Sneha is a 34-year-old marketing manager and the mother of two who recently went through a health scare that made her reconsider the security of her family’s future. She felt that, despite having a good Life Insurance Policy, her financial safety net in case of a critical illness was not as good as she imagined it would be.

And like 60% of Canadians, she did not really know whether she would be able to tack on Critical Illness Coverage to her existing Life Insurance. Being nervous at the thought of having to go through the exercise of selecting an insurance policy, Sarah put it off.

Are you also like Sneha? She thinks her financial plan could use a few more insurances to make it stronger, but she doesn’t know where to start because there is so much jargon and so many choices. You are definitely not alone in this. So many are in your predicament and wonder whether they can add critical illness to an existing Life Insurance Policy. In this blog, we will look at how to add Critical Illness Cover to an existing policy to protect you and your family.

Can You Add Critical Illness Cover to an Existing Policy?

In Canada, this is a time for sure when one should learn the nitty-gritty of Life Insurance with critical illness since it can enable one to make wise decisions congruent to one’s long-term financial well-being. Yes, it actually means that it is not just possible to add Critical Illness Cover to an existing Life Insurance Policy, but it is also wise to make sure that you are prepared for any adversities in your life.

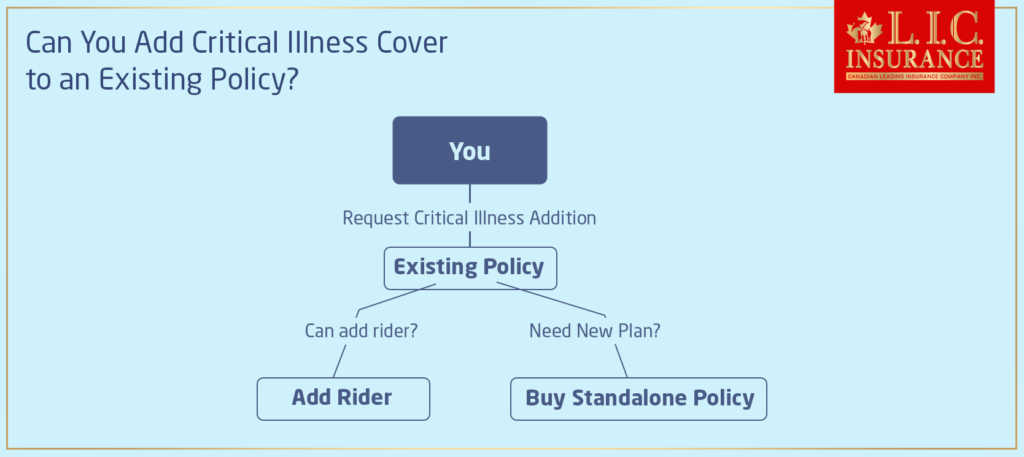

Possibility and Process

So first, you must understand that Life Insurance contracts are not the same. There are Life Insurance Policies developed that have a feature to attach another benefit, like the case of Critical Illness Insurance, with the help of a rider. A rider is an extra provision tacked onto the basic policy. It allows policyholders like you to tailor their Critical Illness Insurance Coverage to suit a specific requirement without having to handle more than one policy.

Alternatively, in case your existing policy doesn’t facilitate this feature, you could either upgrade to a new plan that has ‘Critical Illness Insurance Plans’ incorporated within it or buy one as a standalone Critical Illness Insurance Policy. The details on each of these are what we will consider.

Evaluating Your Current Policy

Just be sure to get acquainted with the terms of your present policy before you draw your conclusions. It may be tedious to do, but this way, you do not get yourself into some mess later. Go through your policy to see if there is a chance of conversion options, or whether it is renewable to include Critical Illness Cover. In most cases, you can beef up your insurance with very little change.

Why People Choose to Add Critical Illness Cover

Michael’s Problem: The Wake-Up Call

Consider the case of Michael, a freelance content writer who never really thought much about critical illness until his father had a stroke. That incident was an eye-opener for him, one in which he realized that a critical illness can be very damaging financially. The realization of such a fact made him attach Critical Illness Cover to his Life Insurance Policy, which gave him peace of mind that he would be able to support himself and his family in case such an incident were to happen to him. Know more on Can you take out a Critical Illness Cover without Life Insurance?

Liara’s Decision: A Family Plan

And then there is Liara, who, after her first delivery, became serious and added Critical Illness Insurance Coverage to her Life Insurance Policy. Her motive is obvious: in the unfortunate event of her falling ill from a serious illness, the expenses both for her ailment and the family’s lifestyle would be taken care of, and she would be in a better state of mind with which she would be able to concentrate on getting better.

The Benefits of Combining Covers: Enhancing Your Financial Safety Net

When you combine ‘Life Insurance with critical illness’ covers, you’re not just simplifying your paperwork; you’re strategically fortifying your family’s financial future. To know the difference between Life Insurance and Critical Illness Insurance click here.

Let’s explore this approach through a few important points that highlight the undeniable advantages of blending these essential Critical Illness Insurance Plans into one comprehensive strategy.

Streamlined Insurance Management

Effortless Tracking: Imagine managing just one policy with all the benefits you need. That’s the convenience of combining your covers. You reduce the hassle of keeping track of multiple premiums, renewal dates, and terms.

Real-life Insight: Take John, for example, a busy IT professional who juggled multiple insurance policies. After merging his covers, John now enjoys the simplicity of a single premium and one set of paperwork, saving time and reducing stress.

Cost Efficiency

Reduced Premiums: Often, adding a critical illness rider to your existing Life Insurance Policy can be more cost-effective than purchasing a standalone critical illness plan. You benefit from lower combined premiums while extending your Critical Illness Insurance scope.

Real-life Insight: Maria, a school teacher, opted to add a Critical Illness Cover to her Life Insurance Policy and discovered that the combined premium was significantly less than the two separate policies. This saving allowed her to allocate funds towards her son’s education fund.

Comprehensive Protection

Wider Coverage: By integrating Critical Illness Coverage with your Life Insurance, you ensure a broader safety net. This coverage extends beyond just life protection, offering financial aid during the critical times of battling severe illnesses.

Real-life Insight: When Alex was diagnosed with cancer, his combined ‘Critical Illness Insurance Plans‘ and Life Insurance provided a lump sum that helped cover his treatment costs without tapping into his savings, which were meant for his daughter’s college fund.

Immediate Financial Support

Accessibility to Funds: The Critical Illness Insurance Plan typically pay out a lump sum upon diagnosis of specified conditions. This feature allows you to access necessary funds quickly without the financial strain of waiting periods.

Real-life Insight: Sarah, who we met earlier, utilized her Critical Illness Insurance payout to cover immediate medical bills and ongoing treatments, which enabled her to focus on recovery rather than financial pressures.

Protection Against Lost Income

Income Replacement: If a critical illness leaves you unable to work, the lump sum from your insurance can act as a temporary income replacement, helping maintain your standard of living.

Real-life Insight: Consider the case of Tom, a freelance photographer, who suffered a stroke. His Critical Illness Cover provided a financial cushion that compensated for his lost income during recovery, ensuring his family’s expenses were covered.

Peace of Mind

Stress Reduction: Knowing that you and your family are protected against both the eventualities of death and critical illnesses can provide immense peace of mind. This coverage ensures that your family’s future is secure, no matter what life throws your way.

Real-life Insight: Emily, a single mother, chose to add Critical Illness Cover to her life policy for the sheer peace of mind it offered. She wanted to ensure that her children would be taken care of financially, regardless of any health complications she might face.

Isn’t it reassuring that with combined cover, you can protect both the family’s lifestyle and your health at the same time? Remember, today’s decisions about your insurance coverage will determine your family’s financial ability tomorrow.

After all, complexity shouldn’t get in the way of a good decision. Contact a Canadian LIC advisor now to learn more about how ‘Life Insurance with critical illness’ and ‘Critical Illness Insurance Plans’ can be customized to your life’s story, ensuring your family’s future with every policy you choose.

Closing Thoughts: Act Now for Peace of Mind

This blog has provided you with various scenarios and what actions you can take to add Critical Illness Coverage to your existing Life Insurance. Now, it is your chance to do something before it is too late. Before you get a wake-up call like Michael or a life-changing event like Liara, review your current coverage today and think about how adding Critical Illness Coverage can help you feel more at ease.

With Canadian LIC, you have a partner who understands what it really means to give the fullest advantage to the customer and is willing to help you review your options to find the best way forward for you and your family.

Check with Canadian LIC today and take the most important step in securing your family’s financial future from the unpredictability of critical illnesses.

Find Out: What cancers are not covered by Critical Illness Insurance?

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Frequently Asked Questions About Combining Life Insurance with Critical Illness Coverage

It cannot be added to all Life Insurance schemes, but most of the policies allow the integration of the add-on. One should always communicate with one’s insurance provider to know if one’s current policy allows for the integration of such a provision. In case your policy does not allow such an addition, you have to switch to another plan that supports both protections.

Raj thought his Life Insurance Policy did not allow the addition of Critical Illness Coverage, but a simple phone call with the insurance provider established the fact that he could upgrade his policy. This addition brought great peace of mind to him, knowing that he had comprehensive coverage.

It actually does save you money. Combining these two different covers can mean you pay less than if you had to pay for two separate policies. This means that having just one policy is easier to manage and has lower administrative costs as well as the time spent on it.

Lucy found that by combining her Life Insurance with Critical Illness Coverage, she saved on monthly premiums and also reduced the hassle of managing multiple insurance documents and renewal dates.

The exact illnesses covered can differ from plan to provider but typically include major illnesses such as cancer, heart attack, stroke, and more. Be sure to look over the list of covered conditions as you discuss your policy options.

Sam was relieved to find that his Critical Illness Coverage included less common conditions, such as Parkinson’s Disease, which runs in his family. This gave him the confidence that he was insured against any future health issues.

Yes, there is a waiting period that has to be met before most Critical Illness Plans are initiated and coverage becomes effective. The period can differ but is typically around 90 days from the start of the policy.

After including Critical Illness Cover on her policy, Mei was actually diagnosed with a critical illness just beyond the waiting period. Waiting was frustrating, but it meant that she was fully covered when she needed the financial support the most.

In many scenarios, yes, you can increase your sum assured, especially if the policy has some assured insurability options, which allow you to adjust your coverage with changing needs without a medical reexamination.

Having recently been promoted, Derek felt he needed to upgrade his Critical Illness Cover to match his current lifestyle and new level of responsibility. That would provide him with confidence that his higher standard of living could continue even if he fell ill.

If you never claim on the critical illness part of your policy, it acts as a safety net. Depending on your policy type, you won’t get these premiums back, but they contribute to a benefit payable on death or policy term. Not once did Nora need to claim her Critical Illness Insurance, but for peace of mind over those years, she felt it was worth every cent, just as she felt about her homeowner’s insurance.

Picking the right level of Critical Illness Insurance Policy will typically hinge on your financial situation, the number of people who depend on you, and your health risk factors. Be sure to consider your regular expenses, potential medical costs, and the needs of your family if you become ill.

To know her exact Critical Illness Insurance, Emily gathered her financial statements and considered her family’s expenses and lifestyle. With a financial adviser’s help, she fixed a value that would keep her family afloat without her income in case she were to be diagnosed with a critical illness.

Yes, Critical Illness Coverage can often be added to both term and whole Life Insurance for a rider. It makes your ‘Life Insurance with critical illness’ plan flexible and enhances the Critical Illness Insurance Coverage to suit the duration of the policy you opt for.

Mark took the term Life Insurance Policy and combined it with Critical Illness Coverage. He didn’t want to compromise on Critical Illness Insurance Coverage during these critical earning years, and this gave him confidence that his family’s future was financially assured during the policy term.

For ‘Critical Illness Insurance Plans,’ claiming is generally done on medical proof in the form of diagnosed illnesses—one of the types of covered conditions under the policy. The process is very simple, but proper documentation is needed.

When Anita was to file her claim under Critical Illness Insurance Coverage based on the diagnosis, it was really convenient for her because she had all the medical documents in place. The insurer helped her understand the process and put things in perspective.

A few policies make the provision for adding a child critical illness rider which allows covering the dependent children from the same policy. It might be an effective way of juggling your family’s health protection. When Sophie added a child rider to her critical illness plan, it just felt like the perfect idea; she felt like with that, the security cover for her children was also under the ‘Critical Illness Insurance Plans.’

Yes, the addition of Critical Illness Cover will raise your premium because you increase the risk that the insurance company has to cover. However, this increase is often far less expensive than it is to buy another, standalone Critical Illness Policy.

Kartik noted that his premium had increased a bit, but the total cost was much more affordable and easy to handle when paying for two separate insurance policies.

It is important to know what, exactly, this Critical Illness Insurance cover pertains to, i.e. the specified illnesses, exclusions, the waiting period, and the terms of renewal of the policy. You should always read the fine print and get clarity for any kind of details that are not clear with the insurer.

That is something that Linda learned the hard way because her friend had been denied a claim through a technicality of one exclusion. Now, she makes sure she understands all the terms before making any decisions regarding insurance.

Critical Illness Insurance pairs well with health insurance as it provides a lump-sum amount that covers all expenses that may not be catered for by the health insurance, like lost income, travel expenses for treatment, or home modifications. To give you an example, Emily’s Critical Illness Insurance payment was used to help pay for home help while she was recovering, which made her life a lot better during a hard time.

These questions and insights on Critical Illness Insurance can help you understand the importance of integrating Critical Illness Insurance with your Life Insurance plan. Remember, it’s about more than just insurance; it’s about ensuring financial security and peace of mind for you and your loved ones.

Sources and Further Reading

Canadian Life and Health Insurance Association (CLHIA): Overview of Critical Illness Insurance in Canada. This site provides general information about what Critical Illness Insurance covers, the types of plans available, and tips on what to consider when buying a policy.

Website: CLHIA – Critical Illness Insurance

Insurance & Investment Journal: Articles and news updates on insurance products in Canada, including Critical Illness Cover and how it integrates with Life Insurance.

Website: Insurance & Investment Journal

Canadian Insurance Top Broker: This source offers insights from industry experts on the latest trends and options in Critical Illness Insurance, helping consumers make informed decisions.

Website: Canadian Insurance Top Broker

Financial Consumer Agency of Canada (FCAC): Provides information on various types of insurance, including critical illness, and offers advice on managing and choosing insurance plans effectively.

Website: FCAC – Insurance

Insurance Bureau of Canada (IBC): Offers detailed explanations of insurance products, including critical illness, and their importance in financial planning.

Website: IBC – Critical Illness Insurance

These resources will provide a deeper understanding of Critical Illness Insurance and Life Insurance integration, helping you make well-informed decisions about your insurance needs.

Key Takeaways

- Most Life Insurance Policies in Canada can include Critical Illness Coverage, either directly or via a rider.

- Combining Critical Illness Cover with existing Life Insurance is often more cost-effective and simplifies financial management.

- Critical Illness Coverage offers a lump sum for specific illnesses, usable for expenses beyond medical bills, like lost income.

- Adding Critical Illness Cover allows for flexible protection that can be tailored to personal needs and life changes.

- It's crucial to know your policy's terms, i

- Proactively adding Critical Illness Cover can secure financial stability and peace of mind before a health crisis occurs.

Your Feedback Is Very Important To Us

We’re interested in understanding the challenges and concerns you may have experienced when considering or adding Critical Illness Insurance Coverage to an existing Life Insurance Policy. Your feedback will help us improve our services and provide better information to those in similar situations.

Please provide your responses in the space provided or use additional sheets if necessary. Your insights are invaluable, and we thank you for taking the time to help us understand your needs better.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com