- Connect with our licensed Canadian insurance advisors

- Schedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

Can You Use Your TFSA To Buy A Life Annuity In Canada In 2026? Here’s What To Know

By Pushpinder Puri

CEO & Founder

- 13 min read

- February 23rd, 2026

SUMMARY

The article explains how Canadians can use funds from a Tax Free Savings Account in Canada to buy a life annuity and create guaranteed income for retirement. It outlines TFSA withdrawal rules, the TFSA contribution limit, and the role of Life Insurance companies in providing annuity payments. It also compares a Tax Free Savings Account vs an RRSP, highlights interest rates’ impact, and offers insights on structuring retirement savings for long-term financial security.

Introduction

We work with a lot of clients who have accumulated significant savings inside their Tax Free Savings Account (TFSA), and they are approaching retirement and wondering if that pool of money can create a reliable lifetime income. In these times of inflation, increased longevity and market volatility, Canadians are looking more than ever for predictable solutions that both protect capital and comfort.

As of 2024, there are now over 15 million Canadians with a TFSA (Statistics Canada). Yet little is understood about how these accounts interact with life annuities — one of the oldest, most durable forms of guaranteed income that can be purchased from a Life Insurance company.

We’ll go over what you can do, or more possibly can’t do in 2026; how the rules work and what to consider before using your TFSA to buy an annuity.

Understanding The Tax-Free Savings Account (TFSA)

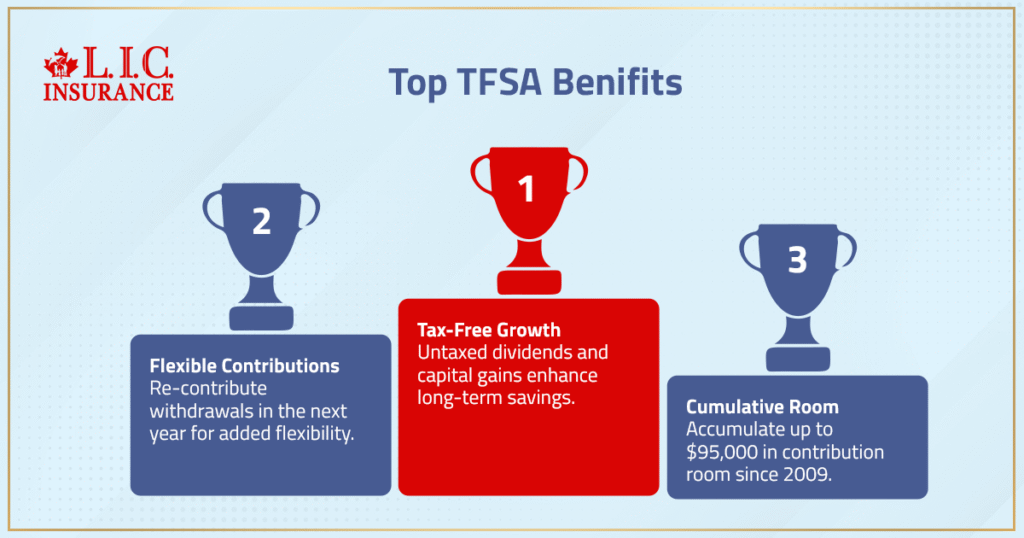

The Tax Free Savings Account Canada program was launched in 2009, giving Canadians the ability to save for retirement in a flexible, tax-sheltered environment. The CRA 2026 TFSA contribution limit stands at $7,500 — meaning anyone eligible since the program launched in 2009 now has a total of $95,000 in cumulative room.

Contrast the tax-free savings account vs RRSP showdown,” where RRSPs provide an upfront deduction but are then taxed, whereas TFSA withdrawals are completely tax-free. This is what makes TFSAs a powerful vehicle for both short-term liquidity and long-term income planning.”

You can only re-contribute your TFSA withdrawal amount in the same year if you still have unused TFSA room; otherwise, the room is restored January 1 of the next year. Anything that grows — interest, dividends, capital gains — is left entirely untaxed.

What Is A Life Annuity?

A life annuity is an agreement with the insurance company in which you hand over a lump sum in exchange for a guaranteed income stream that continues as long as you do. Basically, you swap savings for certainty — no market ups and downs, no guessing, just steady annuity payments wired straight into your account.

Annuities are being revisited by retirees as a way to mitigate outliving their retirement savings (Canadian Life and Health Insurance Association [CLHIA], 2024). Life Insurance companies will use actuarial tables and current interest rates to figure out what your monthly payments should be to last as long as you live, or for a guaranteed period if that’s the option you choose.

Can You Use TFSA Funds To Buy A Life Annuity?

Here’s where clarity matters:

While you generally cannot convert a TFSA directly into an immediate life annuity with most providers, certain annuity contracts are technically TFSA-eligible under the Income Tax Act. In practice, most Canadians withdraw TFSA funds tax-free and then use those funds in a non-registered account to purchase a life annuity.

This two-step withdrawal/purchase process is fully legal, but the tax consequences and timing rules under the TFSA regime must be understood clearly.

How Annuities Work With Withdrawn TFSA Funds

After you take money out of your TFSA, it’s regular cash. At that time, they have the ability to purchase a deferred annuity, term certain annuity or single-life annuity from an approved annuities provider or financial institution.

This is how annuities work: You contribute a lump sum, and in return, the insurer provides regular income payments for life or for however long you want, and yes, this locks them into a fixed period. These payments also persist during a market decline, providing a buffer of stability.

The tax-free shelter is lost once the money exits the TFSA, but you still get guaranteed retirement income – a fair trade-off for many Canadians who are more interested in peace of mind as opposed to potential sweetened upside.

Comparing TFSA Withdrawals And RRSP Conversions

When comparing a Tax-Free Savings Account vs. an RRSP, the difference is straightforward:

- RRSP funds eventually convert into a Registered Retirement Income Fund (RRIF) or can be used to purchase an annuity.

- TFSA withdrawals are tax-free and do not count as taxable income.

But you must keep this crucial rule accurate:

TFSA withdrawals are always tax-free, and the amount withdrawn is added back to your TFSA room on January 1 of the next calendar year unless you still had unused TFSA room. RRSP withdrawals, by contrast, never create new contribution room.

That means TFSA withdrawals can help fund a life annuity without pushing you into a higher tax bracket — but the annuity income itself is taxable and can affect your income-tested government benefits.

The Role Of Guaranteed Income In Retirement Planning

Something we regularly remind clients at Canadian LIC: volatility is the price of growth, predictability brings comfort. A guaranteed income stream from a life annuity can be the foundation of your retirement recipe, especially if you already have the basic expenses covered.

Annuities, when added to CPP and OAS, can help make sure you have enough to cover essentials like housing costs, groceries and health care — protecting you from market volatility while generating a steady income no matter the economic environment.

Understanding The Annuity Contract

Every annuity contract outlines how income payments are structured, how long payments continue, and whether there’s a death benefit. You’ll choose between:

- Single Life Annuity – payments end at death.

- Joint Annuity – payments continue to a surviving spouse.

- Term Certain Annuity – guarantees income payments for a set guaranteed period (e.g., 10 or 20 years).

- Deferred Annuity – begins payments later, allowing growth before income starts.

Most Life Insurance companies in Canada — such as Canada Life, Sun Life, and Manulife — offer variations tailored to different income needs, life expectancy, and retirement income goals.

Evaluating Interest Rates And Market Conditions

Annuity income is predominantly a function of interest rates. When rates are higher, those selling annuities can promise bigger regular payments because they earn more on the underlying investments.

The C.B.O.C.’s monetary policy outlook for 2026 implies a plateauing or modestly decreasing rate, which, if that happens, should mean you may get stronger guaranteed income payments by buying an annuity sooner.

We study rate trends across every Life Insurance company before recommending timing, since anywhere between a 0.5 per cent swing can potentially cost you thousands over your lifetime.

The Importance Of The Initial Investment And Guaranteed Period

The larger your upfront annuity purchase and the longer the guarantee period, the larger (or smaller) your monthly payments will be:

- A longer guarantee = lower monthly income

- A shorter guarantee = higher monthly income

Balancing these trade-offs is essential.

Tax Implications Of Using TFSA Funds

Here is the corrected and accurate tax treatment:

If you withdraw money from a TFSA, that withdrawal is tax-free.

However, once those funds are used to buy a non-registered annuity, each annuity payment includes a taxable portion (interest component):

- Prescribed annuity = level taxation

- Non-prescribed annuity = higher tax at first, gradually decreasing

The TFSA withdrawal itself is tax-free, so it doesn’t affect your tax bracket. The taxable portion of life annuity payments purchased with TFSA funds may influence your tax bracket and how much pension income tax credit you can actually use.

When Buying An Annuity Makes Sense

It will be attractive for you if you like certainty in investment income, avoid volatile investments and reduce the stress of monitoring market activity in retirement.

It is also great for clients with sufficient liquidity already in place for emergencies. Those leaning on their TFSA exclusively for growth, however, may best be served by a diversified mutual fund or balanced portfolio instead of life annuities.

Annuity providers and rate tables will vary by financial institution, so it’s a good idea to shop around for an annuity before signing up. Given the importance of this matter, our consultants frequently request multiple TFSA quote online illustrations from several of the best Life Insurance companies to help ensure you’re not leaving critical money on the table.

Joint Annuity Options For Couples

Joint annuities cover two lives under one contract. Payments continue for as long as either spouse is alive, making them a cornerstone product for couples who rely on shared income to maintain household stability.

A joint life annuity can also qualify for the pension income tax credit after age 65, allowing couples to maintain a steady lifetime income while optimizing tax efficiency.

We often recommend joint structures when one partner depends on the other’s retirement income or when the goal is to ensure consistent financial support after the first spouse passes away.

Understanding How Annuities Fit Into A Broader Financial Plan

Buying an annuity isn’t just about securing income; it’s about building a coordinated financial plan that blends liquidity, growth, and stability.

We help clients integrate Life Insurance, Registered Retirement Savings Plans, and Tax-Free Savings Accounts to create a layered retirement income strategy. For example:

- TFSA for flexible withdrawals and tax-free growth

- RRSP or RRIF for structured retirement income

- Life annuity for a lifelong, guaranteed regular income

Together, these pillars ensure you always have enough income to cover basic expenses while preserving long-term security.

Deciding When To Buy An Annuity

Timing matters. When to buy an annuity depends on interest-rate cycles, life expectancy and your income needs.

On average, for the typical Canadian between the ages of 60 and 70, the most favourable balance of guaranteed income versus lump-sum cost is. Purchase too early, and you restrict liquidity; wait too long, and you expose yourself to the possibility that less money will provide financial support for fewer years of income payments.

“We frequently do side-by-side projections of the variable annuity versus a fixed income strategy to illustrate how annuities work in varying interest rate environments. It’s how clients can make decisions without resorting to guesswork.

Professional Guidance Before You Act

The use of TFSA money for a life annuity requires so much in the way of moving parts (withdrawals, taxes, timing, transfer of funds within financial institutions and insurance policy selection) that dealing with these issues on advisement is crucial.

Compare Annuity Providers, Interest Rates, and After-Tax Income Payments. Our licensed advisors do the work to provide you with all information up front – there are no surprises or hidden details for you to uncover.

Customized financial planning provided to retiring individuals increases their confidence of reaching desired retirement income by 30% (Financial Consumer Agency of Canada, 2026). For that outcome, every Canadian must fight.

The Bottom Line

You cannot simply buy a payout annuity inside a TFSA account with most providers. But:

You can withdraw funds from your TFSA tax-free and use them to purchase a life annuity from a reputable life insurance company.

When executed correctly:

- Your TFSA continues to grow tax-free

- Your annuity provides guaranteed lifetime income

- Your overall retirement income becomes more predictable

It is our job to assist you in weighing options, projecting outcomes and constructing a plan where guaranteed income, flexibility and tax efficiency all work together.

When income becomes predictable, retirement becomes less about uncertainty — and more about the freedom you’ve earned.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

No, a Tax Free Savings Account Canada can’t directly hold a life annuity. However, you can withdraw funds tax-free and then buy an annuity through a Life Insurance company. The resulting annuity payments provide guaranteed income that complements your other retirement savings.

When interest rates rise, annuity providers can offer higher monthly payments because they earn more from investments. If rates fall, guaranteed income payments will generally decrease. That’s why comparing TFSA quote online options and timing your initial investment matters before buying an annuity.

Once a life annuity starts, the income payments are fixed, so your lump sum can’t be withdrawn. To keep flexibility, many clients hold a portion of funds in mutual funds or registered retirement savings plans for liquidity, while using the annuity for a steady income that covers basic expenses.

Yes. A joint annuity allows both partners to receive income payments for life, ensuring the survivor receives guaranteed lifetime income. This structure can also qualify for the pension income tax credit, making it a practical way to maintain a regular income within your long-term financial plan.

A prescribed annuity spreads income tax evenly over time, giving smoother annuity payments, while a non-prescribed one starts higher and tapers off. Choosing the right type depends on your retirement income goals and overall financial plan. We can illustrate both options before you purchase an annuity.

Yes. You can use tax-free withdrawals from your Tax Free Savings Account Canada to purchase a deferred annuity through a licensed Life Insurance company. This lets your initial investment grow before income payments begin, offering a balance between flexibility and future guaranteed income.

TFSA withdrawals do not affect OAS or GIS because they are not taxable income; however, once TFSA funds are used to purchase a non-registered life annuity, the taxable portion of annuity income is included in your net income and may affect OAS clawbacks, while CPP entitlement remains unchanged.

Yes, if you’re over 65, some annuity income may qualify for the pension income tax credit. This applies to certain life annuities or joint annuities providing regular income payments. Proper planning helps maximize available tax credits while securing a guaranteed regular income for retirement.

Life Insurance companies calculate annuity income using their own interest rates and mortality assumptions. Comparing multiple annuity providers helps identify who offers the best guaranteed income for your initial investment. We review rates across top insurers to ensure you get more money for your retirement savings.

Absolutely. Many Canadians pair a life annuity with registered retirement savings plans or mutual funds to create a diversified retirement income stream. This mix provides both steady income and flexibility, allowing you to cover basic expenses while keeping some funds accessible for long-term goals.

Key Takeaways

- You cannot directly buy a life annuity inside a Tax Free Savings Account Canada, but you can withdraw funds tax-free and use them to purchase one.

- The TFSA withdrawal rules allow flexibility—withdrawn funds can later be recontributed, keeping your retirement savings tax-efficient.

- Life Insurance companies provide annuity payments that create guaranteed income for life, helping cover basic expenses in retirement.

- Interest rates play a major role in determining annuity income, making timing and comparison among annuity providers essential.

- Choosing between a Tax Free Savings Account vs an RRSP option depends on your income level, tax implications, and long-term financial plan.

- Joint annuity and guaranteed period options can protect spouses and ensure steady income payments continue after one partner’s passing.

- A life annuity offers stability against market fluctuations and supports consistent retirement income goals for Canadians in 2026.

- Consulting a financial advisor before buying an annuity ensures the right structure for guaranteed lifetime income and sustainable retirement planning.

Sources and Further Reading

- Canada Revenue Agency (CRA) – Tax Free Savings Account (TFSA) Rules and Contribution Limits 2026

https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tfsa.html - Statistics Canada – Retirement Savings and Income Statistics 2024 Report

- Canadian Life and Health Insurance Association (CLHIA) – Factbook 2024: Annuity and Insurance Industry Overview

https://www.clhia.ca/ - Bank of Canada – Monetary Policy Report 2026: Interest Rate Trends and Inflation Outlook

https://www.bankofcanada.ca/ - Financial Consumer Agency of Canada (FCAC) – Annuities and Retirement Income Planning Guide

https://www.canada.ca/en/financial-consumer-agency.html - Office of the Superintendent of Financial Institutions (OSFI) – Guidelines on Life Insurance and Annuity Providers in Canada

https://www.osfi-bsif.gc.ca/ - Investment Industry Regulatory Organization of Canada (IIROC) – Understanding Registered and Non-Registered Accounts

https://www.iiroc.ca/ - Government of Canada – Canada Pension Plan (CPP) and Old Age Security (OAS) – Retirement Income Benefits and Eligibility

https://www.canada.ca/en/services/benefits/publicpensions.html

Feedback Questionnaire:

We’d love to understand your experience and the challenges you face with tax filing in Canada.

Your feedback helps us guide families with clearer, more practical tax planning support.

IN THIS ARTICLE

- Can You Use Your TFSA To Buy A Life Annuity In Canada In 2026? Here’s What To Know

- Understanding The Tax-Free Savings Account (TFSA)

- What Is A Life Annuity?

- Can You Use TFSA Funds To Buy A Life Annuity?

- How Annuities Work With Withdrawn TFSA Funds

- Comparing TFSA Withdrawals And RRSP Conversions

- The Role Of Guaranteed Income In Retirement Planning

- Understanding The Annuity Contract

- Evaluating Interest Rates And Market Conditions

- The Importance Of The Initial Investment And Guaranteed Period

- Tax Implications Of Using TFSA Funds

- When Buying An Annuity Makes Sense

- Joint Annuity Options For Couples

- Understanding How Annuities Fit Into A Broader Financial Plan

- Deciding When To Buy An Annuity

- Professional Guidance Before You Act

- The Bottom Line

Sign-in to CanadianLIC

Verify OTP