- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Travel Insurance vs International Health Insurance For Canadians Travelling Abroad (2026)

By Harpreet Puri

CEO & Founder

- 12 min read

- April 14th, 2026

SUMMARY

A detailed comparison of Travel Insurance Canada and International Health Insurance for Canadians travelling abroad in 2026. The content explains Travel Insurance Coverage, Travel Medical Insurance costs in Canada, pre-existing conditions rules, and options for canadian Travel Insurance for seniors. It also highlights when long-term medical insurance is essential for safe and affordable care overseas.

Introduction

Why Canadians Travelling Abroad Need The Right Coverage In 2026

Leaving Canada for a holiday, a work term, an extended stay or retirement is more popular than ever. Canadians took more than 26 million international trips last year, Statistics Canada reports — a figure that is expected to climb over the next two years as borders settle and free movement around the world rebounds. And although travel sounds like fun, the financial risks of being hit with medical bills abroad can be punishing. The average international hospital stay can run $6,000 to more than $25,000 per day, depending on the country and level of care, according to CIHI reports.

It’s this fact that compels Canadians to look for Travel Insurance Canada, compare the cost of Travel Medical Insurance in Canada, and try to figure out how they can get International Health Insurance instead. We encounter hundreds of cases each year where travellers unwittingly select the wrong plan and are left with unpaid medical bills, denied claims or even suboptimal Travel Insurance — particularly if pre-existing conditions are factored in.

2026 may well be a year where travel numbers continue to rise, but so do global healthcare costs. Whether you’re planning a brief vacation or getting ready for life overseas, distinguishing Travel Insurance from International Health Insurance is the first step in safeguarding yourself financially.

Understanding Medical Emergency Risks For Canadian Travellers

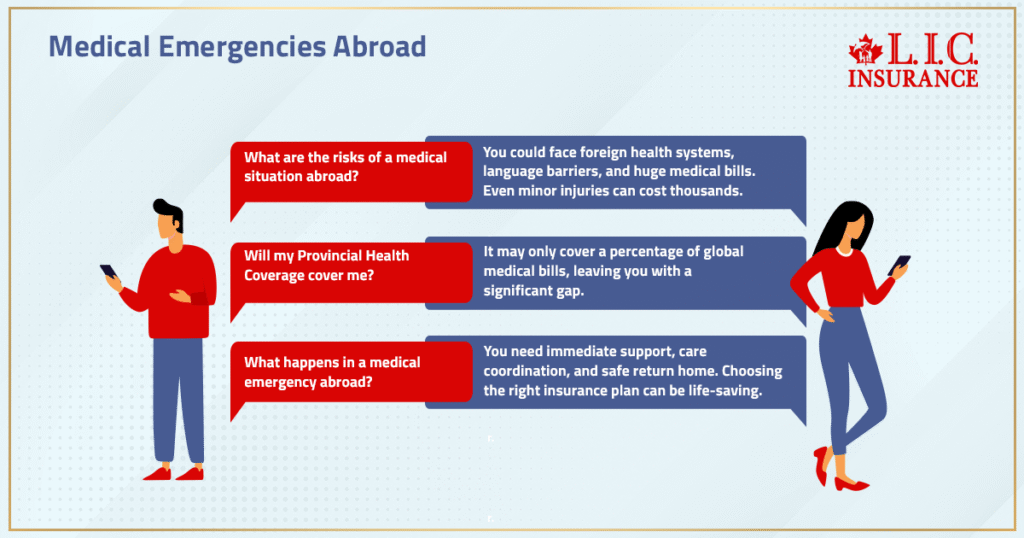

A medical situation abroad can spiral out of control in a hurry. You are in a new country, dealing with foreign health systems, perhaps language barriers and potentially huge medical bills. Even a relatively minor injury can balloon to thousands of dollars. It’s a reason for high costs, ranging from over $30,000 for a fractured arm in California to more than many would expect for an overnight stay in a hospice hotel in Asia.

As our advisers, we’ve helped travellers who thought their Provincial Health Coverage would cover them and discovered that the territorial health plan pays only a percentage of global medical bills. This gap leaves you empty-pocketed, a cost most of us don’t plan for as we travel.

Even worse, those emergencies hardly ever seem to come at a convenient time. There are the straightforward medical emergencies: When something goes wrong — when someone is injured, in an accident or ill with an infection, say, or complications from a medical condition that didn’t seem as serious before. When that happens outside of the country, you want support right away — an insurer to offer emergency help, coordinate care and make sure you are sent home to your home province or return home safely. And that’s when choosing the right plan becomes life-saving.

What Travel Insurance Is Designed To Cover

Travel Insurance is structured for short-term trips — vacations, quick visits abroad, family travel, or business travel. A standard Travel Insurance Policy is built around Emergency Medical Coverage so you can stabilize and return home quickly.

What it normally includes:

- Emergency medical treatment

- Trip cancellation and trip interruption

- Lost luggage or delayed baggage

- Emergency evacuation

- Travel accidents

- Limited insurance coverage for pre-existing conditions (depending on stability periods)

Most travellers choose these plans because they offer protection against immediate disruptions. But it’s important to understand the limitations:

✔ Travel Insurance offers coverage, but only until you’re well enough to return to Canada.

✔ It rarely covers long-term medical care abroad.

✔ It does not replace domestic or international health plans.

✔ It does not cover every treatment, especially when linked to unstable pre-existing medical issues.

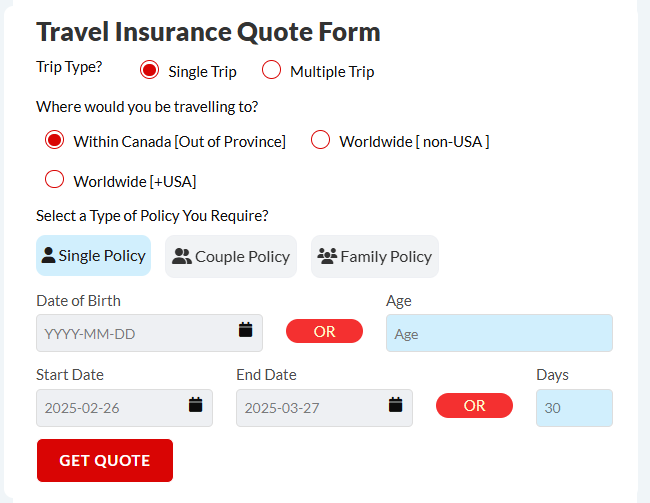

A lot of Canadians buy Travel Insurance based on the average cost of Travel Insurance or cheap Travel Insurance Canada quotes, as it is affordable. And sure, an online Travel Insurance quote is quick — but the plan still needs to fit your health scenario and how long you are travelling.

Travel Insurance is the best investment you can make for short trips. But if you’re spending more than a couple of months abroad, then you’ve entered an entirely different risk category.

International Health Insurance: Long-Term Protection For Canadians Moving Abroad

International Health Insurance is a different world. It isn’t built for quick trips — it exists for Canadians moving abroad, taking job placements overseas, retiring in another country, or splitting time between Canada and another home.

Unlike Travel Insurance, international plans provide:

- Full medical insurance for long-term or permanent stays

- Coverage for both emergency and routine medical treatment

- Access to private hospitals in many regions

- Coverage for chronic conditions

- Pre-existing conditions (depending on underwriting)

- Wider global hospital networks

- Flexibility to choose doctors and hospitals

Most importantly:

International Health Insurance covers the cost of your long-term medical treatment overseas, not just emergency medical stabilization.

Travel Insurance ends when you’re stable.

International health insurance is with you as long as you’re away from home.

And that difference matters more than most people realize. We depend a lot on provincial systems as Canadians. But as soon as you start spending a longer time outside your home country, the system no longer works. That’s when the option to access treatment overseas — without incurring huge costs — is worth considering.

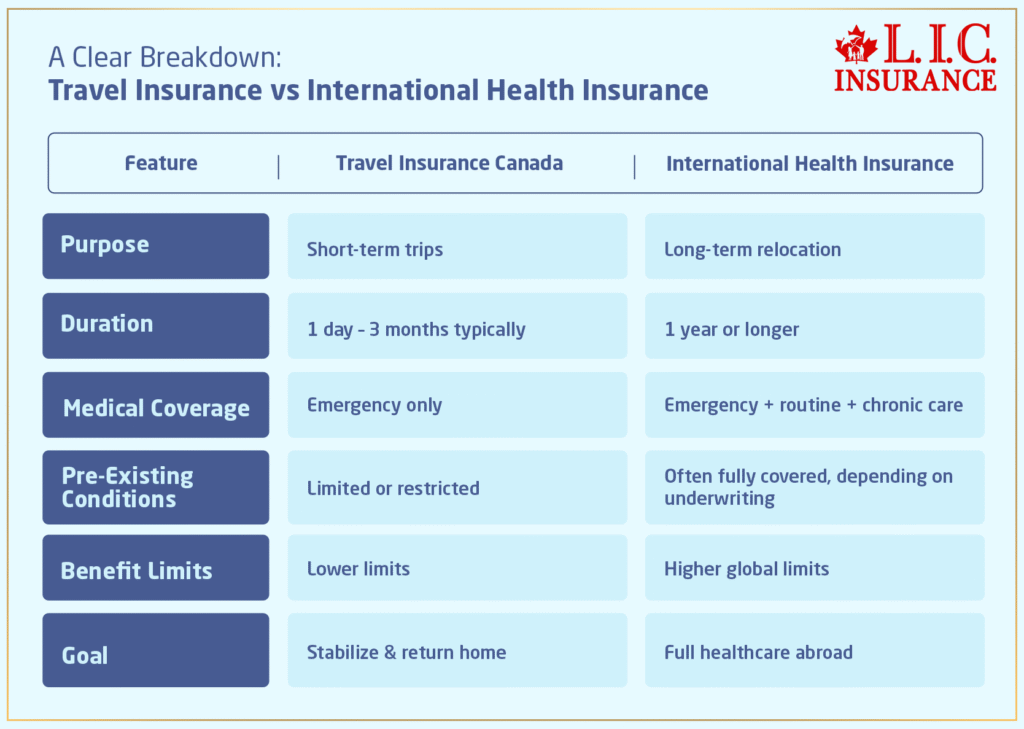

A Clear Breakdown: Travel Insurance vs International Health Insurance

Here’s how the two compare in the real world:

Travel Insurance works for travel abroad.

International Health Insurance works for living abroad.

Picking the wrong plan leads to denied claims, uncovered treatment, and overwhelming related costs.

Buy Travel Health Insurance Or Go With International Coverage? Key Considerations For Canadians

Choosing between the two depends on a few key considerations:

1. How long are you staying abroad?

Short vacations → Travel Insurance

Several months or years → International Health Insurance

2. Do you have any pre-existing conditions?

If you need stable coverage for chronic conditions, international plans provide a far better safety net. Travel Insurance with pre-existing conditions, Canada plans often have strict stability rules.

3. Will you rely on medical providers overseas?

International plans help you access private facilities, English-speaking doctors, and structured medical networks abroad.

4. Are you a senior traveller?

Canadian Travel Insurance for seniors often becomes complicated with age-related underwriting requirements. International plans may offer better long-term options depending on health history.

5. Are you concerned about emergency medical evacuation?

International plans typically have smoother evacuation processes, while travel plans prioritize stabilization.

6. Are there cost differences?

Yes.

- Travel Medical Insurance costs in Canada are usually lower for short trips.

- International plans cost more upfront but offer deeper protection for long stays.

The right choice depends entirely on your situation — and that’s exactly where our advisors step in.

When Pre-Existing Conditions Require The Right Coverage

Any pre-existing conditions — diabetes, heart concerns, respiratory issues, prior surgeries — need careful evaluation before travelling.

Travel insurers may:

- Exclude the condition

- Require a stability period (often 90–180 days)

- Deny claims if the condition worsens unexpectedly

This is one of the most common reasons travellers face denied claims.

International Health Insurance, on the other hand, can sometimes fully include pre-existing medical condition coverage, depending on underwriting. It’s far more reliable for people with ongoing medical needs.

We see travellers every week who assume their medical condition was stable, only to discover exclusions buried deep in policy wording. Getting the right coverage makes all the difference.

Choosing The Right Coverage For Moving Abroad

Once you are moving abroad, your Home Province Coverage may stop after a certain number of months. Most provinces require physical presence in Canada for continued eligibility. That’s why relying on your Territorial Health Plan becomes risky.

When Canadians relocate without proper insurance, they often face:

- Out-of-network hospital fees

- Private healthcare pricing

- Language or cultural barriers

- High upfront bills before reimbursement

- Claims were denied due to a lack of global coverage

This is where international plans shine — they step in to provide comprehensive protection no matter which country you’re in.

Medical Insurance Options For Long-Term Stays Overseas

For Canadians who are splitting time between multiple homes or fully relocating, Medical Insurance becomes non-negotiable.

These plans support:

- Global doctor networks

- Chronic condition management

- Specialist visits

- Emergency surgeries

- Routine checkups

- Diagnostic tests

- Preventive medical care

International plans are designed to ensure you never have to pay out of pocket for unexpected medical bills during long-term stays abroad.

Why Emergency Assistance Matters More Than Ever

When the unplanned happens overseas, 24/7 emergency assistance is your lifeline. It’s not only a matter of answering the phone; it’s about arranging care, directing you to the nearest facility and organizing an emergency evacuation when necessary.

We’ve seen situations where the right insurer saved clients thousands of dollars through watchovers on everything from hospital transfers to doctor communication. Without it, travellers describe feeling lost, stressed and financially vulnerable.

Emergency Medical Coverage Differences Explained

Emergency medical benefits differ widely between travel and international plans.

Travel Insurance:

- Covers emergencies only

- Stops coverage when you’re well enough to return to Canada

- Provides limits that may not support long hospitalizations

International Health Insurance:

- Covers emergency + long-term care

- Supports ongoing treatment abroad

- Allows treatment at private hospitals

The difference is simple but incredibly important.

Right Coverage For Canadians Travelling Abroad In 2026

As travel increases, so does the need to match your insurance to your lifestyle. Whether you’re taking shorter trips, staying abroad for months, or starting a new chapter overseas, having the right coverage is the difference between a protected trip and a financial disaster.

How Canadian LIC Helps You Compare Travel And International Health Options

Our experts help Canadians select the insurance policy that best suits their medical needs, destination, age and travel history. We read the fine print, compare global insurers and help you avoid exclusions that could leave you vulnerable.

That way, you never buy an insurance policy that won’t provide protection for you.

Final Decision Framework: Which Coverage Protects You Best Abroad?

Here’s the simplest way to make informed decisions:

✔ Choose Travel Insurance if your trip is short and you mainly want protection from emergency costs, disruptions, and trip complications.

✔ Choose International Health Insurance if you need long-term coverage, routine care, chronic care, and a stable health framework overseas.

No matter where you’re headed in 2026, the right plan keeps you safe, supported, and financially secure.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

The perks of even the most generous credit card offer no comparison to a comprehensive Travel Insurance Canada plan. Limits are lower, and benefits are often reduced for more complicated claims or emergencies abroad. Certain cards don’t provide coverage for seniors and travellers with pre-existing conditions, so gaps are inevitable. A specialized Travel Insurance Policy means your insurance protection has been designed for the real world, not its best-case scenario.

International plans offer support for medical insurance each day that you are not in your own country, while short-term travel products can supplement these needs. They provide immediate consultation with specialists, private hospital care and ongoing medical attention without the necessity to prematurely return home. For Canadians working and living life abroad, it issues you protection without dependence on unfamiliar systems. It’s a long-term health insurance plan designed for a life outside of your home country.

Areas with more expensive medical care result in higher premiums for travel medical insurance in Canada, particularly if evacuation or high-limit emergency medical coverage is required. Nations with less established infrastructure might need more robust Travel Insurance to avoid major costs. Insurers also factor in local risks, such as extreme climates or few hospitals nearby. When you get a Travel Insurance quote online, it is always specific to where you are going and how long you will be away.

Age corresponds with distinct medical condition considerations, so seniors should look into stability regulations, prescription assistance and upper boundaries for emergency treatment abroad. Those with smoother claims procedures and stronger emergency assistance are generally more trustworthy. It’s also good to know evacuation guidelines for travelling far away from major hospitals. The best Canadian Travel Insurance for seniors strikes a balance between price, coverage and long-term stability.

The coverage depends on health stability, changes in medication or a recent history of treatment that insurers scrutinize closely. Some plans have riders that can be purchased to get coverage beyond the emergency medical that is already included. Others will want answers to health questionnaires or evidence of dependability. With a variety of Travel Insurance policies with pre-existing conditions in Canada, comparing is never as easy as you get to avoid having uncovered related expenses.

Work placements are frequently at private hospitals or subject to employer requirements that standard Travel Insurance Coverage doesn’t cover. Preventive care, chronic management, and continuous coverage. International Medical Insurance protects against breaks in coverage as you move from one country to the next, which is common under other health plans. It allows you to steer clear of paying medical bills up front in strange systems. It is a sure way for Canadians living outside the country to have reliable Health Insurance Coverage.

If you have multiple destinations with greater needs for evacuation readiness or longer protection periods, the average price will be higher. Insurers determine the price using total days in Japan, regional prices for healthcare services and activities such as adventure sports. Those with pre-existing risks may see adjusted premiums. Receiving an itemized online Travel Insurance quote enables you to see how each factor contributes.

Yes, most Travel Insurance Policies include baggage coverage, but the limits vary by plan and company. Reimbursement can also extend to basic purchases until you retrieve or replace your stuff. Travellers will need to keep receipts and pay close attention to the insurer’s claims process. Robust plans provide immediate assistance, so you won’t take on the entire cost out of pocket.

Longer stays also cover regular medical treatment, progressive diseases and a higher level of exposure to local hazards. Short-term plans aren’t designed for continuing care or repeat medical crises. International plans bridge that gap with more pervasive protection and longer-term stability. It’s the difference between standard trip protection and worldwide health insurance that moulds itself to your life.

Risk of medical emergencies rises with adventure activities, so insurers evaluate safety levels, destinations and possible types of injury. Some plans have optional riders for extreme sports, and some exclude them entirely. A good Travel Insurance Canada plan puts what’s covered in plain view before you cross the Canadian border. Reading through these specifics will make sure you are properly covered for the trip you have planned.

Sources and Further Reading

- Government of Canada — “Trip Interruption and Travel Health Insurance” — policy basics and medical coverage abroad. Travel.gc.ca

- Global Albatross — “International Medical Insurance: A Complete Guide for Expats” — detailed breakdown of International Health Insurance vs Travel Insurance. Global Albatross

- Allianz Care — “Expat Health Insurance 101: Navigating the World of Coverage for a Life Overseas” — focused on long-term stays and what’s covered. allianzcare.com

- Government of Canada — “Essential Preparation for Travelling Outside Canada” — emphasizes Travel Insurance and medical emergency risks abroad. Global Affairs Canada

Key Takeaways

- Travel Insurance Canada works best for short trips, providing emergency medical coverage, trip cancellation support, and protection from unexpected travel disruptions.

- International Health Insurance is built for Canadians travelling abroad long term, offering deeper medical insurance benefits, ongoing treatment options, and full health coverage outside the home province.

- Travellers with pre-existing conditions or chronic medical needs must carefully compare Travel Insurance Coverage and long-term international plans to avoid paying major medical expenses out of pocket.

- The right coverage depends on the trip length, destination, personal health history, and the level of medical emergencies you want insured, making proper planning essential for travel abroad in 2026.

Feedback Questionnaire:

IN THIS ARTICLE

- Travel Insurance vs International Health Insurance For Canadians Travelling Abroad (2026)

- Understanding Medical Emergency Risks For Canadian Travellers

- What Travel Insurance Is Designed To Cover

- International Health Insurance: Long-Term Protection For Canadians Moving Abroad

- A Clear Breakdown: Travel Insurance vs International Health Insurance

- Buy Travel Health Insurance Or Go With International Coverage? Key Considerations For Canadians

- When Pre-Existing Conditions Require The Right Coverage

- Choosing The Right Coverage For Moving Abroad

- Medical Insurance Options For Long-Term Stays Overseas

- Why Emergency Assistance Matters More Than Ever

- Emergency Medical Coverage Differences Explained

- Right Coverage For Canadians Travelling Abroad In 2026

- How Canadian LIC Helps You Compare Travel And International Health Options

- Final Decision Framework: Which Coverage Protects You Best Abroad?

Sign-in to CanadianLIC

Verify OTP