- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

- Is Infinite Banking A Smart Financial Strategy?

- Understanding the Infinite Banking Concept

- Why Infinite Banking Appeals to Canadians Seeking Financial Freedom

- How Infinite Banking Strategy Helps Build Financial Independence

- Challenges and Misconceptions About Infinite Banking

- Who Should Consider Infinite Banking for Financial Freedom?

- How to Start Your Infinite Banking Journey

- Key Advantages of the Infinite Banking Strategy

- A Day-to-Day Struggle: Why More Canadians Are Exploring Infinite Banking

- Potential Drawbacks You Should Know

- The Future of Infinite Banking in Canada

- Is Infinite Banking a Smart Financial Strategy?

COMMON INQUIRIES

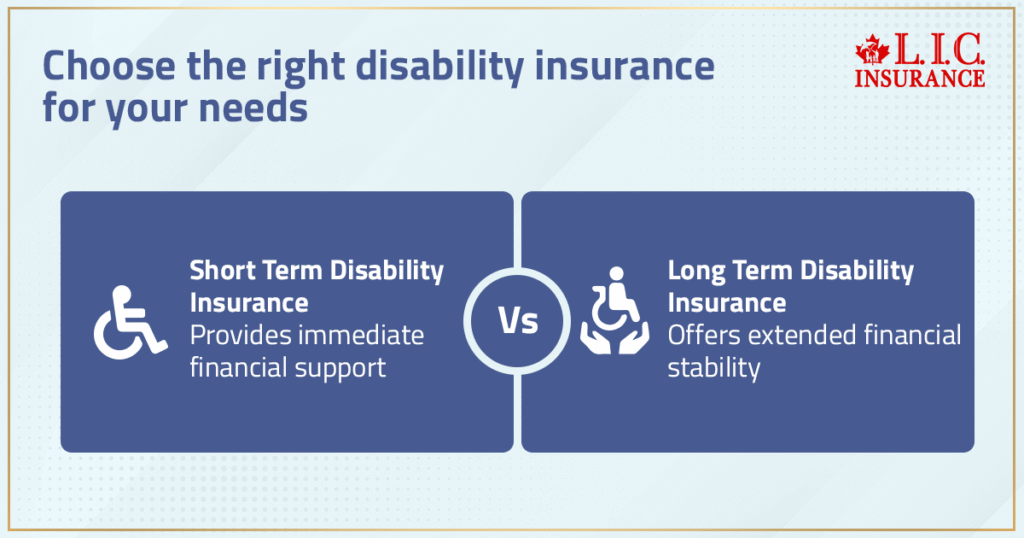

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- What is the minimum income for Term Insurance?

- How Does Income Affect Your Term Life Insurance Policy?

- Can You Buy Term Life Insurance Online with a Low Income?

- How Can You Lower Your Term Life Insurance Cost?

- How Much Term Life Insurance Do You Need?

- Can Your Term Life Insurance Policy Be Adjusted Over Time?

- Why Term Life Insurance Is Ideal for Lower-Income Canadians

- Final Thoughts

- More on Term Life Insurance

New 2026 Super Visa & Family Sponsorship Rules: What Higher Income Thresholds Mean for Canadians

By Pushpinder Puri

CEO & Founder

- 12 min read

- March 26th, 2026

SUMMARY

Canada’s 2026 Super Visa and Family Sponsorship updates increase the minimum income thresholds for Canadian citizens and permanent residents hosting parents and grandparents. The article explains new LICO levels, how family size and dependent children affect eligibility, and why health insurance coverage is essential. It details Super Visa Insurance requirements, Super Visa Insurance cost calculator tips, Super Visa Insurance Monthly Payment options, and Parent Super Visa Insurance Plans in Canada.

Introduction

Families all over Canada have been relying on the Super Visa to reunite with mothers and fathers, grandmothers and grandfathers. But 2026 has introduced its own wrinkles to the process, even as it redesigns how income thresholds are adjusted and how insurance rules function. Sponsors must now hit a higher bar to bring loved ones to stay long-term, with the federal government raising the minimum necessary income.

IRCC updates the Super Visa minimum necessary income table periodically, and the latest published update (July 29, 2026) raised the required amounts for most family sizes. For the vast majority of people from Canada, it now requires financial planning, proof of income and Super Visa Insurance.

We are looking at this as a policy change. It’s a fresh chance to set families up for success. No matter whether you are looking into the best Super Visa Insurance Canada or comparison-shopping through a Super Visa Insurance cost calculator, changes such as these relate directly to your financial preparedness.

Why The Higher Income Thresholds Matter

The Super Visa program has always been modelled on the principle that visitors are allowed to stay in Canada — typically parents and grandparents — without being dependent on public resources. Along with its 2026 update, the minimum income levels have increased so that sponsors need to earn several thousand dollars more than previously.

For example, under IRCC’s updated table (July 29, 2026), a family size of 3 requires $46,720, and a family size of 4 requires $56,724 in funds.

These figures come from IRCC’s published “minimum necessary income requirements” table for Super Visa hosts. The objective is straightforward: To make it possible for Canadian hosts to financially host their visitors without any hardship.

We like to remind our clients that these aren’t just numbers on a piece of paper. It might only be a few hundred dollars, but falling short could trigger a visa refusal. When officers consider an application, they weigh a household income source, verification of employment and supporting tax forms. That’s why we recommend that sponsors collect full documentation — from pay stubs to the Canada Revenue Agency notice of assessment — as a way of assessing financial reliability.

Counting Family Members Correctly

Minimum income is based on “family size” as calculated under IRCC’s Super Visa rules. According to IRCC standards, you must provide for yourself, your spouse or common-law partner, your dependent children (if they are not already sponsored under this application), the parent or grandparent applying for the Super Visa, plus anyone you previously sponsored and remain financially responsible for.

Here’s where many families fall short. You are married and have two children, and you want to invite one parent. Your family size is not four — it is five, because IRCC counts everyone in the household plus the visiting parent.

Under the same July 29, 2026, update, a family size of 5 requires $64,336. This is a step that can be easily overlooked, but even miscounting one person can render the application invalid. We know of applicants who were approved simply by recalculating family size correctly or including a co-signer’s income to meet the new threshold.

Connection To The Parents And Grandparents Program

The Super Visa is often confused with the Parents and Grandparents Program (PGP). The distinction matters. The PGP leads to permanent residency, while the Super Visa allows multiple entries for up to 10 years, with stays of up to five years per visit.

For the Parents and Grandparents Program (PGP), sponsors must prove they meet IRCC’s income requirement for each of the three tax years immediately preceding the application, using CRA Notices of Assessment.

Because PGP intake is capped and highly competitive, many families turn to the Super Visa as a faster way to reunite while remaining compliant with income and insurance rules.

For those families, they need to know that the way to prove an income that is sufficient, without needing to account for every element of cost, and how to get valid health insurance, are key. Each third-party sponsor may provide evidence of financial solvency for the period, and that the visiting parent has sufficient medical insurance. That’s where Canadian LIC comes in — to help keep both sides compliant with the law.

Health Insurance: The Non-Negotiable Requirement

The foundation of the Super Visa is its insurance rule. Applicants must show proof of private health insurance that meets federal standards.

Applicants must show proof of health insurance from either a Canadian insurance company or a foreign insurance company that is OSFI-authorized, federally regulated, and that issued the policy in the course of its insurance business in Canada.

This insurance must:

- Cover a minimum of $100,000 for health care and hospitalization

- Cover health care, hospitalization and repatriation

- Be valid for a minimum of 1 year from the date of entry

- Be paid in full, or paid in instalments with a deposit (quotes are not accepted)

Private health insurance must be valid for each entry to Canada, and applicants should be prepared to show proof of paid insurance to a border services officer on arrival.

We recommend policies that exceed the minimum requirement, especially for longer stays or applicants with medical histories. The best Super Visa Insurance Canada isn’t always the cheapest — it’s the one that protects both the visitor and the host from financial exposure.

Without valid insurance in force, an applicant can be refused for non-compliance, and a Super Visa holder may be questioned at entry if they can’t show proof of paid coverage.

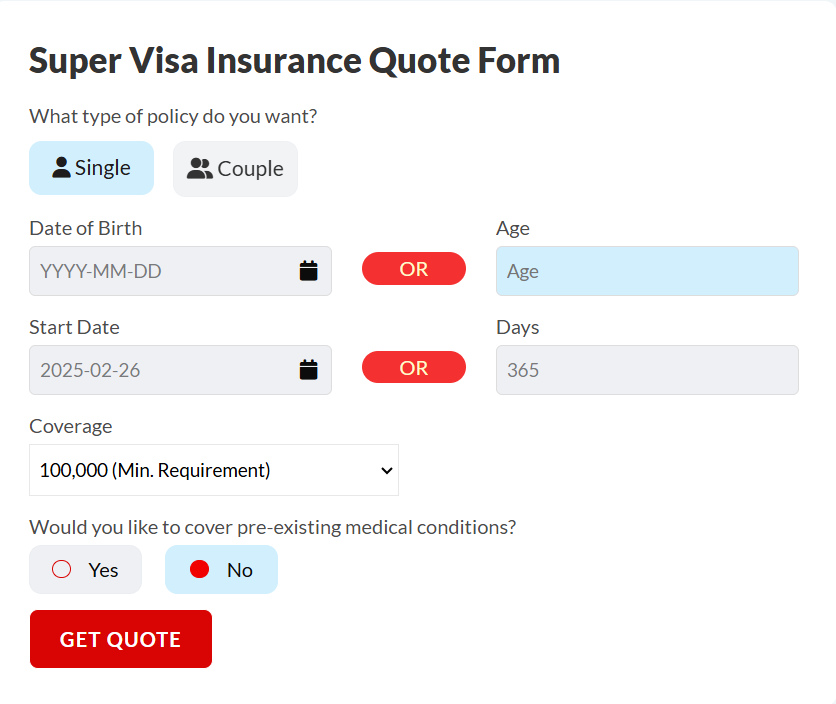

Estimating Super Visa Insurance Costs

The cost of a Parent Super Visa Insurance in Canada varies based on age, health background and length of coverage. Annual premiums typically run between $1,800 and $3,600 for most healthy visitors aged 55 to 65. Applicants who are older or who have pre-existing conditions may be charged higher rates.

Sponsors can estimate potential premiums by using a Super Visa Insurance cost calculator. Helpful hints. This tool allows you to calculate the rate either first monthly or yearly, so you can better budget your Super Visa Insurance Monthly payment.

Most insurance companies now offer flexible payment options, allowing you to spread costs across the year. We help families compare quotes side by side to ensure that every policy meets the required standards and fits the family’s budget.

The bottom line: We can not cover it. All Super Visa applicants need to provide proof of a paid policy prior to arriving.

The Host’s Responsibilities

The host must be a Canadian citizen or permanent resident living in Canada. Responsibilities include providing proof of income, issuing an invitation letter and demonstrating the ability to financially support the visitor.

IRCC allows the host’s spouse or common-law partner (if they are a Canadian citizen or permanent resident) to co-sign the invitation letter so combined income can be used to meet the minimum necessary income.

As a reputed broker, we’ve witnessed many scenarios where an income recalculation and an insurance policy structured correctly led to the potential decline actually being approved! Precision matters here.

How To Meet The Minimum Income Requirements

To calculate the minimum income, we use the number of people you are responsible for supporting. For family sizes above seven, IRCC adds $8,224 for each additional person. To establish eligibility, you need to demonstrate your gross income, not net. Just pay stubs won’t do; pair them with CRA documents and a letter from your employer verifying when you were hired, your job title and your annual income.

If you fall just short — right on the bubble when it comes to what qualifies as a good income — consider having a co-signer (like your husband or wife) apply with you. This is allowed by IRCC, and the sum total usually makes families eligible under the LICO for the Super Visa level.

For self-employed Canadians, Canadian LIC recommends including business financials, bank statements and letters from accountants verifying annual earnings. “When you can show consistent income and how the cash flows, officers tend to find the application more credible.

Application Process: Step-by-Step

- Determine Eligibility Criteria – Ensure you are a Canadian citizen or permanent resident aged 18 or older, living in Canada, and meeting the minimum income standards.

- Count Your Family Size – Include all dependents, your partner, and the visiting parent or grandparent.

- Calculate Minimum Gross Income – Match your family size to the current LICO table and confirm you exceed the amount.

- Gather Proof Of Income – Submit pay stubs, tax returns, and letters from employers or accountants.

- Buy Health Insurance – Secure a Super Visa Insurance quote, confirm coverage for a minimum of $100,000, and keep the payment receipt ready.

- Prepare Invitation Letter – Clearly state the relationship, duration of stay, and promise of financial support.

- Submit Application – The Super Visa applicants apply from their home country with all documents and medical exams completed.

Each file undergoes a financial review and may be returned if the proof of income or insurance documentation is incomplete. We regularly help families review every page before submission to reduce errors.

What If You Don’t Meet The Threshold?

If your income falls below the minimum required, don’t freak out. You have options. You can wait to apply until your next tax year demonstrates a higher income, or add someone, like a spouse, as a co-signer.

Families sometimes time it so that one dependent child graduates from school and no longer counts toward the minimum income levels. We usually guide clients to these strategies so that we are not just doing disincentives and forcing the issue.

Remember: You can always reapply once you are able to meet the financial requirement, even if your application is rejected due to income. And insurance bought on the first application can typically be backdated for the new application, so you don’t lose all of your premium.

Impact On Parents And Grandparents

A Super Visa can allow stays of up to 5 years per entry, with multiple entries over up to 10 years, depending on the document issued and the traveller’s situation (for example, visa-exempt travellers may receive a letter instead of a visa counterfoil).

There is a critical role here for insurance as well. Super Visa Insurance must be valid for the entire period each time the visitor comes; as such, it will need to be renewed if they stay longer or make a repeat visit to Canada. It means advance planning is crucial — something Canadian LIC excels at.

Practical Tips From Canadian LIC

- Start Early – Begin collecting income proof and insurance quotes months before you apply.

- Use A Calculator – Test a Super Visa Insurance cost calculator to understand how age and coverage affect costs.

- Stay Transparent – Declare all income sources honestly; officers verify figures against CRA records.

- Budget for Insurance – Even with a Super Visa Insurance Monthly Payment, remember the first installment must be made before submission.

- Consult Professionals – A licensed broker can explain options for pre-existing conditions or multi-year plans.

Why Canadian LIC Supports The New Standards

Some view the higher threshold as a hurdle, and what we see is an opportunity to help families avoid financial hardship. ‘If you know what the standards are, you can plan smarter and have sustainability over the long term.’ They also mean parents and grandparents coming to visit Canada have access to quality medical care without being too much for their sponsor.

For years, Canadian LIC has assisted families through all Super Visa policy updates. We review income statements, ensure compliance with policies and compare a variety of insurance options in order to provide the best value for our clients. We are here to ensure that nothing falls between the cracks when it comes to policy fine print and immigration criteria.

Final Insights

The new 2026 Super Visa rules are a reminder of one thing: Bringing families together in Canada is about heart and discipline. It’s the love for your parents and grandparents versus financial readiness and policy accuracy.

By satisfying the higher income requirement, you prove that you are able to fulfill this financial obligation; by fulfilling the insurance criteria, you secure protection for your family in case of an unexpected death. In combination, these two steps build a solid base for long-term visits and peaceful reunions.

As we assist Canadian families every day, our message stays consistent—plan early, document carefully, and invest in proper coverage. The effort you put in today will reward you with worry-free time with your loved ones tomorrow.

Get The Best Insurance Quote From Canadian L.I.C

Call +1 416-543-9000 to speak to our advisors.

Get Quote Now

FAQs

In addition to their CRA tax forms, applicants can also submit detailed pay stubs, recent bank statements, and employment confirmation letters that demonstrate they make the minimum gross income specified by IRCC standards. Those who share their income with a spouse or common-law partner must attach the documents for both to establish that earnings are relatively stable.

Yes. Even the addition of a single dependent child to your household increases your minimum income threshold based on IRCC’s chart. Many Canadians don’t realize that children from a previous relationship still count when it comes to Super Visa eligibility.

A co-signer — your spouse, for example, or a common law partner — can help you use combined income to qualify under the higher 2026 thresholds. It’s a savvy approach for Permanent Residents and low-income Canadian citizens to fulfill the minimum required income without the Super Visa being put on hold.

If you are approved with an annual income and it drops afterwards, the Super Visa holder may still be allowed entry into Canada, but following renewals might come under heavy testing. Ideally, you want to have the least amount of money that could meet the threshold that you’ve presented to IRCC and ensure that those bank statements and current pay stubs continue to prove your financial wherewithal.

Apart from meeting IRCC demands, private health insurance protects Super Visa holders from expensive emergency care in Canada. Good health insurance that covers all aspects of health care and unexpected medical expenses, adequate to satisfy the mandatory minimum coverage required by the immigration authorities, is necessary.

Yes, the parents and grandparents program is more strict and requires higher cut-offs, plus 3 years of stable income proof. Sponsors have to prove that they meet or surpass the minimum gross income on an annual basis — something Canada Revenue Agency assessments will confirm — before providing permanent financial support to family members.

Absolutely. If you have sponsored someone before, and they are still on the go with their application, IRCC includes them in your family members ‘ number. This means your income requirement increases accordingly, and you will need to provide more proof of income when reapplying for a new Super Visa sponsorship.

Your family members (ie, you, your host’s spouse, and dependent children, including any invitation letter Super Visa applicants) together determine what your minimum income needs to be. The more people in your household, the higher your minimum income will be, so accuracy can save Super Visa applicants and their sponsors from disaster.

Super Visa holders can be in Canada for up to five years per visit, but are required to have valid health insurance while they remain in the country. IRCC consider that people will return their status or apply for extension before it ends, and each Super Visa application should be compliant with Canada’s visitor rules.

Insurance Brokers have been assisting families to meet the requirements by arranging for them to secure private health insurance that complies with IRCC. They help host individuals through the process of preparing proof for income, and they review the minimum required income according to their service description, supporting criteria (no reference is made to offer explanation _ Super Visa programs provide Canadian citizens & permanent residents with a flexible option.

Sources and Further Reading

- IRCC – Super Visa: Parents and Grandparents Program Overview

Learn about eligibility, the application process, and financial requirements for the Super Visa.

👉 https://www.canada.ca/en/immigration-refugees-citizenship/services/visit-canada/parent-grandparent-super-visa.html - Government of Canada – Family Sponsorship: Sponsor Your Parents and Grandparents

Details on how to apply for permanent residency for parents or grandparents under the Family Sponsorship program.

👉 https://www.canada.ca/en/immigration-refugees-citizenship/services/immigrate-canada/family-sponsorship/sponsor-parents-grandparents.html - IRCC – Required Documents for Super Visa Applicants

A detailed checklist for hosts and applicants, including proof of income and health insurance documentation.

👉 https://www.canada.ca/en/immigration-refugees-citizenship/services/visit-canada/parent-grandparent-super-visa/eligibility.html - CIC News – 2026 Financial Requirement Increase for Parents and Grandparents Visiting Canada

Explains the July 2026 adjustment to LICO levels and its effect on Canadian sponsors.

👉 https://www.cicnews.com/2026/07/government-increases-financial-requirements-to-host-parents-and-grandparents-visiting-canada-0758326.html - Statistics Canada – Income Data and Cost of Living Trends (2026)

Background data supporting income threshold adjustments and national affordability trends.

👉 https://www150.statcan.gc.ca/t1/tbl1/en/tv.action?pid=1110023901 - Manulife – Visitors to Canada and Super Visa Insurance Plans

Coverage details, eligibility, and claim process for Super Visa health insurance.

👉 https://www.manulife.ca/personal/insurance/travel-insurance/visitors-to-canada.html

Key Takeaways

Higher 2026 Income Thresholds:

The Government of Canada has raised the minimum necessary income for hosts under the Super Visa and Family Sponsorship programs, affecting eligibility for many Canadian citizens and permanent residents.

Family Size Matters More Than Ever:

The total number of family members directly determines how much income you must show. Even dependent children or previously sponsored individuals still count when calculating the required income.

Proof Of Financial Stability Is Crucial:

Sponsors must provide verified proof of income through CRA Notices of Assessment, bank statements, pay stubs, or an accountant confirming annual income to meet the updated income requirements.

Health Insurance Is Mandatory:

Every Super Visa applicant must have a valid Health Insurance Policy that provides at least CAD 100,000 in coverage, including hospitalization and repatriation. Policies must be issued by an approved Canadian insurer or one regulated by OSFI.

Choose The Right Insurance Plan:

Selecting the best Super Visa Insurance Canada involves comparing benefits, deductibles, and coverage terms. Use a Super Visa Insurance cost calculator to estimate premiums and check if a Super Visa Insurance Monthly Payment option suits your budget.

Co-Signing Can Help:

If your income falls short, a spouse or common-law partner can co-sign to combine incomes and meet the minimum income requirements for Super Visa sponsorship.

Stay Compliant With All Documentation:

Keep accurate records of your Super Visa Insurance quote, income proof, and completed application process. Missing or outdated documents can delay approval or cause refusal.

Grandparents Program Remains Limited:

The Parents and Grandparents Program continues to have strict quotas, making the Super Visa program the most reliable path for extended family visits in 2026.

Plan Ahead Financially:

Rising LICO levels mean families should budget early for both the Parent Super Visa Insurance Plan in Canada and the overall hosting costs to stay within compliance and avoid last-minute surprises.

Canadian LIC Can Help:

As experienced advisors, Canadian LIC assists families in securing compliant Super Visa Insurance Coverage, ensuring all Super Visa Insurance requirements are met while comparing policies for affordability and protection.

Feedback Questionnaire:

We’d love to hear from you!

These quick questions help us understand what challenges Canadians are facing under the new 2026 Super Visa rules and how Canadian LIC can better guide families like yours.

Thank you for sharing your thoughts.

Your feedback helps Canadian LIC create more accurate, practical, and supportive resources for families preparing under the 2026 Super Visa and Family Sponsorship rules.

IN THIS ARTICLE

- New 2026 Super Visa & Family Sponsorship Rules: What Higher Income Thresholds Mean for Canadians

- Why The Higher Income Thresholds Matter

- Counting Family Members Correctly

- Connection To The Parents And Grandparents Program

- Health Insurance: The Non-Negotiable Requirement

- Estimating Super Visa Insurance Costs

- The Host’s Responsibilities

- How To Meet The Minimum Income Requirements

- Application Process: Step-by-Step

- What If You Don’t Meet The Threshold?

- Impact On Parents And Grandparents

- Practical Tips From Canadian LIC

- Why Canadian LIC Supports The New Standards

- Final Insights

Sign-in to CanadianLIC

Verify OTP