Finally, the time has come after months of waiting; you finally have everything in place for your parents to come to Canada under the Super Visa program. You bought Super Visa Insurance in Canada, checked every box, crossed every T and dotted every i. But then the unexpected happens—a medical emergency results in an insurance claim which gets denied. The confusion, frustration and stress of dealing with this can be overwhelming. You’re not alone in this—many families in Canada are going through the same.

At Canadian LIC, we see this often. Our clients share their distressing experiences of dealing with the appeal process of denied claims. These stories show the emotional and financial stress and the need for guidance and understanding when it comes to Super Visa Insurance. This blog will go through how to appeal a denied claim under Super Visa Insurance and practical tips to get the benefits you deserve.

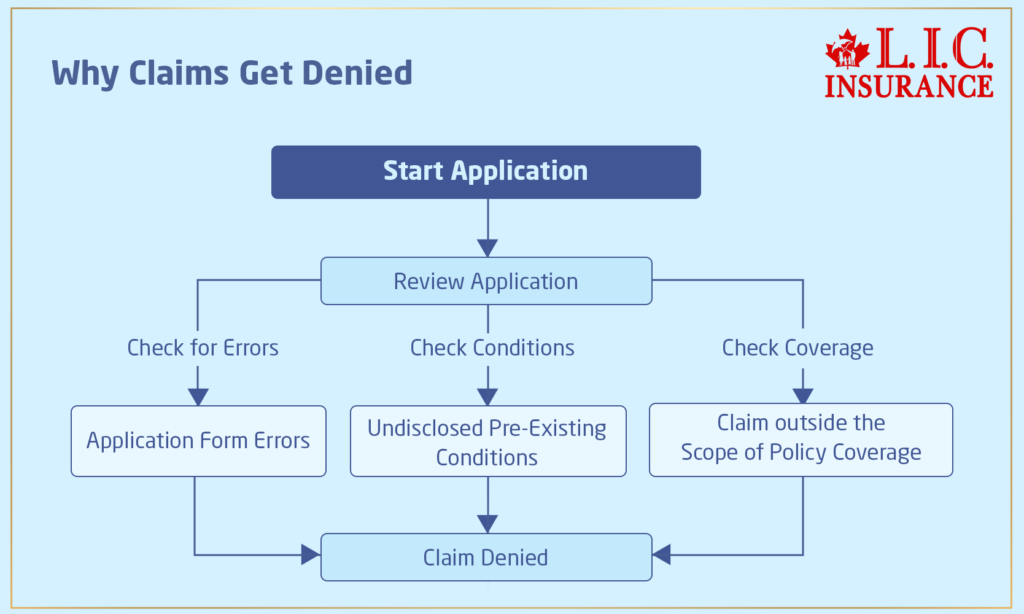

Understanding Why Claims Get Denied

Before we go on to the explanation of the appeal process, there is a critical need first to understand why claims may be rejected under Super Visa Medical Insurance Policies. Such common reasons may include discrepancies in the application form, nondisclosure of pre-existing medical conditions, or the claim being outside the scope of policy coverage. Lessons learned from each of our cases at Canadian LIC show what’s behind an insurance policy and the importance of double-checking the smallest of errors when applying.

For instance, take the case of the denial of Mr. and Mrs. Lopez’s claim for emergency medical expenses because of not acquainting the insurer with the fact that Mr. Lopez has had diabetes. This oversight, although accidental, led to significant stress and financial burden for the family.

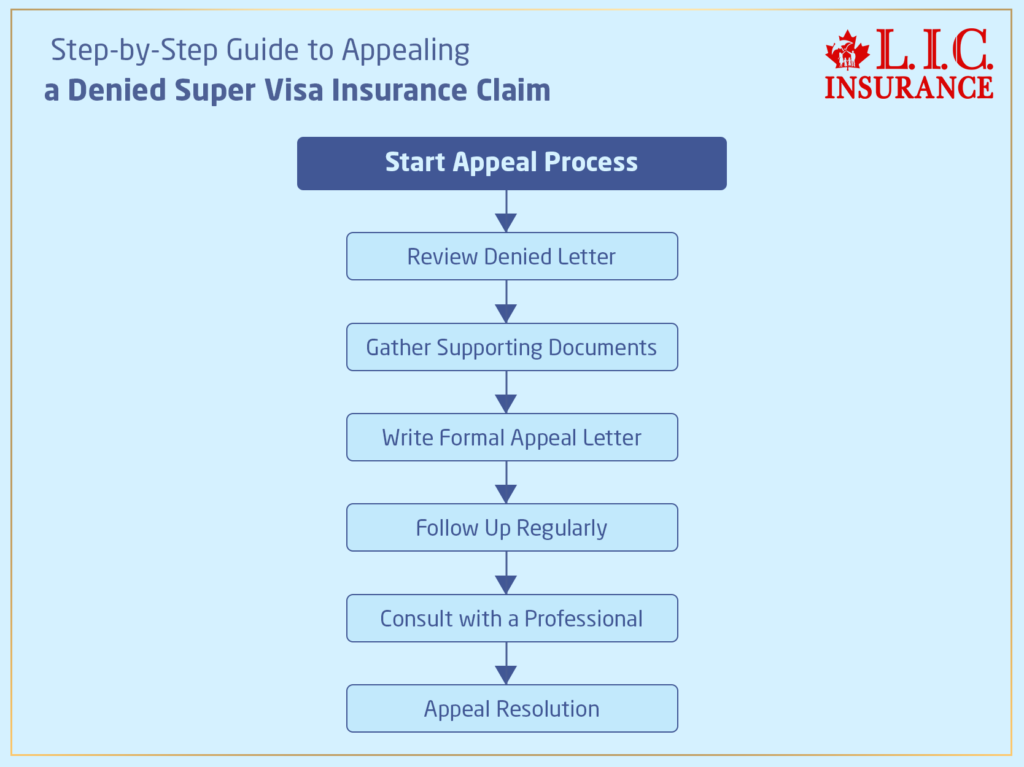

Step-by-Step Guide to Appealing a Denied Claim

Review the Denial Letter Carefully

Any appeal begins with understanding why the insurer has denied an individual’s claim in the first place. Under the law, insurers must clearly spell out the reason for their decision. In the case of the Nguyen family, for example, whose claim was refused due to a misunderstanding about the services rendered by a medical practitioner, it would become clear from the denial letter what misunderstanding needed to be clarified in the appeal.

Gather Supporting Documents

The best is to be borne out in good documentation. Documentation consists of medical records, doctor’s letters, and correspondence with the insurance provider. We helped the Patel family gather all kinds of complete documentation necessary to appeal a rejected claim citing incomplete information.

Write a Formal Appeal Letter

This will be the letter in which you will explicitly make your case, including all the evidence and why it should reconsider the denial. Of course, be professional and courteous. We often draft these letters side by side with our clients, just as we did for the Ahmed family so that their appeal would be not only respectful but also persuasive.

Follow Up Regularly

Regular follow-up can ensure that your case is not forgotten after the appeal has been filed. For instance, regular follow-up was the reason that the case of the Kim family, whom we assisted in their appeal, was considered at the appropriate time.

Consult with a Professional

In most cases, navigating the appeal process may be complex, especially when one has invested heavily in an appeal. Engaging with experts such as Canadian LIC is important to provide the necessary guidance toward a successful appeal. With our expertise in dealing with Super Visa Insurance Providers, we make sure everything is noticed.

Learning from Success Stories

Every successful appeal provides valuable insights. For example, the success of the Chen family’s appeal, which we facilitated last year, underscored the importance of a well-documented medical history and a robust argument aligning with the policy terms. Their story is just one of many that inspire confidence and provide a framework for handling similar challenges.

Conclusion: Why Choose Canadian LIC for Your Super Visa Insurance Needs?

Dealing with denied claims can be scary, but you don’t have to deal with it alone. Canadian LIC has years of experience and a proven track record of helping families like yours with Super Visa Insurance Coverage quotes and appeals. Our knowledge of insurance policies and personal approach to each case makes us your go-to partner for your family’s well-being in Canada.

Don’t let fear of insurance issues hold you back. With Canadian LIC by your side, you are prepared for anything that comes your way. Contact us today to get your Super Visa Insurance in Canada and sleep easy knowing you have the best in the business looking out for you and your loved ones.

More on Super Visa Insurance

- Changing the Effective Dates of My Super Visa Insurance After Purchase

- Including My Spouse in the Same Super Visa Insurance Policy

- Getting Super Visa Insurance Over 85 Years

- Filing a Complaint About My Super Visa Insurance Provider

- The Consequences of Not Having Valid Super Visa Insurance

- Expiring of Super Visa Insurance While the Visitor Is Still in Canada

- Waiting Period For Super Visa Insurance

- Super Visa Insurance – Refundable or not ?

- Find the Most Affordable Super Visa Insurance Plan

- Right Place to Buy Super Visa Insurance in Canada

- Cancelling Super Visa Insurance

- Paying Monthly for Super Visa Insurance

- Starting Super Visa Insurance in Canada

- Super Visa Insurance Benefits

- Know the Mistakes to Avoid While Buying Super Visa Insurance

- Things To Look for in Super Visa Insurance in Canada

- All About the Canadian Super Visa Insurance

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

FAQs on Super Visa Insurance Appeals in Canada

To avoid claim denials, ensure your policy covers all essentials by reviewing it thoroughly with an expert. There was a case in which the Huang family had their claim denied because their insurance did not cater to some medical treatment procedures. We counselled them to change their policy details with their insurer in regard to adequate coverage of all procedures. Always get a detailed Super Visa Insurance Quote outlining what shall be covered in every aspect.

In case your claim is denied, read the letter to see why. Collect your documents and file an appeal. At Canadian LIC, our experts take the clients through the process, just as we did with the Thompsons, whose initial denial due to a paperwork error was successfully overturned after a detailed review and resubmission of the necessary documents.

The time it takes to resolve an appeal varies from some weeks to several months. Consistent follow-up is key. For example, we handled the case of the Martin family, whose case went on for over three months. Regular follow-ups by our team ensured the case was not forgotten and they got a successful resolution.

Absolutely! In case your claim gets declined and you are reconsidering insurance options, Canadian LIC can still help you get a better quote that fits your needs. We compare prices among different Super Visa Insurance Providers to find the best rates and the right coverage. Just like in the Singh family’s case, after being initially declined, we were able to get a more favourable quote with better coverage options and peace of mind.

Common reasons include:

- Failure to disclose pre-existing conditions.

- Submitting claims for non-covered services.

- Errors in the claim submission process.

We often see cases like the Lee family’s, where their claim was denied due to undisclosed health issues. We recommend full transparency when applying for insurance to avoid such issues.

Understanding your insurance policy can be confusing at times. We encourage our clients to sit down with one of our experts at Canadian LIC and go through the policy in detail. The case of Brody’s family is the most apt example of it. They simply misunderstood the terms of their policy due to their ignorance. Our detailed walkthrough helped them get the nuances of their coverage.

Be sure to clearly state in the appeal letter why you think this case should be reconsidered, with all relevant documentation attached, such as medical reports and a copy of your insurance policy. We helped the Gonzalez family draft an effective appeal letter for reconsideration; the earlier claim denial was reconsidered and approved.

Expedited appeals are quite infrequent, but we can definitely accommodate them in cases of dire need. If you face such a situation, contact your Super Visa Insurance Provider and discuss such possibilities with them. In the O’Connor family’s case, we intervened when a medical emergency cropped up and expedited their appeal because it was of an urgent nature. That really made it easier and quicker for them to get the needed coverage.

If your appeal is denied as well, you have the option to file a request for review by someone higher within the insurance company. We guided the Walters family in doing so. While the insurance company initially denied an appeal, a higher review resulted in a favourable decision due to the additional medical documentation we were able to compile with the help of this family.

The right Super Visa Insurance Policy would be to understand your special needs and match them with the right provider. We believe in taking a personalized approach at Canadian LIC. For example, when the Chang family came to us, we assessed their needs based on the grandparents’ health and their stay duration, providing them with multiple Super Visa Insurance Quotes in order to find the best fit for the circumstances.

Most insurance companies do not charge fees to help you with an appeal in case your claim has been denied. You might, though, find fees if you retain legal help or some professional advisor, like Canadian LIC. The Morneau family found this worthwhile, as our expertise led to the successful overturning of their denied claim.

Mistake avoidance starts with understanding everything and disclosing all the necessary information. We always remind the clients, like the Diaz family, to check their applications. We avail ourselves to all clients concerning the collection of necessary documents to prevent potential complications.

Yes, you are free to change your service provider in case you are not satisfied. Just be sure not to leave a gap in your coverage. Poor service is what happened in one of the families we have—the Fishers—and Canadian LIC helped them transition seamlessly over to another provider, ensuring there wasn’t a single gap in coverage throughout their stay.

Look for a quote that provides comprehensive coverage on hospitalization, emergency medical services, repatriation, and more. We would also advise you to see if there is coverage for pre-existing conditions, if any. We guided the Kumar family in picking a policy that would cover their specific health concerns, giving them peace of mind during their visit to Canada.

This also means that clear, concise, and timely updates are part of effective communication. Keep records of every communication. We support practices such as what we did with the Oliver family—to that end, we maintained detailed logs of communication, which greatly increased the efficiency of their claim process.

Check licence status, customer reviews, and industry reputation as a way of verifying if an insurance provider is reliable. At Canadian LIC, we only deal with providers who have strong credentials backed by positive client feedback. For example, when the Rajhans family was looking around, we were able to help them choose a provider renowned for their great handling of claims process and customer service.

Key factors include:

- Coverage limits.

- Deductible amounts.

- Coverage for pre-existing conditions.

- The overall cost of the insurance premium.

We help our clients, like the Gomes family, compare these aspects side-by-side, ensuring they understand each element of the quote to make an informed decision.

You need to file an appeal as early as possible, usually within the time frame specified in your policy; this could be between 30 to 90 days from the denial date. This, again, is another thing the Lee family found out the hard way: they delayed their response and missed almost their deadline.

Of course, we can guide you right from the buying of your Super Visa Insurance Policy to keeping track of claims and even appealing in case of denial. For example, we helped the Moreno family from the start of their policy purchase to a successful appeal process, ensuring they felt supported at every step.

If you wish to remain in Canada beyond the initial period, which is covered by your insurance, contact your provider to discuss extension options. Be sure to avoid having a lapse in coverage. In the case of the Chen family, we made arrangements for a continuation of insurance with no gaps once they decided to stay longer.

We simplify the communication process by serving as your representative—handling all correspondence, keeping your records in order, and making sure your case is clearly and effectively represented. This was particularly beneficial for the Thompson family, whose appeal involved complex medical documentation that we helped compile and submit on their behalf.

Keep your insurer updated about any changes in your medical condition during a policy term. It may affect the coverage and require some necessary policy alterations. We did this when Mr. Patel was diagnosed with a new condition and accordingly updated his policy.

Switching providers mid-policy is possible but may involve complexities such as potential coverage gaps. We would encourage you to carefully consider an advisor who can walk you through all of these details. Once, we helped the O’Malley family switch providers mid-policy; because of our experience, they did not have to worry about not being covered.

Rest assured that stress and uncertainty about insurance claims or appeals are going to be minimized with the proper questions and by knowing all you can about your Super Visa Insurance Policy. Let Canadian LIC be there through it all, making sure your family’s visit to Canada is protected with the right insurance.

Sources and Further Reading

Here are some sources and recommendations for further reading to complement the blog on appealing denied claims under Super Visa Insurance in Canada:

- Immigration, Refugees and Citizenship Canada (IRCC) – This official site provides comprehensive details about the Super Visa program, including insurance requirements. Visit IRCC’s Super Visa section for the latest updates and guidelines.

- Canadian Life and Health Insurance Association (CLHIA) – A great resource for understanding insurance policies and consumer rights within Canada. CLHIA offers insights into various types of insurance, including those required for the Super Visa. Check out their resources at CLHIA Website.

- Financial Consumer Agency of Canada (FCAC) – Provides information on consumer rights and responsibilities relating to financial products, including insurance. Their resources can help you understand the financial implications of insurance policies. Visit FCAC’s official website.

- The Council of Insurance Regulators of Canada – Offers information about insurance regulation across Canada, which can be useful when dealing with disputes or appeals in insurance claims. Learn more on their official website.

- Insurance Brokers Association of Canada (IBAC) – IBAC offers detailed advice and guides on choosing insurance brokers and understanding your policy’s coverage. Visit IBAC’s official site.

These resources will provide reliable information and can help deepen your understanding of managing and appealing Super Visa Insurance claims in Canada.

Key Takeaways

- Recognize common reasons for insurance claim denials such as non-disclosure of conditions.

- Act promptly after receiving a denial to prepare an effective appeal.

- Gather all relevant documentation to support your appeal.

- Prepare a clear and concise appeal letter.

- Maintain regular contact with the insurance provider during the appeal process.

- Consider professional help from firms like Canadian LIC to navigate the appeal complexities.

- Utilize real-life examples from Canadian LIC to understand the appeal process better.

- Engage with a reputable insurance brokerage for comprehensive coverage and support.

Your Feedback Is Very Important To Us

We value your insights and experiences regarding balancing part-time work with receiving Disability Benefits in Canada. Your feedback will help us understand the challenges and needs you face. Please take a few minutes to answer the following questions:

Thank you for sharing your valuable feedback. Your insights are crucial in helping to shape better support systems for individuals balancing work and health challenges.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com