- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Finfluencers Hit by New CSA CIRO Rules In Canada

By Harpreet Puri

CEO & Founder

- 10 min read

- April 22nd, 2026

SUMMARY

CSA and CIRO released new guidance that reshapes financial influencers’ Canada regulations and finfluencer marketing rules in Canada. The discussion explains how social media content can trigger securities laws, registration duties, and disclosure obligations when advice influences investors. It highlights risks around conflicts of interest, sponsored posts, investor inquiries, and trading activity, while clarifying what licensed insurance advisors in Canada and online personalities must do to stay compliant under evolving financial regulations.

Introduction

Why Finfluencer Content Is Now A Regulatory Risk In Canada

The Canadians are being taught about money in a very different manner than how they were taught about money even five years ago. The Ontario Securities Commission confirms that financial information, especially among young Canadians who are first-timers in the stock market, is now heavily dependent on social media as a source of information. Entertainment-based platforms have slowly turned into investment, finance, and financial decision-making classrooms.

That change compelled the regulators to take action.

The Canadian Investment Regulatory Organization (CIRO) and the Canadian Securities Administrators (CSA) issued formal guidance on the financial influencers Canada regulations on December 11, 2025, the way how influencers, companies, and online personalities might already be under the influence of securities laws without even knowing it.

This advice is long overdue in our eyes as an approved insurance consultant in Canada. Education in finance is important. However, lack of regulation, inappropriate disclosure, and conflict of interest may lead to actual damage, especially in the Canadian capital markets, with trust being the baseline of the whole system.

This is no longer a grey area. The rules are clearer. The expectations are higher. And it has the danger of making a mistake.

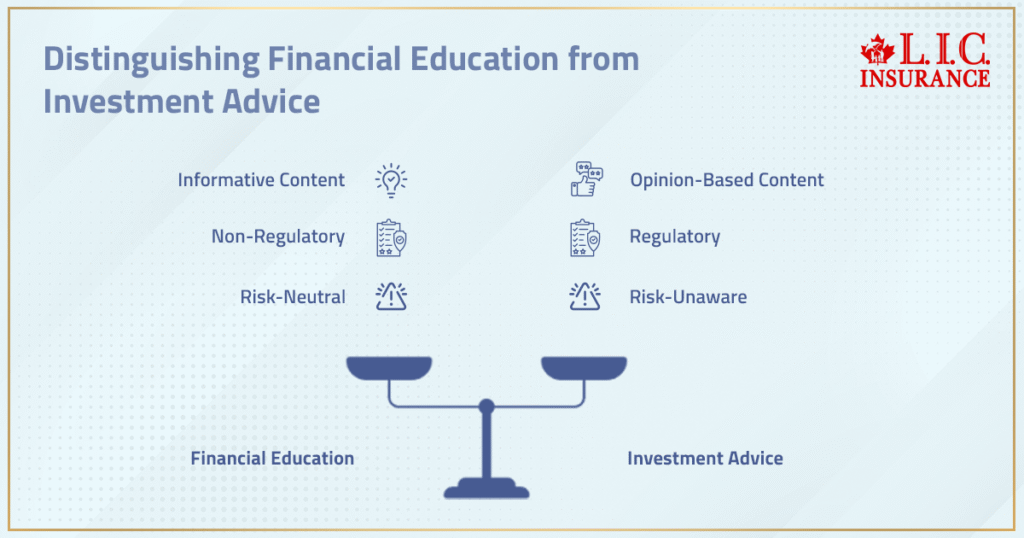

Finfluencers And Financial Education: Where Information Crosses Into Advice

One critical line that regulators are concerned about is education and advice.

Informing the truth about the markets, how registered accounts operate, or what contribution limits do, usually comes under financial education. Such material assists investors, but not in making investment choices.

However, any post that states an opinion about the merits of a security, markets a particular investment, or encourages his or her supporters to act can be construed as investment advice. Even emojis, hyping language, or the use of can-not-miss ” framing can take content into the realm of regulation.

This is important since advice is obligatory. It should take into account risks, appropriateness, and context. In social media, these protective measures are usually absent, but the investors on the ground continue to operate based on what they observe.

The intent may be education. The impact may influence. Regulators focus on impact.

Investor Inquiries And The Moment Registration Is Triggered

Among the least taken risks is the investor inquiries.

A finfluencer can begin with general content that can be subject to a general advice exemption. However, when they start to answer remarks or personal messages with advice based on the situation of the individual, registration needs may occur.

CSA guidance is explicit:

Disclaimers such as this are not advice, do not take the conduct over.

When one talks about suitability, personal situations or advises actions depending on their profile, they can be arousing suitability determination conditions, even without any intention to do so.

Compliance-wise, this is where a good number of the unregistered people unwillingly cross the boundary.

Securities Regulators Are Watching Social Media Closely

This advice is not mere symbolism. It indicates coordination between securities regulators in the provinces in Canada, such as the Ontario Securities Commission and the Alberta Securities Commission.

The CSA and CIRO are striving to have an effective and uniform regulation so that the nation is harmonized in expectations. Protecting the investors is their mandate, not censoring content.

Not only are enforcement actions no longer applied to traditional firms. Securities regulators have now been placed squarely in the realm of online activity, where they have an impact on investing behaviour.

When they affect the trade activity with the use of the content, they may be subject to scrutiny, no matter the size of the platform.

What Makes A Financial Influencer Regulated In Canada

A financial influencer does not need formal credentials to fall under regulation.

According to CSA and CIRO guidance, regulated activity may include:

- Promoting specific investments

- Encouraging copy trading or mirroring strategies

- Advertising or soliciting trades

- Creating hype around guaranteed returns

This applies across equity marketplaces, the stock market, and broader Canadian capital markets. Claims tied to interest practices or exaggerated upside increase regulatory risk.

What matters is not the title someone uses, but what they do.

Client-Focused Reforms And Why They Apply To Finfluencers

The client-centered reforms carried out by CIRO have one principle that is the most important one: the best interest.

Conventional financial advisors should take into consideration the risk-taking, financial objectives, and personal background. The influencer content, by nature, is mass-distributed. That puts a structural clash with the standards of suitability.

Advice that does not take into account the risk profile of the individual investor, though it may not be the intention, can be misleading. This is the reason why regulators are suspicious of wide advice and protection rather than popularity.

Retail Investors Are More Influenced Than They Think

The Ontario Securities Commission put this influence to the test.

In controlled research, 38.1% of individuals who were exposed to a post by a finfluencer bought the promoted asset, and 8.3% of the control group did. The rate declined to just 28.5, even with the disclosures of conflict of interest.

Disclosures lead to loss of influence. They do not eliminate it.

It is the reason that the issue of conflicts of interest is still central to CSA influencer rules. Even where there is disclosure of risks, influence alters financial decisions.

CSA And CIRO: How The New Guidance Changes The Game

This collaborative CSA and CIRO guideline is a change.

It harmonizes jurisdictional regulation and explains expectations, and concentrates on efficient oversight without choking legitimate education. This is aimed at restoring the confidence of Canadians in financial products and markets.

To creators, it is nothing but a mere message that influence is responsibility.

Financial Products, Sponsored Posts, And Referral Arrangements

There are more risks associated with sponsored posts.

In the case, a finfluencer, in exchange for promoting financial products when he/she is being compensated, the relationship can be viewed as a referral arrangement that falls under the securities laws. This is applicable to mutual fund dealers, investment dealers, as well as registered firms.

The disclosures should be transparent, notable, and timely. It is not enough to bury the conflicts at the end of the content or behind the links.

Companies that cooperate with influencers can also be held responsible for the claims of their representatives. The reputation and compliance are closely connected now.

Online Personalities Versus Licensed Financial Advisors

Online reach is not the same as accountability.

Licensed professionals undergo formal training, registration, and ongoing compliance. Online personalities may have influence—but lack regulatory oversight.

This distinction matters. Advice without accountability creates risk for investors and for the person providing it.

Conflicts Of Interest Must Be Disclosed—Properly

CSA guidance is clear: vague disclosures fail.

Saying “I may have interests” does not meet disclosure standards. Conflicts of interest must be identifiable, specific, and presented where the audience connects them directly to the advice.

Disclosure is not a formality. It is a protection mechanism.

Ontario Securities Commission And Provincial Enforcement Reality

The Ontario Securities Commission is considered to be leading in enforcement with the assistance of the coordination with other Canadian provincial regulating bodies, such as the Alberta Securities Commission.

It is not disjointed supervision. It is a unified mechanism which is meant to defend uniform regulation in the country.

What This Means For Insurance Advisors And Financial Professionals

We operate within strict compliance frameworks.

Insurance advice, investment commentary, and financial education must remain clearly separated. Social media does not change that obligation—it amplifies it.

For licensed insurance advisors in Canada, compliance is not optional. It protects clients, reputations, and long-term trust.

Media Inquiries And Public Communication Risks

Media amplification adds another layer of risk.

Content can be reshared, clipped, or quoted without context. Misinterpretation can trigger media inquiries and regulatory attention. Posting information casually can have lasting consequences.

Professional communication discipline matters more than ever.

The Future Of Finfluencing In Canada

The direction is clear.

Regulation is tightening. Power is under investigation. Even with disclosures of risks, investors are still susceptible to a persuasive message.

The situation of finfluencing in Canada is no longer a free-for-all. It belongs to the controlled financial system.

Early adopters will live.

The non-compliant people will find out by their own mistakes.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

The domestic securities law in Canada has influenced the finfluencer marketing rule and is applicable to Canadian securities administrators. Global trends vary inasmuch as the regulation is governed by CSA influencer rules, which are directed towards safeguarding investors in the Canadian provinces. The same material, which appears to be agreeable in other countries, is not necessarily in compliance with Canadian financial laws. Local compliance should be the first.

Yes–but only when confining oneself to the factual information without influencing investment decisions. Securities regulators might take the opinions as advice once they affect the behaviour of investors. The difficulty is how to differentiate between financial education and persuasion. The difference is in where the majority of compliance problems are.

Retail investors have a significant source of financial information through social media. There was more trading, which was directly associated with the influence of the internet. The response by CSA and CIRO guidance to that change is to expand coverage of protection standards to digital locations where investors now study and take action.

They can. In Canada, an insurance advisor must not overstep into the area of investment advice in the commentary on insurance. In a case where the financial products are overlapping, or the comparisons are going to affect the investment, then the compliance requirements rise. Both the advisor and the audience are secure within clear boundaries.

Failure to follow instructions exposes oneself to regulatory measures of securities regulators. Unregistered persons might be restricted, punished, or have a negative reputation. Firms and companies that are contacted by way of referral or promotion can also suffer breaches of compliance.

Even disclosed prejudices cause financial decisions to be skewed by conflicts of interest. The research has indicated that disclosures suggest decreasing but not annihilating influence over investors. This is why the regulators focus on the appropriate identification of interest and transparency, in particular, in cases with money or sponsored posts.

No, but they cause more severe questioning. Sponsored posts of financial products have to comply with laws on securities and disclosure standards. Registration can be necessary in case the promotion is similar to solicitation. Companies that cooperate with online personalities are jointly responsible in regard to compliant messaging.

Not entirely. Even general advice is regulated by the financial regulation if it has a scale effect. Regulators can interfere when the information in the content is used to make investment decisions without risk-taking. All the context, tone, and communication with the audience are important.

Effective and uniform regulation can ensure that investors in all the provinces of Canada are sheltered. It eliminates loopholes where checks and balances are slow to catch. Standardized standards also contribute to confidence in the Canadian capital markets and financial products in the long run.

Accountable leadership, boundary demarcation, and adherence. Promotion Finfluencers who do not promote but practice financial education minimize risk. The people who believe in regulation assist in developing trust among Canadians as well as safeguarding their own future in the finance arena.

Sources and Further Reading

Regulatory Guidance & Official Sources

- CSA And CIRO Finfluencer Guidance (Official Release)

https://www.securities-administrators.ca/news/csa-and-ciro-provide-guidance-for-finfluencers-and-firms-on-how-to-work-with-them-and-protect-investors/ - Joint CSA–CIRO Staff Notice On Finfluencer Activity

https://www.ciro.ca/newsroom/publications/joint-canadian-securities-administrators-and-canadian-investment-regulatory-organization-staff-notice - Canadian Securities Administrators – Finfluencers Resource Hub

https://www.securities-administrators.ca/investor-tools/finfluencers/

Provincial Securities Regulators

- Ontario Securities Commission – Finfluencer Research & Enforcement

https://www.osc.ca/en/investors/investor-protection/finfluencers - Ontario Securities Commission – Social Media & Investing Risks

https://www.osc.ca/en/news-events/news/osc-research-uncovers-concerns-about-finfluencers-power-persuasion - Alberta Securities Commission – Investor Alerts & Social Media Risks

https://www.albertasecurities.com/investors/investing-basics/investor-alerts

Investor Protection & Financial Education

- GetSmarterAboutMoney.ca (OSC-Backed Education Platform)

https://www.getsmarteraboutmoney.ca/ - CIRO – Investor Protection & Advisor Oversight

https://www.ciro.ca/investors - CSA – Understanding Securities Regulation In Canada

https://www.securities-administrators.ca/about-csa/

Compliance, Registration & Advisor Standards

- CIRO Registration & Compliance Requirements

https://www.ciro.ca/registration - Client-Focused Reforms Overview (CIRO)

https://www.ciro.ca/industry/compliance/client-focused-reforms - Securities Law Basics For Registrants

https://www.securities-administrators.ca/securities-law/

Industry Commentary & Analysis (Credible Media)

- Investment Executive – CSA & CIRO Finfluencer Coverage

https://www.investmentexecutive.com/news/csa-ciro-post-finfluencer-guidance/ - Wealth Professional – Finfluencer Regulation In Canada

https://www.wealthprofessional.ca/news/industry-news/regulators-tighten-rules-for-canadas-growing-cohort-of-finfluencers/391125

Global Context (Supporting Authority)

- IOSCO Report On Finfluencers And Investor Harm

https://www.iosco.org/library/pubdocs/pdf/IOSCOPD795.pdf

Key Takeaways

- Financial influencers’ Canada regulations are no longer theoretical.

CSA and CIRO guidance confirms that social media activity can trigger securities laws when content influences investment decisions, even without formal credentials. - Finfluencer marketing rulesin Canada focus on behaviour, not intent.

Emojis, hype language, replies to investor inquiries, and promotional framing can all be interpreted as investment advice by securities regulators. - Disclaimers do not replace compliance.

Saying content is “educational only” does not prevent registration or disclosure obligations once advice affects trading activity or financial decisions. - Conflicts of interest remain a central enforcement risk.

Sponsored posts, referral arrangements, and undisclosed interests continue to undermine investor protection, even when partially disclosed. - CSA and CIRO are coordinating enforcement nationally.

The guidance supports efficient and consistent regulation across Canada’s provinces, reducing loopholes and increasing accountability. - Retail investors are more susceptible to influence than expected.

Research shows social media messaging significantly impacts investing behaviour, reinforcing why regulators are tightening oversight. - Licensed professionals face higher expectations online.

A licensed insurance advisor in Canada must maintain clear boundaries between financial education and regulated advice to avoid compliance exposure. - The future of finfluencing favours discipline, not reach.

Creators who respect regulation, prioritize factual information, and manage influence responsibly are better positioned to operate long-term.

Your Feedback Is Very Important To Us

IN THIS ARTICLE

- Finfluencers Hit by New CSA CIRO Rules In Canada

- Finfluencers And Financial Education: Where Information Crosses Into Advice

- Investor Inquiries And The Moment Registration Is Triggered

- Securities Regulators Are Watching Social Media Closely

- What Makes A Financial Influencer Regulated In Canada

- Client-Focused Reforms And Why They Apply To Finfluencers

- Retail Investors Are More Influenced Than They Think

- CSA And CIRO: How The New Guidance Changes The Game

- Financial Products, Sponsored Posts, And Referral Arrangements

- Online Personalities Versus Licensed Financial Advisors

- Conflicts Of Interest Must Be Disclosed—Properly

- Ontario Securities Commission And Provincial Enforcement Reality

- What This Means For Insurance Advisors And Financial Professionals

- Media Inquiries And Public Communication Risks

- The Future Of Finfluencing In Canada

Sign-in to CanadianLIC

Verify OTP