- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Best Wealth Plan Canada RRSP Vs TFSA Vs Whole Life Plan

By Harpreet Puri

CEO & Founder

- 10 min read

- July 16, 2026

SUMMARY

A detailed comparison of RRSP vs TFSA Canada and Whole Life Insurance Canada, explaining how Tax-Free Savings Account Canada and Registered Retirement Savings Plan Canada support long-term wealth building in Canada. Covers Cash Value Life Insurance Canada, contribution room, tax advantages, and the best investment strategy in Canada, based on personal financial goals.

Introduction

How Canadians Build Long-Term Wealth Today

Wealth accumulation in Canada is not on one track anymore. The growing cost of living, new tax laws, and fluctuating economic cycles have brought a lot of change in terms of how Canadians handle wealth creation. As stated by the Canada Revenue Agency, many Canadians take advantage of the Registered Retirement Savings Plan and the Tax-Free Savings Account to deal with retirement savings as well as reduce their income tax liability. On the other hand, there have been increased requests for Whole Life Insurance in Canada.

For official guidelines, refer to:

- RRSP rules: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/RRSPs-related-plans.html

- TFSA rules: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account.html

The talks with our clients highlight one problem that comes up frequently. Namely, do we go for an RRSP or a TFSA Canada? Do we need to add Whole Life Insurance Plans in Canada to the picture? Well, as usual, everything is a bit more complicated. In Canada, the best way to invest will depend on your efficiency in managing taxes, securing assets, and defining your priorities.

Registered Retirement Savings Plan – Tax Deferral And Retirement Savings Strategy

The Registered Retirement Savings Plan Canada (RRSP) still stands as one of the best-known methods for RRSP planning. The greatest benefit offered by the RRSP is the postponement of taxation through the reduction of taxable income during periods of peak earning potential.

In making contributions to their RRSPs, contributors enjoy a deduction of such contributions from their tax bills for that particular year. In other words, RRSP contributions help in the reduction of taxable income, hence reducing the income tax payable during such a period. Those earning more money have much to benefit from this tax-saving arrangement.

Contributions to the RRSP are dependent on earnings. Every individual gets an allowance for the contributions made annually to the RRSP. This allowance depends on the earnings from the previous year. Any remaining allowance may be added to next year’s allowance for savings purposes.

Pension splitting and spousal plans are part of some of the programs that have particular withdrawal terms prescribed by the Canada Revenue Agency. Individuals can withdraw money from their plans temporarily without having any tax issues, but should repay it to save themselves from income tax in the future.

The RRSP is a tax-deferred program that involves postponing your taxes, allowing investments to grow, and paying taxes later when you make the withdrawal.

Contribution Room And Tax Benefits – Maximizing RRSP Efficiency

It is important to understand the workings of the contribution room to ensure that you fully enjoy the tax benefits of having an RRSP. The contribution room created in each year depends on the income earned for that particular period, while the unused contribution room carries over from year to year.

In such a case, you will be able to delay your contribution until you fall into a high tax bracket to enjoy the benefits associated with the tax deductions. The timing of RRSP contributions can help save tax.

By contributing during years of peak earnings when the tax bracket is high, you will save more money later when withdrawing the funds at a low tax bracket.

Nevertheless, over-contributing more than the maximum amount allowed may result in fines. It is important to keep track of annual contributions and unused contribution room to avoid any unnecessary fees.

The practical use of RRSPs is not only for savings but for effective tax management at various stages in one’s life. It is possible to defer taxes while building up assets in one’s retirement savings plan.

Retirement Savings And Investment Gains Inside RRSP

Investments made within an RRSP do not attract taxes until withdrawal. Investments that do not attract taxes are able to grow and accumulate much more quickly than those that earn profits subject to annual taxes.

Investors may choose mutual funds, exchange-traded funds, and other types of investments. Investors’ funds continue to earn money, even as they grow due to capital appreciation or earnings that have not yet been taxed.

Ultimately, RRSP accounts transform into a registered retirement income fund, after which investors start taking withdrawals. RRSP withdrawals become taxable income, meaning that investors need to pay taxes on money withdrawn from their account.

Withdrawing money from the fund needs to be planned properly. Making large withdrawals leads to higher brackets and higher income taxes in that year. Properly withdrawing funds means maximizing RRSP savings.

While there are some tax effects associated with RRSPs, they remain a powerful way of saving money in Canada.

Tax-Free Savings Account – Flexibility, And Tax Free Growth

A Tax-Free Savings Account Canada can be considered a unique kind of asset. Contributions to a TFSA cannot be written off against tax. Instead, the strength of such a kind of account is the fact that investments grow tax-free and withdrawals can be made without having to pay taxes.

The first difference between RRSPs and TFSAs concerns the use of after-tax money when making deposits into the latter. Once deposited, these funds become the subject of tax-free investment, generating dividends and capital gains which do not have to be paid for.

The amount that can be invested is regulated by the Canada Revenue Agency.

Probably one of the most obvious and strong advantages of a TFSA is that people can withdraw their money whenever they need. In addition, the money withdrawn remains tax-free and does not affect one’s total income; hence, it does not influence government benefits like OAS and GIS.

For instance, RRSP withdrawals are subject to income tax, while this does not apply to a TFSA

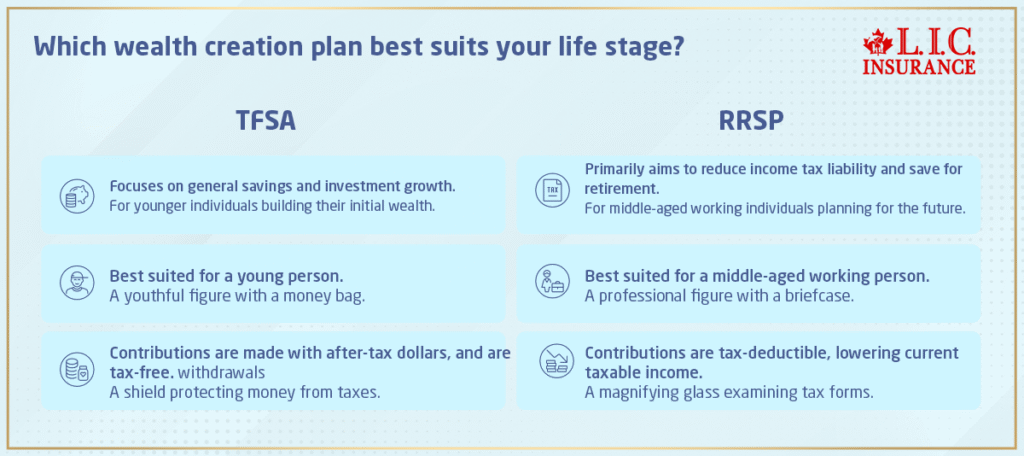

TFSA Vs RRSP – Which One Works Better For Your Personal Circumstances?

Comparing RRSP and TFSA can be based on personal needs rather than a general principle.

When it comes to people who pay high income tax rates, an RRSP is a better option because of its tax-deferral and tax deduction features that allow one to save some money at the moment.

As for those people who belong to the low tax bracket category, they will benefit from choosing a TFSA, as contributions will be made using the after-tax income, which means that future withdrawals will be free of any taxation.

It is worth considering the effect of either account on the benefits program. Withdrawals from RRSPs will lead to the growth of taxable income and might result in losing some benefits. The withdrawals from a TFSA are tax-exempt and thus won’t affect your benefits in any way.

If someone plans to spend considerable money on something urgent, a TFSA will be a more appropriate choice. As for people concerned only about their retirement income, an RRSP or RRSP/TFSA would be a reasonable option.

When you use Canadian LIC services, our specialists usually advise clients to find a balance between the two options.

RRSP First Strategy

An individual making an annual salary of $110,000 visited us to express his concern related to heavy income taxes. As he has a high marginal tax rate, emphasis was placed on the maximization of RRSP contributions.

Through the contribution of all possible contribution space and unused contribution space, there was a huge reduction in the taxable income level of the client. There is a huge tax advantage for him. In the RRSP Plan, money earns returns in a tax-deferred way.

TFSA First Strategy

An individual in his/her early years of work with irregular income and short-term goals needed more flexibility. The financial planner concentrated on TFSA rather than RRSP contributions.

In this way, money could be accumulated on a tax-deferred basis without being inaccessible for emergencies and the eventual down payment. Money withdrawn from TFSAs was not taxed or considered for any government benefits.

With growing income earned in the subsequent year, the strategy changed to include RRSP, thus illustrating how RRSP and TFSA are compatible in light of personal conditions.

Whole Life Insurance Canada – The Overlooked Wealth Strategy

While RRSP and TFSA remain the most talked-about options, Whole Life Insurance Canada adds a new perspective to the process of money management.

As opposed to other investment products, Whole Life Insurance Canada plans ensure both security and investments.

A certain percentage of the total premium pays into the assured cash value that increases with time.

The cash value of Whole Life Insurance Canada does not get affected by the ups and downs of the stock market but accumulates over time.

In case you need extra capital, you can always obtain a loan against your insurance plan or withdraw the accumulated cash value.

Whole Life Insurance can also be helpful for estate planning purposes since the death benefit will typically be paid out tax-free, thus avoiding capital gains or any probate complications when transferring the assets.

When Canadians want to know how to make money in Canada through insurance, Whole Life Insurance to ensure financial security in Canada is the right choice.

Whole Life Strategy For Long-Term Wealth

This client was a businessman earning a stable income with extra cash flows, who came to us with the objective of building wealth in Canada in a way that is more effective than the conventional retirement plans.

Post optimal utilization of both the RRSP and TFSA contribution limits, it was advised that he opt for a participating Whole Life Insurance Plan. He allocated an amount of $25,000 per year towards a participating Whole Life Insurance Plan.

In time, there arose a large pool of accumulated funds in the participating Whole Life Insurance Plan, which could then be used by the businessman for any purpose. It would help him grow wealth safely, without the risks involved in investments made in the market.

Further, the plan also provided a tax-free death benefit, thus helping achieve his objectives for effective estate planning and wealth distribution.

Investment Gains Vs Cash Value – RRSP, TFSA, And Whole Life Compared

Examining the differences among the three choices based on their respective investment gains would show how different each one can be from the others.

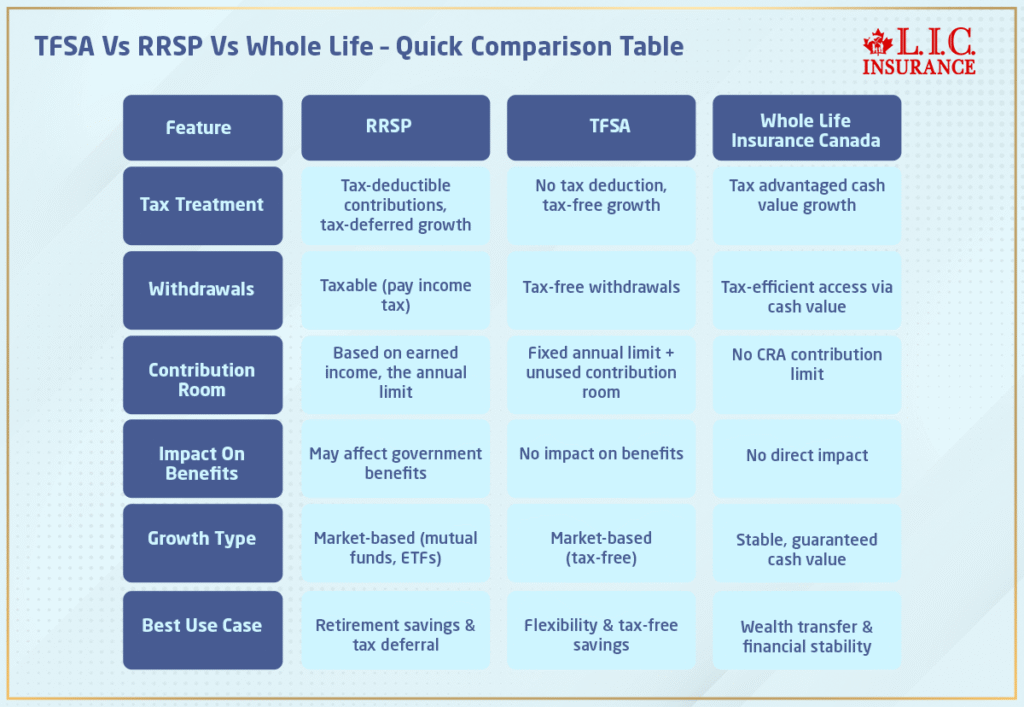

With RRSPs, tax-deferred investments can be made, with taxes paid after withdrawing money from these accounts. As for TFSAs, the investments can grow without being taxed, nor are the withdrawals subject to any taxes.

Unlike the other two choices, Whole Life Insurance allows investments to grow within the plan itself, although this growth may enjoy some tax benefits as well. Although the results are different from those of the market, such investments are more secure.

Because capital gains earned by non-registered investments have to be paid on an annual basis, they cannot be as tax-efficient as RRSPs and TFSAs.

Tax-efficient investments are thus crucial since the three choices differ when it comes to taxation.

Non-Registered Account And Alternative Investment Products

Non-registered accounts become useful when there is no more room left in an individual’s RRSP and TFSA accounts to make contributions.

Investments made within the non-registered account face taxation, unlike those made within the other two accounts. The interest generated is entirely taxed, whereas the gains made in the account benefit from tax relief.

This type of account is commonly used by individuals to make extra investments in financial institutions. The benefits of the non-registered account include flexibility, although it lacks the tax benefits of RRSPs and TFSAs.

Best Investment Strategy Canada – Combining RRSP, TFSA, and Whole Life

The optimal investment plan in Canada does not involve selecting only one product but using combinations of products according to financial objectives and life stage.

RRSPs help with tax deductions and retirement savings, while the TFSA has tax-free savings and flexible withdrawal features. The Whole Life Insurance Policy will add stability, security, and savings by accumulating cash value.

This strategy allows multiple levels of tax benefits since RRSP contributions reduce the taxable income, the TFSA investments earn money without taxation, and the Whole Life Insurance Policy also provides extra tax benefits.

The annual contribution plan in these products will ensure that the maximum contribution limit and tax credits are used effectively.

Is Whole Life Better Than RRSP In Canada? A Realistic Comparison

The issue of whether a whole life would be a better choice than an RRSP in Canada is one that will largely depend on personal circumstances.

High-earning people can benefit much from investing in their RRSP since this will immediately give them a tax deduction, but those who want guaranteed growth and inheritance aspects should invest in a Whole Life Insurance Policy.

A combination of RRSP and Whole Life Insurance Policies can be considered by businessmen, as this will help them plan their money wisely.

Those who are expecting to pay a lot of taxes when in retirement age will find TFSA or Whole Life Insurance better choices.

It all comes down to what people earn and what their intentions and plans are for the future.

TFSA Vs RRSP Vs Whole Life – Quick Comparison Table

Final Wealth Blueprint – Choosing The Right Plan Based On Your Needs

The most effective wealth creation plans are not based on a single financial instrument but rather on a carefully planned combination according to the situation.

For instance, a young person would prefer to put money into their TFSA account, while a middle-aged working person will be interested in RRSP, which would enable them to lower their income tax liability and save for retirement. An affluent person may want to consider a Whole Life Insurance Policy.

All of these options could be integrated by a financial planner to create a wealth plan in accordance with the individual’s goals for saving money in the future.

There is no doubt that a successful wealth plan in Canada does not involve making decisions like RRSP vs. TFSA in Canada or substituting them with Whole Life Insurance in Canada.

Written By: Harpreet Puri

Licensed Insurance Adviser | MDRT Qualifier

With over 14 years of experience in Life Insurance, wealth planning, and tax-efficient strategies for Canadians.

Disclaimer:

This content is for educational purposes only and does not constitute financial, tax, or legal advice. Individual financial decisions should be made based on personal circumstances in consultation with a qualified financial advisor. Tax rules referenced are based on guidelines from the Canada Revenue Agency and may change over time.

FAQs

In cases where there is variation in the income earned, it may be advisable to defer making RRSP contributions and retain room for contributions during high-income earning years. In low-income years, one may take advantage of the TFSA options to continue saving in a tax-free manner.

Yes, withdrawals from a TFSA will be tax-free, whereas the cash value in Whole Life Insurance will give an additional liquidity option. Using these two options ensures that individuals can make withdrawals without interfering with their long-term investments or creating tax liabilities.

Withdrawing RRSPs can lead to increased tax payments and hence reduce access to programs such as the Guaranteed Income Supplement and Old Age Security. Proper planning is essential since the amount withdrawn will determine the person’s eligibility for the benefits provided by the government.

This unused contribution room keeps growing over time and gives one the chance to make bigger contributions in the future. This is useful to people who suddenly receive more income and wish to make larger tax-deductible contributions.

After fully utilizing the contribution room in an RRSP or TFSA, a non-registered investment account is required to achieve further returns. Despite the annual payment of income taxes, this type of investment account allows more investment opportunities.

Whole Life Insurance Canada will be helpful to business people as a source of financial resources that can be taxed efficiently through the provision of cash value while maintaining liquidity within the firm. This option is unlike the RRSP, which is limited to one’s earnings.

When the tax rate is anticipated to increase in the future, then the advantage of tax-free withdrawal makes the TFSA very appealing. When the present marginal tax rate is high, the immediate tax break makes the RRSP advantageous.

Withdrawals from TFSA are frequently used for down payments owing to their flexible nature, whereas RRSP allows the use of funds in programs such as the Home Buyer’s Plan and Lifelong Learning Plan. The selection of either alternative depends on several factors.

A Whole Life Insurance Plan fits well where there are concerns about stability, savings, and inheritance. As opposed to returns from the stock market, which may fluctuate depending on changes in income taxes, the cash value will grow steadily regardless of changes in income tax rates.

Many banks in Canada offer RRSP and TFSA through the same interface, enabling customers to consolidate their available contributions and investments into both plans. Despite being distinct from each other, they tend to be placed next to each other in terms of structure for better monitoring of tax-free and tax-deferred saving methods.

Finding the appropriate firm will involve assessing their fee structure, the kinds of mutual funds or exchange-traded funds they provide, and the level of flexibility they allow for handling withdrawals. Working with an excellent financial planner will assist in matching the requirements to your specific situation.

Whole Life Insurance Policies are usually not part of an RRSP or TFSA portfolio, yet most companies market them as a trio in their financial planning framework. This way, people are able to incorporate tax-deferred growth, tax-exempt returns, and cash-value gains in one single wealth creation process.

Contributions made to RRSPs can earn you an immediate tax break in the form of a tax write-off. However, gains from a TFSA portfolio grow tax-free and do not have any tax consequences when withdrawn. The decision should be based on the tax rate at the present time compared to the tax rate in the future.

The choice is based on income and investment objectives. Those who are in a higher tax bracket may want to invest in an RRSP to get deductions from taxes. While other investors might choose a TFSA because it allows them to withdraw their money tax-free.

The 4% rule is an approximation of how much one should withdraw from their retirement savings each year to finance their retirement. In the case of withdrawing money from an RRSP or RRIF, it assists in controlling taxable income and mitigating the possibility of running out of funds during their lifetime.

Mistakes include over-contributing to one’s TFSA account, constant withdrawal from the account within a short period without proper plans, investing in products that grow at low rates, failure to utilize the available contribution room, and lack of alignment between investments and financial goals.

The savings will depend upon the marginal tax rate that one falls under and the contribution made to the RRSP Plan. Larger contributions to RRSP translate into greater tax savings and hence, the net income is lowered. The extent of savings differs from year to year depending on the earnings.

One drawback is that withdrawals from the RRSP Plan are completely taxable, meaning the person would incur higher taxes while retired. Withdrawals could potentially move an individual to a higher tax bracket. There is also a limit to how much can be contributed each year.

You will be able to make contributions up to the extent of your contribution room for TFSAs. With respect to limits, you have the ability to make a contribution of $100,000, provided you have sufficient contribution room. Going above the limit means paying taxes on the excess contribution.

Sources and Further Reading

- Canada Revenue Agency

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/RRSPs-related-plans.html - Canada Revenue Agency

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account.html - Canadian Life and Health Insurance Association

https://www.clhia.ca - Sun Life Financial – Whole Life Insurance Overview

https://www.sunlife.ca/en/insurance/life/whole-life-insurance/ - Canada Life – Permanent Life Insurance

https://www.canadalife.com/insurance/life-insurance/permanent-life-insurance.html - Financial Consumer Agency of Canada

https://www.canada.ca/en/financial-consumer-agency/services/savings-investments.html - Bank of Canada

https://www.bankofcanada.ca - Government of Canada – Retirement Income Sources

https://www.canada.ca/en/services/benefits/publicpensions.html - Ontario Securities Commission

https://www.getsmarteraboutmoney.ca

Key Takeaways

- RRSP Vs TFSA Canada Is Not A One-Choice Decision

A balanced approach using both a Registered Retirement Savings Plan Canada and a Tax-Free Savings Account Canada helps optimize tax-efficient growth and flexibility. - RRSP Works Best For Tax Reduction In High-Income Years

RRSP contributions are tax-deductible and reduce taxable income, making them ideal for individuals in a higher marginal tax rate looking to defer tax. - TFSA Offers True Tax Free Growth And Withdrawals

A Tax-Free Savings Account Canada allows investments grow tax free, with tax free withdrawals that do not impact income tax or government benefits. - Contribution Room Is A Powerful Wealth Tool

Managing contribution room and unused contribution room effectively can significantly enhance long-term savings and overall investment gains. - Whole Life Insurance Canada Adds Stability And Protection

Whole Life Insurance Plans in Canada provide guaranteed cash value growth and a tax-free death benefit, supporting financial stability and estate planning. - Tax Efficiency Drives Long-Term Wealth Building in Canada

Combining tax-deferred, tax-free, and cash value strategies improves overall tax advantages and reduces future tax implications. - Personal Circumstances Should Drive The Strategy

Income level, financial goals, and expected tax rate changes determine whether RRSP, TFSA, or Whole Life Insurance should be prioritized. - Diversification Across Tools Strengthens Financial Outcomes

Using RRSPs and TFSAs alongside Cash Value Life Insurance in Canada creates multiple layers of growth, protection, and liquidity. - Planning Withdrawals Is As Important As Contributions

Future withdrawals from RRSPs can increase taxable income, while TFSA withdrawals remain tax-free, making withdrawal rules critical in retirement planning. - The Best Investment Strategy Canada Is Integrated, Not Isolated

Long-term wealth building in Canada is achieved by combining RRSP vs TFSA Canada with Whole Life Insurance Canada in a structured, tax-efficient plan.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- Best Wealth Plan Canada RRSP Vs TFSA Vs Whole Life Plan

- Registered Retirement Savings Plan – Tax Deferral And Retirement Savings Strategy

- Contribution Room And Tax Benefits – Maximizing RRSP Efficiency

- Retirement Savings And Investment Gains Inside RRSP

- Tax-Free Savings Account – Flexibility, And Tax Free Growth

- TFSA Vs RRSP – Which One Works Better For Your Personal Circumstances?

- RRSP First Strategy

- TFSA First Strategy

- Whole Life Insurance Canada – The Overlooked Wealth Strategy

- Whole Life Strategy For Long-Term Wealth

- Investment Gains Vs Cash Value – RRSP, TFSA, And Whole Life Compared

- Non-Registered Account And Alternative Investment Products

- Best Investment Strategy Canada – Combining RRSP, TFSA, and Whole Life

- Is Whole Life Better Than RRSP In Canada? A Realistic Comparison

- Final Wealth Blueprint – Choosing The Right Plan Based On Your Needs

Sign-in to CanadianLIC

Verify OTP