer Advantages Explained

By Pushpinder Puri

CEO & Founder

- 15 min read

- April 2nd, 2026

SUMMARY

Group Insurance Plans in Canada provide essential coverage, control costs, and support both employers and employees. It covers Group Insurance Coverage options, employer advantages, Group Insurance costs in Canada, and the value of offering employee benefits plans. It also highlights retirement savings plans, healthcare spending accounts, and how Canadian LIC helps businesses get the right Group Insurance quote online.

Introduction

Every successful Canadian company has one thing in common: they look after their people. Behind the success of every highly productive, dedicated workforce is a sturdy benefits structure that keeps workers safe and satisfied. It’s based on the Group Insurance Plan, a commitment from employers to look after the financial, physical and emotional health of their team.

According to CLHIA’s latest data released, approximately 24 million Canadians have some form of employer-sponsored group insurance coverage, including health, dental, disability, or life insurance. As the labour market continues to change in 2026, companies providing excellent group benefits will become distinguishable — not merely as employers, but as progressive partners in their employees’ success.

We’ve seen firsthand the difference the right benefit package can make to a working culture. From small startups to large corporations, hundreds of thousands of employers across Canada are coming to understand that investing in the protection and wellness of their workforces just makes good business sense.

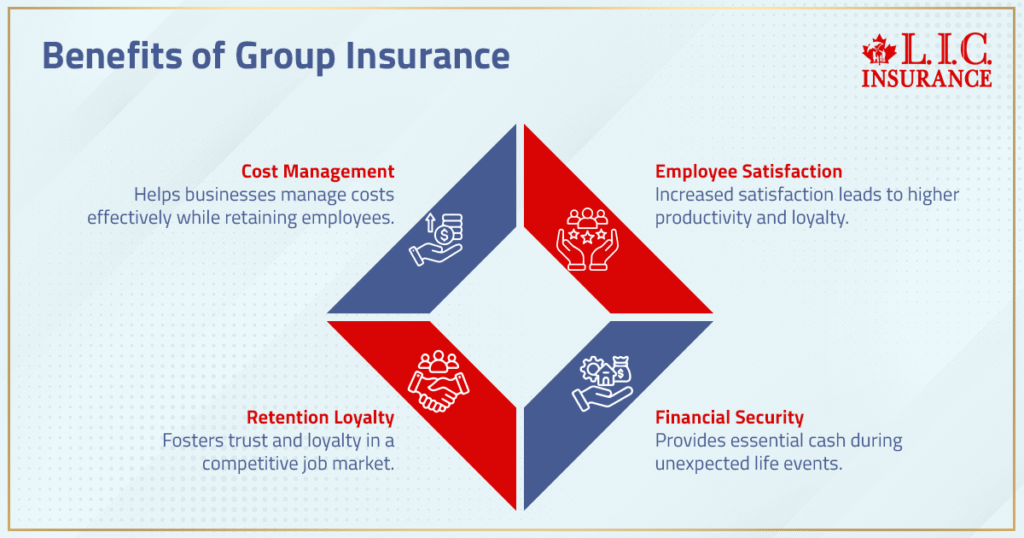

Why Group Insurance Plans Matter For Canadian Employers And Employees

The well-being of workers is now a corporate currency. Retention improves, performance goes through the roof and turnover costs plummet when employees perceive that they are valued. Research published by the Conference Board of Canada in recent years indicates that structured employee benefits programs are consistently linked to higher employee satisfaction and materially improved retention outcomes.

Group Insurance for employees is more than just a basic benefit — it provides financial security when life twists unexpectedly. In times of sickness or when income dries up, these plans provide families with essential cash that helps them stay afloat. For workers, this coverage fosters loyalty and cements trust at a time when industries are competing heavily for skilled labour.

We specialize in creating custom employee benefits packages that achieve two things: retain employees and effectively manage costs for the business. When an employee feels safe, they remain loyal — and that’s how organizations create strong, enduring teams.

What’s Included In A Typical Employee Benefits Plan

A well-rounded Employee Benefits Plan in Canada usually includes several layers of protection. The Group Insurance Coverage typically extends beyond simple medical coverage to form a complete benefits package.

- Health Insurance – Covers hospital care, prescription drugs, and extended health care beyond what Government Health Insurance provides.

- Dental Insurance – Preventive and restorative Dental Coverage, including exams, fillings, crowns, and major dental plans.

- Vision Insurance – Eye exams, frames, and lenses to promote long-term eye health.

- Life Insurance – Provides a tax-free Life Insurance Coverage amount to families in case of death.

- Disability Insurance – Short-term and Long-term Disability Insurance that replaces lost income during illness or injury.

- Critical Illness Insurance – Provides a lump-sum benefit upon diagnosis of a major illness, offering crucial financial security.

- Healthcare Spending Accounts (HSA) – Flexible, tax-advantaged options for medical, dental, or vision expenses.

- Employee Assistance Programs (EAPs) – Confidential counselling and mental health support for emotional, legal, or financial concerns.

- Wellness Programs – Corporate health initiatives, gym memberships, and preventive care programs that enhance overall well-being.

Each basic plan can be customized to reflect the unique structure of the business. We help employers design Group Health benefits that blend mandatory employee benefits with optional employee benefits, ensuring coverage for both business efficiency and employee happiness.

The True Cost Of Group Insurance Plans In Canada

But many employers are loath to offer expanded coverage because they believe the cost of Group Insurance in Canada is simply too high. In reality, though, these costs are much more manageable — and tax-efficient — than many people realize.

Group Insurance Plan premiums in Canada are generally cost-shared between an employer and its employees. In the majority of industries, the employers cover between 50 and 75% of their total premiums. In most cases, employer-paid group insurance premiums are treated as a deductible business expense, subject to CRA rules around benefit type and plan structure (Canada Revenue Agency guidance, 2025).

The number can vary based on factors like the average age of employees, claim history and which benefits are chosen. Firms can contact us online to achieve a Group Insurance quote against leading insurers and see premium variations in seconds.

What few people realize is that providing a benefits plan saves money in the long run. Healthier employees are less absent, more engaged and more loyal. “You cannot just treat it as a line item — you have to look at this as your growth strategy.

Integrating Health And Dental Insurance Within Employee Benefits Packages

One of the most commonly forgotten types of Group Coverage is Disability Insurance. Statistics Canada data show that a significant proportion of working Canadians will experience a disability lasting several months or longer at some point during their working lives.

Employers can offer that flexibility with healthcare spending accounts, or health spending accounts, giving employees control over where to spend their money — whether on prescription drugs, physiotherapy or orthodontics.

We help employers deliver physical and emotional well-being through traditional health plans integrated with wellness programs, disease management, and mental and behavioural health solutions. The end result: Increased productivity, lower stress and real concern throughout the workplace.

Adding Disability Insurance And Critical Illness Coverage To Strengthen Protection

One of the most commonly forgotten types of group coverage is disability insurance. However, Statistics Canada 2025 predicts that one in six working Canadians will have a disability lasting longer than three months at some point in their working life.

Short-term disability insurance pays for weeks or months of income, and long-term disability insurance provides ongoing support for an extended illness or injury. Employers who offer such protection reduce our workplace anxiety and save their employees from financial ruin.

The plan is further enhanced with critical illness cover. Those diagnosed with serious infirmities, including cancer, stroke or heart disease, receive lump-sum benefits, allowing them to concentrate on rehabilitation rather than lost income.

Our consultants frequently work these coverages as a natural fit to an employee benefits package, making coverage affordable and the value of the benefit worthwhile. When you’re sick, it doesn’t bring a benefit; it is literally bringing help to your life.

Retirement Savings Plans And Pension Contributions For The Future

The true comprehensive benefit plan doesn’t stop at health coverage. It looks ahead. Retirement savings plans (RSPs) and pension contributions are key to employee financial wellness in Canada.

Employers have the option of offering pension plans, group RRSPs and deferred profit-sharing plans that are on top of regular Canada Pension Plan (CPP) and Quebec Pension Plans (QPP) contributions. Federal labour and retirement studies consistently show that employers offering formal retirement savings or pension programs experience meaningfully stronger employee retention and long-term workforce stability.

We want business to be a mix of protection with growth.” When we align group health care plans with retirement savings plans, we create a stronger bridge between the protection of income today and having enough when we want to stop working for it. It’s what modern benefits design does for lifelong financial security.

Healthcare Spending Accounts And Supplemental Benefits: Customizing Flexibility

Every business has unique needs. Healthcare spending accounts and supplemental benefits can also give employers the flexibility to customize coverage for different teams. When structured as a qualifying Private Health Services Plan (PHSP), healthcare spending accounts are generally deductible for employers and non-taxable to employees under CRA guidelines (CLHIA and CRA guidance, 2025).

For corporations looking for the tax advantages of HSAs, in particular, they’re especially attractive — they are deductible to an employer and not considered to be taxable income for employees (Source: Canadian Life and Health Insurance Association 2025).

We make it easier for companies to include optional benefits and voluntary benefits as part of their employee benefit packages, enabling everyone – executives to entry-level employees – to get personalized care options. And it’s a method that enhances satisfaction without overstretching budgets.

Employment Insurance, Parental Benefits, And Legal Compliance

Private insurance covers a lot of the gaps; however, employers must also manage government-mandated benefits.

Employment Insurance provides baseline income protection mandated by the federal government, which can be strategically supplemented by private group disability and health benefits.

We create transparency and help employers make sense of how obligatory benefits intersect with private plans to avoid double coverage, taxability issues and compliance risk. Employers that provide government-sanctioned benefits in conjunction with private plans garner respect, confidence and gratitude from their employees.

Offering Employee Benefits That Improve Job Satisfaction And Well-Being

Providing employee benefits is no longer a courtesy — it’s an element of the brand promise. Today’s employers understand that well-being is associated with business performance. A company that invests in its people with ‘health and wellness’ programs, Employee Assistance Programs (EAP) or mental health awareness initiatives will simply engage and retain the best talent.

But receiving confidential support, counselling, or a gym membership has now become standard in progressive workplaces. Such programs alleviate burnout, promote positivity and enhance job satisfaction.

We partner with employers to design Employee Benefits Plans that are cost-effective and make an impact. For when employees thrive, companies prosper.

Additional Benefits And Optional Enhancements For A Competitive Edge

In addition to the basics, some employers also offer accident insurance and/or inclusion of family members or self-employed individuals joining as part of a group association.

Optional benefits such as top-up life insurance, travel medical coverage, or dental plans enable companies to craft tiered packages based on role or tenure. These improvements not only create value but also serve to keep top talent in robust markets.

We work with clients to embrace these opportunities while keeping costs low — balancing coverage options with longevity.

How Canadian LIC Helps Employers Build Smarter Group Insurance Packages

It can be complicated to design the right benefits mix. That’s where we come in. We help plan sponsors at every stage — from market analysis to carrier comparison and compliance review.

We specialize in employer-sponsored plans, and we design an employee benefit plan for you that combines broad protection, cost effectiveness, enrichment of your workplace satisfaction and long-term stability.

Our technology-driven platforms enable employers to request instant online quotes for Group Insurance, handle renewals and easily measure benefit engagement. And by matching the varying needs of employees to intelligent funding models, we ensure every plan sponsor maximizes protection and performance.

Why An Effective Group Benefits Plan Is The Smartest Investment For 2026

But with a changing Canadian workforce, providing competitive group benefits is not a choice but rather a necessity. In a tightening labour market, employers with well-structured group benefits plans are consistently better positioned to attract talent, control turnover costs, and sustain productivity.

Enlightened employers will attract the best and brightest, increase productivity and reduce turnover costs. In a hot labour market, that’s priceless.

We help employers of all sizes measure and identify coverage gaps, negotiate more competitive rates, and bring the right services to ensure unparalleled protection for your employees. Whether it involves implementing a health spending account, increasing retirement savings or improving the disability insurance plan, we ensure your business is set up for 2026 and beyond.

Your staff is your most important investment. Let their benefits reflect it.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

Unlike single policies, where the risk is held with one individual or family, a group plan spreads the risk among employees and offers everybody access to better benefits at a lower premium. Costs are commonly shared by employers, allowing workers to receive important health and dental benefits without a serious monetary burden. It’s a win-win format that builds loyalty among workers and promotes wellness at the same time.

Even small companies can access affordable Employee Benefits Plans through brokers like Canadian LIC. We structure Group Insurance costs in Canada using tiered designs — balancing mandatory benefits and optional employee benefits to match the employer’s budget. This flexible approach helps small firms offer strong employee benefits without sacrificing profitability.

Retirement benefits are a long-term commitment to employee security from the employer’s perspective, and offering retirement savings and pension plans demonstrates your dedication to the future of your employees. Investing in a pension or retirement savings programme provides financial security and allows you to attract talent that is career-focused. For many workers, these forward-looking benefits are as important as today’s health or disability insurance coverage.

Yes — health care spending accounts and health spending accounts are the perfect fit for businesses with a mix of employee needs. They let employees determine how to spend funds — say, dental insurance vs. vision coverage vs. therapy — by offering flexibility that breeds satisfaction. We have built HSAs so that they control costs for employers and provide healthier outcomes to employees.

Employment Insurance is a kind of private plan adjunct, offering floor income protection in case of layoffs or leaves. When you add EI to group health benefits and extended health care, that makes full-spectrum coverage for every worker. We assist employers in combining government-required benefits with employee Group Insurance in the private sector, so you maintain symmetrical compliance.

Companies are enhancing plans with optional benefits like Accident Insurance, travel coverage, and Critical Illness Insurance for greater appeal. These additional benefits not only protect families but also strengthen morale and retention. Employers who invest in these options stand out as forward-thinking and genuinely employee-first.

Employee Assistance Programs provide confidential support for stress, finances, or family challenges. They’re crucial for maintaining morale and mental balance alongside Health Insurance and wellness programs. When employees feel heard and supported, their focus and job satisfaction rise — creating a more resilient organization overall.

Getting a Group Insurance quote online through Canadian LIC saves time while providing transparent, multi-carrier comparisons. Our experts analyze your employee benefits package, suggest optimized Group Insurance Coverage, and ensure legal compliance with federal government standards. It’s the easiest way to modernize your benefits strategy heading into 2026.

Sources and Further Reading

- Statistics Canada — Labour Force Survey (overview + releases)

https://www.statcan.gc.ca/en/survey/household/3701

Latest monthly release (example): https://www150.statcan.gc.ca/n1/daily-quotidien/251107/dq251107a-eng.htm - Government of Canada — Employment Insurance (EI) Benefits

https://www.canada.ca/en/services/benefits/ei.html

EI Regular Benefits: https://www.canada.ca/en/services/benefits/ei/ei-regular-benefit.html - CRA — Employers’ Guide: Taxable Benefits and Allowances (T4130)

https://www.canada.ca/en/revenue-agency/services/forms-publications/publications/t4130/employers-guide-taxable-benefits-allowances.html - FSRA (Ontario) — Pensions (Industry Resources)

https://www.fsrao.ca/industry/pensions

Administrator Roles & Responsibilities: https://www.fsrao.ca/industry/pensions/regulatory-framework/guidance-pensions/pension-plan-administrator-roles-and-responsibilities-1 - Health Canada — About the Canada Health Act https://www.canada.ca/en/health-canada/services/health-care-system/canada-health-care-system-medicare/canada-health-act.html

(Legal text) https://laws-lois.justice.gc.ca/eng/acts/c-6/page-1.html

Key Takeaways

- Group Insurance Plans in Canada provide cost-effective protection for employees, combining health, dental, disability, and life insurance into one powerful package.

- Employers benefit from lower turnover, higher productivity, and tax advantages when they offer a strong employee benefits plan with flexible Group Insurance Coverage.

- Including retirement savings plans, healthcare spending accounts, and disability insurance helps balance short-term protection with long-term financial stability.

- Modern Group Insurance for employees promotes wellness, compliance, and retention—making it one of the smartest business investments for 2026.

Feedback Questionnaire:

We’d love your input! Your feedback helps Canadian LIC create resources that genuinely support employers and professionals in understanding and optimizing group benefits.

Thank You!

Your answers help Canadian LIC continue improving how employers understand and manage Group Insurance Coverage, retirement savings plans, and employee benefits across Canada.

IN THIS ARTICLE

- Understanding Group Benefits Plans in Canada (2026): Coverage, Costs, and Employer Advantages Explained

- Why Group Insurance Plans Matter For Canadian Employers And Employees

- What’s Included In A Typical Employee Benefits Plan

- The True Cost Of Group Insurance Plans In Canada

- Integrating Health And Dental Insurance Within Employee Benefits Packages

- Adding Disability Insurance And Critical Illness Coverage To Strengthen Protection

- Retirement Savings Plans And Pension Contributions For The Future

- Healthcare Spending Accounts And Supplemental Benefits: Customizing Flexibility

- Employment Insurance, Parental Benefits, And Legal Compliance

- Offering Employee Benefits That Improve Job Satisfaction And Well-Being

- Additional Benefits And Optional Enhancements For A Competitive Edge

- How Canadian LIC Helps Employers Build Smarter Group Insurance Packages

- Why An Effective Group Benefits Plan Is The Smartest Investment For 2026

Sign-in to CanadianLIC

Verify OTP